|

시장보고서

상품코드

1848294

유럽의 메디컬 에스테틱 기기 시장 : 시장 점유율 분석, 산업 동향 및 통계, 성장 예측(2025-2030년)Europe Medical Aesthetic Devices - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

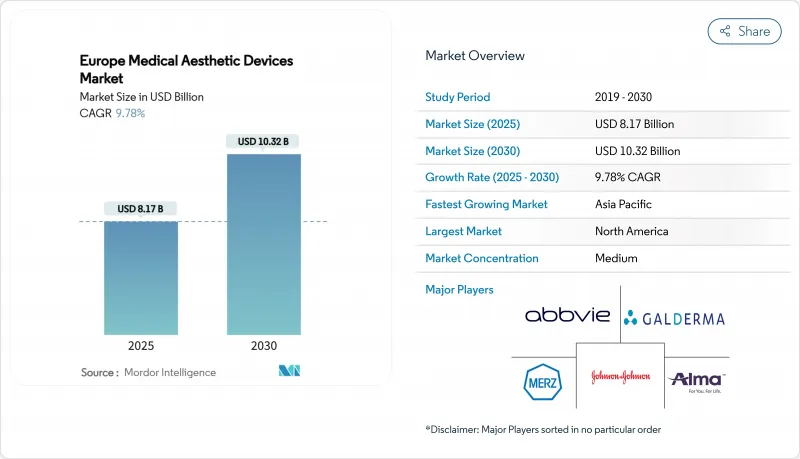

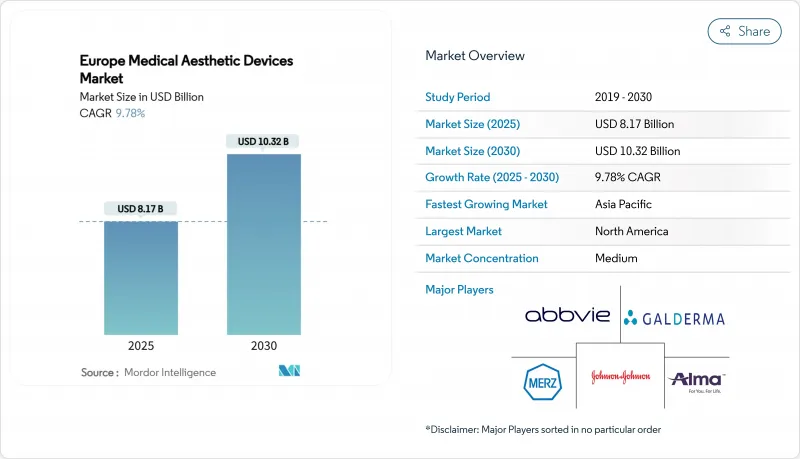

유럽의 메디컬 에스테틱 기기 시장 규모는 2025년에 81억 7,000만 달러로 추정되고, 2030년에는 103억 2,000만 달러에 이를 것으로 예측되며, 예측 기간 중 CAGR 9.78%로 성장이 전망됩니다.

확립된 헬스케어 에코시스템, 엄격하지만 투명성이 높은 유럽연합 의료기기 규제(MDR) 규칙, 저침습 미용 케어로의 소비자 시프트의 확산이 결합되어, 종래의 기기 카테고리를 항상 웃도는 성장 프로파일이 형성되고 있습니다. 에너지 기반 플랫폼은 여전히 유럽의 메디컬 에스테틱 기기 시장의 중심이지만, 주사기와 실의 지속적인 제품 업데이트 사이클이 경쟁 영역을 넓히고 있습니다. 프라이빗 에쿼티 자본이 확장 가능한 서비스 모델을 대상으로 하므로 공급업체와 클리닉 체인의 통합이 진행되고 있습니다. 한편, 국경을 넘은 의료 관광, 특히 쉥겐 협정 회원국 내에서의 의료 관광은 수술 후 후속 케어에서의 격차를 드러내면서도, 유럽의 컴플라이언스에 준거한 의료 제공업체에 대한 품질 프리미엄을 강화하고 있습니다.

유럽의 메디컬 에스테틱 기기 시장 동향 및 인사이트

비만률 상승

EU의 일부 국가에서는 성인 비만률이 25%를 넘어 바디 콘투어링과 셀룰라이트 제거 기술에 대한 수요가 높아지고 있습니다. 독일에서는 2011-2024년 에너지 기반 지방 감소 치료의 수가 190.5% 증가했으며, 이 변화는 고주파 및 크라이오리폴라이시스 시스템의 보급과 밀접한 관련이 있습니다. 치료원은 비외과적 치료에 체중 관리 조언을 번들함으로써 이 인구 동태의 변화를 활용하여 미용과 마찬가지로 건강을 요구하는 환자에게 어필하고 있습니다. 독일과 프랑스는 또한 티켓이 높은 시술에 EU 안전 기준을 선호하는 유럽 내 의료 여행자들로부터 혜택을 받고 있습니다.

저침습 수술에 대한 수요 증가

가동 중지 시간 단축과 양호한 안전성 프로파일은 환자를 주사 및 장치 기반 치료로 계속 끌어들입니다. 국제미용형성외과학회(International Society of Aesthetic Plastic Surgery)의 보고에 따르면, 신경조절제 및 피부충전제의 시술은 유럽 전역에서 6년 연속 증가했습니다. 장비 제조업체 각 회사는 고주파와 펄스 라이트를 한 번에 결합할 수 있는 멀티 모달 에너지 시스템을 전개함으로써 대응하며, 비외과적 툴킷의 폭을 넓히고 있습니다. 메디컬 스파는 야간 및 주말 예약이 가능하며 시간에 쫓기는 전문가를 만족시키기 위해 이 트래픽의 큰 점유율을 획득하고 있습니다.

선택적 조치를 위한 제한된 환불

공공 의료 제도가 선택적 에스테틱 케어에 적용되는 경우는 거의 없으며 환자는 자비 치료를 강요합니다. 이러한 움직임은 특히 북유럽에서는 독립개업의가 청구할 수 있는 가격에 스스로 상한을 마련해 클리닉이 직접 제공하는 할부 플랜의 보급을 촉진하고 있습니다. 장비 제조업체는 임대 및 수익 공유 모델을 제공하여 신규 참가자의 자금 장애물을 낮춤으로써 대응합니다.

부문 분석

에너지 기반 시스템은 2024년 매출의 52.56%를 차지했으며, 광범위한 적응증을 대상으로 하는 레이저, 고주파, HIFU 플랫폼을 배경으로 유럽 최대의 메디컬 에스테틱 기기 시장 점유율을 확보했습니다. 레이저의 하위 부문은 다운타임을 최소화하면서 효과를 유지하는 분수 모드와 하이브리드 모드로 진화하고 있으며, 클리닉의 반복 비즈니스 모델을 지원합니다. 이와 병행하여, 고주파 치료기는 온도 제어된 핸드피스를 활용하여 표피에 손상을 주지 않고 신생 콜라겐 생성을 촉진하고 피츠 패트릭 피부 점수가 높은 환자에게 어필하고 있습니다. 비에너지 툴의 유럽 메디컬 에스테틱 기기 시장 규모는 현재 작지만 차세대 신경조절제 및 가교 히알루론산 필러와 관련된 CAGR 11.67%로 급속한 확대가 전망되고 있습니다. Galderma의 Relfydess와 같은 즉시 사용할 수 있는 보툴리눔툭신(보톡스)액은 예측 가능한 용량과 빠른 회전 시간을 제공하며, 이는 대량의 진료를 하는 클리닉에서 공명하는 이점입니다. 마이크로다마 브레이젼과 같은 기계적 옵션은 엔트리 레벨 서비스로서의 비계를 유지하며 새로운 스레드 리프트 소재는 인장 강도와 수명을 향상시킵니다.

2차적인 시프트로서 휴대용 프랙셔널 레이저 헤드가 출현하고 있습니다. 공급업체는 또한 재활용 가능한 카트리지에서 장비 수명을 연장하는 소프트웨어 업데이트에 이르기까지 서유럽 규제의 환경 우선순위를 반영하여 지속가능성 기능에 대한 관심이 높아지고 있다고 보고합니다. 이러한 진보를 종합하면 에너지 플랫폼의 우위성이 유지되는 한편, 비에너지 대체 기기가 가격 경쟁이 아닌 기술 혁신에 의해 보조를 맞추어 가게 됩니다.

비외과적 치료법은 2024년 매출의 55.87%를 차지했으며, 유럽 전역에서 미용의 첫 선택으로서의 역할을 확고히 하고 있습니다. 초음파와 광학 가이던스의 통합으로 수술자는 밀리미터 단위의 정확도로 피하층을 타겟팅할 수 있게 되었고, 치료 성적이 향상되었기 때문에 현재 많은 환자들이 입문 수준의 수술을 완전히 생략할 수 있게 되었습니다. 뉴로모듈레이터와 프랙셔널 RF와 같은 조합 패키지는 더 적은 방문 횟수로 다각적인 회춘을 제공하며 환자 만족도 점수 및 클리닉 가동률 지표에 반영됩니다. 가격 투명성과 회복 기간 단축은 유럽의 메디컬 에스테틱 기기 시장에서 비외과적 수술의 점유율을 더욱 지원합니다.

수술은 절대 규모는 작지만 침습이 적은 기술이 됨에 따라 CAGR 10.98%로 증가합니다. 예를 들어, 유방 확대술용 마이크로 텍스처의 실리콘 임플란트나 지방 유화를 효율화하는 에너지 지원 지방 흡입 장치 등을 들 수 있습니다. 외과의사는 수술 중에 에너지 기구를 채용하는 것이 늘고 있으며, 전통적인 절개 기술과 기구를 사용한 조직 관리를 융합시켜 치유를 가속화하고 있습니다. 그러나 비침습적인 효능이 향상됨에 따라 장비보다 수술을 선택하는 임계값은 계속 상승하고 있습니다.

유럽의 메디컬 에스테틱 기기 시장은 장비 유형별(에너지 기반 미용 장비 및 비에너지 기반 미용 장비), 용도별(피부 표면 마감 및 긴축, 바디 윤곽 및 셀룰라이트 제거, 탈모, 유방, 기타 용도), 최종 사용자별(병원, 클리닉 및 기타 최종 사용자), 지역별(영국, 독일, 프랑스, 이탈리아, 스페인 및 기타 유럽)로 구분됩니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월의 애널리스트 서포트

목차

제1장 서론

- 조사의 전제조건 및 시장의 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 비만률 상승

- 저침습 수술 수요 증가

- 미용기기의 급속한 기술 진보

- 고령화 및 가처분 소득 증가

- 프리미엄 디바이스를 장려하는 엄격한 유럽 규제 기준

- 유럽 내 메디컬 에스테틱 관광 확대

- 시장 성장 억제요인

- 선택적 치료에 대한 제한적인 상환

- 고액의 자본 비용 및 치료비

- 일회용 소모품에 관한 지속가능성에 대한 우려

- 신규 주입제에 관한 규제의 모호함

- 규제 상황

- Porter's Five Forces 분석

- 신규 참가업체의 위협

- 구매자의 협상력

- 공급기업의 협상력

- 대체품의 위협

- 경쟁 기업 간 경쟁 관계

제5장 시장 규모 및 성장 예측

- 장비 유형별

- 에너지 기반 미용 장비

- 레이저 미용 기기

- 고주파 미용 기기

- 라이트 기반 미용 기기

- 초음파 미용 기기

- 비에너지 기반 미용기기

- 보툴리눔툭신(보톡스)

- 피부 충전제 및 실

- 미세박피술

- 임플란트

- 기타 미용 기기

- 에너지 기반 미용 장비

- 처치 유형별

- 비외과적 및 저침습

- 외과적 수술

- 용도별

- 피부 재생 및 탄력

- 바디 컨투어링 및 셀룰라이트 제거

- 탈모

- 페이셜 에스테틱

- 유방 수술

- 기타 용도

- 최종 사용자별

- 병원

- 클리닉 및 피부과

- 메디컬 스파

- 홈 설정

- 국가별

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 기타 유럽

제6장 경쟁 구도

- 시장 집중도

- 시장 점유율 분석

- 기업 프로파일

- AbbVie Inc(Allergan Aesthetics)

- Galderma SA

- Johnson & Johnson(Mentor Worldwide LLC)

- Merz Pharma GmbH & Co. KGaA

- Sisram Medical(Alma Lasers)

- Lumenis Ltd

- Cutera Inc.

- Bausch Health(Solta Medical)

- Cynosure LLC(Hologic)

- Sciton Inc.

- Syneron Candela Medical

- Venus Concept Inc.

- InMode Ltd

- Fotona doo

- Sientra Inc.

- Human Med AG

- Aerolase Corp.

- Apyx Medical Corp.

- Straumann Group(botiss Biomaterials)

- Zimmer Biomet(Aesthetic Implants)

제7장 시장 기회 및 향후 전망

AJY 25.11.03The Europe medical aesthetic devices market size is USD 8.17 billion in 2025 and is forecast to reach USD 10.32 billion by 2030, advancing at a 9.78% CAGR over the period.

A well-established healthcare ecosystem, strict but transparent European Union Medical Device Regulation (MDR) rules and a widening consumer shift toward minimally invasive cosmetic care combine to create a growth profile that consistently outpaces traditional device categories. Energy-based platforms remain the anchor of the Europe medical aesthetic devices market, yet continuous product refresh cycles in injectables and threads are broadening the competitive field. Consolidation among suppliers and clinic chains is rising as private equity capital targets scalable service models. Meanwhile, cross-border medical tourism, especially within the Schengen area, reinforces the quality premium attached to compliant European providers even as it exposes gaps in postoperative follow-up care.

Europe Medical Aesthetic Devices Market Trends and Insights

Rising Obesity Prevalence

Adult obesity now tops 25% in several EU states, fueling demand for body-contouring and cellulite-reduction technologies. In Germany, the number of energy-based fat-reduction procedures climbed 190.5% between 2011 and 2024, a change closely linked to the uptake of radiofrequency and cryolipolysis systems. Clinics leverage this demographic shift by bundling weight-management advice with non-surgical treatments, appealing to patients seeking wellness as much as aesthetics. Germany and France also benefit from intra-European medical travelers who prefer EU safety standards for high-ticket procedures.

Growing Demand for Minimally Invasive Procedures

Reduced downtime and favorable safety profiles continue to pull patients toward injectable and device-based therapies. The International Society of Aesthetic Plastic Surgery reports that neuromodulator and dermal-filler sessions rose for a sixth straight year across Europe. Device makers respond by rolling out multi-modal energy systems able to combine radiofrequency with pulsed light in one pass, thereby widening the non-surgical toolkit. Medical spas capture a large share of this traffic because they can schedule evening and weekend appointments, satisfying time-pressed professionals.

Limited Reimbursement for Elective Procedures

Public health systems rarely cover elective esthetic care, leaving patients to self-finance treatments. This dynamic places a natural ceiling on price points that independent practitioners can charge, particularly in Northern Europe, and encourages the spread of installment payment plans offered directly by clinics. Device makers respond by offering lease and revenue-share models to lower capital hurdles for new entrants.

Other drivers and restraints analyzed in the detailed report include:

- Rapid Technological Advances in Aesthetic Devices

- Aging Population and Increasing Disposable Income

- High Capital and Treatment Costs

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Energy-based systems generated 52.56% of 2024 revenue, securing the largest Europe medical aesthetic devices market share on the back of lasers, radiofrequency and HIFU platforms that target a broad range of indications. Laser sub-segments are evolving toward fractional and hybrid modes that minimize downtime yet maintain efficacy, supporting repeat-business models for clinics. In parallel, radiofrequency devices leverage temperature-controlled handpieces to promote neocollagenesis without epidermal damage, appealing to patients with higher Fitzpatrick skin scores. The Europe medical aesthetic devices market size for non-energy tools is smaller today yet poised for faster expansion, with an 11.67% CAGR tied to next-generation neuromodulators and cross-linked hyaluronic-acid fillers. Ready-to-use botulinum toxin liquids such as Galderma's Relfydess offer predictable dosing and quicker turnover times, advantages that resonate in high-volume practices. Mechanical options like microdermabrasion retain a foothold as entry-level services, while newer thread-lift materials improve tensile strength and longevity.

A secondary shift is emerging toward portable fractional laser heads that lower space requirements and broaden mobile-clinic concepts in rural Europe. Suppliers also report rising interest in sustainability features, from recyclable cartridges to software updates that extend device lifespan, reflecting environmental priorities in Western European regulations. Collectively these advances preserve the dominance of energy platforms while ensuring non-energy alternatives keep pace through innovation rather than price competition.

Non-surgical modalities accounted for 55.87% of 2024 revenue, cementing their role as first-line aesthetic options across Europe. Integration of ultrasound and optical guidance lets operators target sub-dermal layers with millimetric precision, elevating outcomes so that many patients now skip entry-level surgery altogether. Combination packages-such as neuromodulators plus fractional RF-deliver multidimensional rejuvenation in fewer visits, a format that pays off in patient satisfaction scores and clinic occupancy metrics. Price transparency and shorter recovery windows further anchor non-surgical share within the Europe medical aesthetic devices market.

Surgical procedures, though smaller in absolute terms, will climb at a 10.98% CAGR as techniques become less invasive. Examples include micro-textured silicone implants for breast augmentation and energy-assisted liposuction devices that streamline fat emulsification. Surgeons increasingly adopt energy instruments intra-operatively, blending traditional cutting skills with device-based tissue management to speed healing. Collectively, the surgical arena retains its importance for clients seeking dramatic reshaping, but the threshold for choosing surgery over devices continues to rise as non-invasive efficacy improves.

The Europe Medical Aesthetic Devices Market is Segmented by Type of Devices (Energy-Based Aesthetic Devices and Non-Energy Based Aesthetic Devices), Application (Skin Resurfacing and Tightening, Body Contouring and Cellulite Reduction, Hair Removal, Breast Augmentation, and Other Applications), End-User (Hospitals, Clinics, and Other End-Users), and Geography (United Kingdom, Germany, France, Italy, Spain, and Rest of Europe).

List of Companies Covered in this Report:

- AbbVie Inc (Allergan Aesthetics)

- Galderma

- Johnson & Johnson (Mentor Worldwide LLC)

- Merz Pharma

- Sisram Medical

- Lumenis

- Cutera

- Bausch Health (Solta Medical)

- Cynosure LLC (Hologic)

- Sciton

- Syneron Candela Medical

- Venus Concept Inc.

- InMode Ltd

- Fotona d.o.o.

- Sientra

- Human Med

- Aerolase Corp.

- Apyx Medical Corp.

- Straumann Group (botiss Biomaterials)

- Zimmer Biomet (Aesthetic Implants)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Obesity Prevalence

- 4.2.2 Growing Demand for Minimally Invasive Procedures

- 4.2.3 Rapid Technological Advancements in Aesthetic Devices

- 4.2.4 Aging Population and Increasing Disposable Income

- 4.2.5 Stringent European Regulatory Standards Encouraging Premium Devices

- 4.2.6 Expansion of Medical Aesthetic Tourism Intra-Europe

- 4.3 Market Restraints

- 4.3.1 Limited Reimbursement for Elective Procedures

- 4.3.2 High Capital and Treatment Costs

- 4.3.3 Sustainability Concerns Over Single-Use Consumables

- 4.3.4 Regulatory Ambiguity for Novel Injectable Fillers

- 4.4 Regulatory Landscape

- 4.5 Porter's Five Forces Analysis

- 4.5.1 Threat Of New Entrants

- 4.5.2 Bargaining Power Of Buyers

- 4.5.3 Bargaining Power Of Suppliers

- 4.5.4 Threat Of Substitutes

- 4.5.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Type Of Device

- 5.1.1 Energy-Based Aesthetic Devices

- 5.1.1.1 Laser-Based Aesthetic Devices

- 5.1.1.2 Radiofrequency-Based Aesthetic Devices

- 5.1.1.3 Light-Based Aesthetic Devices

- 5.1.1.4 Ultrasound-Based Aesthetic Devices

- 5.1.2 Non-Energy-Based Aesthetic Devices

- 5.1.2.1 Botulinum Toxin

- 5.1.2.2 Dermal Fillers And Threads

- 5.1.2.3 Microdermabrasion

- 5.1.2.4 Implants

- 5.1.2.5 Other Aesthetic Devices

- 5.1.1 Energy-Based Aesthetic Devices

- 5.2 By Procedure Type

- 5.2.1 Non-Surgical / Minimally Invasive

- 5.2.2 Surgical

- 5.3 By Application

- 5.3.1 Skin Resurfacing And Tightening

- 5.3.2 Body Contouring And Cellulite Reduction

- 5.3.3 Hair Removal

- 5.3.4 Facial Aesthetic Procedures

- 5.3.5 Breast Augmentation

- 5.3.6 Other Applications

- 5.4 By End User

- 5.4.1 Hospitals

- 5.4.2 Clinics And Dermatology Offices

- 5.4.3 Medical Spas

- 5.4.4 Home Settings

- 5.5 By Country

- 5.5.1 Germany

- 5.5.2 United Kingdom

- 5.5.3 France

- 5.5.4 Italy

- 5.5.5 Spain

- 5.5.6 Rest of Europe

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and analysis of Recent Developments)

- 6.3.1 AbbVie Inc (Allergan Aesthetics)

- 6.3.2 Galderma SA

- 6.3.3 Johnson & Johnson (Mentor Worldwide LLC)

- 6.3.4 Merz Pharma GmbH & Co. KGaA

- 6.3.5 Sisram Medical (Alma Lasers)

- 6.3.6 Lumenis Ltd

- 6.3.7 Cutera Inc.

- 6.3.8 Bausch Health (Solta Medical)

- 6.3.9 Cynosure LLC (Hologic)

- 6.3.10 Sciton Inc.

- 6.3.11 Syneron Candela Medical

- 6.3.12 Venus Concept Inc.

- 6.3.13 InMode Ltd

- 6.3.14 Fotona d.o.o.

- 6.3.15 Sientra Inc.

- 6.3.16 Human Med AG

- 6.3.17 Aerolase Corp.

- 6.3.18 Apyx Medical Corp.

- 6.3.19 Straumann Group (botiss Biomaterials)

- 6.3.20 Zimmer Biomet (Aesthetic Implants)

7 Market Opportunities & Future Outlook

- 7.1 White-Space & Unmet-Need Assessment