|

시장보고서

상품코드

1848324

라벨 프리 어레이 시스템 시장 : 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Label-free Array Systems - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

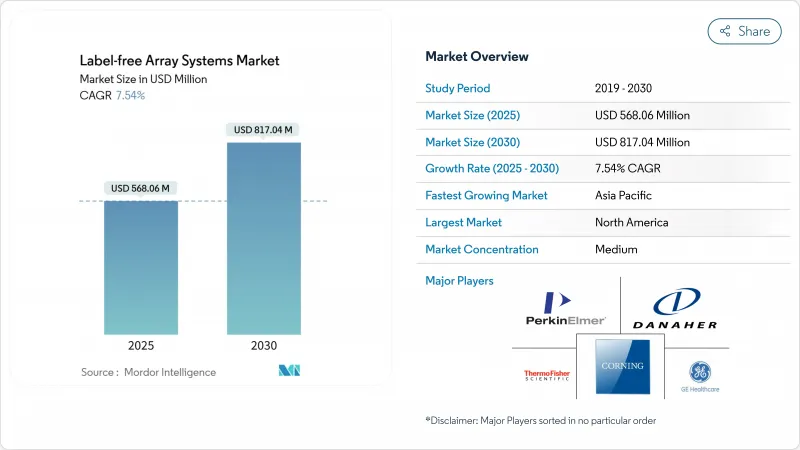

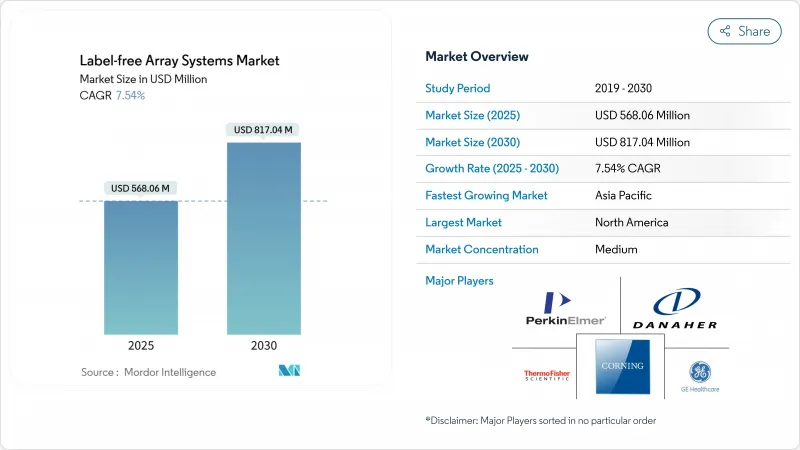

라벨 프리 어레이 시스템 시장은 2025년에 5억 6,806만 달러로 추정되고, 2030년에는 8억 1,704만 달러에 이를 것으로 예측되며, 2025-2030년 CAGR 7.54%로 성장할 전망입니다.

의약품 연구개발 예산 증가, 실시간 동태 데이터에 대한 수요 증가, 복잡한 생물제제로의 이행은 탐색 및 개발 프로그램 전체에서 이 기술의 역할을 확고히 하고 있습니다. 주요 스폰서는 현재 프로젝트의 타임라인을 단축하고 후보 화합물의 성공률을 향상시키기 위해 적중에서 리드로 캐스케이드의 초기 단계에서 라벨 프리 검출을 통합하고 있습니다. 장비 공급업체의 통합은 AI를 활용한 분석과 함께 플랫폼 업그레이드를 가속화하고 데이터 분석 장벽을 낮추고 있습니다. 한편, 북미, 유럽연합(EU), 중국, 인도의 지역 자금 조달 이니셔티브는 POC(Point of Care) 진단 및 세포 요법 제조에 이르기까지 새로운 용도 분야를 위한 비옥한 환경을 창출하고 있습니다. 주력 제품인 SPR이나 BLI 플랫폼에 대한 고액의 설비 투자나, 훈련을 받은 나노옵틱스 기술자의 부족이라고 하는 뿌리 깊은 과제는 가격에 민감한 분야에서의 채용을 계속 억제하고 있지만, 공유 시설 모델이나 리스 방식이 비용면의 허들을 상쇄하기 시작하고 있습니다.

세계의 라벨 프리 어레이 시스템 시장 동향 및 인사이트

라벨이 있는 검출 기술에 대한 이점

라벨 프리법에서는 형광 태그나 방사성 태그를 사용하지 않으므로 결합 동태를 방해하는 입체 장애나 신호 소광을 방지할 수 있습니다. 12.4%의 1차 히트와 92%의 결정학적 확인에서 알 수 있듯이, 단편 기반 캠페인이 수정되지 않은 리간드를 이용하면 히트 비율이 급증합니다. 2차 시약이 필요하지 않기 때문에 분석 개발 시간이 40-60% 단축되고 의약품 화학 팀이 신속하게 반복할 수 있습니다. 스탠포드 대학의 SENSBIT 플랫폼은 기존 센서의 수명이 11시간인 반면 혈청에서 한 달이 지나도 70%의 신호를 유지함으로써 내구성 향상을 더욱 강조하고 있습니다. 이러한 고성능은 라벨 프리 어레이 시스템 시장이 기존의 라벨링 분석에서 빠르게 전환하고 있음을 뒷받침합니다.

제약 및 바이오테크놀러지 기업에 의한 연구개발비 증가

세계 제약 기업의 연구 개발비는 2024년에는 전년 대비 1.5% 증가한 2,880억 달러에 달했으며, 그 상당 부분이 고도 분석 플랫폼에 소비되고 있습니다. 머크사만으로도 179억 달러를 창약 프로그램에 쏟아 부어 라벨 프리 스크리닝 능력을 명확하게 우선시하고 있습니다. 치료제 포트폴리오가 다특이적 항체, 유전자 편집기, 세포 요법에 기울어짐에 따라, 높은 컨텐츠의 키네틱 데이터세트는 규제 당국에 제출된 서류에 미션 크리티컬하게 되고 있습니다. 다이이치 산쿄의 로봇화된 샌디에고 실험실은 이러한 변화를 보여주며, 자동화 및 AI 주도의 라벨 프리 분석을 통합함으로써 벤치에서 IND까지의 타임라인을 단축하고 있습니다. 그 결과 1단계 성공률은 기존 스크리닝의 60-70%에서 AI와 라벨 프리 플랫폼에서 80-90%로 상승하여 지속적인 투자에 대한 경영진의 헌신을 강화하고 있습니다.

장비의 높은 자본 비용

프리미엄 SPR 시스템의 정가는 20만-50만 달러이며, 완전 장비의 BLI 리그는 서비스 계약 전에 30만 달러를 넘습니다. 2030년까지 6만 7,000명의 미국인 엔지니어를 추가해야 하는 반도체의 노동력 부족으로 광학 부품 가격이 상승하고 있습니다. 갈륨과 게르마늄의 수출 제한으로 리드 타임이 길어지고, 포토닉스 제조업체의 75%가 고용 과제를 보고하고 있습니다. 그 결과, 중소형 생명공학기업 및 학술센터는 구매를 연기하고, 공유 코어 시설과 벤더가 자금을 제공하는 리스 프로그램을 이용해, 비용을 수년 단위로 분산시키는 방향으로 유도하고 있습니다.

부문 분석

표면 플라즈몬 공명은 2024년 매출의 41.45%를 차지했으며, 라벨 프리 어레이 시스템 시장에서 가장 큰 슬라이스가 되었습니다. 공급업체는 서브나노몰의 검출 한계를 밀어 올리고 최대 32개의 상호작용을 동시에 측정하는 멀티플렉스 카트리지를 추가하여 리더십을 유지합니다. SPR 플랫폼으로 인한 라벨 프리 어레이 시스템 시장 규모는 제약 기업의 고객이 노후화된 장비를 현대화함에 따라 업계 전체의 CAGR로 꾸준히 증가할 것으로 예측됩니다. 그러나 국소 SPR은 나노플라즈모닉 메타서피스가 우수한 저분자 감도를 제공하고 휴대용 진단에 적합하므로 CAGR 9.65%로 가장 빠른 성장이 기대되고 있습니다.

국립대만대학의 pH-반응성 DNA 나노스위치는 0.57pM의 마이크로RNA 검출 한계를 달성하였고, LSPR을 임상적으로 이용가능한 분석에 접근하였습니다. 휘스퍼 갤러리 모드 마이크로 레이저의 병렬 발전은 초기 암 바이오 마커 패널에 적합한 증폭 에바네센트 필드를 제공합니다. 경쟁으로 인해 기존 기업은 차세대 SPR 라인에 나노 가공 칩을 통합하는 데 박차를 가하고 벌크 광 SPR과 칩 기반 LSPR의 경계가 모호해지고 있습니다. 가격 차이가 감소함에 따라 조달 결정은 원시 감도뿐만 아니라 처리량, 서비스 풋 프린트 및 AI 분석 플러그인에 따라 달라질 것입니다.

지역 분석

북미는 2024년 매출액 점유율 44.56%로 라벨 프리 어레이 시스템 시장을 선도하고 있으며, 풍부한 자본 풀, FDA와 연계한 검증 패스웨이, 서모 피셔의 20억 달러의 국내 확대 계획 등에 지지를 받고 있습니다. 미국 반도체와 포토닉스 에코시스템은 숙련된 노동자 부족에도 불구하고 중요한 광학 부품을 다른 어느 지역보다 빠르게 공급하고 장비 업그레이드를 위한 다운타임을 단축하고 있습니다. 보스턴-캠브리지, 샌프란시스코 베이 지역, 롤리-더럼 회랑의 자본 집약적인 바이오파마 클러스터는 함께 북미의 라벨이 없는 설치 베이스 유닛의 40% 이상을 지원합니다.

아시아태평양은 2023년에 2조 4,000억 위안을 돌파해 매년 12%씩 증가하고 있는 중국의 정밀의료 붐 덕분에 CAGR 8.65%에서 가장 급성장하고 있는 지역입니다. 인도의 2024년 BioE3 정책은 바이오 제조업을 전략적 지주로 지정하고 일본의 JST 프로그램은 1조미국의 멀티플렉스 센싱상을 목표로 하고 있습니다. 2027년에 예정된 시마즈 제작소의 카르나타카 신공장은 크로마토그래프와 질량분석계의 생산을 현지화하여 수입 의존도를 삭감합니다. 상하이의 장강과 하이데라바드의 유전체 밸리에 있는 바이오테크놀러지 파크는 스타트업 기업에 보조금을 내고 핵심 시설에 대한 액세스를 제공하고 있으며, 지역 성장을 더욱 뒷받침하고 있습니다.

유럽은 독일, 영국, 스위스의 레거시 제약 측정에 의해 지원되며 중요한 발자국을 남기고 있습니다. 워터스 코퍼레이션이 영국에 신설한 45,000평방피트의 머시닝 센터는 MS 부품의 현지 생산 능력을 3배로 높여 공급망 충격에 대한 내성을 향상시키고 있습니다. 그럼에도 불구하고 업계 단체는 미국과 중국의 인센티브가 웨이퍼 팹 투자를 해외로 유치하는 가운데 포토닉스의 경쟁력을 지키기 위해 '칩스법 2.0'을 제창하고 있습니다. 호라이즌 유럽 보조금과 유럽 혁신 카운실의 자금은 분산형 테스트를 위한 라벨 프리 마이크로플루이딕스 프로토타입을 시험적으로 개발하는 대학-산업 컨소시엄에 계속 자금을 제공합니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월의 애널리스트 서포트

목차

제1장 서론

- 조사의 전제조건 및 시장의 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 표지 검출 기술에 대한 장점

- 제약 및 바이오테크놀러지 기업에 의한 연구 개발비 증가

- SPR, BLI, CDS 플랫폼에서 급속한 기술 업그레이드

- AI 분석과 높은 처리량 라벨 프리 스크리닝의 통합

- 맞춤형 의료 및 세포 치료 제조에 채용

- POC 진단을 위한 나노플라즈모닉 및 메타서피스의 소형화

- 시장 성장 억제요인

- 계측 기기에 대한 고액의 자본 비용

- 유저측의 인식 및 한정된 트레이닝

- 표현형 분석에서의 데이터 통합 및 표준화의 장애물

- 나노광학 제조 인력 부족

- 규제 상황

- Porter's Five Forces 분석

- 신규 참가업체의 위협

- 구매자의 협상력 및 소비자

- 공급기업의 협상력

- 대체품의 위협

- 경쟁 기업 간 경쟁 관계

제5장 시장 규모 및 성장 예측

- 기술별

- 표면 플라즈몬 공명(SPR)

- 국소 표면 플라즈몬 공명(LSPR)

- 바이오 레이어 간섭법(BLI)

- 세포 유전 분광법(CDS)

- 기타 기술

- 용도별

- 창약

- 단백질-단백질 및 계면 분석

- 항체의 특성 평가 및 개발

- 단백질 복합체 및 캐스케이드 분석

- 기타 용도

- 최종 사용자별

- 제약 및 바이오테크놀러지 기업

- 계약연구기관(CRO)

- 학술연구실 및 연구개발실

- 기타 최종 사용자

- 지역

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 기타 유럽

- 아시아태평양

- 중국

- 일본

- 인도

- 호주

- 한국

- 기타 아시아태평양

- 중동 및 아프리카

- GCC

- 남아프리카

- 기타 중동 및 아프리카

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 북미

제6장 경쟁 구도

- 시장 집중도

- 시장 점유율 분석

- 기업 프로파일

- Danaher Corporation(ForteBio/Molecular Devices)

- Bruker Corporation

- Corning Incorporated

- Thermo Fisher Scientific, Inc.

- Sartorius AG(Octet BLI)

- Carterra Inc.

- GE HealthCare

- PerkinElmer, Inc.

- Waters Corporation

- Agilent Technologies

- Nicoya Lifesciences

- Gator Bio

- Malvern Panalytical

- Horiba Ltd.

- Attana AB

- Quanterix Corp.

- Plexera Bioscience

- Fluidic Analytics

- Delta Life Science

- Biosensor Tools LLC

제7장 시장 기회 및 향후 전망

AJY 25.11.03The label-free array systems market is valued at USD 568.06 million in 2025 and is forecast to reach USD 817.04 million by 2030, registering a 7.54% CAGR over 2025-2030.

Escalating pharmaceutical R&D budgets, rising demand for real-time kinetic data, and the migration toward complex biologics are solidifying the technology's role across discovery and development programs. Major sponsors now embed label-free detection early in hit-to-lead cascades to shorten project timelines and improve candidates' success rates. Consolidation among instrument vendors, coupled with AI-enhanced analytics, is accelerating platform upgrades and lowering data-analysis barriers. Meanwhile, regional funding initiatives in North America, the European Union, China, and India are creating a fertile environment for new applications extending into point-of-care diagnostics and cell-therapy manufacturing. Persistent challenges-chiefly high capital outlays for flagship SPR and BLI platforms and a shortage of trained nano-optics personnel-continue to temper adoption in price-sensitive segments, yet shared-facility models and leasing schemes are starting to offset cost hurdles.

Global Label-free Array Systems Market Trends and Insights

Advantages over Labeled Detection Techniques

Label-free methods eliminate fluorescent or radioactive tags, thereby preventing steric hindrance and signal quenching that often distort binding kinetics. Hit rates jump when fragment-based campaigns capitalize on unmodified ligands, as demonstrated by 12.4% primary hits with 92% crystallographic confirmation. Because no secondary reagents are required, assay development time drops 40-60%, freeing medicinal-chemistry teams to iterate rapidly. Stanford University's SENSBIT platform further highlights durability gains by maintaining 70% signal after one month in serum against 11-hour lifespans for conventional sensors. Collectively, these performance premiums underpin the label-free array systems market's swift pivot away from legacy labeled assays.

Increase in R&D Spending by Pharma & Biotech Firms

Global pharmaceutical R&D outlays reached USD 288 billion in 2024, up 1.5% year-on-year, and sizeable fractions are earmarked for advanced analytical platforms. Merck alone channelled USD 17.9 billion into discovery programs, explicitly prioritizing label-free screening capacity. As therapeutics portfolios tilt toward multispecific antibodies, gene editors, and cell therapies, high-content kinetic datasets become mission-critical for regulatory dossiers. Daiichi Sankyo's robotics-enabled San Diego laboratory illustrates this shift, integrating automation and AI-driven label-free analytics to compress bench-to-IND timelines. The resulting uplift in Phase 1 success rates-from 60-70% with traditional screens to 80-90% on AI-paired label-free platforms-reinforces executive commitment to sustained investment.

High Capital Cost of Instrumentation

Premium SPR systems list between USD 200,000 and USD 500,000, while fully featured BLI rigs exceed USD 300,000 before service contracts. Semiconductor labor shortages that could require 67,000 additional U.S. engineers by 2030 inflate optics-component prices. Export restrictions on gallium and germanium have lengthened lead times, and 75% of photonics manufacturers report hiring challenges. Consequently, smaller biotechs and academic centers defer purchases, nudging them toward shared-core facilities or vendor-financed leasing programs that spread cost over multi-year horizons.

Other drivers and restraints analyzed in the detailed report include:

- Rapid Technology Upgrades in SPR, BLI & CDS Platforms

- Integration of AI Analytics with High-Throughput Label-Free Screens

- Limited User-Side Awareness & Training

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Surface Plasmon Resonance contributed 41.45% of 2024 revenue, making it the largest slice of the label-free array systems market. Vendors sustain leadership by pushing sub-nanomolar detection limits and adding multiplex cartridges that measure up to 32 interactions concurrently. The label-free array systems market size attributed to SPR platforms is expected to rise steadily at the overall industry CAGR as pharma customers modernize aging instruments. Localised SPR, however, promises the fastest growth at a 9.65% CAGR because nano-plasmonic metasurfaces deliver superior small-molecule sensitivity and suit portable diagnostics.

National Taiwan University's pH-responsive DNA nanoswitches achieved 0.57 pM microRNA limits of detection, nudging LSPR closer to clinic-ready assays. Parallel advances in whispering-gallery-mode microlasers offer amplified evanescent fields suited to early cancer biomarker panels. The competition is spurring incumbents to incorporate nano-fabricated chips into next-gen SPR lines, blurring boundaries between bulk-optic SPR and chip-based LSPR. As price differentials narrow, procurement decisions will hinge on throughput, service footprint, and AI-analytics plug-ins rather than on raw sensitivity alone.

The Label-Free Array Systems Market Report is Segmented by Technology (Surface Plasmon Resonance (SPR), and More), Application (Drug Discovery, and More), End User (Pharmaceutical & Biotechnology Companies, Contract Research Organizations (CROs), and More), Geography (North America, Europe, Asia-Pacific, The Middle East and Africa, and South America). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America led the label-free array systems market with a 44.56% revenue share in 2024, supported by deep capital pools, FDA-aligned validation pathways, and Thermo Fisher's USD 2 billion domestic expansion plan. U.S. semiconductor and photonics ecosystems, despite skilled-labor shortages, continue to supply critical optics faster than any other region, reducing downtime for instrument upgrades. Capital-intensive biopharma clusters in Boston-Cambridge, the San Francisco Bay Area, and the Raleigh-Durham corridor collectively anchor over 40% of North American label-free install base units.

Asia-Pacific is the fastest-growing territory at an 8.65% CAGR thanks to China's precision-medicine boom, which topped 2,400 billion yuan in 2023 and is rising 12% annually. India's 2024 BioE3 policy designates biomanufacturing as a strategic pillar, while Japan's JST program seeks a USD 1 trillion multiplex-sensing prize. Shimadzu's new Karnataka factory, due 2027, will localize chromatograph and mass-spec production, trimming import dependencies. Regional growth is further bolstered by biotech parks in Shanghai's Zhangjiang and Hyderabad's Genome Valley that offer subsidized core-facility access to start-ups.

Europe holds a meaningful footprint, buoyed by Germany, the United Kingdom, and Switzerland's legacy pharma majors. Waters Corporation's new 45,000 sq ft UK machining center triples local capacity for MS components, improving resilience against supply-chain shocks. Nonetheless, industry groups advocate a "Chips Act 2.0" to protect photonics competitiveness as U.S. and Chinese incentives lure wafer-fab investments abroad. Horizon Europe grants and European Innovation Council funds continue to seed university-industry consortia that pilot label-free microfluidic prototypes for decentralized testing.

- Danaher Corporation (ForteBio / Molecular Devices)

- Bruker

- Corning

- Thermo Fisher Scientific

- Sartorius AG (Octet BLI)

- Carterra Inc.

- GE Healthcare

- PerkinElmer

- Waters Corporation

- Agilent Technologies

- Nicoya Lifesciences

- Gator Bio

- Malvern Panalytical

- HORIBA

- Attana AB

- Quanterix Corp.

- Plexera Bioscience

- Fluidic Analytics

- Delta Life Science

- Biosensor Tools LLC

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Advantages Over Labeled Detection Techniques

- 4.2.2 Increase In R&D Spending by Pharma & Biotech Firms

- 4.2.3 Rapid Technology Upgrades In SPR, BLI & CDS Platforms

- 4.2.4 Integration Of AI Analytics with High-Throughput Label-Free Screens

- 4.2.5 Adoption In Personalised-Medicine & Cell-Therapy Manufacturing

- 4.2.6 Nano-Plasmonic & Metasurface Miniaturisation for POC Diagnostics

- 4.3 Market Restraints

- 4.3.1 High Capital Cost of Instrumentation

- 4.3.2 Limited User-Side Awareness & Training

- 4.3.3 Data-Integration & Standardisation Hurdles for Phenotypic Assays

- 4.3.4 Shortage Of Nano-Optics Fabrication Talent

- 4.4 Regulatory Landscape

- 4.5 Porter's Five Forces Analysis

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Buyers/Consumers

- 4.5.3 Bargaining Power of Suppliers

- 4.5.4 Threat of Substitute Products

- 4.5.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Technology

- 5.1.1 Surface Plasmon Resonance (SPR)

- 5.1.2 Localised Surface Plasmon Resonance (LSPR)

- 5.1.3 Bio-Layer Interferometry (BLI)

- 5.1.4 Cellular Dielectric Spectroscopy (CDS)

- 5.1.5 Other Technologies

- 5.2 By Application

- 5.2.1 Drug Discovery

- 5.2.2 Protein-Protein / Interface Analysis

- 5.2.3 Antibody Characterisation & Development

- 5.2.4 Protein Complex & Cascade Analysis

- 5.2.5 Other Applications

- 5.3 By End User

- 5.3.1 Pharmaceutical & Biotechnology Companies

- 5.3.2 Contract Research Organisations (CROs)

- 5.3.3 Academic & R&D Laboratories

- 5.3.4 Other End Users

- 5.4 Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 Europe

- 5.4.2.1 Germany

- 5.4.2.2 United Kingdom

- 5.4.2.3 France

- 5.4.2.4 Italy

- 5.4.2.5 Spain

- 5.4.2.6 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 Japan

- 5.4.3.3 India

- 5.4.3.4 Australia

- 5.4.3.5 South Korea

- 5.4.3.6 Rest of Asia-Pacific

- 5.4.4 Middle East & Africa

- 5.4.4.1 GCC

- 5.4.4.2 South Africa

- 5.4.4.3 Rest of Middle East & Africa

- 5.4.5 South America

- 5.4.5.1 Brazil

- 5.4.5.2 Argentina

- 5.4.5.3 Rest of South America

- 5.4.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and analysis of Recent Developments)

- 6.3.1 Danaher Corporation (ForteBio / Molecular Devices)

- 6.3.2 Bruker Corporation

- 6.3.3 Corning Incorporated

- 6.3.4 Thermo Fisher Scientific, Inc.

- 6.3.5 Sartorius AG (Octet BLI)

- 6.3.6 Carterra Inc.

- 6.3.7 GE HealthCare

- 6.3.8 PerkinElmer, Inc.

- 6.3.9 Waters Corporation

- 6.3.10 Agilent Technologies

- 6.3.11 Nicoya Lifesciences

- 6.3.12 Gator Bio

- 6.3.13 Malvern Panalytical

- 6.3.14 Horiba Ltd.

- 6.3.15 Attana AB

- 6.3.16 Quanterix Corp.

- 6.3.17 Plexera Bioscience

- 6.3.18 Fluidic Analytics

- 6.3.19 Delta Life Science

- 6.3.20 Biosensor Tools LLC

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment