|

시장보고서

상품코드

1848301

산업 및 시설용 클리닝 화학제품 시장 : 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Industrial And Institutional Cleaning Chemicals - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

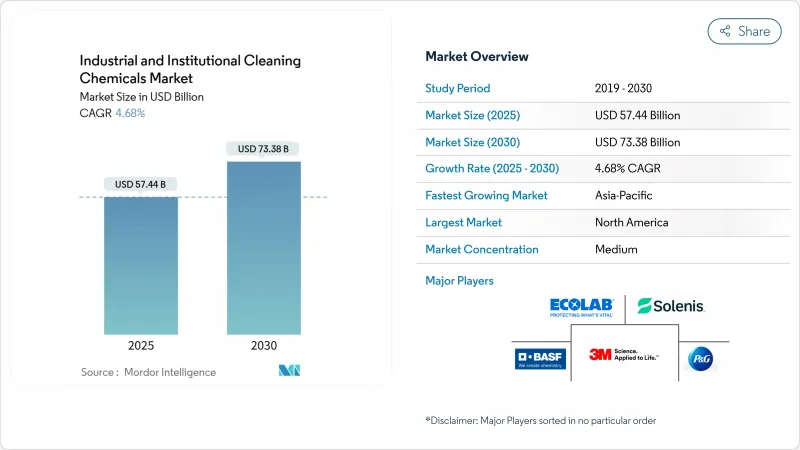

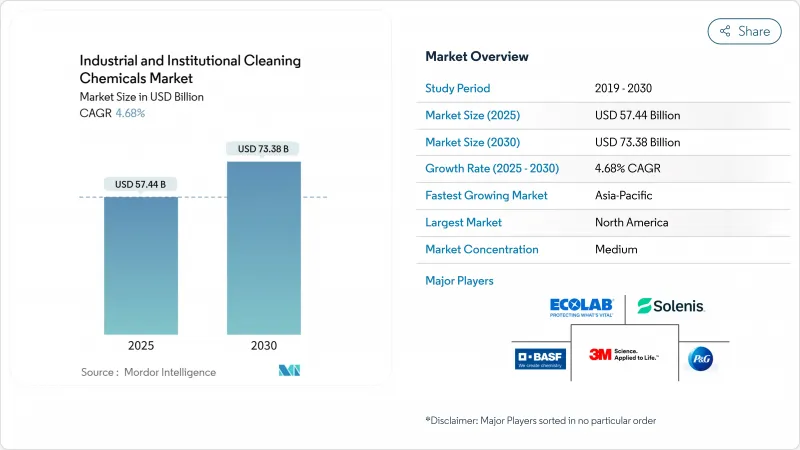

산업 및 시설용 클리닝 화학제품 시장 규모는 2025년에 574억 4,000만 달러로 추정되고, 예측 기간(2025-2030년) CAGR 4.68%로 성장할 전망이며, 2030년에는 733억 8,000만 달러에 이를 것으로 예측됩니다.

헬스케어, 식품가공, 퀵서비스 레스토랑, 접객의 구조적 변화는 주기적인 상승이 아니라 시장의 꾸준한 궤도를 설명하고 있습니다. 급성기 의료나 장기 요양에 있어서 감염 제어 프로토콜의 엄격화에 따라, 접촉 시간이 짧은 프리미엄 소독제가 인기를 모으는 한편, 산업화가 급속히 진행되는 아시아태평양의 경제가 바이오 기반 제제의 평균을 웃도는 성장을 가속하고 있습니다. 북미는 엄격한 규제 감독에 의해 규모의 주도권을 유지하고 있지만, 공급업체는 불안정한 석유화학제품의 투입에 의한 마진 압력에 대항하기 때문에 신흥 시장을 위한 혁신을 현지화하는 경향이 강해지고 있습니다. 디지털 투여, IoT 원격 모니터링, 효소를 이용한 클리닝 화학제품은 이제 경쟁적인 핵심 레버이며, 단일 제품이 아닌 솔루션 생태계가 미래의 차별화를 결정할 것임을 보여줍니다.

세계의 산업 및 시설용 클리닝 화학제품 시장 동향 및 인사이트

급성기 및 장기 요양 시설에서 COVID-19 후의 감염 관리 프로토콜

2024년 CDC에 의한 가이드라인 강화는 다제 내성균에 대한 효능이 입증된 EPA 등록 소독제가 필요하며, 병원은 스펙트럼을 희생하지 않고 접촉 시간을 단축할 수 있는 고급 와이프, 스프레이, 농축액의 표준화를 촉진하고 있습니다. 합동위원회는 현재 시설 방침에서 이러한 연방 관행에 대한 명확한 언급을 의무화하고 있으며, 효과적으로 조달을 전문화하고 규제 서류가 부족한 공급자에게 불리하게 되어 있습니다. 주요 공급업체는 컴플라이언스를 모니터링하는 IoT 지원 디스펜서와 현장 직원 교육을 번들로 제공하며, 침대 난간 및 간호사 스테이션과 같은 접촉 빈도가 높은 영역에서 실수를 최소화합니다. 항균제 내성에 대한 우려 증가는 과초산 블렌드와 같은 표면에서 장시간 활성을 유지하는 광역 스펙트럼 화학제품에 대한 수요를 더욱 촉진하고 있습니다.

아시아의 식육 및 수산물 가공에 있어서 HACCP 주도형 제균제의 채용

아시아 시설에서는 위험 분석 및 중요 관리 지점(HACCP) 시스템이 의무화되어 있기 때문에 가공업자는 풍토병과 물의 경도 변화에 대응하는 살균제를 채택해야 합니다. 2024년에 발표된 카자흐스탄의 연구에서는 HACCP의 도입으로 고기의 잔류 납과 잔류 비소를 줄이고 정량적 안전성 향상을 확인했습니다. 베트남의 새우 리더인 민푸는 현재 효소 기반 세정제와 과산화물 프리 제균제를 혼합하여 전체 세정 비용을 30-50% 삭감하는 동시에 수출 잔류 기준치 내로 억제하고 있습니다. 특히 제품이 할랄 규제 및 수출 규제에 부합하는 경우, 감사 문서와 신속한 현장 기술 조언을 모두 제공하는 공급업체가 이점을 누릴 수 있습니다. 가공업자가 자동화를 확대함에 따라 수요는 화학제품의 과도한 사용과 폐수 COD 부하를 줄이는 제어 투여 시스템으로 이동하고 있습니다.

변동하는 원료 가격

2024년 중반 이후의 나프타 관련 계면활성제 원료의 12-15%의 상승은 배합업자의 조익을 압박했고, 북미와 유럽에서는 선택적인 가격 할증을 강요했습니다. 변동을 완충하기 위해 선두 공급업체는 EO 노출을 최대 40%까지 헤지하여 석유화학 지표가 아닌 농업 지표를 따르는 코코넛 유래의 알코올 에톡실레이트 또는 소포롤리피드 바이오서팩턴트에 대한 대체를 가속화하고 있습니다. 재제제화 프로그램은 또한 보다 고농도의 활성제를 추진하고 패키지의 무게와 운송 비용을 줄입니다. 그럼에도 불구하고 구매력이 제한된 중소규모 블렌더는 운전자금의 스트레스에 직면하여 지역 확대 계획을 늦추고 있습니다.

부문 분석

계면활성제는 2024년 산업 및 시설용 클리닝 화학제품 시장 점유율의 32.1%를 차지했으며, 탈지세정제, 소독용 습식 티슈, 식기세척기용 세제에 필수적입니다. 그 양친매성 구조는 유지 및 미립자 얼룩의 유화를 가능하게 해, HACCP 인증의 식육 공장이나 CDC 준거의 병원 세정제에 있어서 효능 주장의 중심이 되고 있습니다. 그러나 석유화학제품에 대한 의존은 가격 변동 및 탄소발자국의 조사에 노출되어 GHG 배출량을 50% 절감하면서 동등한 습윤성을 실현하는 소홀로리피드와 람노리피드에 대한 투자를 촉구하고 있습니다. 유니레버의 2024년 조달 정책은 트레이서블에서 산림 파괴가 없는 원료를 공급업체에 평가하여 체인 전체에서 지속 가능한 조달을 가속화하고 있습니다.

이와는 대조적으로, 용매는 CAGR 예측 6.3%에서 가장 빠르게 성장하는 원료 카테고리입니다. 수혼화성 글리콜 에테르, 바이오 유래의 락트산 에스테르, 캘리포니아주 2025년 VOC 기준치 0.5%에 적합한 저 VOC d-리모넨 블렌드가 성장의 중심이 되고 있습니다. 멕시코와 미국의 자동차 OEM 공장에서는 불연성 수성 부품 세척 용제의 지정이 늘어나고 있으며, 높은 인화점 이염기산 에스테르에 대한 수요가 높아지고 있습니다. N-메틸-2-피롤리돈(NMP) 및 기타 생식 독성 용매에 대한 규제 압력은 금속 세척 용도 분야에서도 대안을 가속화하고 있으며 위험 유해성 분류에 관계없이 용매의 강도를 조절할 수 있는 공급업체에게 시장의 여지를 제공합니다.

범용 클리너는 바닥, 벽, 경질 표면에 보편적인 적용성으로 2024년 매출의 35%를 차지했습니다. 병으로 희석하는 농축 파우치는 하우스 키핑, 화장실 및 유리 청소를 80% 낮은 플라스틱 중량으로 커버하며 체인 호텔의 ESG 감사에 부응합니다. 제품 스튜어드십은 또한 MIT와 CMIT를 피하기 위한 방부제의 재제조를 추진하고 있으며, 유럽의 2025년 살생물제 개정에 대한 준수를 보장합니다.

살균제 및 제균제는 헬스케어, 외식 산업 및 교통 허브가 위생에 대한 경계를 높이고 있기 때문에 CAGR 6.7%와 다른 모든 유형을 초과합니다. 지역 제제 제조업체는 과산화수소와 구연산을 활용한 4급 암모늄을 포함하지 않는 옵션을 도입하여 소비자의 감수성과 지역 배출 제한에 대응하고 있습니다. 세탁 및 차량 관리의 하위 부문은 꾸준히 성장하고 광열 비용과 화학 물질을 동시에 절약하기 위해 센서 구동 용량 제어 및 물 재사용 시스템을 활용합니다.

지역 분석

북미는 2024년 매출 점유율 33%로, 산업 및 시설용 클리닝 화학제품 시장을 선도하였고, CDC, EPA, FDA의 규제에 힘쓰고 문서화된 고급 솔루션을 지지하고 있습니다. 병원은 CDC의 2024년 환경 세척 절차를 준수하는 살포자성 와이프를 채택하여 안정적인 소독제 수요를 지원하고 있습니다.

아시아태평양이 성장엔진인 위생 기준 상승, 제조업 확대, 식중독에 대한 정부 단속을 배경으로 2025-2030년 CAGR은 7.8%로 성장할 전망입니다. 중국은 살균제에 대한 GB 표준의 개정을 강화하고 국제 공급업체에게 생산 및 문서화의 현지화를 촉구하고 있습니다. 베트남, 태국, 인도네시아는 REACH 스타일의 화학물질 관리법을 도입하여 성분의 투명성에 대한 필요성을 높이고 바이오 채용을 강화합니다.

유럽은 성숙하면서도 혁신적인 시장이며, EU 그린 딜이나 진화하는 살생물제 지령에 의해 배합업자는 식물 유래의 계면활성제나 클로즈드 루프의 패키징을 목표로 합니다. 독일에서는 시설용 클리닝 용기의 예금제도가 시험적으로 도입되고, 스칸디나비아의 지자체에서는 탄소중립적인 조달이 지정되어 간접적으로 효소를 많이 포함한 클리너가 지지되고 있습니다.

중동 및 아프리카는 GCC, 이집트, 케냐에서 급성장하는 접객 프로젝트와 헬스케어 투자로부터 혜택을 받으며 미국과 유럽 브랜드와의 프랜차이즈 계약에 따라 QSR을 충분히 개발함으로써 강화됩니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월의 애널리스트 및 서포트

목차

제1장 서론

- 조사의 전제조건 및 시장의 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 급성기 및 장기 케어 시설에 있어서 COVID-19 후의 감염 제어 프로토콜

- 아시아의 식육 및 수산물 가공에 있어서 HACCP 주도의 소독제 도입

- GCC 국가와 이집트의 퀵 서비스 레스토랑의 붐에서 식기 세척기 자동 투입 필요

- 세계의 관광 및 접객의 회복

- 동아시아에서 반도체 클린 룸의 확장이 초저 잔류물 블렌드 추진

- 시장 성장 억제요인

- 원재료 가격 변동

- 에틸렌옥사이드 원료의 휘발성에 의해 계면활성제 비용 상승

- 엄격한 환경 및 건강 규제

- 밸류체인 분석

- Porter's Five Forces

- 공급기업의 협상력

- 구매자의 협상력

- 신규 참가업체의 위협

- 대체품의 위협

- 경쟁도

제5장 시장 규모 및 성장 예측

- 원재료별

- 염소알칼리

- 가성소다

- 소다 재

- 염소

- 계면활성제

- 비이온성

- 음이온성

- 양이온

- 양성

- 용제

- 알코올

- 탄화수소

- 염소화

- 에테르

- 인산염

- 산

- 살생물제

- 기타 원재료(킬레이트제, 레올로지 개질제, 유백제, 분산제, 케톤, 에스테르)

- 염소알칼리

- 제품 유형별

- 범용 클리너

- 소독제 및 살균제

- 세탁 케어 제품

- 차량 세정 제품

- 원료 원산지별

- 바이오 기반 및그린

- 기존 및 석유화학

- 시장 유형별

- 상업용

- 푸드 서비스

- 소매

- 세탁 및 드라이클리닝

- 헬스케어

- 세차

- 사무실, 호텔, 숙박 시설

- 제조업

- 식품 및 음료 가공

- 금속가공제품

- 전자부품

- 기타 제조업(섬유, 펄프 및 종이, 석유화학)

- 상업용

- 지역별

- 아시아태평양

- 중국

- 인도

- 일본

- 한국

- 말레이시아

- 태국

- 인도네시아

- 베트남

- 기타 아시아태평양

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 북유럽 국가

- 튀르키예

- 러시아

- 기타 유럽

- 남미

- 브라질

- 아르헨티나

- 콜롬비아

- 기타 남미

- 중동 및 아프리카

- 사우디아라비아

- 아랍에미리트(UAE)

- 카타르

- 이집트

- 남아프리카

- 나이지리아

- 기타 중동 및 아프리카

- 아시아태평양

제6장 경쟁 구도

- 시장 집중도

- 전략적 동향

- 시장 점유율 분석

- 기업 프로파일

- 3M

- Akzo Nobel NV

- Albemarle Corporation

- BASF

- Betco

- CLARIANT

- Croda International Plc

- Ecolab

- Henkel AG & Co. KGaA

- Huntsman International LLC

- KERSIA GROUP

- LANXESS

- National Chemical Laboratories, Inc.

- Nouryon

- Procter & Gamble

- Reckitt

- Solenis

- Solvay

- Spartan Chemical Company, Inc.

- Stepan Company

- Westlake Corporation

- WM Barr

제7장 시장 기회 및 향후 전망

AJY 25.11.03The Industrial And Institutional Cleaning Chemicals Market size is estimated at USD 57.44 billion in 2025, and is expected to reach USD 73.38 billion by 2030, at a CAGR of 4.68% during the forecast period (2025-2030).

Structural shifts in healthcare, food processing, quick-service restaurants, and hospitality, rather than cyclical upswings, explain the market's steady trajectory. Premium disinfectants with rapid contact times are gaining traction as infection-control protocols tighten in acute and long-term care, while Asia-Pacific's fast-industrializing economies stimulate above-average growth for bio-based formulations. North America retains scale leadership through stringent regulatory oversight, but suppliers increasingly localize innovation for emerging markets to counter margin pressure from volatile petrochemical inputs. Digital dosing, IoT remote monitoring, and enzyme-enabled cleaning chemistries are now core competitive levers, signaling that solution ecosystems, not standalone products, will define future differentiation.

Global Industrial And Institutional Cleaning Chemicals Market Trends and Insights

Infection-Control Protocols Post-COVID-19 in Acute and Long-Term Care Facilities

Tighter guidelines from the CDC in 2024 require EPA-registered disinfectants with demonstrated efficacy against multidrug-resistant organisms, prompting hospitals to standardize on premium wipes, sprays and concentrates that shorten contact time without sacrificing spectrum. The Joint Commission now mandates explicit reference to these federal practices within facility policies, effectively professionalizing procurement and disadvantaging suppliers lacking regulatory dossiers. Leading vendors bundle on-site staff training with IoT-enabled dispensers that monitor compliance, minimizing error in high-touch zones such as bed rails and nurse stations. Elevated antimicrobial resistance concerns further spur demand for broad-spectrum chemistries like peracetic acid blends that remain active on surfaces for extended periods.

HACCP-Driven Sanitizer Adoption in Asian Meat and Seafood Processing

Mandatory hazard analysis and critical control point (HACCP) systems across Asian facilities compel processors to adopt sanitizers targeted to endemic pathogens and variable water hardness. A Kazakh study published in 2024 showed HACCP deployment cut lead and arsenic residues in meat, underscoring quantifiable safety gains. Vietnamese shrimp leader Minh Phu now blends enzyme-based cleaners with peroxide-free sanitizers, reducing overall cleaning costs 30-50% while staying within export residue limits. Suppliers that deliver both documentation for audits and rapid on-site technical advice have the inside track, particularly when products align with halal and export regulations. As processors scale automation, demand is shifting toward controlled-dosing systems that cut chemical overuse and wastewater COD loads.

Fluctuating Raw Material Prices

Surges of 12-15% in naphtha-linked surfactant feedstocks since mid-2024 squeezed formulators' gross margins and forced selective price surcharges in North America and Europe. To buffer volatility, large suppliers hedge up to 40% of EO exposure and accelerate substitution with coconut-derived alcohol ethoxylates or sophorolipid biosurfactants that track agricultural rather than petrochemical indices. Reformulation programs also push higher actives concentrations, cutting package weight and shipping costs. Still, small and mid-size blenders with limited purchasing leverage face working-capital stress, delaying regional expansion plans.

Other drivers and restraints analyzed in the detailed report include:

- QSR Boom in GCC and Egypt Requiring Automated Warewash Dosing

- Global Tourism and Hospitality Recovery

- Ethylene-Oxide Feedstock Volatility Elevating Surfactant Costs

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Surfactants retained 32.1% of industrial and institutional cleaning chemicals market share in 2024, anchored by indispensability across degreasers, disinfectant wipes and ware-wash detergents. Their amphiphilic structure enables emulsification of fats, oils and particulate soils, making them central to efficacy claims in HACCP-certified meat plants and CDC-compliant hospital cleaners. Yet petrochemical dependency exposes formulators to both price swings and carbon footprint scrutiny, pushing investment toward sophorolipids and rhamnolipids that deliver comparable wetting with 50% lower GHG emissions. Unilever's 2024 procurement policy now scores suppliers on traceable, deforestation-free feedstocks, accelerating sustainable sourcing across the chain.

Solvents, by contrast, represent the fastest-growing raw material category with a 6.3% forecast CAGR. Growth leans on water-miscible green glycol ethers, bio-derived lactate esters and low-VOC d-limonene blends that comply with California's 2025 0.5% VOC threshold for general cleaners. Auto OEM plants in Mexico and the United States increasingly specify non-flammable aqueous parts-wash solvents, fuelling demand for high-flashpoint dibasic esters. Regulatory pressure on N-methyl-2-pyrrolidone (NMP) and other reproductive-toxicity solvents accelerates substitution even in metal cleaning applications, opening market room for suppliers able to tailor solvency strength without hazardous classifications.

General-purpose cleaners represented 35% of 2024 revenue due to universal applicability on floors, walls and hard surfaces. Concentrated pouches that dilute in proportioned bottles now cover housekeeping, restroom and glass cleaning tasks with 80% lower plastic weight, answering chain-hotel ESG audits. Product stewardship also drives preservatives reformulation to avoid MIT and CMIT, ensuring compliance with Europe's 2025 biocide revisions.

Disinfectants and sanitizers outpace all other types at 6.7% CAGR because healthcare, foodservice and transit hubs maintain an elevated baseline of hygiene vigilance. Regional formulators introduce quaternary-ammonium-free options that leverage hydrogen peroxide and citric acid to meet consumer sensitivities and local discharge limits. Laundry and vehicle care subsegments grow steadily, tapping sensor-driven dosage control and water-re-use systems to conserve utilities and chemicals simultaneously.

The Industrial and Institutional Cleaning Chemicals Market Report Segments the Industry by Raw Material (Chlor-Alkali, Surfactants, Solvents, and More), Product Type (General-Purpose Cleaners, Disinfectants and Sanitizers, and More), Ingredient Origin (Bio-based/Green and Conventional/Petrochemical), Market Type (Commercial and Manufacturing), and Geography (Asia-Pacific, North America, Europe, and More).

Geography Analysis

North America led the industrial and institutional cleaning chemicals market with 33% revenue share in 2024, buoyed by CDC, EPA and FDA regulations that favor premium, fully documented solutions. Hospitals adopt sporicidal wipes that comply with the CDC's 2024 environmental-cleaning procedures, underpinning steady disinfectant demand.

Asia-Pacific is the growth engine, registering a 7.8% CAGR over 2025-2030 on the back of rising hygiene standards, manufacturing expansion and government crackdowns on food-borne illness. China tightens GB standard revisions on disinfectants, nudging international suppliers to localize production and documentation. Vietnam, Thailand and Indonesia roll out REACH-style chemical control laws, heightening the need for ingredient transparency and bolstering bio-based adoption.

Europe remains a mature yet innovative market where the EU Green Deal and evolving biocide directives drive formulators toward plant-derived surfactants and closed-loop packaging. Germany pilots deposit systems for commercial cleaning canisters, while Scandinavian municipalities specify carbon-neutral procurement, indirectly favoring enzyme-rich cleaners.

The Middle East and Africa benefit from burgeoning hospitality projects and health-care investment across GCC, Egypt and Kenya, augmented by ample QSR rollout under franchise agreements with US and European brands.

- 3M

- Akzo Nobel N.V.

- Albemarle Corporation

- BASF

- Betco

- CLARIANT

- Croda International Plc

- Ecolab

- Henkel AG & Co. KGaA

- Huntsman International LLC

- KERSIA GROUP

- LANXESS

- National Chemical Laboratories, Inc.

- Nouryon

- Procter & Gamble

- Reckitt

- Solenis

- Solvay

- Spartan Chemical Company, Inc.

- Stepan Company

- Westlake Corporation

- WM Barr

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Infection-Control Protocols Post-COVID-19 in Acute and Long-Term Care Facilities

- 4.2.2 HACCP-Driven Sanitizer Adoption in Asian Meat and Seafood Processing

- 4.2.3 Quick-Service Restaurant Boom in GCC and Egypt Requiring Automated Warewash Dosing

- 4.2.4 Global Tourism and Hospitality Recovery

- 4.2.5 Semiconductor Cleanroom Expansion Driving Ultra-Low-Residue Blends in East Asia

- 4.3 Market Restraints

- 4.3.1 Fluctuating Raw Material Prices

- 4.3.2 Ethylene-Oxide Feedstock Volatility Elevating Surfactant Costs

- 4.3.3 Stringent Environmental and Health Regulations

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Degree of Competition

5 Market Size and Growth Forecasts (Value)

- 5.1 By Raw Material

- 5.1.1 Chlor-alkali

- 5.1.1.1 Caustic Soda

- 5.1.1.2 Soda Ash

- 5.1.1.3 Chlorine

- 5.1.2 Surfactants

- 5.1.2.1 Non-ionic

- 5.1.2.2 Anionic

- 5.1.2.3 Cationic

- 5.1.2.4 Amphoteric

- 5.1.3 Solvents

- 5.1.3.1 Alcohols

- 5.1.3.2 Hydrocarbons

- 5.1.3.3 Chlorinated

- 5.1.3.4 Ethers

- 5.1.4 Phosphates

- 5.1.5 Acids

- 5.1.6 Biocides

- 5.1.7 Other Raw Materials (Chelants, Rheology Modifiers, Opacifiers, Dispersants, Ketones, Esters)

- 5.1.1 Chlor-alkali

- 5.2 By Product Type

- 5.2.1 General-Purpose Cleaners

- 5.2.2 Disinfectants and Sanitizers

- 5.2.3 Laundry Care Products

- 5.2.4 Vehicle Wash Products

- 5.3 By Ingredient Origin

- 5.3.1 Bio-based / Green

- 5.3.2 Conventional / Petrochemical

- 5.4 By Market Type

- 5.4.1 Commercial

- 5.4.1.1 Foodservice

- 5.4.1.2 Retail

- 5.4.1.3 Laundry and Dry-Cleaning

- 5.4.1.4 Healthcare

- 5.4.1.5 Car Washes

- 5.4.1.6 Offices, Hotels and Lodging

- 5.4.2 Manufacturing

- 5.4.2.1 Food and Beverage Processing

- 5.4.2.2 Fabricated Metal Products

- 5.4.2.3 Electronic Components

- 5.4.2.4 Other Manufacturing (Textile, Pulp and Paper, Petrochemical)

- 5.4.1 Commercial

- 5.5 By Geography

- 5.5.1 Asia-Pacific

- 5.5.1.1 China

- 5.5.1.2 India

- 5.5.1.3 Japan

- 5.5.1.4 South Korea

- 5.5.1.5 Malaysia

- 5.5.1.6 Thailand

- 5.5.1.7 Indonesia

- 5.5.1.8 Vietnam

- 5.5.1.9 Rest of Asia-Pacific

- 5.5.2 North America

- 5.5.2.1 United States

- 5.5.2.2 Canada

- 5.5.2.3 Mexico

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Nordics

- 5.5.3.7 Turkey

- 5.5.3.8 Russia

- 5.5.3.9 Rest of Europe

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Argentina

- 5.5.4.3 Colombia

- 5.5.4.4 Rest of South America

- 5.5.5 Middle-East and Africa

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 United Arab Emirates

- 5.5.5.3 Qatar

- 5.5.5.4 Egypt

- 5.5.5.5 South Africa

- 5.5.5.6 Nigeria

- 5.5.5.7 Rest of Middle-East and Africa

- 5.5.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global-level Overview, Market-level Overview, Core Segments, Financials, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 3M

- 6.4.2 Akzo Nobel N.V.

- 6.4.3 Albemarle Corporation

- 6.4.4 BASF

- 6.4.5 Betco

- 6.4.6 CLARIANT

- 6.4.7 Croda International Plc

- 6.4.8 Ecolab

- 6.4.9 Henkel AG & Co. KGaA

- 6.4.10 Huntsman International LLC

- 6.4.11 KERSIA GROUP

- 6.4.12 LANXESS

- 6.4.13 National Chemical Laboratories, Inc.

- 6.4.14 Nouryon

- 6.4.15 Procter & Gamble

- 6.4.16 Reckitt

- 6.4.17 Solenis

- 6.4.18 Solvay

- 6.4.19 Spartan Chemical Company, Inc.

- 6.4.20 Stepan Company

- 6.4.21 Westlake Corporation

- 6.4.22 WM Barr

7 Market Opportunities and Future Outlook

- 7.1 White-Space and Unmet-Need Assessment

- 7.2 Emerging Use of Bio-based Cleaning Chemicals