|

시장보고서

상품코드

1848172

광학 3차원 측정기 : 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Optical Coordinate Measuring Machine - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

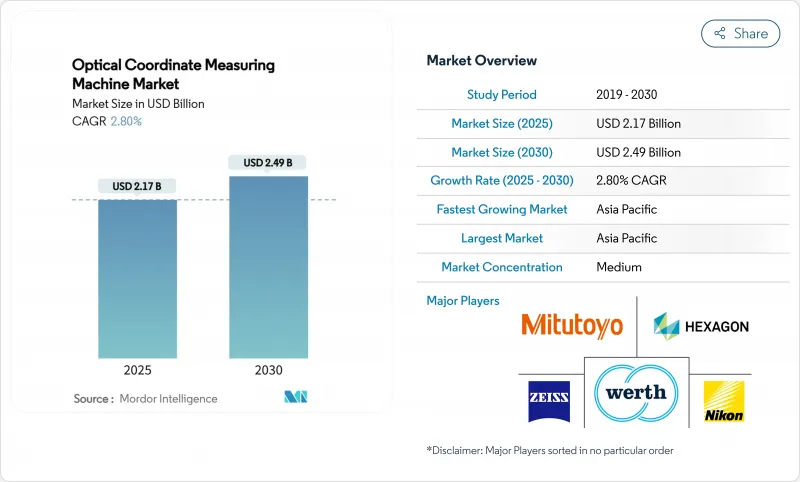

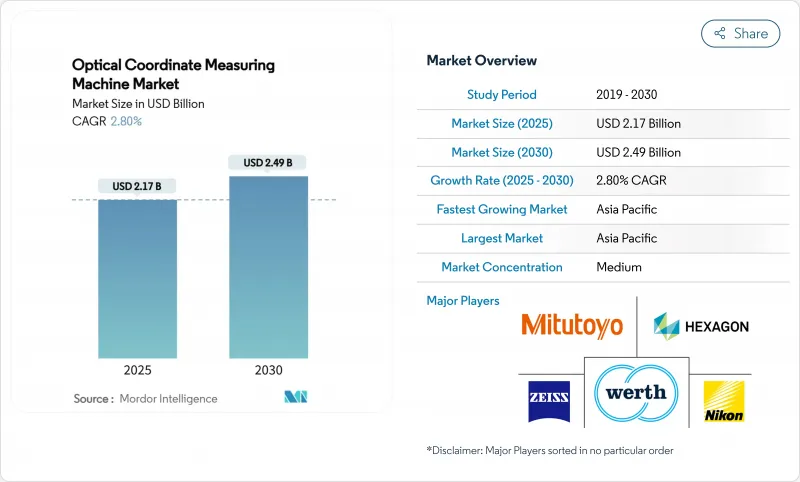

광학 3차원 측정기 시장 규모는 2025년에 21억 7,000만 달러로 평가되었고, 2030년에는 24억 9,000만 달러에 이를 것으로 예측되며, 기간 중 CAGR은 2.80%를 나타낼 전망입니다.

인더스트리 프로그램이 실시간 치수 데이터를 요구함에 따라 측정 실험실에서 생산 라인으로의 도입이 확대되고 있습니다. 자동차 전동화, 항공우주 복합재 사용, 의료기기 맞춤화는 시장 성숙에도 불구하고 수요를 안정적으로 유지합니다. 구조광 및 AI 강화 3D 비전 시스템은 속도와 정확도를 향상시켜 제조업체가 인력 확대 없이 무결점 목표를 달성할 수 있게 합니다. 아시아태평양 지역의 39.6% 매출 점유율은 이 지역이 세계 정밀 제조 허브로서의 역할을 강조하는 반면, 북미와 유럽은 규제 준수를 유지하기 위해 기술 갱신 주기를 추구하고 있습니다.

세계의 광학 3차원 측정기 시장 동향 및 인사이트

인더스트리 4.0의 제품 설계 변화

제조업체들은 제품 맞춤화와 경량화를 위해 기하학적 복잡성을 높이고 있으며, 이는 복잡한 표면을 신속하게 포착할 수 있는 비접촉식 측정 솔루션 수요를 촉진합니다. 광학식 CMM 공급업체들은 이제 사이버-물리 인터페이스를 내장하여 치수 데이터를 제조 실행 시스템에 직접 공급합니다. 구조광과 레이저 스캐닝을 결합한 다중 센서 플랫폼은 설정 시간을 최대 40% 단축하여 자동차 및 정밀 기계 공장에서 높이 평가받고 있습니다. 실시간 통합은 고밀도 포인트 클라우드 데이터가 시뮬레이션 정확도를 향상시키므로 디지털 트윈 이니셔티브를 지원합니다. 이러한 기능들은 기업들이 경쟁력을 유지하기 위해 접촉식 장비를 교체함에 따라 광학 3차원 측정기 시장이 더 빠른 교체 주기로 나아가도록 촉진합니다.

인라인 검사 및 자동화 채택

자동차 및 전자제품 제조업체들은 탈락 결함 제거를 위해 100% 검사를 목표로 합니다. 광학 센서가 장착된 협동 로봇은 생산 라인 옆에서 무인 측정을 제공하여 검사 주기 시간을 75% 단축하고 기술자 부족 문제를 완화합니다. 머신러닝 소프트웨어는 치수 편차를 예측하여 작업자가 불량 발생 전에 공정을 수정할 수 있게 합니다. 초기 도입 기업들은 2년 이내에 프리미엄 장비 비용을 상쇄할 수 있는 재료 절감 효과를 보고하며, 이는 광학 3차원 측정기 시장의 자본 지출 결정을 강화합니다.

높은 자본 지출과 TCO

30,000달러에서 250,000달러까지의 시스템 가격은 중소 제조업체의 도입 장벽이 됩니다. 시설 업그레이드, 교정, 유지보수 비용이 추가되면 총소유비용은 두 배로 증가합니다. 불량품 및 재작업 비용 절감 효과를 정량화하면 경제적 타당성이 개선되지만, 여전히 많은 관리자들이 주저하여 광학 3차원 측정기 시장의 비용 민감 지역에서 교체 주기가 지연되고 있습니다.

부문 분석

3D 비전 기계는 단일 촬영 표면 캡처 기술이 복잡한 형상 검사를 가속화함에 따라 2024년 매출 점유율 43.1%를 차지했습니다. 구조광 플랫폼은 규모는 작지만 반사 표면 성능이 개선되면서 2030년까지 연평균 3.9% 성장률을 기록할 것으로 전망됩니다. 레이저 스캐닝 장치는 미크론 단위 정밀도보다 측정 범위가 더 중요한 차체 본체 측정 분야에서 여전히 선호됩니다.

다중 센서 설계는 접촉식 및 광학 방식을 결합하여 사용자에게 다양한 부품을 위한 단일 스테이션을 제공함으로써 활용률을 높이고 광학 3차원 측정기 시장 내 광범위한 채택을 지원합니다. 소프트웨어 기반 AI 알고리즘은 이제 가변 조명 환경을 극복하기 위해 노출 및 패턴 투사를 제어하여 구조광 방식의 매력을 더욱 높입니다. 2D 비전 기계는 깊이 캡처에 한계가 있지만, Z축 데이터가 불필요한 고속 전자 부품 검사 분야에서 계속 활용되고 있습니다.

브릿지 설계는 열적 안정성, 서브마이크론 정확도, 자동 팔레트 적재를 결합하여 2024년 40.7%의 시장 점유율을 확보했습니다. 연평균 성장률(CAGR) 4.0%로 성장 중인 휴대용 벤치탑 기계는 생산 라인 근처에서 현장 검증을 가능하게 하여 부품 이송 시간을 단축합니다. 갠트리 모델은 초대형 항공우주 패널을 검사하며, 관절식 암은 내부 공동 접근을 지원합니다.

수평 암 변형 모델은 자동차 도장 공장에서 스탬핑 바디 검사에 활용되며, 확장된 작업 반경과 컨베이어 통합의 이점을 제공합니다. 브릿지 시스템은 제조업체가 작업장 환경(+/-5°C) 인증을 획득하며 새로운 활력을 얻어, HVAC 비용을 절감하고 비용 효율성을 중시하는 구매자 사이에서 광학 3차원 측정기 시장 규모를 확대합니다. 코보틱스 혁신은 휴대용 장치에 무인 운영 기능을 추가하여 중견 공급업체에게 새로운 수익원을 창출합니다.

광학 좌표 측정기 시장은 제품 유형(다중 센서, 2D 비전 측정기 등), 기계 유형(브릿지, 갠트리 등), 구성 요소(하드웨어, 소프트웨어, 서비스), 측정 용적 범위(소형, 중형, 대형), 최종 사용자 산업(항공우주 및 방위, 자동차 등), 지역별로 세분화됩니다. 시장 전망은 가치(USD) 기준으로 제공됩니다.

지역 분석

아시아태평양의 2024년 매출은 39.6%를 차지하고 2030년까지의 CAGR은 3.6%가 될 것으로 예상되며 중국의 반도체 장치 건설과 일본의 정밀 기계 수출이 주도합니다. 아시아태평양의 이점은 전자, 자동차 및 공작기계공급망이 밀집되어 있기 때문입니다. 메이드 인 차이나 2025와 같은 정부 프로그램은 스마트 제조 업그레이드를 장려하고 비접촉 측정을 공장 자동화 보조금에 필수적인 것으로 삼고 있습니다. 일본의 Tier-one은 전기자동차 부품의 수출을 지원하기 위해 AI 구동 소프트웨어를 탑재한 브릿지 유형의 기계의 리프레시를 계속하고 있습니다.

북미 시장은 항공우주, 정형외과용 임플란트, 다품종 적층조형이 중심이 되고 있습니다. 이 지역은 다변량 데이터 분석과 규제 추적성을 중시하고 소프트웨어 중심의 조달 결정을 뒷받침하고 있습니다. FDA와 FAA 가이드라인은 검증된 측정 시스템에 대한 수요를 강화하고, 광학 3차원 측정기 시장은 수량이 감소했음에도 불구하고 활기를 유지하고 있습니다.

유럽에서는 자동차 및 풍력에너지 분야에서 지속가능성과 제로 결함 생산이 중요합니다. 독일 공장에서는 스탬핑 라인에 코봇 탑재 3D 비전 헤드를 도입하여 3℃의 변동 하에서 작업 현장의 회복력을 실증하고 있습니다. 프랑스와 이탈리아는 중견 정밀 기계 가공 회사에 휴대용 벤치탑을 채택하여 광학 계측에 대한 지역적 접근을 확대했습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

목차

제1장 서론

- 조사의 전제조건과 시장의 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 인더스트리 4.0 환경에서의 제품 설계 변화

- 인라인 검사 및 자동화 도입

- 경량 복합재 부품에 필요한 광학 계측 기술

- 고정밀 적층 제조 수요 증가

- 첫 번째 제품 검사(FAI)에 대한 규제 강화

- 인공지능 기반 오차 보정 알고리즘

- 시장 성장 억제요인

- 높은 자본 지출 및 총소유비용(TCO)

- 숙련된 계측 인력 부족

- 작업 현장의 환경 민감성

- 사이버 보안 및 지적 재산 유출 우려

- 밸류체인 분석

- 기술의 전망

- 규제 상황

- Porter's Five Forces 분석

- 공급기업의 협상력

- 구매자의 협상력

- 신규 참가업체의 위협

- 대체품의 위협

- 경쟁 기업간 경쟁 관계

- 거시 경제 요인이 시장에 미치는 영향

제5장 시장 규모와 성장 예측

- 제품 유형별

- 다중 센서

- 2D 비전 측정기

- 3D 비전 측정기

- 레이저 주사형 광학 CMM

- 구조화 광광학 CMM

- 기종별

- 브릿지

- 갠트리

- 관절식 암

- 수평

- 휴대용 벤치 탑

- 컴포넌트별

- 하드웨어

- 소프트웨어

- 서비스

- 측정 범위별

- 소(500mm 이하)

- 중(500-2000mm)

- 대(2000mm 초과)

- 최종 사용자 업계별

- 항공우주 및 방위

- 자동차

- 의료기기 및 정형외과

- 중장비 및 금속가공

- 전자 및 반도체

- 에너지와 발전

- 기타 최종 사용자 산업

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 남미

- 브라질

- 아르헨티나

- 칠레

- 기타 남미

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 기타 유럽

- 아시아태평양

- 중국

- 일본

- 인도

- 한국

- 호주

- 싱가포르

- 말레이시아

- 기타 아시아태평양

- 중동 및 아프리카

- 중동

- 사우디아라비아

- 아랍에미리트(UAE)

- 튀르키예

- 기타 중동

- 아프리카

- 남아프리카

- 나이지리아

- 기타 아프리카

- 북미

제6장 경쟁 구도

- 시장 집중도

- 전략적 동향

- 시장 점유율 분석

- 기업 프로파일

- Hexagon AB

- Carl Zeiss AG

- Mitutoyo Corp.

- Nikon Metrology NV

- Werth Messtechnik GmbH

- OGP(Quality Vision International, Inc.)

- Micro-Vu Corp.

- Keyence Corp.

- Renishaw plc

- FARO Technologies Inc.

- Creaform Inc.(AMETEK)

- Perceptron Inc.(Atlas Copco)

- LK Metrology Ltd.

- Coord3 Srl

- Automated Precision Inc.(API)

- Wenzel Group GmbH and Co. KG

- Vision Engineering Ltd.

- Metronor AS

- Helmel Engineering Products Inc.

- Aberlink Ltd.

- InspecVision Ltd.

- Innovative Optical Measuring Systems(IOMS)

제7장 시장 기회와 장래의 전망

HBR 25.11.12The optical coordinate measuring machine market size is USD 2.17 billion in 2025 and is forecast to reach USD 2.49 billion in 2030, reflecting a 2.80% CAGR over the period.

Adoption is moving from metrology labs to production lines as Industry 4.0 programs demand dimensional data in real time. Automotive electrification, aerospace composite usage, and medical-device personalization keep demand steady despite the market's maturity. Structured-light and AI-enhanced 3D vision systems are improving speed and accuracy, which allows manufacturers to meet zero-defect goals without expanding headcount. Asia-Pacific's 39.6% revenue share underscores the region's role as the world's precision-manufacturing hub, while North America and Europe pursue technology refresh cycles to maintain regulatory compliance.

Global Optical Coordinate Measuring Machine Market Trends and Insights

Changing Product Designs in Industry 4.0

Manufacturers are increasing geometric complexity to personalize products and reduce weight, which drives demand for non-contact measurement solutions that can capture intricate surfaces quickly. Optical CMM suppliers now embed cyber-physical interfaces so dimensional data feeds directly into manufacturing-execution systems. Multi-sensor platforms that blend structured light and laser scanning shorten set-up time by up to 40%, a benefit valued by automotive and precision-machinery plants. Real-time integration supports digital-twin initiatives, since dense point-cloud data improves simulation accuracy. These capabilities push the optical coordinate measuring machine market toward faster refresh cycles as firms replace tactile equipment to stay competitive.

Adoption of In-line Inspection and Automation

Automotive and electronics producers target 100% inspection to eliminate escape defects. Collaborative robots equipped with optical sensors provide unattended measurements beside the production line, cutting inspection cycle times by 75% and mitigating technician shortages. Machine-learning software predicts dimensional drift, allowing operators to correct processes before scrap occurs. Early adopters report material savings that justify premium equipment costs within two years, reinforcing capital-expenditure decisions in the optical coordinate measuring machine market.

High Capital Expenditure and TCO

System prices ranging from USD 30,000 to USD 250,000 create adoption hurdles for small manufacturers. The total cost of ownership doubles when facility upgrades, calibration, and maintenance are added. Economic justification improves when scrap and rework savings are quantified, yet many managers still hesitate, slowing replacement cycles in cost-sensitive regions of the optical coordinate measuring machine market.

Other drivers and restraints analyzed in the detailed report include:

- Lightweight Composite Metrology

- High-precision Additive Manufacturing Demand

- Lack of Skilled Metrology Workforce

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

3D vision machines held 43.1% revenue share in 2024 because single-shot surface capture accelerates complex geometry inspection. Structured-light platforms, though smaller, are forecast to post a 3.9% CAGR through 2030 as reflective-surface performance improves. Laser-scanning units remain popular for body-in-white measurement, where range outweighs micron-level accuracy.

Multi-sensor designs combine tactile and optical modes, giving users one station for diverse parts, which elevates utilization rates and supports broader adoption within the optical coordinate measuring machine market. Software-driven AI algorithms now guide exposure and pattern projection to overcome variable lighting, further boosting structured-light appeal. 2D vision machines, although limited in depth capture, continue to serve high-speed electronic-component checks where z-axis data is unnecessary.

Bridge designs secured 40.7% market share in 2024 by blending thermal stability, sub-micron accuracy, and automated pallet loading. Portable benchtop machines, rising at a 4.0% CAGR, enable spot verification near production lines, reducing part-transfer times. Gantry models inspect very large aerospace panels, while articulated arms aid access to internal cavities.

Horizontal-arm variants serve stamped-body inspection in automotive paint shops, benefiting from extended reach and conveyor integration. Bridge systems gain new life as vendors certify them for +-5 °C shop-floor environments, cutting HVAC costs and broadening the optical coordinate measuring machine market size among cost-conscious buyers. Cobotic innovations add unattended operation capabilities to portable units, opening new revenue streams for mid-tier suppliers.

Optical Coordinate Measuring Machine Market is Segmented by Product Type (Multi-Sensor, 2D Vision Measurement Machine, and More), Machine Type (Bridge, Gantry, and More), Component (Hardware, Software, and Services), Measurement Volume Range (Small, Medium, and Large), End-User Industry (Aerospace and Defense, Automotive, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific accounted for 39.6% revenue in 2024 and is expected to post a 3.6% CAGR through 2030, led by China's semiconductor equipment build-out and Japan's precision machinery exports. Asia-Pacific's dominance stems from dense electronics, automotive, and machine-tool supply chains. Government programs such as Made in China 2025 incentivize smart-manufacturing upgrades, making non-contact metrology integral to factory-automation grants. Japanese tier-ones continue to refresh bridge-type machines with AI-driven software to support electric-vehicle component exports, while Korean battery makers install in-line structured-light scanners to verify prismatic cell cases.

North America's market revolves around aerospace, orthopedic implants, and high-mix additive manufacturing. The region values multivariate data analytics and regulatory traceability, driving software-centric procurement decisions. FDA and FAA guidelines reinforce demand for validated measurement systems, keeping the optical coordinate measuring machine market vibrant despite lower unit volumes.

Europe emphasizes sustainability and zero-defect production in the automotive and wind-energy sectors. German factories deploy cobot-mounted 3D vision heads on stamping lines, demonstrating shop-floor resilience under +-3 °C fluctuations. France and Italy adopt portable benchtops to serve midsized precision-machining firms that cannot justify granite-bed infrastructure, broadening regional access to optical metrology.

- Hexagon AB

- Carl Zeiss AG

- Mitutoyo Corp.

- Nikon Metrology NV

- Werth Messtechnik GmbH

- OGP (Quality Vision International, Inc.)

- Micro-Vu Corp.

- Keyence Corp.

- Renishaw plc

- FARO Technologies Inc.

- Creaform Inc. (AMETEK)

- Perceptron Inc. (Atlas Copco)

- LK Metrology Ltd.

- Coord3 S.r.l.

- Automated Precision Inc. (API)

- Wenzel Group GmbH and Co. KG

- Vision Engineering Ltd.

- Metronor AS

- Helmel Engineering Products Inc.

- Aberlink Ltd.

- InspecVision Ltd.

