|

시장보고서

상품코드

1849829

수경 재배 : 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Hydroponics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

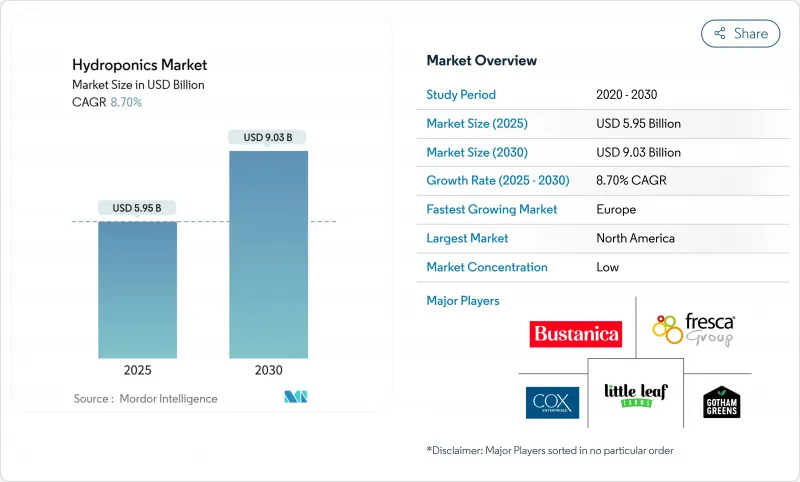

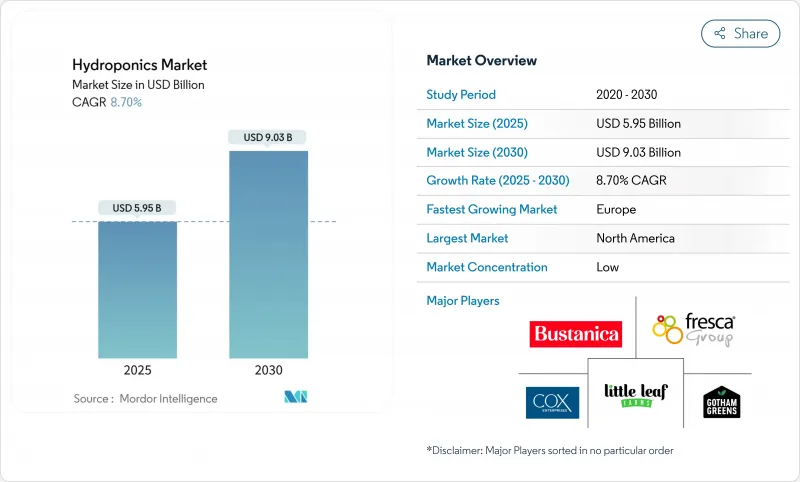

수경 재배 시장 규모는 2025년에 59억 5,000만 달러로 평가되었고, 예측 기간(2025-2030년)의 CAGR은 8.7%를 나타낼 것으로 예측되며, 2030년에 90억 3,000만 달러에 달할 전망입니다.

이러한 상승세는 도시 인구 증가, 기업의 지속가능성 요구, 그리고 급속히 발전하는 제어 환경 기술의 융합에 힘입어 추진되고 있습니다. 현재는 운영이 간편한 집적형 재배 시스템이 주류를 이루고 있으나, 운영자들이 자원 효율성 향상을 추구함에 따라 액체 시스템이 더 빠르게 확대되고 있습니다. 기업들은 수확량 증대와 운영 비용 절감을 위해 인공지능 기반 영양 공급 루틴을 통합하고 있으며, LED 가격 하락으로 연중 생산이 경제적으로 가능해지고 있습니다. 에너지 사용량 증가는 여전히 우려사항이지만, 조명 효율 개선과 현장 재생에너지 접근성 확대로 변동성 높은 전력 가격에 대한 노출은 줄어들고 있습니다.

세계의 수경 재배 시장 동향 및 인사이트

평방미터당 수율이 높고 낮은 물 사용량

수경 재배 시설은 평방미터당 최대 11배 높은 생산량을 제공하면서 물 소비량을 80-90% 절감해 건조하거나 고밀도 건축 환경에 매력적입니다. 스카이스크래퍼 팜(Skyscraper Farm)과 같은 수직 농장은 관개용수를 거의 모두 재활용하여 일반 농경지 대비 95-99%의 절감 효과를 보여줍니다. 에덴 그린 테크놀로지(Eden Green Technology)의 텍사스 시설은 단 62,000평방피트(약 5,750㎡) 면적에서 연간 340,000그루의 식물을 생산하며, 제어 환경 농업이 어떻게 한계 토지를 안정적인 식량 공급원으로 전환하는지 입증합니다. 상승하는 지방자치단체의 수도 요금은 절감된 물 1리터당 운영 비용이 직접 감소로 연결됨에 따라 수경 재배 시장의 가치 제안을 강화합니다. 도시 계획가들은 도심 내 신규 농장 승인 시 물 효율성을 강조하며, 토지 제약이 있는 대도시 지역에서 허가 절차와 시설 구축을 가속화하고 있습니다. 이 추세는 지하수 고갈과 수입 의존도가 폐쇄형 농업에 대한 정책적 지원을 촉진하는 중동 및 아시아의 메가시티에서 특히 두드러집니다.

도시 인구의 변화와 현지 식품에 대한 수요

전 세계 인구의 56% 이상이 도시에 거주하며, 주민들은 신선도와 추적성을 보장하기 위해 가까운 지역에서 재배된 농산물을 점점 더 요구하고 있습니다. 코로나19 기간 동안 공급망 충격은 월마트와 같은 소매업체들이 지역 수직 농장 공급업체에 공동 투자하여 진열대 연속성을 보호하도록 했습니다. 캘거리와 휴스턴에서 볼 수 있듯이, 지방자치단체 프로그램은 활용도가 낮은 도심 사무실을 연중 재배 허브로 전환하여 상업용 공실 공간이 어떻게 식품 공장으로 변모할 수 있는지 보여줍니다. 젊은 소비자들은 무농약 지역 채소에 15-20%의 프리미엄을 기꺼이 지불하며, 이는 구독형 박스 서비스를 제공하는 도시 농장에 예측 가능한 현금 흐름을 창출합니다. 공공-민간 보조금이 창업 비용을 상쇄하여 소규모 운영자들이 과거 소매점이나 공유 오피스 사업에 한정되었던 주요 입지에 임대 계약을 체결할 수 있게 합니다. 이러한 요소들이 결합되어 안정적인 도시 고객 기반을 형성하며, 이는 평균 판매 가격 상승을 지원하고 유통 과정의 탄소 배출을 감소시킵니다.

초기 자본 지출과 긴 회수 기간

높은 초기 비용과 긴 회수 기간은 상업용 수경 재배 도입을 저해합니다. 일반적인 500제곱미터 규모의 초보 농장에는 15,000-40,000달러가 필요하며, 월간 에너지 및 영양분 비용은 1,300달러에 달할 수 있어 자금 제약이 있는 기업가들을 주저하게 만듭니다. 운영 비용의 최대 50%를 차지하는 에너지 비용은 자유화된 전력 시장의 현물 가격 급등에 마진을 노출시킵니다. 2023년 미국 수직 농장 다수를 파산으로 몰아넣은 시장 정리는 공격적인 확장이 현금 흐름을 앞질렀음을 드러냈습니다. 2023년 초 실내 농업에 대한 벤처 자금 조달은 91% 감소하여 기업들이 성장보다 수익성을 우선시하도록 강요했습니다. 많은 개발도상국에서는 두 자릿수 금리가 상환 기간을 연장시켜 잠재적 수요에도 불구하고 수경 재배 시장 침투를 저해합니다. 국부펀드가 식량 안보 인프라를 지원할 경우 대규모 상업 프로젝트가 추진되지만, 소규모 재배자들은 저렴한 턴키 키트가 등장할 때까지 투자를 미루는 경우가 많습니다.

