|

시장보고서

상품코드

1849824

자동차 마이크로모터 : 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Automotive Micro Motor - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

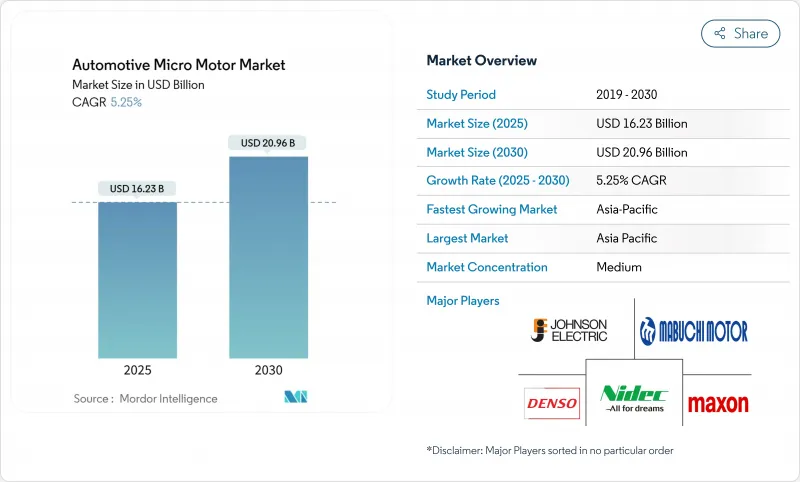

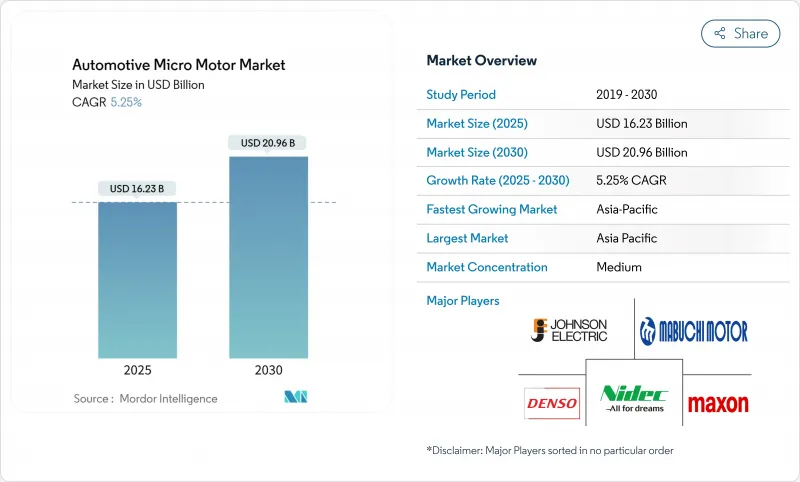

자동차 마이크로모터 시장 규모는 2025년에 162억 3,000만 달러, 2030년에는 약 209억 6,000만 달러에 이르고, CAGR 5.25%를 나타낼 것으로 예측됩니다.

이는 전기자동차(EV)의 대수가 급증하고 있으며, 48V 마일드 하이브리드 아키텍처로의 전환, 파워트레인, 안전성, 쾌적성의 각 모듈에서 1대당 컨텐츠가 증가하고 있기 때문입니다. 일본전산은 자동차 마이크로모터 시장의 추가 점유율을 획득하기 위해 E 액슬의 생산 능력 증강에 70억 달러 이상의 예산을 계상했습니다. 아시아태평양은 중국의 수출 리더십에 힘입어 여전히 수요의 중심지이며, 북미와 유럽에서는 고전압 플랫폼이 브러시리스 모터 기술의 가장 빠른 채용에 박차를 가하고 있습니다.

세계의 자동차 마이크로모터 시장 동향과 인사이트

EV 생산 대수 급증

EV의 세계 출하량은 경차 전체의 성장을 뛰어넘고 있으며, 순수한 배터리 모델은 각각 열 관리, 공기 역학, 스티어링, 브레이크 및 배터리 팩 냉각을 위해 수십 개의 보조 마이크로모터에 의존합니다. Assembly Magazine 잡지는 2034년까지 트랙션 모터의 생산 대수가 4배인 1억 2,000만대 이상으로 급증할 것으로 예측하고 있으며, 이 동향은 서브 시스템 전체의 소형 모터 수요에도 파급됩니다. 중국의 2023년 자동차 수출 대수는 491만대가 되어 일본을 상회했지만, 이것은 이 변화를 반영했으며, 자동차 마이크로모터 시장의 대부분이 이 지역에 집중했습니다. 프리미엄 EV에 탑재된 800V의 고전압 아키텍처는 실리콘 카바이드 디바이스를 중심으로 구축되는 마이크로모터 제어 일렉트로닉스의 성능 수준을 더욱 끌어올려 공급자는 견고한 고주파 드라이버 모듈로 향합니다.

48V 마일드 하이브리드 아키텍처의 상승

기존 12V 전기에서 48V 보드로 전환함으로써 자동차 제조업체는 연료 사용량을 최대 15%까지 줄일 수 있지만, 액티브 서스펜션, 스타트 스톱, 전기 슈퍼 충전기와 같은 새로운 마이크로모터 용도를 개발할 수 있습니다. CLEPA는 2025년까지 신차 10대에 1대가 48V 시스템이 될 것으로 예측했습니다. 이에 따라 48V 배터리 분야도 상승할 것으로 예상되며 자동차 마이크로모터 시장에 큰 디자인인 기회를 줍니다. 테슬라가 사이버 트럭에 48V 배선을 채용함으로써 업계의 전환이 가속되고 있지만, 기존의 제조업체는 고전압에 대응하기 위해 하네스, 커넥터, 검증 툴을 오버홀해야 합니다.

희토류 자석 가격 동향

영구 자석의 가격 변동은 자동차 마이크로모터 공급업체에게 가장 심각한 비용 문제입니다. 네오디뮴의 스팟 가격은 지난 1년간 42% 하락했지만 중국이 수출 규제를 강화함에 따라 장기적인 공급 위험이 다가오고 있습니다. 일본의 스즈키의 스위프트 라인과 같이 자석의 출하가 멈추고 생산이 일시 정지한 차량 프로그램도 이미 보고되었습니다. 업계 각사는 조달처를 다양화하고 있다 : 일본전산은 미국에서 생산되는 Noveon Ecoflux 자석을 채용하는 2025년 계약을 체결하여 통화와 지정학적 충격을 완화하고 있습니다.

부문 분석

12-24V 클래스가 2024년 자동차 마이크로모터 시장 점유율의 42.44%를 차지했습니다. 그러나 고전압(48V 이상) 부문은 OEM이 효율 향상을 위해 마일드 하이브리드 및 800V EV 드라이브 트레인을 채택하기 때문에 CAGR로 가장 빠른 5.78%를 나타낼 전망입니다. 이 변화는 높은 토크 브러시리스 유닛과 낮은 게이지 와이어 하네스를 결합한 자동차 마이크로모터 시장 규모를 확대하고 저항 손실을 줄이고 열 부하를 완화합니다. 테슬라의 48V 하네스 전개는 다음 전기 표준에 대한 업계의 광범위한 협력을 강조합니다.

CLEPA는 48V 기술이 연료 사용량을 최대 15% 절감할 수 있음을 확인하고 있으며, 유럽의 CO2 컴플라이언스 전략 채택을 가속화하고 있습니다. 이를 통해 공급업체는 24V 블로어 모터에서 400V 트랙션 보조 장비까지 커버하는 모듈형 고정자 제품군의 규모를 확대하여 플랫폼 재사용을 극대화하고 있습니다. 신흥 저전력(11V 미만) 틈새는 센서 노드와 관련이 있지만 수익에 차지하는 비율은 제한적입니다.

DC 모터는 윈도우 리프트, 시트 조정기 및 HVAC 플랩을 위한 비용 효율적인 설계로 2024년 매출의 59.65%를 차지했습니다. 하지만 AC 모터는 CAGR 6.5%로 성장을 지속하고, 있습니다. 이는 가변 속도 운전이 스티어링, 브레이크 및 냉각수 펌프의 에너지 소비를 줄이기 때문입니다. 따라서 자동차 마이크로모터 시장은 인버터 구동 AC 옵션이 전동 파워 스티어링의 효율 목표를 충족하는 균형 잡힌 포트폴리오로 DC 플랫폼이 온/오프 작동에 계속 유효합니다.

일본 전산의 SynRA 제품 라인은 희토류 자석을 제거하고 공급 회복력을 높이는 동기 릴랙턴스 아키텍처의 추진을 보여줍니다. 존슨 일렉트릭의 FY23/24 매출은 두 모터 유형 모두에서 OEM의 지속적인 캡처를 보여주고 멀티 기술 로드맵을 검증합니다.

지역 분석

아시아태평양은 2024년 세계 매출의 48.48%를 차지했고, 2030년까지의 CAGR은 6.20%를 나타낼 전망이며, 이 지역은 자동차 마이크로모터 시장의 최전선에 위치하고 있습니다. 중국의 수출업체는 2023년 491만대의 자동차를 출하해 일본을 뽑아 마이크로모터, 반도체, 자석의 광범위한 공급 기반을 굳혔습니다. 일본 전산은 대련 공장의 인원을 최대 50% 증원하여 연간 100만대 생산 가능한 세계 최대의 EV 모터 거점으로 할 계획입니다. 태국과 인도네시아는 통합 EV 공급망을 구축하기 위해 새로운 투자를 실시하고 지역 조달 옵션을 확장합니다.

유럽에서는 엄격한 배기가스 규제가 48V 도입에 박차를 가하고 프리미엄 OEM이 액티브 에어로다이나믹스를 채용하는 가운데 꾸준한 진보를 이루고 있습니다. CLEPA가 마일드 하이브리드 파워트레인을 추진하고, 셰플러가 2024년에 Vitesco와 합병함으로써 현지 모터의 전문성이 강화되었습니다. 독일의 신흥기업 딥드라이브는 50% 적은 자석을 사용한 듀얼 로터 설계를 상업화하기 위해 3,350만 달러를 획득하고 소재가 가벼운 혁신을 추진하는 유럽의 자세를 부각하고 있습니다.

북미는 리쇼어링 정책과 테슬라 주도의 전압 표준화가 원동력이 되고 있습니다. KPS Capital Partners가 지멘스의 이노모틱스 부문에서 35억 유로를 인수하는 것은 사모 펀드가 고가치 모터 브랜드에 대한 의지를 보여줍니다. 남미는 브라질과 아르헨티나 생산에서 전자 비율을 높이는 데 도움이되어 소규모 기지에서 높은 성장을 보입니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월의 애널리스트 지원

목차

제1장 서론

- 조사 전제조건과 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- EV 생산량의 급증

- 고급 인테리어와 프리미엄 인테리어 수요 증가

- 차량의 경량화와 부품의 소형화의 추진

- 48V 마일드 하이브리드 아키텍처의 상승

- 액티브 에어로 다이내믹스 시스템에 통합

- 객실내의 건강 유지 기능(이온 발생기, 방향제)의 보급

- 시장 성장 억제요인

- 희토류 자석 가격 상승 추세

- 지속적인 기술 업그레이드로 유닛 비용 상승

- 엄격한 공차 사양으로 인정 비용 상승

- 피에조 액추에이터의 대체품의 출현

- 밸류체인/공급망 분석

- 규제 상황

- 기술 전망

- Porter's Five Forces

- 공급기업의 협상력

- 구매자의 협상력

- 신규 참가업체의 위협

- 대체품의 위협

- 경쟁 기업 간 경쟁 관계

제5장 시장 규모와 성장 예측(금액(달러)과 수량(단위))

- 소비 전력별

- 11V 이하

- 12-24V

- 25-48V

- 48V 이상

- 모터유형별

- DC 모터

- AC 모터

- 기술별

- 브러시 마이크로모터

- 브러시리스 마이크로모터

- 용도별

- 차체 전자장치(윈도우, 시트, 미러)

- 파워트레인 및 구동계 시스템

- 섀시 및 스티어링

- 안전 및 ADAS 모듈

- 인포테인먼트 및 커넥티비티

- 차량 유형별

- 승용차

- 상용차

- 판매 채널별

- OEM

- 애프터마켓

- 지역별

- 북미

- 미국

- 캐나다

- 기타 북미

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 러시아

- 기타 유럽

- 아시아태평양

- 중국

- 일본

- 인도

- 한국

- 호주 & 뉴질랜드

- 기타 아시아태평양

- 중동 및 아프리카

- 사우디아라비아

- 아랍에미리트(UAE)

- 튀르키예

- 남아프리카

- 기타 중동 및 아프리카

- 북미

제6장 경쟁 구도

- 시장 집중도

- 전략적 동향

- 시장 점유율 분석

- 기업 프로파일

- Nidec Corporation

- Johnson Electric Holdings Ltd.

- Mabuchi Motor Co., Ltd.

- Maxon Motor AG

- Mitsuba Corporation

- Buhler Motor GmbH

- Denso Corporation

- Robert Bosch GmbH

- Continental AG

- Valeo SA

- Brose Fahrzeugteile SE

- Ametek Inc.

- MinebeaMitsumi Inc.

- Mitsumi Electric Co., Ltd.

- Shenzhen Kinmore Motor Co.

- Constar MicroMotor

- Wellings Holdings Ltd.

제7장 시장 기회와 향후 전망

KTH 25.11.03The automotive micromotor market size stood at USD 16.23 billion in 2025 and is forecast to reach about USD 20.96 billion by 2030, advancing at a 5.25% CAGR.

Gains stem from fast-rising electric-vehicle (EV) volumes, the migration to 48 V mild-hybrid architectures and growing content per vehicle across powertrain, safety and comfort modules. Manufacturers are scaling regional production hubs to meet local sourcing rules; Nidec alone earmarked more than USD 7 billion for expanded E-Axle capacity to capture additional automotive micromotor market share. Asia-Pacific remains the demand epicentre, helped by China's export leadership, while higher-voltage platforms spur the fastest adoption of brushless motor technologies in North America and Europe.

Global Automotive Micro Motor Market Trends and Insights

Surge in EV Production Volumes

Global EV shipments continue to outpace overall light-vehicle growth, and each pure battery model relies on dozens of auxiliary micromotors for thermal management, aerodynamics, steering, braking and battery-pack cooling. Assembly Magazine forecasts a fourfold jump in traction-motor output to more than 120 million units by 2034, a trend that cascades into parallel demand for smaller motors across sub-systems. China's rise to 4.91 million vehicle exports in 2023, surpassing Japan, reflects this shift and concentrates much of the automotive micromotor market in the region. Higher 800 V architectures in premium EVs further raise the performance bar for micromotor control electronics built around silicon-carbide devices, pushing suppliers toward robust, high-frequency driver modules.

Rise in 48V Mild-Hybrid Architectures

Moving from traditional 12 V electrics to 48 V boards allows automakers to cut fuel use by up to 15% while unlocking new micromotor applications in active suspension, start-stop and electric superchargers. CLEPA projects 48 V systems in one out of every ten new cars by 2025. The accompanying 48 V battery segment is anticipated to climb, giving the automotive micromotor market a sizeable design-in opportunity. Tesla's adoption of 48 V wiring in the Cybertruck accelerates industry conversion, although legacy manufacturers must overhaul harnesses, connectors and validation tools to cope with higher voltages.

Up-trend in Rare-Earth Magnet Prices

Permanent-magnet pricing volatility is the most acute cost challenge for automotive micromotor suppliers. Neodymium spot values slid 42% over the past year, yet long-term supply risk looms as China tightens export controls. Vehicle programmes already report production pauses, such as Suzuki's Swift line in Japan, when magnet shipments stalled. Industry players are diversifying sourcing: Nidec signed a 2025 deal to adopt Noveon Ecoflux magnets produced in the United States, buffering currency and geopolitical shocks.

Other drivers and restraints analyzed in the detailed report include:

- Growing Demand for Luxury & Premium Interiors

- Vehicle Lightweighting & Component Miniaturisation Push

- Constant Tech Upgrades Inflating Unit Costs

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

The 12 to 24 V class held 42.44% of the 2024 automotive micromotor market share, reflecting legacy electrical architectures across the light-vehicle parc. Higher-voltage (More than 48 V) segments, however, register the fastest 5.78% CAGR as OEMs adopt mild-hybrid and 800 V EV drivetrains for efficiency gains. This shift enlarges the automotive micromotor market size for high-torque brushless units paired with low-gauge wiring harnesses, cutting resistive losses and easing thermal loads. Tesla's 48 V harness rollout underscores broad industry alignment on the next electrical standard.

CLEPA confirms that 48 V technology can trim fuel use by up to 15%, accelerating its inclusion in European CO2-compliance strategies. Suppliers therefore scale modular stator families that cover 24 V blower motors through 400 V traction auxiliaries, maximising platform reuse. Emerging low-power (Less than 11 V) niches remain relevant for sensor nodes yet represent a limited portion of revenue.

DC motors commanded 59.65% of 2024 revenue thanks to cost-effective designs for window lifts, seat adjusters and HVAC flaps. Nevertheless, AC machines record a robust 6.5% CAGR because variable-speed operation reduces energy draw in steering, braking and coolant pumps. The automotive micromotor market therefore witnesses a balanced portfolio where DC platforms remain viable for on-off actuation, while inverter-driven AC options satisfy efficiency targets in electric power steering.

Nidec's SynRA line illustrates the push toward synchronous-reluctance architectures that remove rare-earth magnets, boosting supply resilience. Johnson Electric's FY23/24 sales indicate sustained OEM uptake across both motor types, validating a multi-technology roadmap.

The Automotive Micro Motors Market Report is Segmented by Power Consumption (Below 11V, 12 To 24V, and More), Motor Type (DC Motor and AC Motor), Technology (Brushed Micromotor and Brushless Micromotor), Application (Body Electronics and More), Vehicle Type (Passenger Cars and Commercial Vehicles), Sales Channel (OEM and Aftermarket), and Geography. The Market Forecasts are Provided in Terms of Value (USD) and Volume (Units).

Geography Analysis

Asia-Pacific generated 48.48% of global revenue in 2024, and its 6.20% CAGR to 2030 keeps the region at the forefront of the automotive micromotor market. Chinese exporters shipped 4.91 million vehicles in 2023, surpassing Japan and consolidating a broad supply base for micromotors, semiconductors and magnets. Nidec plans to raise headcount at its Dalian complex by up to 50%, turning it into the world's largest EV-motor site capable of one-million-unit output a year. Thailand and Indonesia court fresh investment to create integrated EV supply chains, broadening regional sourcing options.

Europe advances at a steady rate as strict emissions targets spur 48 V roll-outs and premium OEMs adopt active aerodynamics. CLEPA's promotion of mild-hybrid powertrains and Schaeffler's 2024 merger with Vitesco bolster local motor expertise. German start-up DeepDrive secured USD 33.5 million to commercialise dual-rotor designs using 50% fewer magnets, highlighting Europe's push for material-light innovations.

North America is powered by reshoring policies and Tesla-led voltage standardisation. KPS Capital Partners' EUR 3.5 billion takeover of Siemens' Innomotics division signals private equity appetite for high-value motor brands. South America exhibits the highr growth off a smaller base, aided by rising electronics content in Brazilian and Argentine production.

- Nidec Corporation

- Johnson Electric Holdings Ltd.

- Mabuchi Motor Co., Ltd.

- Maxon Motor AG

- Mitsuba Corporation

- Buhler Motor GmbH

- Denso Corporation

- Robert Bosch GmbH

- Continental AG

- Valeo SA

- Brose Fahrzeugteile SE

- Ametek Inc.

- MinebeaMitsumi Inc.

- Mitsumi Electric Co., Ltd.

- Shenzhen Kinmore Motor Co.

- Constar MicroMotor

- Wellings Holdings Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surge in EV production volumes

- 4.2.2 Growing demand for luxury & premium interiors

- 4.2.3 Vehicle lightweighting & component miniaturisation push

- 4.2.4 Rise in 48 V mild-hybrid architectures

- 4.2.5 Integration in active aerodynamics systems

- 4.2.6 Proliferation of cabin wellness features (ionizers, scent dispensers)

- 4.3 Market Restraints

- 4.3.1 Up-trend in rare-earth magnet prices

- 4.3.2 Constant tech upgrades inflating unit costs

- 4.3.3 Tight tolerance specs raising qualification costs

- 4.3.4 Emerging piezo-actuator substitutes

- 4.4 Value/Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value (USD) and Volume (Units))

- 5.1 By Power Consumption

- 5.1.1 Below 11 V

- 5.1.2 12 to 24 V

- 5.1.3 25 to 48 V

- 5.1.4 Above 48 V

- 5.2 By Motor Type

- 5.2.1 DC Motor

- 5.2.2 AC Motor

- 5.3 By Technology

- 5.3.1 Brushed Micromotor

- 5.3.2 Brushless Micromotor

- 5.4 By Application

- 5.4.1 Body Electronics (window, seat, mirror)

- 5.4.2 Powertrain & Drivetrain Systems

- 5.4.3 Chassis & Steering

- 5.4.4 Safety & ADAS Modules

- 5.4.5 Infotainment & Connectivity

- 5.5 By Vehicle Type

- 5.5.1 Passenger Cars

- 5.5.2 Commercial Vehicles

- 5.6 By Sales Channel

- 5.6.1 OEM

- 5.6.2 Aftermarket

- 5.7 By Geography

- 5.7.1 North America

- 5.7.1.1 United States

- 5.7.1.2 Canada

- 5.7.1.3 Rest of North America

- 5.7.2 South America

- 5.7.2.1 Brazil

- 5.7.2.2 Argentina

- 5.7.2.3 Rest of South America

- 5.7.3 Europe

- 5.7.3.1 Germany

- 5.7.3.2 United Kingdom

- 5.7.3.3 France

- 5.7.3.4 Italy

- 5.7.3.5 Spain

- 5.7.3.6 Russia

- 5.7.3.7 Rest of Europe

- 5.7.4 Asia-Pacific

- 5.7.4.1 China

- 5.7.4.2 Japan

- 5.7.4.3 India

- 5.7.4.4 South Korea

- 5.7.4.5 Australia & New Zealand

- 5.7.4.6 Rest of Asia-Pacific

- 5.7.5 Middle East and Africa

- 5.7.5.1 Saudi Arabia

- 5.7.5.2 United Arab Emirates

- 5.7.5.3 Turkey

- 5.7.5.4 South Africa

- 5.7.5.5 Rest of Middle East and Africa

- 5.7.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products and Services, and Recent Developments)

- 6.4.1 Nidec Corporation

- 6.4.2 Johnson Electric Holdings Ltd.

- 6.4.3 Mabuchi Motor Co., Ltd.

- 6.4.4 Maxon Motor AG

- 6.4.5 Mitsuba Corporation

- 6.4.6 Buhler Motor GmbH

- 6.4.7 Denso Corporation

- 6.4.8 Robert Bosch GmbH

- 6.4.9 Continental AG

- 6.4.10 Valeo SA

- 6.4.11 Brose Fahrzeugteile SE

- 6.4.12 Ametek Inc.

- 6.4.13 MinebeaMitsumi Inc.

- 6.4.14 Mitsumi Electric Co., Ltd.

- 6.4.15 Shenzhen Kinmore Motor Co.

- 6.4.16 Constar MicroMotor

- 6.4.17 Wellings Holdings Ltd.