- Innovative Optical Measuring Systems (IOMS)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Changing product designs in Industry 4.0

- 4.2.2 Adoption of in-line inspection and automation

- 4.2.3 Lightweight composite parts require optical metrology

- 4.2.4 High-precision additive manufacturing demand

- 4.2.5 Regulatory push for first-article inspection

- 4.2.6 AI-driven error-compensation algorithms

- 4.3 Market Restraints

- 4.3.1 High capital expenditure and TCO

- 4.3.2 Lack of skilled metrology workforce

- 4.3.3 Environmental sensitivity on shop-floor

- 4.3.4 Cyber-security and IP-leakage concerns

- 4.4 Value Chain Analysis

- 4.5 Technological Outlook

- 4.6 Regulatory Landscape

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Impact of Macroeconomic Factors on the Market

5 MARKET SIZE AND GROWTH FORECASTS (VALUES)

- 5.1 By Product Type

- 5.1.1 Multi-sensor

- 5.1.2 2D Vision Measurement Machine

- 5.1.3 3D Vision Measurement Machine

- 5.1.4 Laser Scanning Optical CMM

- 5.1.5 Structured-light Optical CMM

- 5.2 By Machine Type

- 5.2.1 Bridge

- 5.2.2 Gantry

- 5.2.3 Articulated Arm

- 5.2.4 Horizontal

- 5.2.5 Portable Benchtop

- 5.3 By Component

- 5.3.1 Hardware

- 5.3.2 Software

- 5.3.3 Services

- 5.4 By Measurement Volume Range

- 5.4.1 Small (<= 500 mm)

- 5.4.2 Medium (500-2 000 mm)

- 5.4.3 Large (> 2 000 mm)

- 5.5 By End-user Industry

- 5.5.1 Aerospace and Defense

- 5.5.2 Automotive

- 5.5.3 Medical Device and Orthopedics

- 5.5.4 Heavy Machinery and Metal Fabrication

- 5.5.5 Electronics and Semiconductor

- 5.5.6 Energy and Power Generation

- 5.5.7 Other End-user Industries

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 South America

- 5.6.2.1 Brazil

- 5.6.2.2 Argentina

- 5.6.2.3 Chile

- 5.6.2.4 Rest of South America

- 5.6.3 Europe

- 5.6.3.1 Germany

- 5.6.3.2 United Kingdom

- 5.6.3.3 France

- 5.6.3.4 Italy

- 5.6.3.5 Spain

- 5.6.3.6 Rest of Europe

- 5.6.4 Asia-Pacific

- 5.6.4.1 China

- 5.6.4.2 Japan

- 5.6.4.3 India

- 5.6.4.4 South Korea

- 5.6.4.5 Australia

- 5.6.4.6 Singapore

- 5.6.4.7 Malaysia

- 5.6.4.8 Rest of Asia-Pacific

- 5.6.5 Middle East and Africa

- 5.6.5.1 Middle East

- 5.6.5.1.1 Saudi Arabia

- 5.6.5.1.2 United Arab Emirates

- 5.6.5.1.3 Turkey

- 5.6.5.1.4 Rest of Middle East

- 5.6.5.2 Africa

- 5.6.5.2.1 South Africa

- 5.6.5.2.2 Nigeria

- 5.6.5.2.3 Rest of Africa

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Hexagon AB

- 6.4.2 Carl Zeiss AG

- 6.4.3 Mitutoyo Corp.

- 6.4.4 Nikon Metrology NV

- 6.4.5 Werth Messtechnik GmbH

- 6.4.6 OGP (Quality Vision International, Inc.)

- 6.4.7 Micro-Vu Corp.

- 6.4.8 Keyence Corp.

- 6.4.9 Renishaw plc

- 6.4.10 FARO Technologies Inc.

- 6.4.11 Creaform Inc. (AMETEK)

- 6.4.12 Perceptron Inc. (Atlas Copco)

- 6.4.13 LK Metrology Ltd.

- 6.4.14 Coord3 S.r.l.

- 6.4.15 Automated Precision Inc. (API)

- 6.4.16 Wenzel Group GmbH and Co. KG

- 6.4.17 Vision Engineering Ltd.

- 6.4.18 Metronor AS

- 6.4.19 Helmel Engineering Products Inc.

- 6.4.20 Aberlink Ltd.

- 6.4.21 InspecVision Ltd.

- 6.4.22 Innovative Optical Measuring Systems (IOMS)

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment