|

시장보고서

상품코드

1848299

동반진단 시장 : 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Companion Diagnostics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

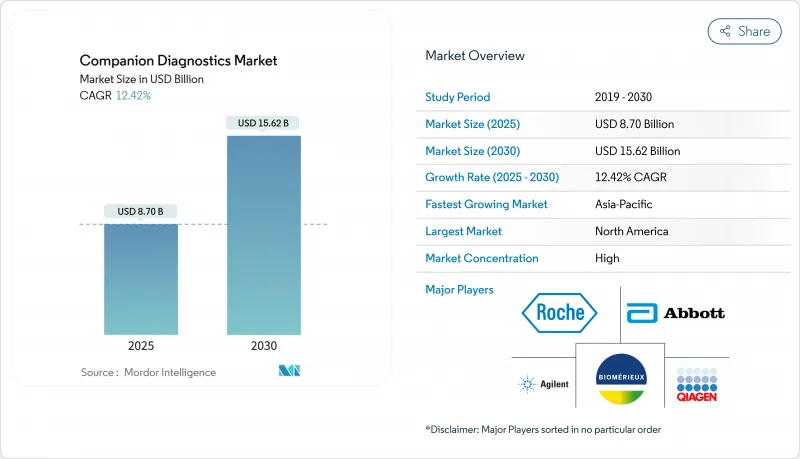

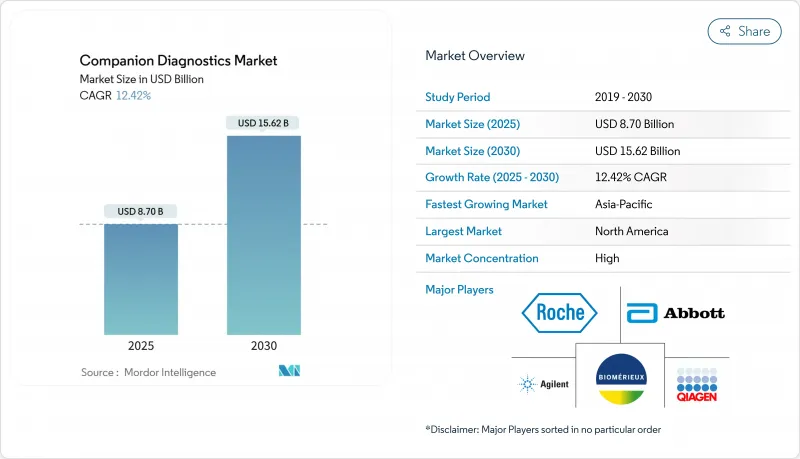

동반진단 시장 규모는 2025년 87억 달러로 추정되고, CAGR 12.42%로 성장할 전망이며, 2030년에는 156억 2,000만 달러로 확대될 것으로 예측됩니다.

동반진단 분자 검사와 표적 치료제를 통합하여 진단 정보와 최적의 치료법 선택을 일치시킵니다. Precision Medicine의 용도 분야는 의약품 제조업체의 투자 우선순위를 동시에 시프트시키고 정책 입안자가 진단을 매우 중요한 비용 억제 도구로 인식함에 따라 지불자의 상환 모델을 재구성하고 있습니다.

세계의 동반진단 시장 동향 및 인사이트

종양 진료에서 리퀴드 바이옵시 CDx의 급속한 보급

리퀴드 바이옵시 동반진단든 종양 불균일성을 실시간으로 파악하는 저침습 반복 검사 경로를 제공함으로써 암 관리를 재정의하고 있습니다. 임상의는 현재 순환하는 종양 DNA를 통해 질병의 진화를 추적하고 정적 조직 스냅샷에 의존하지 않고 동적으로 치료를 조절할 수 있습니다. 2차 영향으로, 병원의 실험실은 더 많은 양의 혈액 기반 분석을 수용하기 위해 처리량과 콜드체인 물류를 재조정해야 하며 종양학 서비스 라인 전체의 자본 할당 일정에 영향을 미칩니다. 2024년에 여러 FDA 승인을 받은 FoundationOne Liquid CDx는 시장 도입을 가속화하는 규제 기세를 보여줍니다. 그러나 리퀴드 바이옵시의 감도는 암의 병기와 종양의 배출 생물학에 의해 아직 다르고, 의료 제공업체는 검사의 중복성을 통제하면서 진단 정밀도를 유지하는 조직+혈액의 하이브리드 전략을 채용할 필요가 있습니다.

맞춤형 의료 및 프리시전 종양의 진보

동반진단은 선택적 애드온 영역을 넘어 많은 표적 치료제를 이용하기 위한 전제조건으로 성문화되어 있습니다. FDA는 승인된 검사와 관련된 168개의 바이오마커와 약물 쌍을 나열하고 있으며, 분자학적 확인이 부족한 치료 과정에 대한 지불을 상환기관이 단계적으로 삼가는 것을 시사하고 있습니다. 이와 관련하여 제약회사는 1상 시험 초기에 검사를 공동 개발하는 방향으로 방향타를 자르고 전체 프로그램 일정을 단축하고 있지만 전임상 복잡성은 증가하고 있습니다. CRO(의약품 개발 업무 수탁기관)는 바이오마커 검증 벤치를 확대하고 다년간의 전략적 아웃소싱 계약을 확보함으로써 바이오의약품 파이프라인의 사실상 분자 게이트키퍼로서의 지위를 확립하고 있습니다.

높은 개발 비용

동반진단의 개발에는 5,000만 달러에서 1억 달러, 3년에서 5년의 기간이 필요하며, 진단약은 긴 사이클의 자본 프로젝트입니다. 중소기업은 주요 제약기업과의 얼라이언스에 의존하는 경향이 강해지고, 개발자금을 얻기 위해 출자 비율을 거래하고 있습니다. 대기업이 장치의 권리를 흡수함에 따라 신규 진출기업 영업 활동의 자유도는 좁아지고 있습니다. 이러한 지적 재산의 박멸은 벤처 투자자를 단일 마커 개념보다 확장 가능한 분석 메뉴를 갖춘 플랫폼 기업으로 유도하고 틈새 바이오 마커에서 확장 가능한 정보 주도 솔루션으로 벤처 자금을 미묘하게 전환하고 있습니다.

부문 분석

2024년 시장 점유율은 여전히 PCR이 22.2%로 최대였지만, NGS는 다른 모든 기술을 능가할 것으로 예측됩니다. 동반진단의 NGS 시장 규모는 PCR 기반 대체 기술을 상회하며 2025-2030년 CAGR은 14.3%로 확대될 것으로 예측됩니다. 병원 조달 위원회는 높은 샘플 처리량이 3년의 감가상각 기간 동안 높은 NGS 소모품 비용을 상쇄한다는 것을 밝히는 총소유비용(Total Cost of Ownership) 분석을 실시합니다. 결과적으로 장비 공급업체는 분석 소프트웨어를 시약 계약에 번들로 제공하여 이 계약을 통해 수익 인식이 일회성 하드웨어 판매에서 정기적인 서비스 스트림으로 이동하여 분기 수익 가시성이 향상되었습니다.

흑색종 동반진단 면역요법과의 병용요법이 보급되어 2030년까지 CAGR 13.6%로 시장 점유율이 가속화될 전망입니다. 하류에 미치는 영향으로 피부과 클리닉은 신속한 반사 테스트를 보장하기 위해 분자 검사 실험실과 긴밀하게 협력해야 하며 역사적으로 분리된 두 개의 임상 사일로를 효과적으로 융합시킵니다. 이 통합을 통해 전자 의료기기 공급업체는 주문 엔트리 모듈을 리플렉스 분자 패널에 대응시켜야 하며, 표면적으로는 작은 IT 조정이지만 의료 시스템 전체에서 주목할만한 관리 투자가 됩니다.

동반진단 시장 조사 보고서는 업계를 기술별(면역조직화학, 중합효소 연쇄반응, 기타), 적응증별(폐암, 유방암, 기타), 제품 유형별(어세이와 키트, 장비 및 분석 장치, 기타), 샘플 유형별(조직 생검, 리퀴드 바이옵시, 기타), 최종 사용자별(제약기업별, 바이오테크놀러지 기업)

지역 분석

2024년 시장 점유율은 북미가 40.4% UnitedHealthcare는 FDA가 승인한 동반진단 및 해당 의약품을 다루는 정책이며, 이는 채용 속도에 직접적인 영향을 미치는 지불자의 지원을 나타냅니다. 추측되는 결과로는 UnitedHealthcare 산하 이외의 민간 보험사도 경쟁을 유지하기 위해서 이 방침을 모방할 가능성이 있어, 업계 전체의 검사 상환율을 안정시키는 캐스케이드로 연결됩니다.

아시아태평양은 2025-2030년 연평균 복합 성장률(CAGR) 12.7%로 성장할 것으로 예측됩니다. 일본의 정부 지원에 의한 암 유전체 프로파일링(CGP) 프로그램은 2035년까지 540억 엔의 CGP 시장을 예측해 국내 연구소에 시퀀싱 능력의 확대를 촉구하고 있습니다. 이 정부의 헌신은 이웃 국가들이 복제하고 규제 기대를 조화시키며 국경을 넘어서는 임상시험 등록에 박차를 가하고 연구가 불충분한 아시아 집단에서의 데이터 축적을 가속화할 수 있는 선례를 보여줍니다.

유럽의 체외진단제 규제 환경은 기업에 출시 전략의 재검토를 촉구하고 있습니다. 신고기관의 용량이 제한되어 시장 출시까지의 시간적 리스크가 증대하고, 진단약 기업은 잠정적인 해결책으로서 집중 시험 모델을 검토하게 됩니다. 이러한 일원화는 부주의하게 일부 표준검사기관을 강화하고 검사량이 피크에 도달한 후의 가격 결정 역학을 흔들 수 있는 준올리고폴리를 창출해 낼 가능성이 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 서포트

목차

제1장 서론

- 조사의 전제조건 및 시장의 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 종양학 진료에서 리퀴드 바이옵시 CDx의 급속한 도입

- 맞춤형 의료 및 정밀 종양학의 진보

- 진단 툴에 있어서 기술 혁신

- 만성 질환 증가

- 멀티플렉스 CDx 플랫폼을 필요로 하는 ADC에 중점을 둔 종양학 파이프라인

- 제약회사로부터의 투자 증가

- 시장 성장 억제요인

- 높은 개발 비용

- FDA의 시판 후 조사 의무에 의해 라이프 사이클 비용 상승

- 엄격한 규제 정책

- 신흥국의 인프라 부족

- 공급망 분석

- 규제 전망

- Porter's Five Forces 분석

- 신규 참가업체의 위협

- 구매자의 협상력

- 공급기업의 협상력

- 대체품의 위협

- 경쟁 기업 간 경쟁 관계

제5장 시장 규모 및 성장 예측

- 기술별

- 면역조직화학(IHC)

- 중합효소 연쇄반응(PCR)

- 실시간 PCR(RT-PCR)

- 인사이츄 하이브리드화(ISH)

- 차세대 및 유전자 서열 분석(NGS)

- 기타 기술

- 적응증별

- 폐암

- 유방암

- 대장암

- 백혈병

- 흑색종

- 위암

- 전립선암

- 기타 적응증

- 제품 및 서비스별

- 분석 및 키트

- 계측 기기 및 분석 장치

- 소프트웨어 및 서비스

- 샘플 유형별

- 조직 생검

- 액체 생검

- 세포 진단 도말 검체

- 최종 사용자별

- 제약 및 바이오테크놀러지 기업

- 계약연구기관(CRO)

- 임상 실험실

- 병원과 암 센터

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 기타 유럽

- 아시아태평양

- 중국

- 일본

- 인도

- 한국

- 호주

- 기타 아시아태평양

- 중동

- GCC

- 남아프리카

- 기타 중동

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 북미

제6장 경쟁 구도

- 시장 집중도

- 전략적 동향

- 시장 점유율 분석

- 기업 프로파일

- Abbott

- Agilent Technologies Inc.

- F. Hoffmann-La Roche Ltd

- bioMerieux SA

- QIAGEN NV

- Siemens Healthineers AG

- Thermo Fisher Scientific Inc.

- Danaher Corp.(Beckman Coulter)

- Illumina Inc.

- Myriad Genetics Inc.

- Guardant Health Inc.

- Sysmex Corp.

- Abnova Corp.

- Biogenex Laboratories Inc.

- Tempus Labs Inc.

- Foundation Medicine Inc.

- Exact Sciences Corp.

- PerkinElmer Inc.

- Invivoscribe Inc.

제7장 시장 기회 및 향후 전망

AJY 25.11.03The market size is valued at USD 8.70 billion in 2025 and is forecast to expand to USD 15.62 billion by 2030, reflecting a 12.42 % CAGR.

Companion diagnostics integrate molecular testing with targeted therapeutics, aligning diagnostic information with optimal therapy choices. The widening application of precision medicine is simultaneously shifting investment priorities for drug makers and reshaping payer reimbursement models as policy makers recognize diagnostics as pivotal cost-containment tools.

Global Companion Diagnostics Market Trends and Insights

Companion Diagnostics Market Trends & Insights Rapid Adoption of Liquid-Biopsy CDx in Oncology Practices

Liquid biopsy companion diagnostics are redefining cancer management by providing a minimally invasive route for repeat testing that captures tumor heterogeneity in real time. Clinicians now track disease evolution through circulating tumor DNA, dynamically adjusting therapy rather than relying on static tissue snapshots. A second-order implication is that hospital laboratories must recalibrate throughput and cold-chain logistics to accommodate larger volumes of blood-based assays, affecting capital-allocation timelines across the entire oncology service line. FoundationOne Liquid CDx, granted multiple FDA approvals in 2024, illustrates the regulatory momentum that is quickening market uptake . Yet liquid biopsy sensitivity still varies by cancer stage and by tumor shedding biology, meaning providers are pressured to adopt hybrid tissue-plus-blood strategies that preserve diagnostic accuracy while controlling test redundancy.

Advancements in Personalized Medicine and Precision Oncology

Companion diagnostics have moved beyond optional add-ons; they are codified prerequisites for access to many targeted drugs. The FDA lists 168 biomarker-drug pairings linked to approved tests, signaling that reimbursement agencies will progressively withhold payment for therapy courses lacking molecular confirmation. This linkage is steering pharmaceutical companies to co-develop tests earlier in Phase I trials, compressing total program timelines but increasing preclinical complexity. An immediate knock-on effect is that contract research organizations (CROs) are expanding biomarker-validation benches to secure multi-year strategic outsourcing contracts, positioning themselves as de-facto molecular gatekeepers for biopharma pipelines.

High Development Costs

Developing a companion diagnostic can require USD 50-100 million and 3-5 years, framing diagnostics as long-cycle capital projects. Smaller firms increasingly tie their fortunes to big-pharma alliances, trading equity stakes for developmental funding. The second-order consequence is a consolidation of intellectual-property portfolios: as large companies absorb device rights, freedom-to-operate for newcomers narrows. This tightening IP landscape nudges venture investors to favor platform companies with expandable assay menus rather than single-marker concepts, subtly migrating venture dollars away from niche biomarkers toward scalable informatics-driven solutions.

Other drivers and restraints analyzed in the detailed report include:

- Technological Innovations in Diagnostic Tools

- Growing Prevalence of Chronic Diseases

- Stringent Regulatory Policies

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

PCR still owns the largest 2024 slice at 22.2 % market share, yet NGS is expected to outpace all other technologies. NGS market size in companion diagnostics is forecast to outpace PCR-based alternatives, expanding at 14.3% CAGR between 2025-2030. Hospital procurement committees increasingly run total-cost-of-ownership analyses that reveal high sample throughput offsets higher NGS consumable costs over a three-year amortization window. Consequently, instrument vendors now bundle analytics software into reagent contracts, an arrangement that shifts revenue recognition from one-time hardware sales to recurring service streams-reshaping quarterly earnings visibility.

Melanoma companion diagnostics will capture a market share acceleration to 13.6% CAGR through 2030 as immunotherapy combinations proliferate. The downstream impact is that dermatology clinics must coordinate closely with molecular labs to ensure rapid reflex testing, effectively blending two historically separate clinical silos. This integration forces electronic medical record vendors to adapt order-entry modules to accommodate reflex molecular panels, an IT adjustment that, although minor on the surface, represents a notable administrative investment across health systems.

The Companion Diagnostics Market Report Segments the Industry Into Technology (Immunohistochemistry, Polymerase Chain Reaction, and More), Indication (Lung Cancer, Breast Cancer, and More), Product Type (Assays and Kits, and Instruments and Analyzers, and More), Sample Type (Tissue Biopsy, Liquid Biopsy, and More), End-User (Pharmaceutical and Biotechnology Companies, Contract Research Organizations (CROs), and More), and Geography

Geography Analysis

North America holds 40.4% market share in 2024. UnitedHealthcare's policy to cover FDA-approved companion diagnostics when matched with the corresponding drug signals payer endorsement that directly influences adoption velocity. An inferred outcome is that private insurers outside the UnitedHealthcare umbrella may emulate the policy to remain competitive, leading to a cascade that can stabilize test reimbursement rates industry-wide.

Asia-Pacific is projected to log a 12.7% CAGR from 2025-2030. Japan's government-supported cancer genome profiling (CGP) program forecasts a 54 billion-yen CGP market by 2035, prompting domestic labs to scale sequencing capacity. This governmental commitment sets a precedent that neighboring countries may replicate, harmonizing regulatory expectations and spurring cross-border clinical-trial enrollment that accelerates data accumulation in under-studied Asian populations.

Europe's In Vitro Diagnostic Regulation environment is prompting companies to reexamine launch strategies. The limited capacity of notified bodies amplifies time-to-market risk, causing diagnostic firms to consider centralized testing models as interim solutions. Such centralization may inadvertently strengthen select reference laboratories, creating a quasi-oligopoly that could sway pricing dynamics once test volumes peak.

- Abbott Laboratories

- Agilent Technologies

- Roche

- bioMerieux

- QIAGEN

- Siemens Healthineers

- Thermo Fisher Scientific

- Danaher Corp. (Beckman Coulter)

- Illumina

- Myriad Genetics

- Guardant Health

- Sysmex Corp.

- Abnova Corp.

- BioGenex

- Tempus Labs Inc.

- Foundation Medicine Inc.

- Exact Sciences Corp.

- PerkinElmer

- Invivoscribe Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rapid adoption of liquid-biopsy CDx in oncology practices

- 4.2.2 Advancements in Personalized Medicine and Precision Oncology

- 4.2.3 Technological Innovations in Diagnostic Tools

- 4.2.4 Growing Prevalence of Chronic Diseases

- 4.2.5 ADC-focused oncology pipeline requiring multiplex CDx platforms

- 4.2.6 Rising Investment from Pharmaceutical Companies

- 4.3 Market Restraints

- 4.3.1 High Development Costs

- 4.3.2 FDA post-market evidence obligations raising lifecycle costs

- 4.3.3 Stringent Regulatory Policies

- 4.3.4 Limited infrastructure in Emerging Countries

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Outlook

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Bargaining Power of Suppliers

- 4.6.4 Threat of Substitutes

- 4.6.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Technology

- 5.1.1 Immunohistochemistry (IHC)

- 5.1.2 Polymerase Chain Reaction (PCR)

- 5.1.3 Real-Time PCR (RT-PCR)

- 5.1.4 In-Situ Hybridization (ISH)

- 5.1.5 Next-Generation / Gene Sequencing (NGS)

- 5.1.6 Other Technologies

- 5.2 By Indication

- 5.2.1 Lung Cancer

- 5.2.2 Breast Cancer

- 5.2.3 Colorectal Cancer

- 5.2.4 Leukemia

- 5.2.5 Melanoma

- 5.2.6 Gastric Cancer

- 5.2.7 Prostate Cancer

- 5.2.8 Other Indications

- 5.3 By Product & Service

- 5.3.1 Assays & Kits

- 5.3.2 Instruments & Analyzers

- 5.3.3 Software & Services

- 5.4 By Sample Type

- 5.4.1 Tissue Biopsy

- 5.4.2 Liquid Biopsy

- 5.4.3 Cytology Smears

- 5.5 By End-user

- 5.5.1 Pharmaceutical & Biotechnology Companies

- 5.5.2 Contract Research Organizations (CROs)

- 5.5.3 Clinical Reference Laboratories

- 5.5.4 Hospital & Cancer Centers

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 Europe

- 5.6.2.1 Germany

- 5.6.2.2 United Kingdom

- 5.6.2.3 France

- 5.6.2.4 Italy

- 5.6.2.5 Spain

- 5.6.2.6 Rest of Europe

- 5.6.3 Asia-Pacific

- 5.6.3.1 China

- 5.6.3.2 Japan

- 5.6.3.3 India

- 5.6.3.4 South Korea

- 5.6.3.5 Australia

- 5.6.3.6 Rest of Asia-Pacific

- 5.6.4 Middle East

- 5.6.4.1 GCC

- 5.6.4.2 South Africa

- 5.6.4.3 Rest of Middle East

- 5.6.5 South America

- 5.6.5.1 Brazil

- 5.6.5.2 Argentina

- 5.6.5.3 Rest of South America

- 5.6.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global-level Overview, Market-level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products & Services, Recent Developments)

- 6.4.1 Abbott

- 6.4.2 Agilent Technologies Inc.

- 6.4.3 F. Hoffmann-La Roche Ltd

- 6.4.4 bioMerieux SA

- 6.4.5 QIAGEN N.V.

- 6.4.6 Siemens Healthineers AG

- 6.4.7 Thermo Fisher Scientific Inc.

- 6.4.8 Danaher Corp. (Beckman Coulter)

- 6.4.9 Illumina Inc.

- 6.4.10 Myriad Genetics Inc.

- 6.4.11 Guardant Health Inc.

- 6.4.12 Sysmex Corp.

- 6.4.13 Abnova Corp.

- 6.4.14 Biogenex Laboratories Inc.

- 6.4.15 Tempus Labs Inc.

- 6.4.16 Foundation Medicine Inc.

- 6.4.17 Exact Sciences Corp.

- 6.4.18 PerkinElmer Inc.

- 6.4.19 Invivoscribe Inc.

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment