|

시장보고서

상품코드

1848293

폴리이미드 필름 시장 : 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Polyimide Films - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

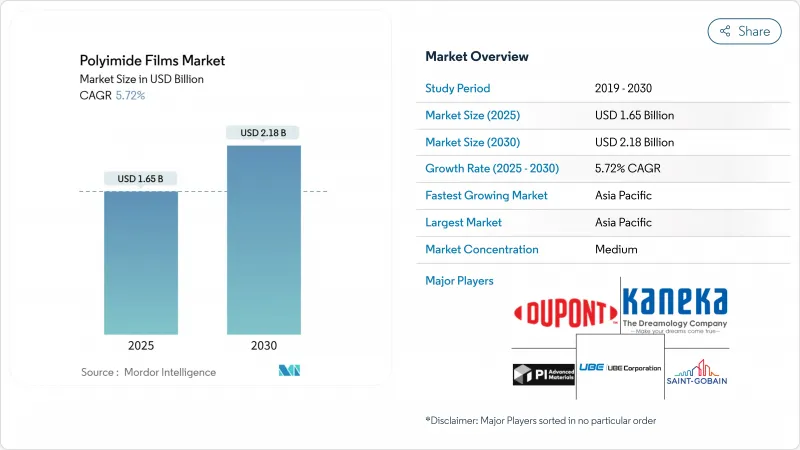

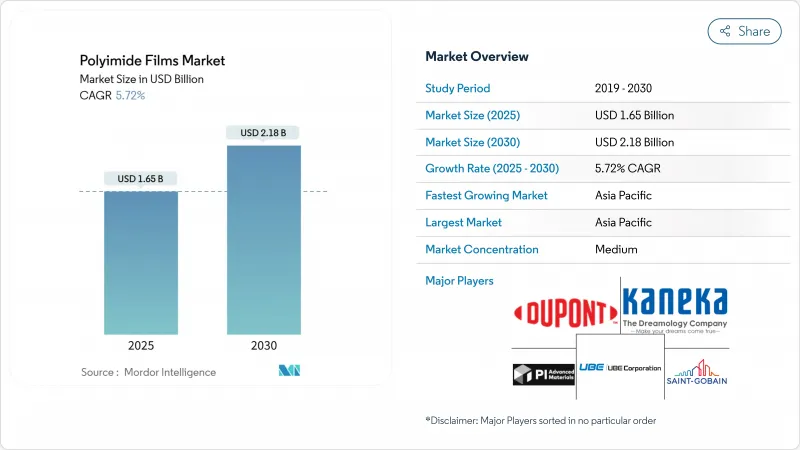

세계의 폴리이미드 필름 시장은 2025년에 16억 5,000만 달러로 추정되고, 2025-2030년 CAGR 5.72%로 성장할 전망이며, 2030년에는 21억 8,000만 달러에 달할 것으로 예측됩니다.

소형화된 컨슈머 일렉트로닉스, 전동화된 수송 수단, 고온의 항공우주용 일렉트로닉스가 수요의 주요 원동력이 되고 있습니다. 5G 인프라에 대한 지속적인 투자 및 SiC/GaN 파워 디바이스로의 전환은 고신뢰성 필름의 장기 소비를 강화합니다. 또한 PFAS 관련 규제 압력은 수지의 화학적 특성과 조달 패턴을 재구성할 수 있습니다.

세계의 폴리이미드 필름 시장 동향 및 인사이트

폴더블 디스플레이 및 롤 디스플레이가 무색 폴리이미드 필름의 보급 가속

스마트폰 제조업체가 2세대 폴더블 디바이스를 상품화함에 따라 반경 3mm 이하로 접을 수 있는 투명 기판에 대한 수요가 높아지고 있습니다. 컬러리스 기판은 450nm에서 85% 이상의 투과율을 실현하고, 100,000회 이상의 폴딩 사이클에서도 기계적 무결성을 유지하기 때문에 OEM는 초박형 유리의 대체품을 통합할 수 있어 힌지의 경량화도 실현할 수 있습니다. 한국 공급업체는 빛 열화를 억제하고 자동차 대시보드의 옥외 사용 수명을 연장하는 스타형 자외선 흡수제를 발표했습니다. 중국과 한국에서는 패널에 대한 투자가 계속되고 있으며 안정적인 공급량을 지원하고 있습니다. 또한 롤러블 TV용 파이프라인이 용도의 밑단을 넓히고 폴리이미드 필름 시장이 프리미엄 디스플레이 틈새로 확대되고 있습니다.

고밀도 EV 배터리 팩을 가능하게 하는 열전도성 폴리이미드 필름

800V 아키텍처로 전환하는 자동차 플랫폼에서는 보다 높은 열 부하가 발생하기 때문에 면내 열전도성을 향상시킨 얇은 전기 절연체가 필수적입니다. 흑연을 포함한 폴리이미드 라미네이트는 현재 200kV/mm 이상의 절연 파괴 강도를 유지하면서 0.5W/m*K에 가까운 열전도율을 제공하여 엄격한 안전 마진을 충족하고 있습니다. 북극곰에 힌트를 얻은 중공 SiO2 구조체의 조사에서는 한랭지에서의 폭주 위험을 경감하는 0.041W/m*K를 달성했습니다. 이러한 진보는 중국, 미국, 독일에서 적극적인 배터리 팩 고밀도화 프로그램을 지원하고 폴리이미드 필름 시장에 파워트레인의 밸류체인에서 확고한 발판을 제공합니다.

저비용 대체품 가용성

앰버 폴리이미드는 동등한 PEN 필름의 2배를 넘는 가격 프리미엄이 붙어 있습니다. Kaladex PEN의 기계적 RTI는 160℃이며 가전제품 및 표준 자동차 하네스에 적합합니다. 커패시터나 미드레인지의 플렉스 회로에서는 바이어는 열 마진을 부품 비용과 비교 검토하기 때문에 PEN의 경제성이 조달을 좌우하게 되어 왔습니다. 차세대 디스플레이 및 파워 디바이스의 성능이 다시 상승할 때까지 비용에 민감한 지역, 특히 동남아시아와 라틴아메리카에서는 고온 폴리에스테르의 연구개발이 강화되어 폴리이미드 필름 시장에서 수량이 떨어질 수 있습니다.

부문 분석

기존의 앰버 제품은 레거시 와이어 절연과 플렉스 회로의 강점을 살려 2024년 폴리이미드 필름 시장 점유율의 45%를 차지했습니다. 이 부문은 폴리이미드 필름 시장 규모의 최대 슬라이스를 구성하고 있지만, 새로운 케미스트리가 주목을 받고 있는 가운데, 그 성장률은 시장 평균보다 낮습니다. 무색 PI 폼 CAGR은 6.14%로 폴더블폰, 권선형 TV, 투명 터치 인터페이스의 채용 곡선을 타고 있습니다. 폴리이미드 필름 업계는 하이브리드 UV 컷 첨가제의 파이프라인을 눈에 띄게 해, 태양열에 의한 경년 열화로부터 백본을 보호하고, 한때 유리 커버 윈도우의 우위성을 지지하고 있던 성능 갭을 메웁니다.

열전도성 등급은 국부적인 핫스팟을 분산시키는 평면 절연 재료로 전기자동차 배터리에 공급되며 흑연 또는 세라믹 마이크로 필러가 평면 내 경로를 지원합니다. 불소 코팅이 적용된 등급은 산 안정성이 중요한 틈새 화학 처리 장치에 계속 사용됩니다. 2축 연신 필름은 그 분자 배열에 의해 0.1% 이내의 치수 재현성을 실현해, 항공우주용 센서의 굴곡에 여전히 선호되고 있습니다. 폴리이미드 필름 시장 규모에 차지하는 2축 연신 필름의 비율은 작지만, 그 초고 마진은 일본과 벨기에에서의 생산 능력 증강의 인센티브가 되고 있습니다. 모든 제품 유형에 걸친 기술 혁신은 폴리이미드 필름 시장의 탄력성을 지원합니다.

지역 분석

아시아태평양은 폴리이미드 필름 시장의 2024년 매출액의 44%를 차지하였고, 2030년까지 CAGR 6.00%로 성장이 예측됩니다. 중국 본토 패널 제조업체는 2025-2026년 플렉서블 OLED의 생산 능력을 확대하여 지역 소비를 지원합니다. 국내 수지 제조업체는 과거에는 호박색의 전기 등급에 한정되어 있었지만, 현재는 전자 등급의 폴리이미드를 타겟으로 하고 있어 수입 의존도를 낮추고 비용 경쟁력을 향상시키고 있습니다. 일본과 한국은 초청정반응기 및 다단용매회수시스템으로 리드를 유지해 고급 스마트폰 OEM이 요구하는 일관된 광학적 투명성을 가능하게 하고 있습니다. 인도는 전자기기 수탁제조의 중심지로 부상하고, 플렉서블 기판에 대한 현지에서의 인계를 확대하는 외국 직접 투자를 끌고 있습니다.

북미는 항공우주, 방위, 첨단 반도체 용도 분야에서 큰 점유율을 차지합니다. 듀퐁의 오하이오주 서클빌에서 2억 2,000만 달러의 확장은 하이엔드 캡턴과 피라룩스의 국내 공급을 강화하고 지정학적 공급 우려를 완화하며 국방부 프로그램의 리드타임을 단축시킵니다. 실리콘밸리 주변에 집적된 신흥기업은 MEMS 센서 어레이나 마이크로 LED 백플레인과의 폴리이미드 호환성을 이용하여 폴리이미드 필름 시장의 지역적 용도 범위를 넓히는 기술 혁신을 추진하고 있습니다.

유럽은 대륙의 자동차 및 재생에너지 장비에 구조적으로 지원되어 안정적인 산업 수요를 견인하고 있습니다. PFAS를 둘러싼 규제의 기운은 처방의 재설계를 가속화해, 현지공급자에게 그린 용제 시스템과 불소 프리모노머에 대한 투자를 촉구하고 있습니다. 이 적응 능력은 이 지역의 폴리이미드 필름 시장을 전반적인 축소로부터 보호하는 동시에 유사한 규제를 채택하는 다른 관할 구역에 환경 솔루션을 수출합니다. 남미와 중동 및 아프리카는 여전히 소규모 최종 시장이지만, 브라질의 전자 클러스터의 싹트고 걸프 방위 위성 계획은 수요 증가를 가져옵니다. 이 지역에서는 수입에 의존하는 공급 모델이 주류이지만, 합작 투자에 관한 협의는 현지 컨버팅 사업으로의 전환이 점차 진행되고 있음을 보여줍니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월의 애널리스트 서포트

목차

제1장 서론

- 조사의 전제조건 및 시장의 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 폴더블 및 롤러블 디스플레이가 무색 폴리이미드 필름의 보급 가속

- 고밀도 EV 배터리 팩을 실현하는 열전도성 폴리이미드 필름

- 내방사선성 폴리이미드 절연체를 필요로 하는 위성 '신우주' 전자기기

- 5G 인프라 확장

- 항공우주 분야에서 고온 SiC/GaN 파워 일렉트로닉스로의 이행

- 시장 성장 억제요인

- 저비용 대체품의 가용성

- 이미드화 및 용매회수라인에 대한 고액의 설비 투자

- 폴리이미드 등급에 영향을 미치는 PFAS 단계적 폐지 규제

- 밸류체인 분석

- Porter's Five Forces

- 공급기업의 협상력

- 구매자의 협상력

- 신규 참가업체의 위협

- 대체품의 위협

- 경쟁 기업 간 경쟁 관계

제5장 시장 규모 및 성장 예측

- 제품 유형별

- 기존(앰버) PI 필름

- 무색 PI 필름

- 불소 코팅 PI 필름

- 열전도성 및 흑연 충전 PI 필름

- 2축 연신 PI 필름

- 용도별

- 플렉서블 프린트 기판(FPCB)

- 특수가공제품

- 감압 테이프

- 전선 및 케이블

- 모터 및 제너레이터

- 최종 이용 산업별

- 일렉트로닉스

- 자동차

- 항공우주

- 라벨링

- 기타 최종 사용자 산업

- 지역별

- 아시아태평양

- 중국

- 일본

- 한국

- 인도

- 기타 아시아태평양

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 기타 유럽

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 중동 및 아프리카

- 사우디아라비아

- 남아프리카

- 기타 중동 및 아프리카

- 아시아태평양

제6장 경쟁 구도

- 시장 집중도

- 전략적 움직임(합병 및 인수, 합작 사업, 생산 능력의 증강)

- 시장 점유율 분석

- 기업 프로파일

- 3M

- AGC Inc.

- Arakawa Chemical Industries,Ltd.

- DuPont

- IST Corporation

- KANEKA CORPORATION

- Kolon Industries, Inc.

- Mitsui Chemicals, Inc.

- PI Advanced Materials Co., Ltd.

- Saint-Gobain

- Taimide Tech. Inc.

- TORAY INDUSTRIES, INC.

- UBE Corporation

- Von Roll

- Wuhan Imide New Materials Technology Co.,LTD

- Zhejiang Hecheng Smart Electric Co., Ltd.

제7장 시장 기회 및 향후 전망

AJY 25.11.03The global polyimide films market reached USD 1.65 billion in 2025 and is projected to advance to USD 2.18 billion by 2030, reflecting a 5.72% CAGR over 2025-2030.

Miniaturized consumer electronics, electrified transportation, and high-temperature aerospace electronics are the principal engines of demand, while colorless formulations unlock opportunities in foldable displays. Persistent investment in 5G infrastructure and the transition toward SiC/GaN power devices reinforce long-term consumption of high-reliability films. Supply security remains a strategic issue because capacity additions lag the speed at which downstream sectors scale, and PFAS-related regulatory pressures could realign resin chemistry and sourcing patterns.

Global Polyimide Films Market Trends and Insights

Foldable and rollable displays accelerating colorless polyimide film uptake

Demand for transparent substrates that can fold below a 3 mm radius has intensified as smartphone makers commercialize second-generation foldable devices. Colorless substrates deliver more than 85% transmittance at 450 nm and retain mechanical integrity for more than 100,000 folding cycles, allowing original-equipment makers to integrate ultra-thin glass alternatives while achieving lighter hinges. Korean suppliers have introduced star-shaped UV absorbers that inhibit photodegradation and extend outdoor service life in automotive dashboards. Ongoing panel investments across China and South Korea underpin steady offtake, and the pipeline for rollable televisions is widening the application base, ensuring the polyimide films market continues to expand into premium display niches.

Thermally-conductive polyimide films enabling high-density EV battery packs

Vehicle platforms transitioning to 800 V architectures generate higher heat loads, making thin electrical isolators with enhanced in-plane thermal conductivity indispensable. Graphite-laden polyimide laminates now offer thermal conductivities approaching 0.5 W/m*K while sustaining dielectric breakdown strengths above 200 kV/mm, satisfying stringent safety margins. Research into polar-bear-inspired hollow SiO2 constructs achieved 0.041 W/m*K to mitigate cold-climate runaway risk. These advances support aggressive battery-pack densification programs in China, the United States, and Germany, giving the polyimide films market a solid foothold in power-train value chains.

Availability of low-cost substitutes

Amber polyimide commands a price premium that can exceed 2X comparable PEN films. Kaladex PEN delivers a mechanical RTI of 160 °C, adequate for consumer appliances and standard automotive harnesses. In capacitors and mid-range flex circuits, buyers weigh thermal margins against component cost, and PEN's economics increasingly sway procurement. Intensified research and development into higher-temperature polyester variants could peel volume away from the polyimide films market in cost-sensitive regions, particularly Southeast Asia and Latin America, until next-generation displays and power devices lift performance thresholds again.

Other drivers and restraints analyzed in the detailed report include:

- Satellite New-Space electronics requiring radiation-hard polyimide insulators

- Expansion of 5G infrastructure

- PFAS-phase-out regulations affecting polyimide grades

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Conventional amber products generated 45% of polyimide films market share in 2024 on the strength of legacy wire insulation and flex circuitry. The segment constitutes the largest slice of polyimide films market size, yet its growth rate stays below the market average as newer chemistries capture attention. Colorless PI Form are on track for a 6.14% CAGR, riding the adoption curve in folding phones, rollable televisions, and transparent touch interfaces. The polyimide films industry witnesses a pipeline of hybrid UV-blocking additives that protect the backbone against solar aging, closing performance gaps that once anchored glass cover-window dominance.

Thermally-conductive grades supply electric-vehicle batteries with planar insulation that distributes localized hotspots, supported by graphite or ceramic micro-fillers for in-plane pathways. Fluorine-coated variants continue to serve niche chemical-processing equipment where acid stability is decisive. Biaxially stretched films, whose molecular alignment delivers dimensional repeatability within 0.1%, remain favored for aerospace sensor flexes. Although they hold a smaller slice of polyimide films market size, their ultra-high margins incentivize capacity additions in Japan and Belgium. Collective innovation across all product types sustains the resilience of the broader polyimide films market.

The Polyimide Film Market Report Segments the Industry by Product Type (Conventional PI Film, Colorless PI Film, and More), Application (Flexible Printed Circuit Boards, Specialty Fabricated Products, and More), End-Use Industry (Electronics, Automotive, Aerospace, and More), and Geography (Asia-Pacific, North America, Europe, South America, and Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific generated 44% of 2024 revenue for the polyimide films market and is projected to deliver a 6.00% CAGR through 2030. Mainland Chinese panel makers expand flexible OLED capacity during 2025-2026, underpinning regional consumption. Domestic resin suppliers, once confined to amber electrical grades, now target electronic-grade polyimide, narrowing import reliance and improving cost competitiveness. Japan and South Korea maintain a lead in ultra-clean reactors and multi-stage solvent-recovery systems, enabling consistent optical clarity demanded by premium smartphone OEMs. India emerges as a focal point for contract electronics manufacturing, drawing foreign direct investment that enlarges local pull for flexible substrates.

North America holds a prominent share attributable to aerospace, defense, and advanced semiconductor applications. DuPont's USD 220 million expansion in Circleville, Ohio deepens domestic supply of high-end Kapton and Pyralux variants, mitigating geopolitical supply concerns and shortening lead times for Department of Defense programs. Start-ups clustered around Silicon Valley exploit polyimide's compatibility with MEMS sensor arrays and micro-LED backplanes, injecting innovation that broadens the regional application canvas within the polyimide films market.

Europe commands stable industrial demand, structurally underpinned by continental automotive and renewable-energy equipment. Regulatory momentum around PFAS accelerates formulation redesign, prompting local suppliers to invest in green solvent systems and fluorine-free monomers. This adaptive capacity shields the regional polyimide films market from outright contraction while exporting environmental solutions to other jurisdictions adopting similar restrictions. South America and the Middle East and Africa remain smaller end-markets, yet Brazil's budding electronics clusters and Gulf defense satellite programs seed incremental demand. Import-reliant supply models dominate these regions, though joint-venture talks indicate gradual movement toward local converting operations.

- 3M

- AGC Inc.

- Arakawa Chemical Industries,Ltd.

- DuPont

- I.S.T Corporation

- KANEKA CORPORATION

- Kolon Industries, Inc.

- Mitsui Chemicals, Inc.

- PI Advanced Materials Co., Ltd.

- Saint-Gobain

- Taimide Tech. Inc.

- TORAY INDUSTRIES, INC.

- UBE Corporation

- Von Roll

- Wuhan Imide New Materials Technology Co.,LTD

- Zhejiang Hecheng Smart Electric Co., Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Foldable and Rollable Displays Accelerating Colorless PolyImide Film Uptake

- 4.2.2 Thermally-Conductive Poly Imide Films Enabling High-Density EV Battery Packs

- 4.2.3 Satellite "New-Space" Electronics Requiring Radiation-Hard Poly Imide Insulators

- 4.2.4 Expansion of 5G infrastructure

- 4.2.5 Shift to High-Temperature SiC/GaN Power Electronics in Aerospace

- 4.3 Market Restraints

- 4.3.1 Availability of low-cost substitutes

- 4.3.2 High CapEx for Imidisation and Solvent-Recovery Lines

- 4.3.3 PFAS-Phase-out Regulations Affecting Poly Imide Grades

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Competitive Rivalry

5 Market Size and Growth Forecasts (Value)

- 5.1 By Product Type

- 5.1.1 Conventional (Amber) PI Film

- 5.1.2 Colorless PI Film

- 5.1.3 Fluorine-Coated PI Film

- 5.1.4 Thermally-Conductive/Graphite-Filled PI Film

- 5.1.5 Biaxially-Stretched PI Film

- 5.2 By Application

- 5.2.1 Flexible Printed Circuit Boards (FPCB)

- 5.2.2 Specialty Fabricated Products

- 5.2.3 Pressure Sensitive Tapes

- 5.2.4 Wire and Cable

- 5.2.5 Motor/Generator

- 5.3 By End-use Industry

- 5.3.1 Electronics

- 5.3.2 Automotive

- 5.3.3 Aerospace

- 5.3.4 Labelling

- 5.3.5 Other End-user Industries

- 5.4 By Geography

- 5.4.1 Asia-Pacific

- 5.4.1.1 China

- 5.4.1.2 Japan

- 5.4.1.3 South Korea

- 5.4.1.4 India

- 5.4.1.5 Rest of Asia-Pacific

- 5.4.2 North America

- 5.4.2.1 United States

- 5.4.2.2 Canada

- 5.4.2.3 Mexico

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 France

- 5.4.3.4 Italy

- 5.4.3.5 Rest of Europe

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Rest of South America

- 5.4.5 Middle East and Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 South Africa

- 5.4.5.3 Rest of Middle East and Africa

- 5.4.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves (Mergers and Acquisitions, JVs, Capacity Adds)

- 6.3 Market Share Analysis

- 6.4 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)}

- 6.4.1 3M

- 6.4.2 AGC Inc.

- 6.4.3 Arakawa Chemical Industries,Ltd.

- 6.4.4 DuPont

- 6.4.5 I.S.T Corporation

- 6.4.6 KANEKA CORPORATION

- 6.4.7 Kolon Industries, Inc.

- 6.4.8 Mitsui Chemicals, Inc.

- 6.4.9 PI Advanced Materials Co., Ltd.

- 6.4.10 Saint-Gobain

- 6.4.11 Taimide Tech. Inc.

- 6.4.12 TORAY INDUSTRIES, INC.

- 6.4.13 UBE Corporation

- 6.4.14 Von Roll

- 6.4.15 Wuhan Imide New Materials Technology Co.,LTD

- 6.4.16 Zhejiang Hecheng Smart Electric Co., Ltd.

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-need Assessment

- 7.2 Increased Research and Development in aerospace and space tech