|

시장보고서

상품코드

1848288

천장 타일 : 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Ceiling Tiles - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

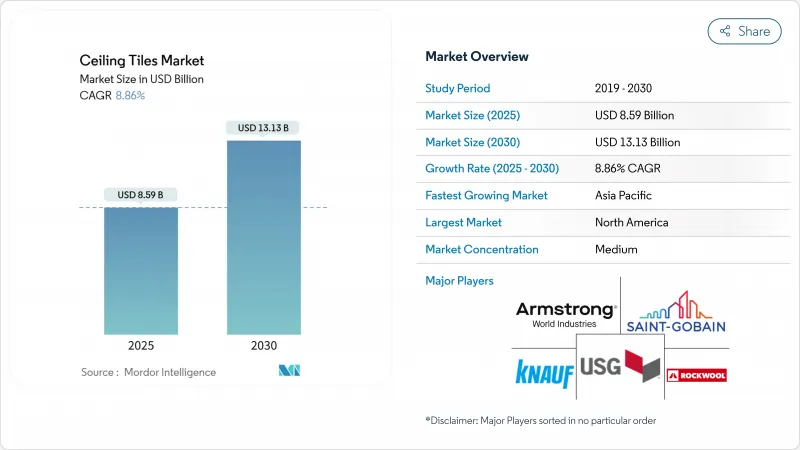

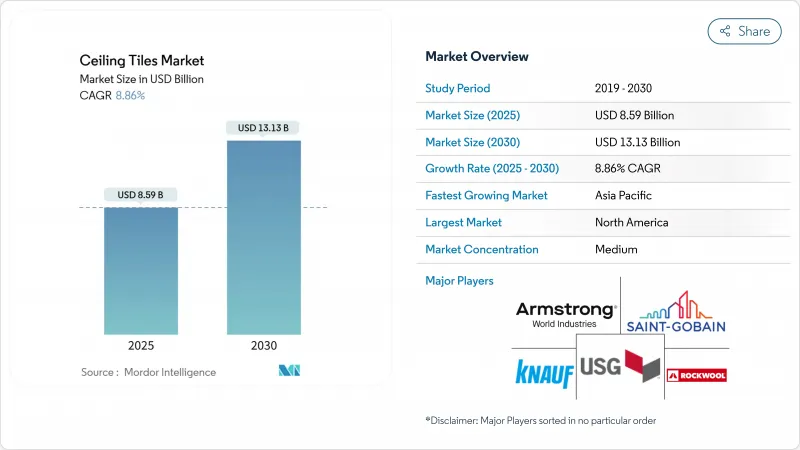

천장 타일 시장 규모는 2025년에 85억 9,000만 달러로 평가되었고, 예측 기간(2025-2030년)의 CAGR은 8.86%를 나타낼 것으로 예측되며, 2030년에는 131억 3,000만 달러에 달할 전망입니다.

강화되는 소음 규제, 에너지 효율을 목표로 한 리모델링 프로그램 확대, 그리고 급속한 도시 교통망 발전은 상업용 및 주거용 천장 시스템에 지속적인 투자를 이끌고 있습니다. 상변화물질(PCM) 패널과 저탄소 함유 미네랄울 보드 같은 에너지 중심 혁신 기술은 이제 미적 요소만큼이나 구매 결정에 영향을 미칩니다. 업계 선도 기업들은 순환경제 약속을 최우선 과제로 삼고 있으며, 검증된 재활용 체계가 입찰 평가에서 중요성을 더해가고 있습니다. 한편, 중국에서 주거용 천장 높이를 높이는 추세와 걸프 지역 고급 프로젝트에서 프리미엄 디지털 프린트 석고 타일의 사용이 확대되면서 시장 규모가 넓어지고 있어 천장 타일 시장의 장기적 전망이 강화되고 있습니다.

세계의 천장 타일 시장 동향 및 인사이트

북미 및 유럽 전역의 오픈 플랜 사무실에서 음향 천장 시스템의 급속한 도입

오픈 플랜 오피스 레이아웃은 신규 기업 인테리어를 주도하지만, 배경 소음으로 인해 측정된 직원 집중 시간이 66% 감소했습니다. 음향적 쾌적성을 회복하기 위해 기업들은 소음 감소 계수(NRC) 0.90 이상의 미네랄울 및 유리섬유 패널을 설치하고 있습니다. 암스트롱 소나타(Sonata) 및 할시온(Halcyon) 보드는 이러한 등급을 충족하면서도 매끄러운 화이트 미학을 유지합니다. 기술 및 금융 기업들이 도입을 주도하는 이유는 직원 유지 평가에서 음향적 프라이버시가 정신 건강과 연결되기 때문입니다. 구매팀은 또한 허들룸과 콜센터에 높은 천장 감쇠 등급을 지정하여 천장 타일 시장의 주문량을 가속화하고 있습니다.