부문 분석

2024년에도 집적 배지(Aggregate substrates)가 매출의 79.6%를 차지하며, 토양 재배에서 무토양 재배로 전환하는 재배자들에게 익숙함이 주는 안정감을 보여줍니다. 낮은 자본 요구량과 단순한 작동 방식이 지속적인 우위를 뒷받침합니다. 그러나 액체 시스템은 운영자들이 산소 공급과 영양분 주입을 정밀하게 제어하려는 노력으로 2030년까지 연평균 12.6%의 성장률을 보일 전망입니다. 심해양식법(DWC) 및 영양막 기술(NFT) 설비는 덩어리 기질 대비 잎채소 수확량을 30-50% 증가시킵니다. 폐쇄형 설계는 또한 거의 모든 용액 유출물을 재활용하여 물 요금이 상승하는 환경에서 중요한 차별화 요소로 작용합니다.

하이브리드 방식이 등장하고 있습니다. 불활성 기질에 내장된 센서가 자동으로 액체 영양분 공급을 촉발하여, 골재의 뿌리 안정성과 액체의 정밀성을 결합합니다. 이러한 적응성은 기업의 ESG 목표와 부합하며 투자 자본 수익률을 높입니다. 따라서 수경 재배 시장이 성숙해짐에 따라 더 많은 생산자들이 정적 기질에서 센서 기반 영양분 필름 라인으로 업그레이드할 것으로 예상됩니다.

지역 분석

북미는 성숙한 인프라, 적극적인 미국 농무부(USDA) 보조금, 풍부한 벤처 자금 조달을 바탕으로 2024년 글로벌 매출의 35.8%를 차지했습니다. 병원, 학교, 기업 캠퍼스가 식품 마일 배출량을 줄이기 위해 현장 농장을 구축함에 따라 미국 상업용 수경 재배 시장 규모는 계속해서 확대되고 있습니다. 캐나다는 대마초 합법화 과정에서 다져진 통제 환경 기술 전문성을 채소 생산으로 확장하며 기술적 깊이를 더하고 있습니다.

유럽은 2030년까지 연평균 13.2% 성장률로 가장 빠른 상승세를 보일 전망입니다. EU의 ‘농장에서 식탁까지(Farm-to-Fork)’ 이니셔티브가 명확한 정책적 뒷받침을 제공하는 가운데, 네덜란드 등 국가들은 화학 투입량을 줄이고 수확량을 높이는 AI 기반 센서 네트워크를 도입 중입니다. 독일의 온실 클러스터와 재생에너지 자산의 공동 배치 추진은 운영 비용을 절감하고 장기 자금 조달 접근성을 확대하고 있습니다. 스페인의 수경 재배 상추 주류화 현상은 소비자의 높은 수용도를 보여주며, 이는 슈퍼마켓 제휴를 가속화하는 요인입니다.

아시아태평양 지역은 아직 개척되지 않은 거대한 성장 잠재력을 지닌다. 중국에는 60개 이상의 전문 장비 제조업체가 있으며, 지방 정부의 인센티브로 대도시에서 수직 농장이 활성화되고 있습니다. 인도의 스타트업들은 토양 재배 대비 40배의 수확량 증가를 입증하며 추가 벤처 캐피털을 유치하고 있습니다. 동남아시아 국가들의 식량 안보 우려는 신규 프로젝트에 대한 입법적 지지를 이끌어내고 있으나, 불안정한 전력 공급은 여전히 규모 확대를 복잡하게 합니다. 해당 지역의 중산층 증가와 도시화 확대는 기술 비용이 하락함에 따라 수경 재배 시장이 동쪽으로 전환될 것임을 시사합니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

목차

제1장 서론

- 조사의 전제조건과 시장의 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 평방미터당 높은 수확량 및 낮은 물 사용량

- 도시 인구 이동 및 지역 식품 수요 증가

- LED 기술의 설비 투자 삭감

- 기업 현장에서 ESG 농업의 의무화

- AI에 의한 영양 믹스 최적화로 ROI를 향상

- 통제 환경 농업(CEA) 농장의 탄소 크레딧 현금화

- 시장 성장 억제요인

- 초기 자본 지출 및 긴 투자 회수 기간

- 통제 환경 농업 분야의 기술 격차

- 인(P) 기반 영양소 폐기물 규제 강화

- 전력 공급 중단 위험 및 에너지 가격 변동성

- 규제 상황

- 기술의 전망

- Five Forces 분석

- 공급기업의 협상력

- 구매자의 협상력

- 신규 참가업체의 위협

- 대체품으로부터의 위협

- 경쟁 기업간 경쟁 관계

제5장 시장 규모와 성장 예측

- 유형별

- 집적형 시스템

- 폐쇄형 시스템

- 개방형 시스템

- 액체 시스템

- 집적형 시스템

- 작물 유형별

- 토마토

- 상추와 잎 야채

- 페퍼

- 오이

- 마이크로 그린

- 기타 작물(딸기, 바질 등)

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 기타 북미

- 유럽

- 독일

- 영국

- 프랑스

- 스페인

- 이탈리아

- 네덜란드

- 기타 유럽

- 아시아태평양

- 중국

- 일본

- 인도

- 호주

- 기타 아시아태평양

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 중동

- 사우디아라비아

- 아랍에미리트(UAE)

- 기타 중동

- 아프리카

- 남아프리카

- 기타 아프리카

- 북미

제6장 경쟁 구도

- 시장 집중도

- 전략적 동향

- 시장 점유율 분석

- 기업 프로파일

- GrowUp Farms

- BrightFarms(COX Enterprises, Inc)

- Pure Harvest Smart Farms

- Little Leaf Farms

- Thanet Earth(Fresca Group)

- Hydro Produce

- Emirates Hydroponics Farms

- Revol Greens

- Gotham Greens

- Nutrifresh India

- Badia Farms

- Sundrop Farms(Centuria Capital)

- Emirates Bustanica

- Sky Greens

제7장 시장 기회와 장래의 전망

HBR 25.11.12The Hydroponics Market size is estimated at USD 5.95 billion in 2025 and is projected to reach USD 9.03 billion by 2030, at a CAGR of 8.7% during the forecast period (2025-2030).

This upward trajectory is propelled by the convergence of urban population growth, corporate sustainability mandates, and rapidly improving controlled-environment technologies. Aggregate growing systems currently dominate because they are simple to operate, but liquid systems are expanding more quickly as operators seek higher resource efficiency. Companies are integrating AI-driven nutrient routines to boost yields and cut operating costs, while falling LED prices are making year-round production economical. Rising energy use remains a concern; however, improvements in lighting efficiency and access to onsite renewables are lowering exposure to volatile power prices.

Global Hydroponics Market Trends and Insights

High-yield per square meter and lower water use

Hydroponic installations deliver up to 11-fold higher output per square meter while cutting water consumption by 80-90%, making them compelling for arid or densely built environments. Vertical farms such as Skyscraper Farm recycle nearly all irrigation water, demonstrating 95-99% savings compared with field agriculture. Eden Green Technology's Texas facility produces 340,000 plants annually on just 62,000 square feet, validating how controlled-environment agriculture turns marginal real estate into reliable food sources. Rising municipal water tariffs strengthen the hydroponics market value proposition as each liter of savings converts directly into lower operating costs. Urban planners highlight water efficiency when approving new inner-city farms, accelerating permit cycles, and build-outs in land-constrained metro areas. The trend is particularly acute in Middle Eastern and Asian megacities, where groundwater depletion and import dependency drive policy support for closed-loop farming.

