|

시장보고서

상품코드

1849850

줄기세포 : 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Stem Cell - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

줄기세포 시장은 2025년에 171억 3,000만 달러로 평가되었고, 2030년에 298억 8,000만 달러에 이를 것으로 예측되며, CAGR은 11.77%를 나타낼 전망입니다.

성장은 여러 전선에서 전개되고 있습니다. 새로 승인된 중간엽 줄기세포 치료제는 상업화 리드 타임을 단축시켰고, 유도만능줄기세포(iPSC) 플랫폼에 투자가 쏟아지고 있으며, 전문 CDMO(위탁개발생산) 기업들은 생산 역량을 확대 중입니다. 특히 미국과 일본에서 가속화된 규제 경로는 치료제를 환자에게 더 빨리 제공하고 있으며, CRISPR 기반 편집 기술과 AI 기반 생산 워크플로는 제품 품질을 높이고 치료 범위를 넓히고 있습니다. 지역적 동력은 아시아태평양으로 이동 중이며, 해당 지역 국가 정책은 줄기세포를 전략적 기술로 포지셔닝하고 있습니다. 대형 바이오파마 기업들이 체내 투여를 용이하게 하는 전달 도구를 확보하기 위해 혁신 기업들을 인수함에 따라 경쟁 강도가 높아지고 있습니다.

세계의 줄기세포 시장 동향 및 인사이트

만성 질환과 퇴행성 질환의 높은 부담

고령화 인구 구조가 재생 치료 옵션에 대한 수요를 증폭시키고 있습니다. 파킨슨병은 2050년까지 2,520만 명에게 영향을 미칠 것으로 예상되며, 인구 고령화가 증가분의 89%를 주도할 전망입니다. 중간엽 줄기세포(MSCs)는 염증을 감소시키고 조직 분해를 억제하며 회복을 촉진하여 만성 질환 관리에 비용 효율적인 도구로 자리매김하고 있습니다. 의료 시스템은 고비용 장기 요양을 지연시킬 수 있는 치료법으로 예산을 재편성하며, MSC 기반 제품 조달을 강화하고 줄기세포 시장을 공고히 하고 있습니다.

빠르게 확대되는 재생의학 파이프라인

4,000개 이상의 유전자, 세포 및 RNA 치료제가 개발 중이며, 2024년 초 1상 프로그램은 11% 증가했습니다. CRISPR 편집 기술은 CAR-T 성능을 향상시키고 자가면역 질환 적응증을 개척하고 있습니다. AI 기반 분석은 세포 표현형 분석을 자동화하여 출시 전 테스트 기간을 며칠에서 몇 시간으로 단축합니다. 임상 증거는 확대되고 있습니다. 망막 세포 이식은 의미 있는 시력을 회복시켰으며, iPSC 유래 구조체는 제1형 당뇨병에서 유망한 혈당 조절 효과를 보여주었습니다. 이러한 진전은 대상 환자군을 확대하여 줄기세포 시장 전망을 밝게 합니다.

안전성과 유효성의 불확실성

다능성 세포 유형의 종양 유발성과 면역원성은 여전히 핵심 우려 사항입니다. 배치 간 변동성은 효능 분석을 복잡하게 하여 규제 기관의 감독 강화로 이어지고 있습니다. 연구 그룹들은 NK 세포 탐지를 회피하면서 숙주 조직에 통합되는 면역 은폐 이식편을 개발했습니다. 세포 치료제에 대한 FDA 권한을 확정한 제9순회법원 판결은 준수 의무를 명확히 하지만 승인 기간을 연장할 수 있습니다.

부문 분석

성체 줄기세포는 입증된 안전성과 광범위한 치료 적용성으로 2024년 줄기세포 시장 점유율 55.0%를 차지했습니다. MSC 전용 품질 관리 지침이 효능 분석을 표준화하여 임상적 활용을 확대하고 있습니다. 정형외과, 심장, 면역학 프로그램이 성숙함에 따라 성체 줄기세포 제품 시장 규모는 꾸준히 성장할 전망입니다. 반면, iPSC는 재프로그래밍 효율 개선과 GMP 생산 능력 확대로 10.43%의 연평균 복합 성장률(CAGR)을 기록하며 발전하고 있습니다. 아스펜 뉴로사이언스는 2025년 1월 파킨슨병 치료제 ANPD001의 자동화 생산을 성공시켜 폐쇄형 시스템 워크플로우가 자가 세포 치료제의 리드 타임을 단축할 수 있음을 입증했습니다. VSEL은 기형종 위험 없이 다계통 분화 가능성을 지닌 세포로 주목받고 있습니다(frontiersin.org). 투자자 관심은 면역 회피를 위해 설계된 즉시 사용 가능한 iPSC 계통으로 이동 중이며, 이는 2030년까지 지속적 자본 유입을 시사합니다.

동결보호제 칵테일의 발전으로 해동 후 세포 사멸이 감소하여 성체 및 iPSC 유래 세포 모두에서 생존율이 향상되고 있습니다. 규제 기관은 통합된 출시 규격을 장려하여 두 제품군의 비용 격차를 점진적으로 좁힐 것입니다. 이러한 혁신이 일상적 진료에 통합됨에 따라, 특히 맞춤형 치료의 신속한 확장이 필요한 분야에서 줄기세포 시장의 활용 사례가 수렴될 전망입니다.

2024년 줄기세포 시장 규모에서 정형외과 적응증은 23.0%를 차지했으며, 이는 골관절염 통증 점수 개선 및 척추 유합 촉진 효과가 입증된 중간엽줄기세포(MSC) 주사 치료에 기인합니다. MSC 치료는 재생 정형외과 옵션 중 가장 높은 통증 감소 계수를 기록했습니다. 고령화 인구가 관절 복구 수요를 주도함에 따라 해당 부문은 여전히 탄력성을 유지하고 있습니다. 그러나 신경계 질환은 11.23%의 연평균 성장률(CAGR)로 성장할 전망입니다. 도파민성 신경세포 대체 기술의 진전은 파킨슨병 환자 집단에서 측정 가능한 운동 기능 개선을 가져왔다. 혈뇌장벽 통과 기술의 향상과 면역 회피 세포주 개발은 알츠하이머병 및 뇌졸중 치료를 위한 임상 파이프라인을 확대하고 있습니다. 심혈관 프로그램 역시 확대되고 있습니다. 셀리폰트(Cellipont)의 cGMP 파트너십은 심장 전구세포 공급을 목표로 합니다.

임상 시험의 다양성이 증가하고 있습니다. 혈액암은 이식 건수를 계속 주도하는 반면, 당뇨병을 위한 베타세포 대체 치료는 2상 평가 단계에 진입했습니다. 이러한 추세들은 균형 잡힌 적용 분야 조합을 강화하여 줄기세포 시장 전반에 걸친 지속적인 수익 성장을 뒷받침합니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

목차

제1장 서론

- 조사의 전제조건과 시장의 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 만성 및 퇴행성 질환의 높은 부담

- 급속히 확장되는 재생의학 파이프라인

- 바람직한 규제 촉진 경로

- 공공 및 민간 제대혈/조직 은행 및 맞춤형 의학 프로그램의 확산 증가

- 즉시 사용 가능한 치료법 구현을 가능케 하는 기술적 돌파구

- 해당 분야 혁신 및 발전을 위한 시장 참여자 간 협력 강화

- 시장 성장 억제요인

- 치료법과 관련된 안전성과 효능 불확실성

- 제한적인 보험급여 정책

- 제조 규모의 과제와 제품 및 절차의 고비용

- 뿌리 깊은 도덕적 우려로 인한 윤리와 정책의 차이

- 가치/공급망 분석

- 규제 전망

- 기술의 전망

- Porter's Five Forces 분석

- 신규 참가업체의 위협

- 구매자의 협상력

- 공급기업의 협상력

- 대체품의 위협

- 경쟁 기업간 경쟁 관계

제5장 시장 규모와 성장 예측

- 제품 유형별

- 성체 줄기세포

- 중간엽 줄기세포

- 조혈 줄기세포

- 신경 줄기세포

- 인간 배아 줄기세포

- 유도 만능 줄기세포(iPSCs)

- 초소형 배아 유사 줄기세포

- 기타 제품 유형(암 줄기세포 등)

- 성체 줄기세포

- 용도별

- 신경질환

- 정형외과 치료

- 종양 질환

- 심혈관질환 및 심근경색

- 당뇨병과 대사질환

- 상처 및 화상

- 기타 용도

- 치료 유형별

- 동종이계 줄기세포요법

- 자가이식요법

- 동계 줄기세포요법

- 최종 사용자별

- 학술연구기관

- 병원과 외과 센터

- 제약 및 생명 공학 기업

- 줄기세포은행과 동결보존시설

- 계약 개발 제조 조직(CDMO)

- 지역

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 기타 유럽

- 아시아태평양

- 중국

- 일본

- 인도

- 한국

- 호주

- 기타 아시아태평양

- 중동 및 아프리카

- GCC

- 남아프리카

- 기타 중동 및 아프리카

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 북미

제6장 경쟁 구도

- 시장 집중도

- 전략적 동향

- 시장 점유율 분석

- 기업 프로파일

- ATCC

- Thermo Fisher Scientific Inc.