유럽 그린빌딩 인증, 미네랄울 타일 개조 수요 촉진

BREEAM 및 DGNB 프레임워크는 우수한 음향 성능과 재활용 함량 모두에 대해 프리미엄 포인트를 부여합니다. 따라서 30-70%의 재생 섬유를 함유한 미네랄울 타일은 이중 크레딧을 획득하여 2024년 개정된 EU 건물 에너지 성능 지침(EPBD) 하에서 점수 프로필을 높입니다. 재활용 재료가 50% 이상 포함된 서틴티드(CertainTeed) 미네랄울 보드는 외관 및 HVAC 리모델링 시 선호되는 교체용 제품으로 자리 잡았으며, 프로젝트 소유주가 구조적 개조 없이도 의무화된 에너지 기준을 충족할 수 있게 합니다.

에너지 가격 변동성으로 미네랄울 비용 상승

미네랄울 생산은 1,450°C 이상의 용광로 온도에 의존하므로, 천연가스 및 전기 요금 급등으로 2024년 유럽 생산라인의 투입 비용이 최대 40% 상승했습니다. ROCKWOOL은 미시시피에 열회수 루프를 최적화하는 1억 달러 규모의 에너지 효율 시설을 건설해 대응했으나, 단기적인 가격 전가 옵션은 여전히 제한적입니다. 높은 견적 가격으로 인해 설계자들이 금속 또는 복합 보드로 대체하는 경향이 증가하면서 천장 타일 시장의 미네랄울 출하량이 일시적으로 감소하고 있습니다.

부문 분석

미네랄울은 2024년 천장 타일 시장 점유율의 41%로 가장 큰 비중을 차지했으며, 이는 동급 최고의 흡음성과 불연성에 기반합니다. 프로젝트 관리자들은 소음 및 화재 규정이 엄격한 사무실, 교실, 의료 시설 복도에 이를 정기적으로 선택합니다. 그러나 에너지 비용 변동과 내재 탄소량에 대한 관심이 높아지면서 제조업체들은 혁신을 강요받고 있습니다. 내재 탄소량을 43% 절감한 Ultima LEC 보드는 미네랄울 공급업체들이 지속가능성을 중심으로 어떻게 재포지셔닝하고 있는지 보여줍니다.

금속 패널은 교통 및 고급 소매 프로젝트에서 인지도를 확보하며 2030년까지 연평균 8.99% 성장률을 보일 전망입니다. 이들은 엄격한 화염 확산 제한을 충족하며, 음향과 공기 순환 요구사항을 균형 있게 조정하는 복잡한 천공 패턴을 수용합니다. 통합 재활용 가능성은 순환 경제 목표를 추가로 지원하여 성장세를 강화합니다. 복합재 및 바이오 기반 하이브리드 제품은 틈새 역할을 하지만 천장 타일 시장에서 미래 저탄소 소재 과학을 위한 실험실 역할을 제공합니다.

지역 분석

북미는 성숙한 지붕 교체 주기, 엄격한 음향 규정, 음향 제어 수요를 증폭시키는 오픈 플랜 사무실 문화에 힘입어 2024년 매출 점유율 35%로 천장 타일 시장을 주도했습니다. 에너지 효율 개조를 위한 연방 인센티브는 공공 부문 건물 전반에 걸쳐 미네랄울 및 PCM 패널의 지속적인 채택을 지원합니다. 대형 기존 업체들은 국내 생산 기지를 유지하여 운송 변동성을 최소화하고 유통업체에 신속한 서비스를 보장합니다.

유럽은 국가 에너지 효율 계획 하의 엄격한 친환경 건축 프레임워크와 리모델링 보조금으로 인해 근소한 차이로 뒤를 이었습니다. 미네랄울의 높은 재활용 함량은 BREEAM 및 DGNB 인증 기준과 완벽히 부합하여 에너지 가격 변동성에도 불구하고 꾸준한 주문 흐름을 유지하고 있습니다. 유럽 대륙의 건설사들은 또한 수명이 다한 타일을 재활용하는 ‘Rockcycle’ 프로그램과 같은 순환형 회수 방안을 시범 운영 중이며, 이는 천장 타일 시장의 지속가능성 신뢰도를 강화하고 있습니다.

아시아태평양 지역은 공항, 지하철, 복합용도 타워를 아우르는 메가 프로젝트 파이프라인을 바탕으로 2025년부터 2030년까지 연평균 10.5%의 성장률을 기록하며 가장 빠르게 성장하는 시장입니다. 중국이 주거용 천장 높이를 3m로 표준화하도록 지시함에 따라 표면적 요구 사항이 확대되고 있으며, 인도의 지하철 확장으로 A급 방화 등급 금속 보드에 대한 기회가 증가하고 있습니다. 그러나 현지 가격 민감도와 뿌리 깊은 석고보드(POP) 관행은 수입 석고 타일에게 경쟁적 도전 과제를 제기합니다. 한편, 걸프협력회의(GCC) 국가들은 디자인 중심의 프리미엄 솔루션을 추구하며, 중동 럭셔리 시장을 천장 타일 시장 내 고마진 클러스터로 부각시키고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

목차

제1장 서론

- 조사의 전제조건과 시장의 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 북미 및 유럽 전역의 오픈 플랜 사무실에서 음향 천장 시스템의 급속한 도입

- 유럽의 친환경 건축 크레딧 제도가 촉진하는 미네랄울 타일 교체 수요

- 아시아 지하철 및 공항 건설에서 불연성 천장 타일 의무화

- 천장 타일 제조용 원자재 가공 과정에서의 탄소 영향 감소

- 중동 고급 부동산 시장에서 프리미엄화를 가능케 하는 디지털 프린팅 석고 타일

- 시장 성장 억제요인

- 에너지 가격 변동성으로 인한 미네랄울 원가 상승

- 아스팔트 및 모르타르 등 대체재의 위협

- 아시아태평양 지역에서 석고 타일 채택을 제한하는 저비용 POP 가천장

- 밸류체인 분석

- Porter's Five Forces 분석

- 공급기업의 협상력

- 구매자의 협상력

- 신규 참가업체의 위협

- 대체품의 위협

- 경쟁도

제5장 시장 규모와 성장 예측

- 원재료별

- 미네랄울

- 금속

- 석고

- 기타(복합재, 플라스틱, 목재)

- 성질별

- 음향

- 비음향

- 용도별

- 주거용

- 상업용

- 산업용

- 공공 공익 기관

- 지역별

- 아시아태평양

- 중국

- 인도

- 일본

- 한국

- ASEAN 국가

- 기타 아시아태평양

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 북유럽 국가

- 기타 유럽

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 중동 및 아프리카

- 사우디아라비아

- 아랍에미리트(UAE)

- 남아프리카

- 나이지리아

- 기타 중동 및 아프리카

- 아시아태평양

제6장 경쟁 구도

- 시장 집중도

- 전략적 동향

- 시장 점유율 분석

- 기업 프로파일

- AWI Licensing LLC

- Foshan Ron Building Material Trading

- Georgia-Pacific

- Guangzhou Titan Building Materials Co., Ltd.

- Haining Shamrock Import & Export Co. Ltd.

- Hunter Douglas NV

- Imerys

- Kingspan Group

- Knauf Group

- Mada Gypsum Company

- New Ceiling Tiles LLC

- Odenwald Faserplattenwerk GmbH

- PVC Ceilings SA

- ROCKWOOL A/S

- Saint-Gobain

- SAS International

- Shandong Huamei Building Materials Co., Ltd.

- Techno Ceiling Products

- USG Corporation

제7장 시장 기회와 장래의 전망

HBR 25.11.12The Ceiling Tiles Market size is estimated at USD 8.59 billion in 2025, and is expected to reach USD 13.13 billion by 2030, at a CAGR of 8.86% during the forecast period (2025-2030).

Intensifying acoustic regulations, expanding retrofit programs aimed at energy efficiency, and rapid urban transport development continue to draw sustained investment into commercial and residential ceiling systems. Energy-focused innovations such as Phase Change Material (PCM) panels and low-embodied-carbon mineral wool boards now influence procurement decisions as much as aesthetics. Segment leaders are prioritizing circularity commitments, with verified recycling schemes gaining weight in bid evaluations. Meanwhile, the shift toward taller residential ceilings in China and premium digital-print gypsum tiles in Gulf luxury projects is broadening the addressable base, strengthening the long-term outlook for the ceiling tiles market.

Global Ceiling Tiles Market Trends and Insights

Rapid adoption of acoustic ceiling systems in open-plan offices across North America & Europe

Open-plan layouts dominate new corporate fit-outs, yet background chatter cuts measured employee focus time by 66%. To restore acoustic comfort, enterprises are installing mineral-wool and fiberglass panels with Noise Reduction Coefficient values above 0.90. Armstrong Sonata and Halcyon boards match these ratings while retaining a seamless white aesthetic. Technology and financial firms lead deployments because staff retention reviews now link acoustic privacy with mental wellness. Procurement teams are also specifying high Ceiling Attenuation Class for huddle rooms and call centers, accelerating order volumes in the ceiling tiles market.

Europe green-building credits accelerating mineral-wool tile retrofit demand

BREEAM and DGNB frameworks grant premium points for both acoustic excellence and recycled content. Mineral wool tiles that contain 30-70% reclaimed fibers therefore earn double credit, lifting their score profiles under the EU Energy Performance of Buildings Directive update of 2024. CertainTeed mineral wool boards, comprising more than 50% recycled material, have become a preferred drop-in during facade and HVAC refurbishments, allowing project owners to meet mandated energy thresholds without structural overhaul.

Energy-price volatility inflating mineral-wool costs

Mineral wool production relies on furnace temperatures above 1,450 °C, so spikes in natural-gas and electricity tariffs have lifted input costs by up to 40% for European lines in 2024. ROCKWOOL responded with a USD 100 million energy-efficient facility in Mississippi that optimizes heat-recovery loops, but near-term price pass-through options remain limited. Higher quote values encourage specifiers to substitute toward metal or composite boards, temporarily softening mineral-wool shipments in the ceiling tiles market.

Other drivers and restraints analyzed in the detailed report include:

- Asian metro & airport build-outs mandating non-combustible ceiling tiles

- Reduced carbon impacts in processing of raw materials for manufacturing ceiling tiles

- Threat of substitutes, such as asphalt and mortar

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Mineral wool held the largest portion of the ceiling tiles market share at 41% in 2024, anchored by its class-leading acoustic absorption and non-combustibility. Project managers routinely select it for offices, classrooms, and healthcare corridors where both sound and fire codes are strict. Yet energy cost swings and embodied-carbon scrutiny are pressuring manufacturers to innovate. Ultima LEC boards that cut embodied carbon by 43% demonstrate how mineral-wool suppliers are repositioning around sustainability.

Metal panels are capturing mindshare in transport and prestige retail projects, advancing at an 8.99% CAGR to 2030. They satisfy stringent flame-spread limits and accept complex perforation patterns that balance acoustics and air-return requirements. Integral recyclability streams additionally support circular-economy targets, reinforcing their rise. Composite and bio-based hybrids occupy niche roles but provide laboratories for future low-carbon material science in the ceiling tiles market.

The Ceiling Tiles Market Report Segments the Industry by Raw Material (Mineral Wool, Metal, Gypsum, and Others), Property (Acoustic and Non-Acoustic), Application (Residential, Commercial, Industrial, and Institutional), and Geography (Asia-Pacific, North America, Europe, South America, and Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America led the ceiling tiles market with 35% revenue share in 2024, driven by a mature reroofing cycle, tight acoustic codes, and a culture of open-plan offices that amplifies sound-control needs. Federal incentives for energy-efficient retrofits support continued mineral-wool and PCM panel adoption across public-sector buildings. Large incumbents maintain domestic manufacturing bases, minimizing freight volatility and ensuring rapid service to distributors.

Europe follows closely, fueled by stringent green-building frameworks and refurbishment subsidies under national energy-performance plans. Mineral wool's high recycled content aligns neatly with BREEAM and DGNB credit metrics, fostering steady order flow despite energy-price volatility. Continental contractors are also trialing circular take-back schemes such as the Rockcycle program that reuses end-of-life tiles, reinforcing sustainability credentials in the ceiling tiles market.

Asia Pacific is the fastest-growing theatre, posting a 10.5% CAGR from 2025-2030 on the back of megaproject pipelines encompassing airports, metros, and mixed-use towers. China's directive to raise standard residential ceiling heights to 3 m expands surface area requirements, while India's metro expansion multiplies opportunities for Class A fire-rated metal boards. Yet local price sensitivity and entrenched POP practices pose competitive challenges for imported gypsum tiles. Elsewhere, GCC states pursue design-led premium solutions, highlighting Middle-East luxury as a distinct high-margin cluster within the ceiling tiles market.

- AWI Licensing LLC

- Foshan Ron Building Material Trading

- Georgia-Pacific

- Guangzhou Titan Building Materials Co., Ltd.

- Haining Shamrock Import & Export Co. Ltd.

- Hunter Douglas N.V.

- Imerys

- Kingspan Group

- Knauf Group

- Mada Gypsum Company

- New Ceiling Tiles LLC

- Odenwald Faserplattenwerk GmbH

- PVC Ceilings SA

- ROCKWOOL A/S

- Saint-Gobain

- SAS International

- Shandong Huamei Building Materials Co., Ltd.

- Techno Ceiling Products

- USG Corporation

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rapid adoption of acoustic ceiling systems in open-plan offices across North America and Europe

- 4.2.2 Europe green-building credits accelerating mineral-wool tile retrofit demand

- 4.2.3 Asian metro and airport build-outs mandating non-combustible ceiling tiles

- 4.2.4 Reduced Carbon Impacts in Processing of Raw Materials for Manufacturing Ceiling Tiles

- 4.2.5 Digital-print gypsum tiles enabling premiumisation in Middle-East luxury real estate

- 4.3 Market Restraints

- 4.3.1 Energy-price volatility inflating mineral-wool costs

- 4.3.2 Threat of Substitutes, such as Asphalt and Mortar

- 4.3.3 Low-cost POP false ceilings constraining gypsum tile uptake in Asia Pacific

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces Analysis

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Degree of Competition

5 Market Size and Growth Forecasts (Value)

- 5.1 By Raw Material

- 5.1.1 Mineral Wool

- 5.1.2 Metal

- 5.1.3 Gypsum

- 5.1.4 Others (Composite, Plastic and Wood)

- 5.2 By Property

- 5.2.1 Acoustic

- 5.2.2 Non-Acoustic

- 5.3 By Application

- 5.3.1 Residential

- 5.3.2 Commercial

- 5.3.3 Industrial

- 5.3.4 Institutional

- 5.4 By Geography

- 5.4.1 Asia Pacific

- 5.4.1.1 China

- 5.4.1.2 India

- 5.4.1.3 Japan

- 5.4.1.4 South Korea

- 5.4.1.5 ASEAN Countries

- 5.4.1.6 Rest of Asia Pacific

- 5.4.2 North America

- 5.4.2.1 United States

- 5.4.2.2 Canada

- 5.4.2.3 Mexico

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 France

- 5.4.3.4 Italy

- 5.4.3.5 Spain

- 5.4.3.6 Nordics

- 5.4.3.7 Rest of Europe

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Rest of South America

- 5.4.5 Middle East and Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 United Arab Emirates

- 5.4.5.3 South Africa

- 5.4.5.4 Nigeria

- 5.4.5.5 Rest of Middle East and Africa

- 5.4.1 Asia Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)}

- 6.4.1 AWI Licensing LLC

- 6.4.2 Foshan Ron Building Material Trading

- 6.4.3 Georgia-Pacific

- 6.4.4 Guangzhou Titan Building Materials Co., Ltd.

- 6.4.5 Haining Shamrock Import & Export Co. Ltd.

- 6.4.6 Hunter Douglas N.V.

- 6.4.7 Imerys

- 6.4.8 Kingspan Group

- 6.4.9 Knauf Group

- 6.4.10 Mada Gypsum Company

- 6.4.11 New Ceiling Tiles LLC

- 6.4.12 Odenwald Faserplattenwerk GmbH

- 6.4.13 PVC Ceilings SA

- 6.4.14 ROCKWOOL A/S

- 6.4.15 Saint-Gobain

- 6.4.16 SAS International

- 6.4.17 Shandong Huamei Building Materials Co., Ltd.

- 6.4.18 Techno Ceiling Products

- 6.4.19 USG Corporation

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment

- 7.2 Innovation in Gypsum Tiles for its Biodegradable Properties