Urban population shift and demand for local food

Cities account for over 56% of the world's population, and residents increasingly demand produce grown within a short radius to guarantee freshness and traceability. During the COVID-19 period, supply chain shocks pushed retailers such as Walmart to co-invest in regional vertical-farm suppliers to safeguard shelf continuity. Municipal programs convert under-utilized downtown offices into year-round grow hubs, as seen in Calgary and Houston, demonstrating how commercial vacancies can become food factories. Younger consumers willingly pay a 15-20% premium for pesticide-free local greens, creating predictable cash flow for urban farms serving subscription boxes. Public-private grants offset start-up costs, allowing small operators to secure leases in prime locations once reserved for retail or coworking ventures. Together, these factors underpin a steady urban customer base that supports higher average selling prices and reduces distribution emissions.

Up-front capex and long pay-back periods

High upfront costs and long payback periods hinder commercial hydroponics adoption. Typical 500 square meter starter farms require USD 15,000-40,000, while monthly energy and nutrient bills can reach USD 1,300, deterring cash-constrained entrepreneurs. Energy accounts for up to 50% of operating costs, exposing margins to spot-price spikes in liberalized power markets. The 2023 shakeout that pushed several U.S. vertical farms into bankruptcy highlighted how aggressive expansion outpaced cash flow. Venture funding for indoor agriculture slipped 91% during early 2023, forcing firms to prioritize profitability over growth. In many developing countries, double-digit interest rates exacerbate pay-back horizons, slowing hydroponics market penetration despite latent demand. Where sovereign wealth funds subsidize food security infrastructure, larger commercial projects move forward, and smaller growers often delay investments until cheaper turnkey kits emerge.

Other drivers and restraints analyzed in the detailed report include:

- Reduced capital expenditure for LED technology

- Corporate on-site ESG farming mandates

- Skills gap in controlled-environment agronomy

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Aggregate substrates continued to command 79.6% of revenue in 2024, illustrating how familiarity reassures growers shifting from soil to soilless cultivation. Their lower capital needs and simple mechanics underpin persistent dominance. Liquid systems, however, are accelerating at a 12.6% CAGR through 2030 as operators pursue finer control of oxygenation and nutrient dosing. Deep-water culture and nutrient film technique installations boost leafy-green yields by 30-50% compared with aggregate counterparts. Closed-loop designs also recycle nearly all solution runoff, an important differentiator where water tariffs are rising.

Hybrid approaches are emerging: sensors embedded in inert substrates automatically trigger liquid nutrient pulses, merging the root stability of aggregates with the precision of liquids. Such adaptability aligns with corporate ESG targets and elevates return on invested capital. Hence, more producers are expected to upgrade from static substrates to sensor-guided nutrient film lines as the hydroponics market matures.

The Hydroponics Market Report is Segmented by Type (Aggregate System and Liquid System), by Crop Type (Tomato, Lettuce and Leafy Greens, Pepper, Cucumber, and More), and by Geography (North America, Europe, Asia-Pacific, South America, Middle East, and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America secured 35.8% of global revenue in 2024 on the back of mature infrastructure, proactive USDA grants, and abundant venture financing. The hydroponics market size for U.S. commercial operations continues to swell as hospitals, schools, and corporate campuses build onsite farms to trim food-mile emissions. Canada's controlled-environment expertise, honed during cannabis legalization, is migrating into vegetable production and adding technical depth.

Europe promises the fastest climb with a 13.2% CAGR through 2030. The EU's Farm-to-Fork initiative supplies clear policy backing, while countries such as the Netherlands deploy AI-fueled sensor networks that cut chemical inputs and lift yields. Germany's push to co-locate greenhouse clusters with renewable power assets is lowering operating expenses and broadening access to long-term financing. Spain's mainstream acceptance of hydroponic lettuce highlights strong consumer readiness, a factor that accelerates supermarket partnerships.

Asia-Pacific presents a large untapped upside. China has more than 60 specialized equipment manufacturers, and provincial incentives encourage vertical farming in megacities. India's start-ups demonstrate 40-fold yield gains over soil plots, enticing additional venture capital. Food-security concerns in Southeast Asian nations are winning legislative support for new projects, although inconsistent power supply still complicates scaling. The region's rising middle class and urban footprint suggest the hydroponics market will pivot eastward as technological costs fall.

- GrowUp Farms

- BrightFarms (COX Enterprises, Inc)

- Pure Harvest Smart Farms

- Little Leaf Farms

- Thanet Earth (Fresca Group)

- Hydro Produce

- Emirates Hydroponics Farms

- Revol Greens

- Gotham Greens

- Nutrifresh India

- Badia Farms

- Sundrop Farms (Centuria Capital)

- Emirates Bustanica

- Sky Greens

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 High-yield per square meter and lower water use

- 4.2.2 Urban population shift and demand for local food

- 4.2.3 Reduced capital expenditure for LED technology

- 4.2.4 Corporate on-site ESG farming mandates

- 4.2.5 AI nutrient-mix optimization boosting ROI

- 4.2.6 Carbon-credit monetization of CEA farms

- 4.3 Market Restraints

- 4.3.1 Up-front capex and long pay-back periods

- 4.3.2 Skills gap in controlled-environment agronomy

- 4.3.3 Rising P-based nutrient-waste regulations

- 4.3.4 Grid-outage risk and energy-price volatility

- 4.4 Regulatory Landscape

- 4.5 Technological Outlook

- 4.6 Porters Five Forces

- 4.6.1 Bargaining Power of Suppliers

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Threat of New Entrants

- 4.6.4 Threat from Substitutes

- 4.6.5 Intensity of Competitive Rivalry

5 Market Size and Growth Forecasts (Value, USD)

- 5.1 By Type

- 5.1.1 Aggregate System

- 5.1.1.1 Closed System

- 5.1.1.2 Open System

- 5.1.2 Liquid System

- 5.1.1 Aggregate System

- 5.2 By Crop Type

- 5.2.1 Tomato

- 5.2.2 Lettuce and Leafy Greens

- 5.2.3 Pepper

- 5.2.4 Cucumber

- 5.2.5 Micro-greens

- 5.2.6 Other Crops (Strawberry, Basil, etc.)

- 5.3 By Geography

- 5.3.1 North America

- 5.3.1.1 United States

- 5.3.1.2 Canada

- 5.3.1.3 Mexico

- 5.3.1.4 Rest of North America

- 5.3.2 Europe

- 5.3.2.1 Germany

- 5.3.2.2 United Kingdom

- 5.3.2.3 France

- 5.3.2.4 Spain

- 5.3.2.5 Italy

- 5.3.2.6 Netherlands

- 5.3.2.7 Rest of Europe

- 5.3.3 Asia-Pacific

- 5.3.3.1 China

- 5.3.3.2 Japan

- 5.3.3.3 India

- 5.3.3.4 Australia

- 5.3.3.5 Rest of Asia-Pacific

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle East

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 United Arab Emirates

- 5.3.5.3 Rest of Middle East

- 5.3.6 Africa

- 5.3.6.1 South Africa

- 5.3.6.2 Rest of Africa

- 5.3.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 GrowUp Farms

- 6.4.2 BrightFarms (COX Enterprises, Inc)

- 6.4.3 Pure Harvest Smart Farms

- 6.4.4 Little Leaf Farms

- 6.4.5 Thanet Earth (Fresca Group)

- 6.4.6 Hydro Produce

- 6.4.7 Emirates Hydroponics Farms

- 6.4.8 Revol Greens

- 6.4.9 Gotham Greens

- 6.4.10 Nutrifresh India

- 6.4.11 Badia Farms

- 6.4.12 Sundrop Farms (Centuria Capital)

- 6.4.13 Emirates Bustanica

- 6.4.14 Sky Greens