|

시장보고서

상품코드

1849808

네트워크 분석 : 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Network Analytics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

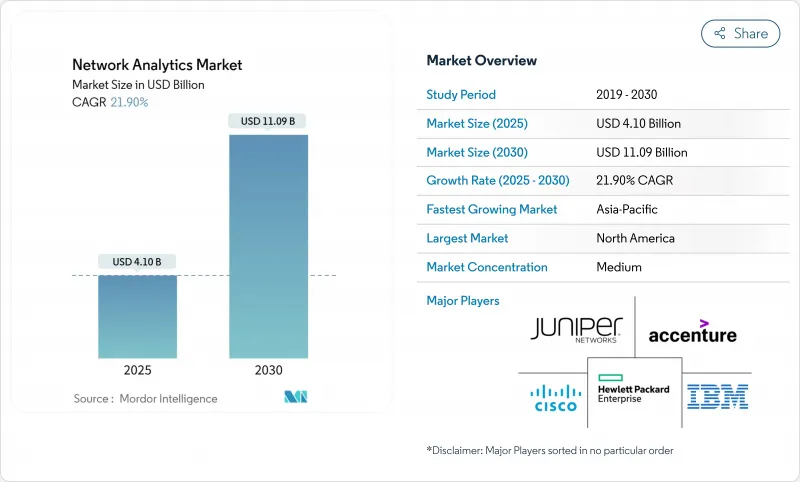

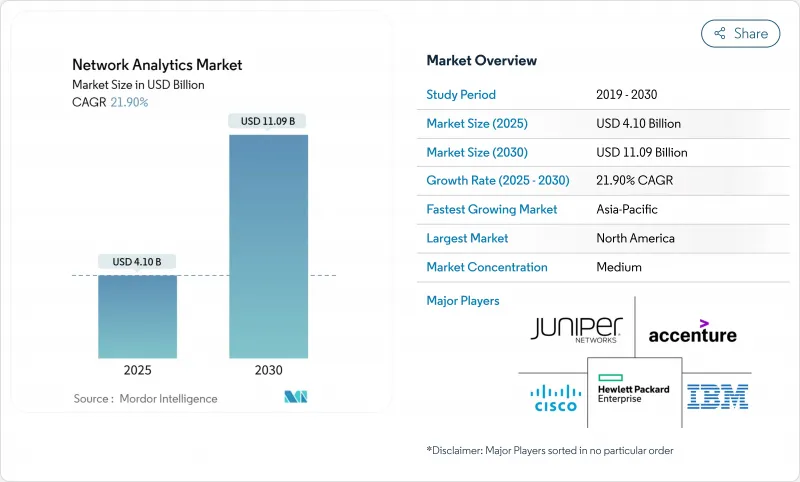

네트워크 분석 시장은 2025년에 41억 달러의 현재 가치를 보유하고 있으며, 2030년에는 110억 9,000만 달러에 이르고, CAGR 21.9%를 나타낼 것으로 예측됩니다.

급속한 데이터 트래픽 증가, 5G 배포, 연결 장치의 급증으로 네트워크 분석은 단순한 모니터링에서 디지털 인프라 전략의 핵심 요소로 밀어 올랐습니다. 기업은 애널리틱스를 예측 보전, 용량 계획, 보안에 필수적이라고 생각하며, 서비스 제공업체는 프로그래머블 네트워크의 수익화에 활용하고 있습니다. 인공지능은 현재 대부분의 주요 플랫폼을 지원하고 있으며, 기술계 이그제큐티브의 60%는 AI를 활용한 자동화를 계획하고 운영의 합리화를 도모하고 있습니다. IBM의 HashiCorp의 64억 달러 인수로 대표되는 공급업체 간의 통합은 애널리틱스를 보다 광범위한 IT 관리와 통합하는 엔드 투 엔드 스택에 대한 수요를 보여줍니다. 초기 비용의 높이나 전문 기술의 부족이 여전히 도입의 방해가 되고 있는 것, 클라우드 제공 모델이나 매니지드 서비스가 진입 장벽을 완화하고 있습니다.

세계의 네트워크 분석 시장 동향과 인사이트

자율 및 자체 관리 네트워크에 대한 요구

네트워크 복잡성과 다운타임 비용(클라우드 중심 기업에서는 분당 9,000달러)이 증가함에 따라 자체 복구 인프라에 대한 수요가 증가하고 있습니다. AI가 장착된 분석 플랫폼을 사용하면 장애를 예측하고 복구하여 문제 해결을 사후 대응에서 사전 대응으로 최적화할 수 있습니다. 미션 크리티컬 워크로드를 실행하는 아키텍처에서는 AIOps에 대한 의존도가 높아지고 있으며, IT 리더의 72%가 애널리틱스, 자동화, 관측 가능성을 통합한 플랫폼 기반 아키텍처를 계획하고 있습니다. 결과적으로 공급업체는 실시간 비정상 감지와 정책 기반 오케스트레이션을 통합하여 평균 수리 시간을 단축하고 서비스 수준 목표를 보호합니다.

IoT와 기계 간 통신의 상승

네트워크 분석 플랫폼은 이기종 트래픽을 관리하기 위해 장치 수준 시각화, 프로토콜 디코딩 및 비헤이비어 기반 라이닝을 추가했습니다. 제조업, 유틸리티, 스마트시티의 전개는 실시간 분석이 예지보전과 에너지 최적화를 지원하여 측정가능한 비용 절감과 가동시간 개선을 실현합니다.

높은 초기 비용과 불투명한 투자 수익률

종합적인 배포에는 소프트웨어 라이선스, 원격 측정 가능 하드웨어, 시스템 통합 및 직원 교육이 필요합니다. 정전을 줄이고 고객 경험을 향상시키는 재무 수익을 정량화하는 것은 특히 중소규모 조직에서 여전히 어렵습니다. 구독 기반 클라우드 배포는 자본 부담을 완화하지만 신흥 경제 지역에서는 예산 급박이 여전히 도입을 늦추고 있습니다.

부문 분석

클라우드 도입은 CAGR 24%로 확대되어 네트워크 분석 시장 전체를 웃돌았습니다. 이러한 움직임은 탄력적인 확장성, 종량 과금제의 경제성, 분산된 팀에 대한 접근성 등에 밀려있습니다. 이러한 기세에도 불구하고 On-Premise 설치는 보안과 소블린 요구 증가로 인해 2024년에는 56%의 매출을 유지했습니다. 하이브리드 아키텍처는 레거시 투자와 미래의 민첩성을 다루는 조직으로 지지를 모으고 있으며 금융기관에서는 91%가 이미 클라우드의 현대화에 착수하고 있습니다.

하이브리드의 운영 형태는 현실적인 관점을 보여줍니다. 엄격한 데이터 관리 요구 사항이 있는 워크로드는 On-Premise에 남아 있으며 폭발적인 분석 작업은 퍼블릭 클라우드로 마이그레이션됩니다. 이 이중성은 거버넌스를 희생하지 않고 비용 최적화를 지원합니다. 애널리스트에 따르면 기업 워크로드의 30%는 현재 퍼블릭 클라우드에 있으며 애널리틱스와 DevOps가 마이그레이션을 주도하고 있다고 합니다. 공급업체는 컨테이너화된 컬렉터, SaaS 대시보드, 프라이빗 및 퍼블릭 영역을 통한 통합 정책 엔진을 제공함으로써 대응합니다. 지속적인 통합 파이프라인은 애널리틱스를 일상 업무에 더욱 통합하여 개발 주기를 압축합니다.

2024년 수익은 솔루션이 63%를 차지했지만 조직이 전문 지식을 요구하기 때문에 서비스는 매년 23.1% 성장할 것으로 예측됩니다. 컨설팅 및 통합 계약은 애널리틱스 아키텍처를 비즈니스 목표에 맞추고 관리 서비스는 매일 튜닝 및 규칙 유지 관리를 오프로드합니다. 서비스 파동은 보다 광범위한 IT 아웃소싱 패턴을 반영하며, 매니지드 서비스 제공업체 분야는 2024년에 3,500억 달러에 이르렀고, 2033년에는 1조 달러 이상에 달할 것으로 예상됩니다.

서비스 파트너는 성능에 대한 인사이트를 비즈니스 성과에 연결하는 AI 중심의 권고 서비스를 제공합니다. 이러한 모델을 채용하는 기업에서는 20-30%의 비용 절감과 최대 25%의 생산성 향상이 보고되었습니다. 수요에 부응하기 위해 벤더는 런북, 사전 학습된 모델, 원격 SOC 기능을 패키징하여 가치 제공 시간을 단축하고 AI의 기술 격차를 완화합니다. 이러한 진화로 서비스는 네트워크 분석 시장의 핵심으로 확고한 지위를 구축하고 지속적인 수익과 고객과의 깊은 관계를 구축하고 있습니다.

지역 분석

북미는 조기 도입, 대규모 IT 예산, 선진적인 공급업체 에코시스템에 지지되어 2024년에 38%의 매출 점유율을 유지했습니다. 미국 금융 서비스 및 건강 관리 회사는 엄격한 가동 시간과 개인 정보 보호 요구 사항을 충족하기 위해 AI를 통합한 분석을 도입했습니다. 캐나다 통신 사업자는 애널리틱스를 활용하여 전국적인 5G 배포를 최적화하고 지역의 커버 의무를 관리합니다. 규제의 명확화와 풍부한 인재는 예측 자동화 실험을 촉진하며, 이 지역은 혁신의 최전선에 위치하고 있습니다.

아시아태평양은 2030년까지 연평균 복합 성장률(CAGR)이 23.3%로 가장 급성장하고 있는 지역입니다. 중국과 인도는 대규모 5G, 스마트 시티, 산업용 IoT 프로젝트에 자금을 제공하고 있으며, 멀티벤더 환경에 대한 세밀한 가시성이 요구되고 있습니다. 일본과 한국은 인공지능과 네트워크 모니터링를 통합하여 자율주행차 테스트 및 공장 자동화를 지원하고 호주는 애널리틱스를 활용하여 중요한 인프라를 사이버 위협으로부터 보호하고 있습니다.

유럽은 엄격한 규제와 보안 의식의 고조 속에서 전진. 영국과 독일은 금융서비스와 제조업 채택을 선도하고 있으며, 하이브리드 아키텍처 전반에 걸쳐 GDPR(EU 개인정보보호규정)을 준수하는 인사이트를 요구하고 있습니다. 프랑스와 이탈리아는 경쟁이 치열한 모바일 시장에서 고객 만족도를 유지하기 위해 통신 사업자의 도입을 강화. 북유럽과 동유럽의 에너지 및 유틸리티자는 스마트 그리드의 텔레메트리에서 이상을 검출하기 위해 애널리틱스를 도입하고 있습니다. 이 지역에서 성공적인 공급업체는 데이터 주권 관리, 세분화된 사용자 액세스 정책 및 자동화된 규정 준수 보고서를 강조합니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

목차

제1장 서론

- 조사 전제조건과 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 인사이트

- 시장 개요

- 시장 성장 촉진요인

- 자율적이고 자기 관리적인 네트워크의 필요성

- 사물인터넷(IoT)과 머신간 통신의 대두

- 지수 함수적인 데이터 트래픽과 5G 전개의 압력

- 폐루프 인공지능(AI) 디지털 트윈 최적화

- API 기반 네트워크 애즈 코드 수익화에는 실시간 분석이 필요

- 시장 성장 억제요인

- 초기 비용이 높고 투자 수익률(RoI)이 불확실

- 데이터 프라이버시와 규제상의 제약

- 네트워크 데이터 파이프라인의 AI/ML Ops 스킬 갭

- 독자적인 텔레메트리 프로토콜에 의한 벤더 락인

- 가치/공급망 분석

- 규제 상황

- 기술 전망

- Porter's Five Forces 분석

- 공급기업의 협상력

- 구매자의 협상력/소비자

- 신규 참가업체의 위협

- 대체품의 위협

- 경쟁 기업 간 경쟁 관계

제5장 시장 세분화

- 배포 모델별

- On-Premise

- 클라우드

- 하이브리드

- 구성 요소별

- 솔루션

- 네트워크 인텔리전스 플랫폼

- 성능 관리

- 보안 분석

- 근본 원인 및 이상 탐지

- 트래픽 최적화

- 서비스

- 전문 서비스

- 매니지드 서비스

- 솔루션

- 용도별

- 성능 관리

- 장애 관리

- 고객 경험 관리

- 보안 및 이상 탐지

- 스마트 라우팅 및 트래픽 최적화

- 최종 사용자별

- 통신 서비스 제공업체

- 통신사

- 인터넷 서비스 제공업체

- 위성 통신 제공업체

- 케이블 네트워크 제공업체

- 클라우드 서비스 제공업체

- 기업

- 은행, 금융서비스 및 보험(BFSI)

- 헬스케어

- 소매 및 전자상거래

- 제조

- 정부 및 공공 부문

- 통신 서비스 제공업체

- 지역별

- 북미

- 미국

- 캐나다

- 남미

- 브라질

- 기타 남미

- 유럽

- 영국

- 독일

- 프랑스

- 이탈리아

- 스페인

- 러시아

- 기타 유럽

- 아시아태평양

- 중국

- 일본

- 인도

- 한국

- 호주 및 뉴질랜드

- 기타 아시아태평양

- 중동 및 아프리카

- 중동

- 사우디아라비아

- 아랍에미리트(UAE)

- 튀르키예

- 기타 중동

- 아프리카

- 남아프리카

- 기타 아프리카

- 북미

제6장 경쟁 구도

- 시장 집중도

- 전략적 동향

- 시장 점유율 분석

- 기업 프로파일

- Accenture PLC

- Cisco Systems Inc.

- Hewlett Packard Enterprise Co.

- IBM Corporation

- Juniper Networks Inc.

- SAS Institute Inc.

- Sandvine Corporation

- Alcatel-Lucent Enterprise SA

- TIBCO Software Inc.

- Broadcom Inc.(incl. VMware)

- Nokia Corporation

- Ericsson Inc.

- Huawei Technologies Co. Ltd.

- Dell Technologies Inc.

- Oracle Corporation

- NetScout Systems Inc.

- Allot Ltd.

- NEC Corporation

- ZTE Corporation

- Amdocs Ltd.

- F5 Networks Inc.

- Splunk Inc.

- Keysight Technologies Inc.

제7장 시장 기회와 미래 동향

- 화이트 스페이스와 미충족 요구의 평가

The network analytics market holds a present value of USD 4.10 billion in 2025 and is forecast to reach USD 11.09 billion by 2030, advancing at a 21.9% CAGR.

Rapid data-traffic growth, 5G roll-outs, and the surge in connected devices have pushed network analytics from simple monitoring to a core element of digital infrastructure strategy. Enterprises view analytics as essential for predictive maintenance, capacity planning, and security, while service providers use it to monetize programmable networks. Artificial intelligence now underpins most leading platforms, with 60% of technology executives planning AI-enabled automation to streamline operations. Consolidation among vendors, illustrated by IBM's USD 6.4 billion acquisition of HashiCorp, signals demand for end-to-end stacks that blend analytics with broader IT management. Although high initial costs and specialized skill shortages still hinder adoption, cloud delivery models and managed services are easing entry barriers.

Global Network Analytics Market Trends and Insights

Need for Autonomous and Self-Managing Networks

Escalating network complexity and the cost of downtime-USD 9,000 per minute for cloud-centric firms-have intensified demand for self-healing infrastructure. AI-infused analytics platforms now predict and remediate faults, enabling a shift from reactive troubleshooting to proactive optimisation. Industries running mission-critical workloads increasingly depend on AIOps, with 72% of IT leaders planning platform-based architectures that merge analytics, automation, and observability. As a result, vendors are embedding real-time anomaly detection and policy-driven orchestration to cut mean-time-to-repair and protect service-level objectives.

Rise of IoT and Machine-to-Machine Communications

Network analytics platforms have added device-level visibility, protocol decoding, and behavioural baselining to manage heterogeneous traffic. In manufacturing, utilities, and smart-city roll-outs, real-time analytics supports predictive maintenance and energy optimisation, unlocking measurable cost savings and uptime improvements.

High Initial Costs and Uncertain Return on Investment

Comprehensive deployments require software licences, telemetry-ready hardware, systems integration, and staff training. Quantifying financial returns linked to reduced outages or improved customer experience remains challenging, particularly for small and mid-sized organisations. Subscription-based cloud delivery eases capital burdens, yet budget pressures in emerging economies still slow adoption.

Other drivers and restraints analyzed in the detailed report include:

- Exponential Data Traffic and 5G Roll-Out Pressure

- Closed-Loop AI Digital-Twin Optimisation

- API-Based Network-as-Code Monetisation Needs Real-Time Analytics

- Data-Privacy and Regulatory Constraints

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Cloud deployments are set to expand at a 24% CAGR, outpacing the overall network analytics market. The move is driven by elastic scalability, pay-as-you-go economics, and easier access for distributed teams. Despite that momentum, on-premise installations retained 56% revenue in 2024 due to heightened security and sovereignty needs. Hybrid architectures have gained favour as organisations bridge legacy investments with future agility, a trend reinforced by financial institutions, where 91% have already begun their cloud modernisation journeys.

Hybrid operating patterns illustrate a pragmatic view: workloads with stringent data-control requirements remain on-premise, while bursty analytic tasks shift to public clouds. This duality supports cost optimisation without sacrificing governance. Analysts note that 30% of enterprise workloads now sit in public clouds, with analytics and DevOps leading migrations. Vendors have responded by delivering containerised collectors, SaaS dashboards, and unified policy engines that span private and public domains. Continuous integration pipelines further embed analytics into daily operations, compressing development cycles.

Solutions dominated 2024 revenue with 63%, yet services are forecast to grow 23.1% annually as organisations seek specialised expertise. Consulting and integration engagements align analytics architectures with business objectives, while managed services offload daily tuning and rule-maintenance. The services wave mirrors broader IT outsourcing patterns; the managed service provider segment is projected to reach USD 350 billion in 2024 and top USD 1 trillion by 2033.

Service partners increasingly deliver AI-driven advisory offerings that contextualise performance insights into business outcomes. Enterprises adopting such models have reported 20-30% cost savings and up to 25% productivity gains. To meet demand, vendors package runbooks, pre-trained models, and remote SOC capabilities, shortening time to value and mitigating the AI skills gap. This evolution cements services as a cornerstone of the network analytics market, unlocking recurring revenue and deeper client relationships.

Network Analytics Market Report is Segmented by Deployment Model (On-Premise, Cloud, and Hybrid), Component (Solutions and Services), Application (Performance Management, Fault Management, and More), End-User (Communication Service Providers, Cloud Service Providers, and More), and Geography (North America, Europe, Asia-Pacific, and More). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America retained 38% revenue share in 2024, supported by early adoption, sizeable IT budgets, and an advanced supplier ecosystem. United States financial-services and healthcare organisations deploy AI-infused analytics to satisfy stringent uptime and privacy mandates. Canadian carriers use analytics to optimise nationwide 5G roll-outs and manage rural-coverage obligations. Regulatory clarity and abundant talent expedite experimentation with predictive automation, keeping the region at the forefront of innovation.

Asia-Pacific is the fastest-growing region with a 23.3% CAGR to 2030. China and India fund large-scale 5G, smart-city, and industrial-IoT projects that demand granular visibility into multi-vendor environments. Japan and South Korea integrate AI with network monitoring to support autonomous-vehicle trials and factory automation, while Australia leverages analytics to protect critical infrastructure from cyber threats.

Europe advances amid stringent regulations and heightened security awareness. United Kingdom and Germany lead adoption in financial services and manufacturing, seeking GDPR-compliant insights across hybrid architectures. France and Italy augment telecom deployments to maintain customer satisfaction in competitive mobile markets. Energy and utilities operators in Northern and Eastern Europe deploy analytics to detect anomalies in smart-grid telemetry. Vendors thriving in the region emphasise data-sovereignty controls, granular user-access policies, and automated compliance reporting.

- Accenture PLC

- Cisco Systems Inc.

- Hewlett Packard Enterprise Co.

- IBM Corporation

- Juniper Networks Inc.

- SAS Institute Inc.

- Sandvine Corporation

- Alcatel-Lucent Enterprise SA

- TIBCO Software Inc.

- Broadcom Inc. (incl. VMware)

- Nokia Corporation

- Ericsson Inc.

- Huawei Technologies Co. Ltd.

- Dell Technologies Inc.

- Oracle Corporation

- NetScout Systems Inc.

- Allot Ltd.

- NEC Corporation

- ZTE Corporation

- Amdocs Ltd.

- F5 Networks Inc.

- Splunk Inc.

- Keysight Technologies Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Need for autonomous and self-managing networks

- 4.2.2 Rise of Internet of Things (IoT) and machine-to-machine communications

- 4.2.3 Exponential data traffic and 5G roll-out pressure

- 4.2.4 Closed-loop Artificial Intelligence (AI) digital-twin optimisation

- 4.2.5 API-based network-as-code monetisation needs real-time analytics

- 4.3 Market Restraints

- 4.3.1 High initial costs and uncertain Return on Investment (RoI)

- 4.3.2 Data-privacy and regulatory constraints

- 4.3.3 AI/ML Ops skills gap for network data pipelines

- 4.3.4 Vendor lock-in via proprietary telemetry protocols

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers/Consumers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitute Products

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 By Deployment Model

- 5.1.1 On-premise

- 5.1.2 Cloud

- 5.1.3 Hybrid

- 5.2 By Component

- 5.2.1 Solutions

- 5.2.1.1 Network intelligence platforms

- 5.2.1.2 Performance management

- 5.2.1.3 Security analytics

- 5.2.1.4 Root-cause and anomaly detection

- 5.2.1.5 Traffic optimisation

- 5.2.2 Services

- 5.2.2.1 Professional services

- 5.2.2.2 Managed services

- 5.2.1 Solutions

- 5.3 By Application

- 5.3.1 Performance management

- 5.3.2 Fault management

- 5.3.3 Customer experience management

- 5.3.4 Security and anomaly detection

- 5.3.5 Smart routing and traffic optimisation

- 5.4 By End User

- 5.4.1 Communication service providers

- 5.4.1.1 Telecom providers

- 5.4.1.2 Internet service providers

- 5.4.1.3 Satellite communication providers

- 5.4.1.4 Cable network providers

- 5.4.2 Cloud service providers

- 5.4.3 Enterprises

- 5.4.3.1 Banking, Financial Services, and Insurance (BFSI)

- 5.4.3.2 Healthcare

- 5.4.3.3 Retail and e-commerce

- 5.4.3.4 Manufacturing

- 5.4.3.5 Government and public sector

- 5.4.1 Communication service providers

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 United Kingdom

- 5.5.3.2 Germany

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Russia

- 5.5.3.7 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 India

- 5.5.4.4 South Korea

- 5.5.4.5 Australia and New Zealand

- 5.5.4.6 Rest of Asia-Pacific

- 5.5.5 Middle East and Africa

- 5.5.5.1 Middle East

- 5.5.5.1.1 Saudi Arabia

- 5.5.5.1.2 United Arab Emirates

- 5.5.5.1.3 Turkey

- 5.5.5.1.4 Rest of Middle East

- 5.5.5.2 Africa

- 5.5.5.2.1 South Africa

- 5.5.5.2.2 Rest of Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)}

- 6.4.1 Accenture PLC

- 6.4.2 Cisco Systems Inc.

- 6.4.3 Hewlett Packard Enterprise Co.

- 6.4.4 IBM Corporation

- 6.4.5 Juniper Networks Inc.

- 6.4.6 SAS Institute Inc.

- 6.4.7 Sandvine Corporation

- 6.4.8 Alcatel-Lucent Enterprise SA

- 6.4.9 TIBCO Software Inc.

- 6.4.10 Broadcom Inc. (incl. VMware)

- 6.4.11 Nokia Corporation

- 6.4.12 Ericsson Inc.

- 6.4.13 Huawei Technologies Co. Ltd.

- 6.4.14 Dell Technologies Inc.

- 6.4.15 Oracle Corporation

- 6.4.16 NetScout Systems Inc.

- 6.4.17 Allot Ltd.

- 6.4.18 NEC Corporation

- 6.4.19 ZTE Corporation

- 6.4.20 Amdocs Ltd.

- 6.4.21 F5 Networks Inc.

- 6.4.22 Splunk Inc.

- 6.4.23 Keysight Technologies Inc.

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 White-space and Unmet-need Assessment