- Merck KGaA

- STEMCELL Technologies

- Takara Bio Inc.

- Miltenyi Biotec

- Pluri Inc.

- AllCells LLC

- International Stem Cell Corp.

- ReNeuron Group plc

- Bio-Techne Corp.

- Gamida Cell Ltd.

- Fate Therapeutics Inc.

- Cynata Therapeutics Ltd

- BioRestorative Therapies Inc.

- BrainStorm Cell Therapeutics

- Lineage Cell Therapeutics

- Regenexx LLC

- Orchard Therapeutics plc

- Mesoblast Ltd

- Athersys Inc.

- Medipost Co. Ltd.

- PromoCell GmbH

제7장 시장 기회와 장래의 전망

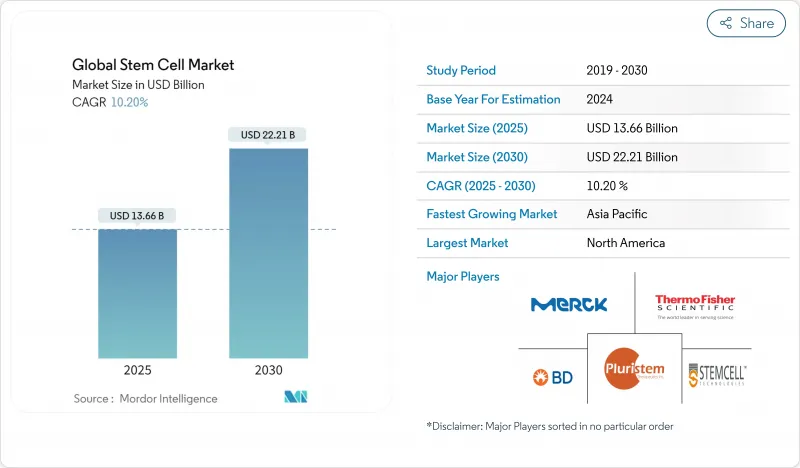

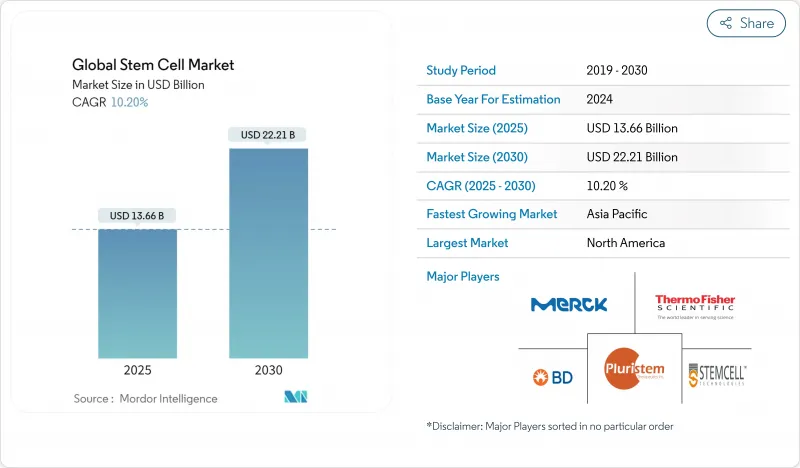

HBR 25.11.12The stem cell market stands at USD 17.13 billion in 2025 and is projected to reach USD 29.88 billion by 2030, advancing at an 11.77% CAGR.

Growth is unfolding on several fronts: newly approved mesenchymal stromal cell therapies have shortened commercial lead times, investment is pouring into induced pluripotent stem cell (iPSC) platforms, and specialized CDMOs are scaling manufacturing capacity. Accelerated regulatory pathways, especially in the United States and Japan, are bringing therapies to patients sooner, while CRISPR-enabled editing and AI-guided production workflows are lifting product quality and broadening therapeutic scope. Regional momentum is shifting toward Asia-Pacific, where national policies are positioning stem cells as strategic technologies. Competitive intensity is increasing as large biopharma acquires innovators to secure delivery tools that ease in-vivo administration.

Global Stem Cell Market Trends and Insights

High Burden of Chronic and Degenerative Diseases

Aging demographics are magnifying demand for regenerative options. Parkinson's disease is forecast to affect 25.2 million people by 2050, with population aging driving 89% of the increase.Mesenchymal stem cells (MSCs) reduce inflammation, inhibit tissue breakdown, and spur repair, positioning them as cost-effective tools for chronic disease management. Health systems are reallocating budgets toward therapies that can defer expensive long-term care, reinforcing procurement of MSC-based products and fortifying the stem cell market.

Rapidly Expanding Regenerative-Medicine Pipeline

More than 4,000 gene, cell, and RNA therapies are in development, and Phase I programs climbed 11% in early 2024. CRISPR editing is boosting CAR-T performance and opening autoimmune indications. AI-enabled analytics now automate cell phenotyping, trimming release testing from days to hours. Clinical evidence is broadening: retinal cell transplants restored meaningful visual acuity, and iPSC-derived constructs demonstrated promising glycemic control in type 1 diabetes. These advances expand addressable populations, lifting the stem cell market outlook.

Safety and Efficacy Uncertainties

Tumorigenicity and immunogenicity remain central concerns for pluripotent cell types. Batch variability complicates potency assays, prompting regulators to reinforce oversight. Research groups have engineered immune-cloaked grafts that evade NK-cell detection while integrating into host tissue. A Ninth Circuit ruling affirming FDA authority over cell therapies clarifies compliance obligations but may lengthen timelines.

Other drivers and restraints analyzed in the detailed report include:

- Favorable Regulatory Acceleration Pathways

- Rising Penetration of Cord-Blood/Tissue Banking

- Restrictive Reimbursement Policies

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Adult stem cells held 55.0% of stem cell market share in 2024 owing to a well-documented safety record and broad therapeutic latitude. MSC-specific quality control guidelines now standardize potency assays, supporting widespread clinical use. The stem cell market size for adult stem-cell products is projected to grow steadily as orthopedic, cardiac, and immunological programs mature. Conversely, iPSCs are advancing at a 10.43% CAGR, propelled by improved reprogramming efficiency and expanding GMP capacity. Aspen Neuroscience automated production of ANPD001 for Parkinson's disease in January 2025, demonstrating how closed-system workflows can compress autologous lead times. VSELs are gaining attention for multi-lineage potential without teratoma risk frontiersin.org. Investor focus is shifting toward off-the-shelf iPSC lines engineered for immune evasion, indicating sustained capital inflows through 2030.

Advances in cryoprotectant cocktails are reducing post-thaw apoptosis, enhancing viability across both adult and iPSC derivatives. Regulatory bodies encourage harmonized release specifications, which will gradually narrow the cost gap between the two product classes. As these innovations integrate into routine practice, the stem cell market will likely see convergence in use cases, particularly where personalized therapies must scale quickly.

Orthopedic indications represented 23.0% of the stem cell market size in 2024, anchored by evidence that MSC injections improve pain scores in osteoarthritis and promote spinal fusion. MSC therapy recorded the highest pain-reduction coefficient among regenerative orthopedic options.The segment remains resilient as an aging population drives demand for joint repair. Neurological disorders, however, are on track to grow at an 11.23% CAGR. Progress in dopaminergic neuron replacement has yielded measurable motor gains in Parkinson's cohorts. Enhanced blood-brain barrier crossing techniques and immune-cloaked cell lines are widening the clinical pipeline for Alzheimer's disease and stroke. Cardiovascular programs are similarly expanding; Cellipont's cGMP partnership targets cardiac progenitor cell supply.

Clinical trial diversity is rising. Hematologic cancers continue to anchor transplant volumes, while beta-cell replacement for diabetes is entering Phase II evaluation. Together, these trends reinforce a balanced application mix, supporting continuous revenue growth across the stem cell market.

The Stem Cells Market is Segmented by Product Type (Adult Stem Cell, Human Embryonic Cell, Induced Pluripotent Stem Cell, and More), Application (Neurological Disorders, Orthopedic Treatments, and More), Treatment Type (Allogeneic Stem Cell Therapy and More), End User (Academic and Research Institutes, Hospitals and Surgical Centers and More) and Geography. The Market and Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- ATCC

- Thermo Fisher Scientific

- Merck

- Stem Cell Technologies

- Takara Bio

- Miltenyi Biotec

- Pluri Inc.

- AllCells

- International Plastics

- ReNeuron Group

- Bio-Techne Corp.

- Gamida Cell Ltd.

- Fate Therapeutics Inc.

- Cynata Therapeutics

- BioRestorative Therapies Inc.

- BrainStorm Cell

- Lineage Cell Therapeutics

- Regenexx LLC

- Orchard Therapeutics plc

- Mesoblast

- Athersys

- Medipost Co. Ltd.

- PromoCell

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 High Burden of Chronic and Degenerative Diseases

- 4.2.2 Rapidly Expanding Regenerative-Medicine Pipeline

- 4.2.3 Favorable Regulatory Acceleration Pathways

- 4.2.4 Rising Penetration of Public and Private Cord-blood/Tissue Banking and Personalized-Medicine Programs

- 4.2.5 Technology Breakthroughs Enabling Off-the-Shelf Therapies

- 4.2.6 Intesifying Colloboration Among Market Players for Innovation and Development in The Field

- 4.3 Market Restraints

- 4.3.1 Safety and Efficacy Uncertainties Associated with Therapies

- 4.3.2 Restrictive Reimbursement Policies

- 4.3.3 Manufacturing Scale Challenges and High Cost of Products and Procedures

- 4.3.4 Ethical and Policy Divergence Due to Persistent Moral Concerns

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Outlook

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 Market Size and Growth Forecasts (Value-USD)

- 5.1 By Product Type

- 5.1.1 Adult Stem Cells

- 5.1.1.1 Mesenchymal Stem Cells

- 5.1.1.2 Hematopoietic Stem Cells

- 5.1.1.3 Neural Stem Cells

- 5.1.2 Human Embryonic Stem Cells

- 5.1.3 Induced Pluripotent Stem Cells (iPSCs)

- 5.1.4 Very Small Embryonic-like Stem Cells

- 5.1.5 Other Product Types (e.g., Cancer Stem Cells)

- 5.1.1 Adult Stem Cells

- 5.2 By Application

- 5.2.1 Neurological Disorders

- 5.2.2 Orthopedic Treatments

- 5.2.3 Oncology Disorders

- 5.2.4 Cardiovascular and Myocardial Infarction

- 5.2.5 Diabetes and Metabolic Disorders

- 5.2.6 Wounds and Burns

- 5.2.7 Other Applications

- 5.3 By Treatment Type

- 5.3.1 Allogeneic Stem Cell Therapy

- 5.3.2 Autologous Stem Cell Therapy

- 5.3.3 Syngeneic Stem Cell Therapy

- 5.4 By End User

- 5.4.1 Academic & Research Institutes

- 5.4.2 Hospitals and Surgical Centers

- 5.4.3 Pharmaceutical and Biotechnology Companies

- 5.4.4 Stem Cell Banks and Cryopreservation Facilities

- 5.4.5 Contract Development and Manufacturing Organizations (CDMOs)

- 5.5 Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 South Korea

- 5.5.3.5 Australia

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 Middle East & Africa

- 5.5.4.1 GCC

- 5.5.4.2 South Africa

- 5.5.4.3 Rest of Middle East & Africa

- 5.5.5 South America

- 5.5.5.1 Brazil

- 5.5.5.2 Argentina

- 5.5.5.3 Rest of South America

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 ATCC

- 6.4.2 Thermo Fisher Scientific Inc.

- 6.4.3 Merck KGaA

- 6.4.4 STEMCELL Technologies

- 6.4.5 Takara Bio Inc.

- 6.4.6 Miltenyi Biotec

- 6.4.7 Pluri Inc.

- 6.4.8 AllCells LLC

- 6.4.9 International Stem Cell Corp.

- 6.4.10 ReNeuron Group plc

- 6.4.11 Bio-Techne Corp.

- 6.4.12 Gamida Cell Ltd.

- 6.4.13 Fate Therapeutics Inc.

- 6.4.14 Cynata Therapeutics Ltd

- 6.4.15 BioRestorative Therapies Inc.

- 6.4.16 BrainStorm Cell Therapeutics

- 6.4.17 Lineage Cell Therapeutics

- 6.4.18 Regenexx LLC

- 6.4.19 Orchard Therapeutics plc

- 6.4.20 Mesoblast Ltd

- 6.4.21 Athersys Inc.

- 6.4.22 Medipost Co. Ltd.

- 6.4.23 PromoCell GmbH

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment