|

시장보고서

상품코드

1848326

혈관 폐쇄 기기 시장 : 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Vascular Closure Device - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

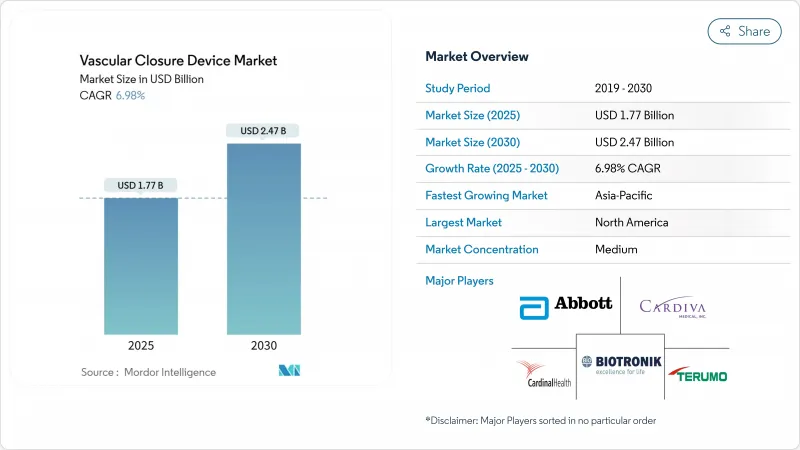

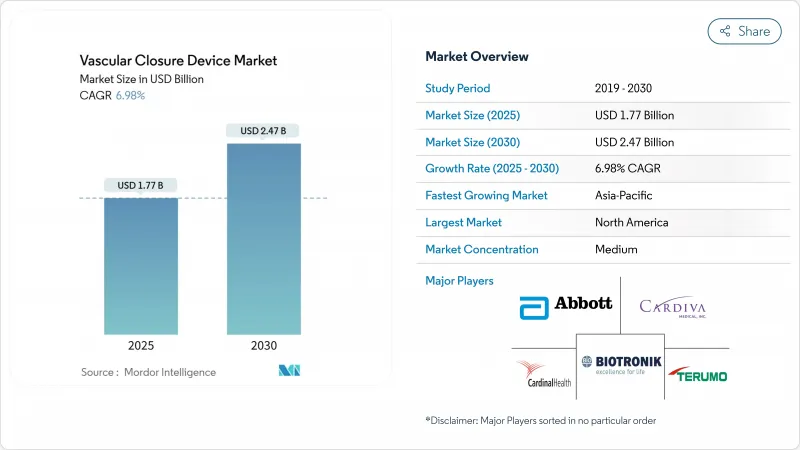

혈관 폐쇄 기기 시장 규모는 2025년에 17억 7,000만 달러로 추정되고, 2030년에는 24억 7,000만 달러에 이를 것으로 예상되며, 예측 기간 중 CAGR 6.98%로 성장할 전망입니다.

경 카테터 대동맥 판막 치환술(TAVR), 혈관내 동맥류 수복술(EVAR), 신경 인터벤션, 복잡한 말초 사례에서의 절차의 복잡화는 혈관 폐쇄를 현대 혈관 내 치료에서 필수적인 단계로 자리잡고 있습니다. 25Fr까지의 대구경 접근 부위에서는 예측 가능한 지혈이 요구되고, 또 당일 퇴원에서는 신속한 이동이 요구되기 때문에 구매자의 기호는 수동의 압박으로부터 멀어지고 있습니다. 외래 환자 수 증가, 고위험 노인 환자에 대한 저침습 치료의 채택, 외래 치료에 대한 상환 확대는 기기 기반 폐쇄 비즈니스 사례를 강화하고 있습니다. 기술 혁신의 기세가 가장 강한 것은 생체 흡수성 재료 및 대구경 임플란트의 디자인이며, 이로써 전개 시간이 단축되어, 술자의 편차가 해소됩니다. 동시에, 요골에 특화된 압박 밴드는 대퇴골에서 요골 루트로의 수술적 전환에 대응하여 혈관 폐쇄 기기 시장이 정체되지 않고 계속 진화할 수 있도록 보장하고 있습니다.

세계의 혈관 폐쇄 기기 시장 동향 및 인사이트

카테터 관련 시술 증가

경피적 관상동맥 인터벤션, 심장 구조 수복, 복잡한 말초 혈액 순환 재건술의 적응이 확대됨에 따라 수술은 증가하고 있습니다. Abbot은 혈관 폐쇄 제품이 2025년 1분기 의료기기 매출 성장률 12.5%의 주요 요인임을 확인했습니다. 기계적 혈전 제거술과 높은 외장 전기 생리학적 치료는 환자 1인당 여러 개의 천자 부위를 필요로 하기 때문에 술자는 다양한 크기의 혈관을 안정된 치료 성과로 관리할 수 있는 폐쇄 시스템을 요구하고 있습니다. AMBULATE와 같은 임상시험은 수작업으로 인한 압박을 VASCADE MVP 시스템으로 대체할 때 보행까지의 시간이 54% 단축되었음을 보여주며 워크플로우 개선이 강조되었습니다. 이러한 역학을 종합하면 수기 건수 증가가 혈관 폐쇄 기기 시장의 지속적인 촉매가 됩니다.

저침습 치료에 대한 선호도 증가

병원과 외래 센터에서는 재원 일수의 단축, 감염 위험의 저감, 환자의 만족도 향상을 위해, 저침습 치료가 선호되고 있습니다. 심장 리듬 학회와 미국 심장병 학회는 확실한 정맥 지혈이 달성되면 심근 내 절제 후 당일 퇴원을 권장하며 폐쇄술의 성능은 처리량과 직접 연결됩니다. Termo의 심장 및 혈관 회사의 수익이 15.6% 급증한 것은 이 거대 이동에 따른 것으로 견고한 폐쇄 도구가 카테터 기반 치료의 채택을 가속화하는 방법을 보여줍니다. 영상 진단 네비게이션의 향상은 작은 천자로 치료 가능한 병변의 범위를 더욱 넓혀 액세스를 신속하고 예측 가능하게 봉쇄하는 혈관 폐쇄 기기 시장의 솔루션에 대한 의존도를 높이고 있습니다.

수동 압박에 비해 고급 VCD의 높은 비용

단일 폐쇄 장치는 일반적으로 200-250달러 수준이지만, 수동 압박에 필요한 재료비는 거의 들지 않습니다. 고소득 국가의 의료체계에서는 인력 시간을 절감할 수 있어 이러한 지출을 정당화할 수 있는 반면, 많은 신흥 시장에서는 예산 관리를 위해 여전히 수동 압박에 의존하고 있습니다. 가치 기반 구매는 점차 시술과 관련된 전체 치료 과정에서 발생하는 비용까지 고려하는 방식으로 이동하고 있으나, 자본이 부족한 시장에서는 가격 민감도가 여전히 높으며, 특히 카테터 시술 건수가 이제 막 증가하고 있는 지역에서 두드러집니다. 이에 제조사들은 제품 라인을 단계화하고, 간호 시간 감소와 입원 기간 단축 효과를 강조한 맞춤형 상환 자료를 제시하며 대응하고 있습니다.

부문 분석

2024년 혈관 폐쇄 기기 시장의 54.34%를 액티브 근사기가 차지했습니다. 이 리더십은 봉합사를 통하거나 클립 기반 메커니즘이 동맥 절개를 즉시 잠그고 항응고 치료를 받거나 대구경 환자가 몇 시간 이내에 걸을 수 있게 하는 것에 기인합니다. Abbot의 Perclose ProGlide는 여러 하이시스 테스트에서 100%의 성공적인 절차를 거쳤으며 이 카테고리의 강도를 보여줍니다. 병원은 특히 수술 중 항응고 요법이 필수인 경우 이러한 기구가 제공하는 결정론적 폐쇄를 높이 평가합니다.

패시브형 근사기는 베이스가 작지만, 2030년까지 CAGR 8.45%로 성장할 전망입니다. Haemonetics의 VASCADE MVP와 같은 플러그, 패치 및 실런트 시스템은 배치가 원 푸시로 단축되어 투시 및 운영자의 피로를 완화합니다. AMBULATE 연구는 앙뷰레이션에 소요되는 시간이 54% 단축되었음을 확인하여 외래 환자 프로그램에 유익한 워크플로우를 보여주었습니다. 간소화된 절차는 훈련 장벽을 낮추고 중간 규모 시설에서의 채용을 증가시킵니다. 규제 당국의 압력에 의해 같은 날 퇴원이 선호되는 가운데, 수동적 근사기는 혈관 폐쇄 기기 시장에 대한 공헌을 확대하는 입장에 있습니다.

콜라겐 플러그는 2024년에 51.23%의 점유율을 유지했으며, 30년에 걸친 임상적인 친근함을 반영합니다. Termo의 Angio-Seal VIP는 콜라겐 스폰지, 폴리머 앵커 및 봉합사로 구성되며, 모두 90일 이내에 흡수되므로 혈관 치유를 예측할 수 있습니다. 의사는 콜라겐의 트롬빈이 풍부한 매트릭스를 높이 평가하고 있으며, 특히 항응고 치료를 받는 환자에서 혈전 형성을 촉진합니다.

폴리글리콜산, 폴리에틸렌 글리콜 또는 독특한 폴리머로 만든 봉합사와 필라멘트 장치는 CAGR 8.95%로 발전하고 있습니다. Vivasure사의 PerQseal Elite는 완전히 생체 흡수성으로 14-22Fr의 TAVR 시스용으로 설계되어 이물체의 체류나 화상 아티팩트를 배제하고 있습니다. 폴리머의 기술 혁신으로 분해 속도를 조정하여 영구 임플란트를 사용하지 않고 대구경의 안전성을 확보할 수 있습니다. 클립 기반 금속 시스템은 엑스레이 불투과성 마커가 추적 영상 진단에 도움이 되는 사례를 위한 틈새 시스템입니다. 소재의 다양화로 혈관 폐쇄 기기 시장에서 경쟁사와의 차별화가 강화되고 있습니다.

지역 분석

북미는 42.67%의 점유율을 차지하며, 혈관 폐쇄 기기 시장의 최대 지역 구성국가가 되고 있습니다. 1인당 시술률의 높이, 조기 기술 도입, 견고한 상환의 틀이 리더십을 지원하고 있습니다. FDA는 2024년 코디스의 MYNX CONTROL 정맥 VCD를 510(k) 인가하고 있으며, 이 지역이 차세대 시스템의 주요 게이트웨이 역할을 담당하고 있음을 강조합니다. 리콜에도 불구하고 북미는 체계적인 교육과 시판 후 조사를 통해 의사의 신뢰를 유지하고 있습니다.

아시아태평양은 2030년까지 연평균 복합 성장률(CAGR)로 가장 빠른 7.84%로 성장할 전망이며, 의료 인프라 정비, 심혈관 치료에 대한 정부 투자, 협착성 질환 및 변막증이 되기 쉬운 고령화 사회가 박차를 가하고 있습니다. 중국의 국가의료제품관리국은 2023년에 61건의 혁신적인 의료기기 신청을 접수하였으며, 국내외 공급업체에 대한 규제 당국의 대응이 가속화되고 있음을 나타냅니다. Termo의 심장혈관 매출은 2자리 성장했으며, 마이크로 포트 카디오 플로우의 VitaFlow Liberty TAVI는 2025년초에 승인되었습니다. 의료기기의 비용에 민감한 경향은 변하지 않지만, 민간 보험 및 공적 조성의 확대에 의해 구입하기 쉬운 가격이 되고 있습니다.

유럽에서는 의료기기 규제 프레임워크로의 이행이 진행되는 가운데 완만하면서도 꾸준한 확대를 유지하고 있습니다. Termo의 Angio-Seal VIP와 Vivasure의 PerQseal Elite가 MDR의 CE 마크를 획득하면 제조업체의 적응 능력이 높습니다. 북미 대륙의 센터에서 레이디얼 유치의 보급률은 북미보다 높고 대퇴골 폐쇄술의 증례 수는 감소하고 있지만, 대구경의 구조적 심장 유치술의 증례 수는 증가하고 있어 감소를 보충하고 있습니다. 남유럽의 경제적 압력은 비싼 장치의 도입을 억제하고 있지만 북유럽 네트워크는 기술 혁신으로 보완되어 혈관 폐쇄 기기 시장을 유지하고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월의 애널리스트 서포트

자주 묻는 질문

목차

제1장 서론

- 조사의 전제조건 및 시장의 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 카테터 관련 처치 증가

- 저침습 개입에 대한 관심 증가

- PCI 및 전기 생리학에서 요골 동맥 접근으로의 전환

- 고령화 사회에서의 CVD 치료 건수의 확대

- 대구경 TAVR/EVAR의 확대가 차세대 VCD 수요 견인

- 외래 및 당일 퇴원 환불 인센티브

- 시장 성장 억제요인

- 고급 VCD의 고비용 및 수동 압축의 비교

- 디바이스 관련 합병증 및 제품 리콜

- 생체 흡수성 폴리머의 긴 승인 사이클

- 저비용 레이디얼 압축 밴드로부터의 공식

- 규제 상황

- Porter's Five Forces 분석

- 신규 참가업체의 위협

- 구매자의 협상력

- 공급기업의 협상력

- 대체품의 위협

- 경쟁 기업간 경쟁 관계

제5장 시장 규모 및 성장 예측

- 제품 유형별

- 액티브 근사기

- 클립 기반 기기

- 봉합 기반 기기

- 플러그 기반 기기

- 패시브 근사기

- 지혈 패드 및 패치

- 압축 장치

- 액티브 근사기

- 재료 조성별

- 콜라겐베이스

- PEG 및 폴리머 베이스

- 봉합사 및 필라멘트 베이스

- 금속 클립 베이스

- 액세스 모드별

- 대퇴골 접근

- 대구경 대퇴골

- 레이디얼 액세스

- 기타 액세스 방법

- 처치 유형별

- 인터벤셔널 카디올로지

- 말초 혈관

- 신경혈관

- 구조적 심장 및 TAVR

- 전기 생리학

- 최종 사용자별

- 병원

- 외래수술센터(ASC)

- 카테터 검사실 및 외래 혈관 센터

- 지역

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 기타 유럽

- 아시아태평양

- 중국

- 일본

- 인도

- 호주

- 한국

- 기타 아시아태평양

- 중동 및 아프리카

- GCC

- 남아프리카

- 기타 중동 및 아프리카

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 북미

제6장 경쟁 구도

- 시장 집중도

- 시장 점유율 분석

- 기업 프로파일

- Abbott Laboratories

- Terumo Corporation

- Medtronic plc

- Haemonetics Corp.

- Teleflex Inc.

- Cardinal Health/Cordis

- Becton, Dickinson & Co.

- B. Braun Melsungen AG

- Biotronik SE & Co. KG

- Merit Medical Systems

- Vivasure Medical Ltd

- Cardiva Medical Inc.

- Advanced Vascular Dynamics

- Essential Medical

- InSeal Medical

- Manta(Abbott-Manta)

- Forge Medical

- Rex Medical

- Morrison Medical

- Medeon Biodesign

제7장 시장 기회 및 향후 전망

AJY 25.11.03The vascular closure devices market size is valued at USD 1.77 billion in 2025 and is forecast to reach USD 2.47 billion by 2030, registering a 6.98% CAGR over the period.

Heightened procedural complexity in transcatheter aortic valve replacement (TAVR), endovascular aneurysm repair (EVAR), neuro-interventions, and complex peripheral cases positions vascular closure as an indispensable step in contemporary endovascular therapy. Purchaser preference is tilting away from manual compression because large-bore access sites up to 25 Fr demand predictable hemostasis, and same-day discharge mandates rapid ambulation. Growing outpatient volumes, adoption of minimally invasive therapies for high-risk elderly patients, and expanding reimbursement for ambulatory care are reinforcing the business case for device-based closure. Innovation momentum is strongest in bio-absorbable materials and large-bore implant designs that shorten deployment time and remove operator variability. Concurrently, radial-specific compression bands address the procedural migration from femoral to radial routes, ensuring that the vascular closure devices market continues to evolve rather than stagnate.

Global Vascular Closure Device Market Trends and Insights

Increase in Catheterization-Related Procedures

Procedure counts have escalated as indications for percutaneous coronary interventions, structural heart repair, and complex peripheral revascularization broaden. Abbott confirmed that vessel closure products were a key contributor to its 12.5% medical devices revenue growth in Q1 2025, reflecting direct linkage between access-site volumes and device demand. Mechanical thrombectomy and high-sheath electrophysiology cases produce multiple puncture sites per patient, pushing operators toward closure systems that manage varied vessel sizes with consistent outcomes. Trials such as AMBULATE demonstrated a 54% reduction in time to ambulation when the VASCADE MVP system replaced manual compression, underscoring workflow gains. Together, these dynamics position procedural volume growth as a persistent catalyst for the vascular closure devices market.

Growing Preference for Minimally Invasive Interventions

Hospitals and ambulatory centers favor minimally invasive care to trim length of stay, reduce infection risk, and improve patient satisfaction. The Heart Rhythm Society and the American College of Cardiology endorse same-day discharge after intracardiac ablation when secure venous hemostasis is achieved, directly tying closure performance to throughput. Terumo's 15.6% revenue jump in its Cardiac & Vascular Company aligns with this macro-shift and illustrates how robust closure tools accelerate adoption of catheter-based therapies. Imaging navigation improvements further widen the scope of lesions treatable through small punctures, amplifying reliance on vascular closure devices market solutions that seal access quickly and predictably.

High Cost Of Advanced VCDs Versus Manual Compression

A single closure unit often prices between USD 200 and USD 250, contrasted with negligible material cost for manual compression. While high-income systems justify expenditure through staff time savings, many emerging markets still rely on manual pressure to contain budgets. Value-based purchasing is gradually shifting toward total episode economics, but capital scarcity keeps price sensitivity high, especially where catheter volumes are just now scaling. Manufacturers are responding with tiered product lines and targeted reimbursement dossiers that highlight reduced nursing hours and shorter admissions.

Other drivers and restraints analyzed in the detailed report include:

- Aging Population Expanding Cardiovascular Treatment Volumes

- Expansion of Large-Bore TAVR/EVAR Driving Next-Gen Device Demand

- Device-Related Complications And Product Recalls

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Active approximators controlled 54.34% of the vascular closure devices market in 2024. This leadership derives from their suture-mediated or clip-based mechanisms that lock arteriotomies immediately, enabling anticoagulated or large-bore patients to ambulate within hours. Abbott's Perclose ProGlide illustrates category strength by offering 100% procedural success in multiple high-sheath trials. Hospitals prize the deterministic closure these devices provide, particularly when intra-procedural anticoagulation is mandatory.

Passive approximators occupy a smaller base but are pacing growth at 8.45% CAGR through 2030. Plug, patch, and sealant systems such as Haemonetics' VASCADE MVP shorten deployment to a single push, reducing fluoroscopy and operator fatigue. The AMBULATE study confirmed a 54% decline in time-to-ambulation, showcasing workflow dividends that resonate with outpatient programs. Simplified technique lowers training barriers, raising adoption in mid-volume centers. As regulatory pressures favor same-day discharge, passive approximators are positioned to expand their contribution to the vascular closure devices market.

Collagen plugs retained 51.23% share in 2024, reflecting three decades of clinical familiarity. Terumo's Angio-Seal VIP employs a collagen sponge, a polymer anchor, and a suture that collectively resorb within 90 days, offering predictable vessel healing. Physicians value collagen's thrombin-rich matrix, which accelerates clot formation especially in anticoagulated patients.

Suture and filament devices built from polyglycolic acid, polyethylene glycol, or proprietary polymers are advancing at 8.95% CAGR. Vivasure's PerQseal Elite is entirely bio-absorbable and designed for 14-22 Fr TAVR sheaths, eliminating retained foreign material and imaging artifacts. Polymer innovations provide tailored degradation kinetics, enabling large-bore security without permanent implants. Clip-based metal systems remain a niche for cases where radiopaque markers aid follow-up imaging. Material diversification reinforces competitive differentiation inside the vascular closure devices market.

The Vascular Closure Device Market Report is Segmented by Product Type (Active Approximators and Passive Approximators), Material Composition (Collagen-Based, PEG/Polymer-based, and More), Mode of Access (Femoral Access), Procedure Type (Interventional Cardiology, and More), End-User (Hospitals, and More), Geography (North America, Europe, Asia-Pacific, and More). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America, with 42.67% share, remains the largest regional constituent of the vascular closure devices market. High per-capita procedure rates, early technology adoption, and robust reimbursement frameworks underpin leadership. The FDA granted 510(k) clearance for Cordis' MYNX CONTROL venous VCD in 2024, emphasizing the region's role as a primary gateway for next-generation systems. Notwithstanding recalls, North America maintains physician confidence through structured training and rapid post-market surveillance.

Asia-Pacific records the fastest 7.84% CAGR through 2030, spurred by health infrastructure build-out, government investment in cardiovascular care, and an aging population predisposed to stenotic and valvular disease. China's National Medical Products Administration accepted 61 innovative device dossiers in 2023, signaling accelerating regulatory throughput for local and foreign suppliers. Terumo's double-digit cardiovascular revenue growth and MicroPort CardioFlow's VitaFlow Liberty TAVI approval in early 2025 confirm vibrant regional demand. Although device cost sensitivity persists, expanding private insurance and public funding improve affordability.

Europe maintains steady, albeit slower, expansion amid transition to the Medical Device Regulation framework. CE marks awarded to Terumo's Angio-Seal VIP and Vivasure's PerQseal Elite under MDR attest to adaptability of manufacturers. Radial penetration in continental centers is higher than in North America, moderating femoral closure volumes, yet growth in large-bore structural heart programs counterbalances attrition. Economic pressures in Southern Europe constrain premium device uptake, but Northern European networks compensate with procedure innovation, sustaining the vascular closure devices market.

- Abbott Laboratories

- Terumo

- Medtronic

- Haemonetics Corp.

- Teleflex

- Cardinal Health / Cordis

- Beckton Dickinson

- B. Braun

- BIOTRONIK

- Merit Medical Systems

- Vivasure Medical

- Cardiva Medical

- Advanced Vascular Dynamics

- Essential Medical

- InSeal Medical

- Manta (Abbott-Manta)

- Forge Medical

- Rex Medical

- Morrison Medical

- Medeon Biodesign

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Increase In Catheterization-Related Procedures

- 4.2.2 Growing Preference for Minimally Invasive Interventions

- 4.2.3 Shift Toward Radial Access in PCI & Electrophysiology

- 4.2.4 Aging Population Expanding CVD Treatment Volumes

- 4.2.5 Expansion Of Large-Bore TAVR/EVAR Driving Next-Gen VCD Demand

- 4.2.6 Out-Patient & Same-Day Discharge Reimbursement Incentives

- 4.3 Market Restraints

- 4.3.1 High Cost of Advanced Vcds Vs. Manual Compression

- 4.3.2 Device-Related Complications & Product Recalls

- 4.3.3 Lengthy Approval Cycles for Bio-Absorbable Polymers

- 4.3.4 Cannibalisation From Low-Cost Radial Compression Bands

- 4.4 Regulatory Landscape

- 4.5 Porter's Five Forces Analysis

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Bargaining Power of Suppliers

- 4.5.4 Threat of Substitutes

- 4.5.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Product Type

- 5.1.1 Active Approximators

- 5.1.1.1 Clip-based Devices

- 5.1.1.2 Suture-based Devices

- 5.1.1.3 Plug-based Devices

- 5.1.2 Passive Approximators

- 5.1.2.1 Hemostatic Pads & Patches

- 5.1.2.2 Compression Devices

- 5.1.1 Active Approximators

- 5.2 By Material Composition

- 5.2.1 Collagen-based

- 5.2.2 PEG / Polymer-based

- 5.2.3 Suture / Filament-based

- 5.2.4 Metal Clip-based

- 5.3 By Mode of Access

- 5.3.1 Femoral Access

- 5.3.2 Large-bore Femoral

- 5.3.3 Radial Access

- 5.3.4 Other Mode of Access

- 5.4 By Procedure Type

- 5.4.1 Interventional Cardiology

- 5.4.2 Peripheral Vascular

- 5.4.3 Neurovascular

- 5.4.4 Structural Heart / TAVR

- 5.4.5 Electrophysiology

- 5.5 By End User

- 5.5.1 Hospitals

- 5.5.2 Ambulatory Surgical Centres

- 5.5.3 Cath-labs & Out-patient Vascular Centres

- 5.6 Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 Europe

- 5.6.2.1 Germany

- 5.6.2.2 United Kingdom

- 5.6.2.3 France

- 5.6.2.4 Italy

- 5.6.2.5 Spain

- 5.6.2.6 Rest of Europe

- 5.6.3 Asia-Pacific

- 5.6.3.1 China

- 5.6.3.2 Japan

- 5.6.3.3 India

- 5.6.3.4 Australia

- 5.6.3.5 South Korea

- 5.6.3.6 Rest of Asia-Pacific

- 5.6.4 Middle East & Africa

- 5.6.4.1 GCC

- 5.6.4.2 South Africa

- 5.6.4.3 Rest of Middle East & Africa

- 5.6.5 South America

- 5.6.5.1 Brazil

- 5.6.5.2 Argentina

- 5.6.5.3 Rest of South America

- 5.6.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and analysis of Recent Developments)

- 6.3.1 Abbott Laboratories

- 6.3.2 Terumo Corporation

- 6.3.3 Medtronic plc

- 6.3.4 Haemonetics Corp.

- 6.3.5 Teleflex Inc.

- 6.3.6 Cardinal Health / Cordis

- 6.3.7 Becton, Dickinson & Co.

- 6.3.8 B. Braun Melsungen AG

- 6.3.9 Biotronik SE & Co. KG

- 6.3.10 Merit Medical Systems

- 6.3.11 Vivasure Medical Ltd

- 6.3.12 Cardiva Medical Inc.

- 6.3.13 Advanced Vascular Dynamics

- 6.3.14 Essential Medical

- 6.3.15 InSeal Medical

- 6.3.16 Manta (Abbott-Manta)

- 6.3.17 Forge Medical

- 6.3.18 Rex Medical

- 6.3.19 Morrison Medical

- 6.3.20 Medeon Biodesign

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment