|

시장보고서

상품코드

1849854

동물 성장 촉진제 : 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Animal Growth Promoters - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

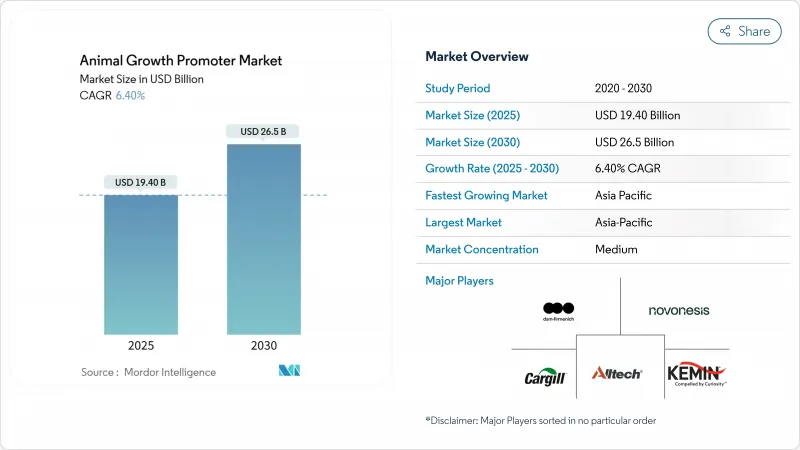

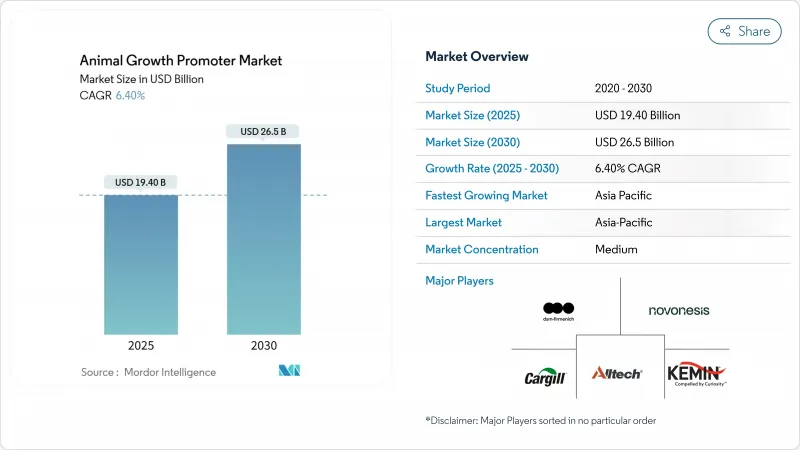

동물 성장 촉진제 시장 규모는 2025년에 194억 달러로 평가되었고, 예측기간 중 CAGR은 6.40%를 나타낼 것으로 예측되며, 2030년에 265억 달러에 이를 전망입니다.

이러한 견고한 성장세는 가축 사육 분야의 전환을 반영하는데, 이는 생산 과정의 환경적 영향을 줄이면서 동물의 건강을 유지하는 기능성 영양으로의 전환입니다. 항생제 무첨가 육류에 대한 소비자의 요구 증가, 주요 수출 거점에서의 규제 강화, 아시아태평양 지역의 지속적인 단백질 수요가 종합적으로 제조업체의 상업적 성장 여력을 확대하고 있습니다. 전통적 단백질 사료에 대한 가격 압박이 심화되면서, 사료 1kg당 더 많은 영양소를 추출하는 효소와 프로바이오틱스에 대한 관심이 높아지고 있습니다. 공장 내 디지털화, 특히 AI 기반 미세 투여 기술은 폐기물을 줄이고 첨가제 투입률을 실시간 동물 요구에 맞춰 조정하여 원자재 비용이 급변할 때도 마진을 유지합니다. 탄소 중립 농업으로의 추세는 성능과 지속가능성 이점을 동시에 제공하는 바실러스 기반 프로바이오틱스와 같은 생물학적 솔루션의 가치를 더욱 높입니다.

세계의 동물 성장 촉진제 시장 동향 및 인사이트

세계의 항생제 무첨가 육류 수요 급증

소매업체와 패스트푸드 레스토랑이 항생제 무첨가 공급망을 요구함에 따라 전 세계 생산자들은 성장 성능을 유지하는 천연 대체재에 투자하고 있습니다. 이 추세는 항생제 무첨가 라벨링이 시장성을 높이는 가금류 및 돼지 부문에서 특히 두드러집니다. EU의 항생제 성장 촉진제 금지 조치는 이미 명확한 모델을 제시했으며, 북미 식료품점들은 인증 제품에 대해 15-25%의 프리미엄을 제공합니다. 따라서 동물 성장 촉진제 시장은 규제와 소비자 지불 의향 모두로부터 꾸준한 수요 기반을 확보하고 있습니다.

대규모 축산과 사료 효율 중시의 생산 강화

아시아태평양 및 남미의 메가 농장들은 변동성 높은 곡물 가격을 상쇄하기 위해 사료 전환율(FCR)을 지속적으로 낮추고 있습니다. 생산자들은 영양소 소화율을 3-5% 향상시키는 효소와 사료 필요량을 2-4% 절감하는 표적 프로바이오틱 균주를 활용해 육계는 2.0 미만, 돼지는 2.5 미만의 FCR을 목표로 삼고 있습니다. 2024년 글로벌 사료 생산량이 0.2% 감소한 12억 9,000만 톤을 기록함에 따라, 생산량 증가가 아닌 효율성 향상이 성장을 주도할 전망입니다. 이러한 필수 요인들은 고급 솔루션에 대한 프리미엄 수요를 강화하고 동물 성장 촉진제 시장의 가치 기준 확장을 이끌고 있습니다.

사료용 유기산의 가격 변동

2024년 포름산 비용은 천연가스 가격 급등과 소수 대형 공장의 계획되지 않은 가동 중단으로 40-60% 급등했습니다. 프로피온산 기준 가격은 다년간 최고치를 기록하며 사료 공장 마진을 잠식했고, 이로 인해 배합량 감축이나 저가 대체재 사용이 촉발되었습니다. 장기 계약이 없는 소규모 사료 공장들은 이러한 불안정성으로 인해 고가 첨가제 도입 의욕이 위축되고, 동물 성장 촉진제 시장 확장이 일시적으로 둔화되었습니다.

부문 분석

프로바이오틱스는 사료 효율성과 장 건강을 지속적으로 향상시키는 바실러스(Bacillus) 및 락토바실러스(Lactobacillus) 균주의 강력한 검증에 힘입어 2024년 글로벌 매출의 34.5%를 차지했습니다. 통합 생산자들이 AGP(동물성장촉진제) 철수를 상쇄하기 위해 모든 사료 단계에 다중 균주 컨소시엄을 점점 더 혼합함에 따라, 이러한 주도적 위상은 전체 동물성장촉진제 시장을 강화합니다. 상당한 설치 기반은 펠릿화 온도를 견딜 수 있는 포자 형성 변종에 대한 연구 개발을 촉진하여 사용 사례를 더욱 확대하고 있습니다. 이미 5억 달러 규모의 카테고리인 식물성 원료 시장은 천연 착색, 항산화 및 항균 효과로 클린 라벨 수요와 부합하여 다른 모든 그룹을 앞지르는 9.4%의 연평균 성장률(CAGR)로 발전하고 있습니다. 효소는 고온 펠릿화 과정을 견디는 내열성 설계로 저급 곡물의 손실 영양소를 활용할 수 있어 지속적인 투자를 유치하고 있습니다. 한편 산성화제는 사료 부패 위험이 높은 열대 기후 지역에서 특히 안정적인 수요를 유지합니다.

식물성 원료의 성장세는 에센셜 오일과 유기산의 시너지 효과를 활용하는 복합 제품으로 확산되며, 각 성분 단독 대비 강력한 병원체 억제 효과를 제공합니다. 질병 압박과 항생제 규제 강화가 맞물린 돼지와 가금류 분야에서 도입이 가장 활발합니다. 프리바이오틱스는 상주 미생물군을 영양 공급하고 프로바이오틱스 정착을 강화하는 동반 성분으로 주목받는다. 항생제와 이오노포어는 후퇴했으나 엄격한 규제가 없는 지역에서는 여전히 사용됩니다. 동물 성장 촉진제 시장은 생물학적 또는 식물 유래 변종으로의 전환을 지속합니다. 데이터가 축적됨에 따라 보수적인 반추동물 사육장조차도 다가올 탄소 감사를 대비해 메탄 저감을 위한 식물성 혼합물을 도입합니다. 상업적 업체들은 환경적 기대를 충족시키면서 일관된 활성 성분 함량을 보장하기 위해 무용제 추출 방법의 규모를 확대하며 대응하고 있습니다.

가금류 부문은 2024년 매출의 37.5%를 차지하며, 이 카테고리의 글로벌 인기와 영양 미세 조정에 대한 민감성을 반영했습니다. 통합업체들은 항생제 제한에도 불구하고 성장을 유지하기 위해 동물 성장 촉진제에 투자하고 있으며, 첨단 제형은 대규모 상업 시설에서 가금류 사망률을 4-6% 낮추는 데 기여한 것으로 평가됩니다. AI 기반 육계 관리 플랫폼이 센서 데이터를 기반으로 첨가제 혼합 비율을 처방함에 따라 사용 강도는 더욱 심화될 전망입니다. 어류 사료 비용 상승과 지속 가능한 수생 사료 수요 증가로 수산업이 8.6%의 연평균 성장률(CAGR)로 가장 빠르게 확장 중입니다. 동남아시아 새우 양식업자들이 프로바이오틱스와 효소 혼합물을 도입하면서 사료 전환율이 6-8% 개선되었다고 보고하여 해당 부문의 상업적 성과를 입증했습니다.

양돈 사육업자들은 산화제(acidifiers)가 이유 후 설사를 억제하고 효소가 고섬유질 사료의 에너지를 해방시키는 단계별 급여 프로그램을 채택하며, 동물 성장 촉진제 시장의 견고한 점유율을 유지하고 있습니다. 반추동물은 2024년 12월 영국에서 사용이 새로 승인된 보베어(Bovaer)와 같은 메탄 감소 화합물에 대한 안정적인 수요를 창출합니다. 특수 부문인 말, 반려동물, 특수 이국적 동물은 소량 소비되지만 소유주들이 기능성 인간용 등급 성분을 추구하기 때문에 프리미엄 마진을 창출합니다. 모든 종에서 통합업체들은 투자 수익률(ROI) 증명을 요구하여, 공급업체들이 첨가제 관리 체계와 성장 및 건강 결과를 연결하는 현장 데이터 대시보드를 제작하도록 촉진하고 있습니다.

지역 분석

아시아태평양 지역은 2024년 글로벌 매출의 41.6%를 차지했으며, 약 8%의 연평균 성장률(CAGR)로 성장할 것으로 예상되어 동물 성장 촉진제 시장의 중심지로서의 역할을 공고히 할 것입니다. 중국의 대형 통합 기업들은 수출 목표에 부합하는 항생제 무첨가 약속을 이행하며 프로바이오틱스와 효소의 급격한 채택을 주도하고 있습니다. 베이징 사이톱 바이오테크(Beijing Scitop Bio-tech)만 해도 2024년 프로바이오틱스 매출이 3억 279만 위안(4,213만 달러)에 달해 국내 생산 역량을 입증했습니다. 인도의 중산층 확대는 닭과 계란 수요를 촉진하는 한편, 정부의 농업 지원 프로그램은 농가에게 항생제 사용을 줄이는 방법을 가르쳐 식물성 및 유기산 카테고리에 자연스러운 성장 동력을 제공하고 있습니다. 동남아시아 양식업은 태국과 베트남이 연못 내 센서를 신속히 설치해 적응형 첨가제 투여를 유도함으로써 어류 생존율을 높이고 글로벌 수산물 공급을 확대하며 새로운 물량을 창출하고 있습니다.

북미는 엄격한 고객 사양이 육류 가치 사슬 전반에 반영되면서 여전히 기술 시험장으로 기능합니다. 미국의 AI 연계 사료공장은 입고되는 옥수수 품질과 육계 증체량 예측에 따라 교대마다 첨가제 처방을 조정합니다. 캐나다의 사료장 운영자들은 더 엄격해질 탄소 규제를 예상하며 메탄 저감 첨가제를 도입해 수출 경쟁력을 유지하고 있습니다. 가축 두수는 느리게 증가하지만, 개체당 첨가제 지출은 증가 추세를 보여 동물 성장 촉진제 시장 내 지역적 가치 성장을 강화하고 있습니다.

성숙했으나 규제가 매우 엄격한 유럽은 항생제 성장 촉진제 사용을 계속 금지하는 한편 천연 솔루션을 장려하고 있습니다. 독일은 사료 전환율 향상을 효소 혼합제와 직접 연계하는 농장 내 센서 활용을 선도하며, 반복 구매를 촉진하는 세분화된 증거를 제공합니다. 프랑스와 스페인은 유기농 사육을 주창하며 화학 용매가 없는 표준화된 식물성 오일 수요를 촉진합니다. 동유럽은 사료 인프라 현대화와 EU 추적성 의무 통합으로 빠르게 따라잡고 있으며, 이는 첨가제 사용을 규정 준수 절차의 일부로 포함시킵니다. 이러한 수렴하는 힘들은 가축 수가 정체된 상황에서도 유럽이 전체 동물 성장 촉진제 시장 확장에 꾸준한 기여자로 남게 합니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월의 애널리스트 지원

목차

제1장 서론

- 조사의 전제조건과 시장의 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 성장 촉진요인

- 항생제 미사용 고기 수요가 세계적으로 급증

- 대규모 축산 생산 확대 및 사료 효율성 강화

- 이오노포어 대비 프로바이오틱스 제조 비용 경쟁력 확보

- 포스트바이오틱스 장내 미생물군집 혁신으로 성장 성능 향상

- 탄소 중립 바이오리액터 기술로 바실러스 비용 대폭 절감

- 사료 공장에서의 AI 기반 정밀 미세 투여

- 시장 성장 억제요인

- 사료용 유기산 가격의 변동

- 급속히 진화하는 세계의 AGP 규제

- 프로바이오틱스 발효용 설탕 공급 병목 현상

- 첨가제 효능을 저하시키는 마이코톡신 상호작용

- 규제 상황

- 기술의 전망

- Five Forces 분석

- 공급기업의 협상력

- 구매자의 협상력

- 신규 참가업체의 위협

- 대체품의 위협

- 경쟁 기업간 경쟁 관계

제5장 시장 규모와 성장 예측

- 유형별

- 프로바이오틱스

- 프리바이오틱스

- 식물 유래 성분

- 산화제

- 효소

- 항생제

- 기타 유형(이오노포어, 호르몬)

- 동물 유형별

- 가금

- 돼지

- 반추동물

- 양식업

- 기타 동물(말, 반려동물)

- 형태별

- 드라이

- 액체

- 원료별

- 세균

- 효모

- 곰팡이

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 기타 북미

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 유럽

- 독일

- 영국

- 프랑스

- 스페인

- 러시아

- 기타 유럽

- 아시아태평양

- 중국

- 일본

- 인도

- 호주

- 기타 아시아태평양

- 중동

- 튀르키예

- 사우디아라비아

- 아랍에미리트(UAE)

- 기타 중동

- 아프리카

- 남아프리카

- 이집트

- 기타 아프리카

- 북미

제6장 경쟁 구도

- 시장 집중도

- 전략적 동향

- 시장 점유율 분석

- 기업 프로파일

- DSM-Firmenich

- Cargill, Inc.

- Vetoquinol

- Alltech

- Kemin Industries

- Huvepharma

- Novonesis

- BASF SE

- ADM

- Evonik Industries

- Adisseo

- Phibro Animal Health

- Virbac

- Nutreco

제7장 시장 기회와 장래의 전망

HBR 25.11.12The Animal Growth Promoter Market size is estimated at USD 19.40 billion in 2025 and is anticipated to reach USD 26.5 billion by 2030, at a CAGR of 6.40% during the forecast period.

This solid trajectory mirrors the livestock sector's transition toward functional nutrition that keeps animals healthy while trimming the environmental impact of production. Rising consumer insistence on antibiotic-free meat, stricter regulations across major export hubs, and sustained protein demand in Asia-Pacific collectively widen commercial headroom for manufacturers. Intensifying price pressure on traditional protein meals amplifies interest in enzymes and probiotics that unlock more nutrients from every kilogram of feed. Digitalization inside mills, especially AI-enabled micro-dosing, reduces waste and aligns additive inclusion rates with real-time animal needs, preserving margins even when raw-material costs swing sharply. Momentum toward carbon-neutral farming further elevates biological solutions such as Bacillus-based probiotics that deliver both performance and sustainability benefits.

Global Animal Growth Promoters Market Trends and Insights

Global Antibiotic-Free Meat Demand Boom

Retailers and quick-service restaurants now stipulate antibiotic-free supply chains, prompting producers worldwide to invest in natural alternatives that preserve growth performance. This trend is especially strong in the poultry and swine sectors, where antibiotic-free labeling boosts marketability. EU prohibitions on antimicrobial growth promoters have already shown a clear template, and North American grocers offer premiums of 15-25% for certified products. The animal growth promoters market, therefore, gains a steady demand floor from both regulation and consumer willingness to pay.

Intensifying Large-Scale Livestock Production and Feed Efficiency Focus

Mega farms in Asia-Pacific and South America aim for ever-lower feed conversion ratios to offset volatile grain prices. Producers now target sub-2.0 FCR in broilers and sub-2.5 in swine by leveraging enzymes that lift nutrient digestibility by 3-5% and targeted probiotic strains that shave 2-4% off feed needs. With global feed output dipping 0.2% to 1.29 billion metric tons in 2024, efficiency gains, not tonnage, will fuel growth. These imperatives reinforce premium demand for advanced solutions and expand the animal growth promoters market in value terms.

Feed-Grade Organic-Acid Price Volatility

Formic-acid costs swung 40-60% in 2024, influenced by natural gas price spikes and unplanned shutdowns at a handful of large plants. Propionic-acid benchmarks climbed to multi-year highs, eroding feed-mill margins and prompting ration cuts or cheaper substitutes. For small mills without long-term contracts, this instability dampens the appetite for premium inclusions and temporarily tempers the animal growth promoters' market expansion.

Other drivers and restraints analyzed in the detailed report include:

- Probiotic Manufacturing Cost-Parity with Ionophores

- Postbiotic Gut-Microbiome Breakthroughs Boosting Growth Performance

- Rapidly Evolving Global AGP Regulatory Restrictions

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Probiotics generated 34.5% of global revenue in 2024, supported by robust validation of Bacillus and Lactobacillus strains that consistently enhance feed efficiency and gut health. This leadership bolsters the overall animal growth promoters market, as integrated producers increasingly blend multi-strain consortia into every diet phase to offset AGP withdrawal. The sizable installed base encourages Research and Development into spore-forming variants that can withstand pelleting temperatures, further widening use cases. The phytogenic niche, already a USD 500 million category, advances at a forecast 9.4% CAGR, outpacing all other groups thanks to natural coloration, antioxidative, and antimicrobial benefits that dovetail with clean-label demands. Enzymes continue to draw investment because thermostable designs survive high-temperature pelleting, unlocking otherwise lost nutrients in lower-grade grains. Meanwhile, acidifiers hold steady, especially in tropical climates where feed spoilage risk is acute.

Momentum in phytogenics spills into combinatory products that tap the synergistic effects of essential oils plus organic acids, delivering stronger pathogen suppression than either class alone. Adoption is strongest in swine and poultry, where disease pressure and antibiotic curbs converge. Prebiotics gain traction as companion ingredients that nourish resident microbiota and reinforce probiotic colonization. Antibiotics and ionophores retreat but remain present in regions lacking strict rules. The animal growth promoters market continues its pivot toward biological or plant-derived variants. As data accumulate, even conservative ruminant operations adopt phytogenic blends seeking methane mitigation to meet upcoming carbon audits. Commercial players respond by scaling solvent-free extraction methods, ensuring consistent active compound loads while meeting environmental expectations.

Poultry captured 37.5% of 2024 revenue, reflecting the category's global popularity and responsiveness to nutritional fine-tuning. Integrators invest in animal growth promoters to maintain growth despite antibiotic limits, and advanced formulations are credited with lowering flock mortality by 4-6% in large commercial setups. Usage intensity is poised to deepen as AI-assisted broiler management platforms prescribe additive inclusion rates based on sensor data. Aquaculture expands fastest at an 8.6% CAGR, driven by escalating fishmeal costs and the push for sustainable aquatic diets. As shrimp farmers in Southeast Asia integrate probiotic and enzyme blends, they report feed conversion improvements of 6-8%, underlining the segment's commercial payoff.

Swine producers adopt phase-feeding programs where acidifiers curb post-weaning diarrhea, and enzymes unlock energy from high-fiber rations, sustaining a solid share of the animal growth promoters market. Ruminants contribute a stable demand for methane-reducing compounds such as Bovaer, newly cleared for UK use in December 2024. Specialty segments, horses, pets, and niche exotics-consume small volumes yet deliver premium margins because owners seek functional, human-grade ingredients. Across species, integrators demand proof of ROI, spurring suppliers to produce field-data dashboards that link additive regimes to growth and health outcomes.

The Animal Growth Promoters Market Report is Segmented by Type (Probiotics, Prebiotics, Phytogenics, Acidifiers, and More), by Animal Type (Poultry, Swine, Ruminants, Aquaculture, and Others), by Form (Dry and Liquid), by Source (Bacterial, Yeast, and Fungal), and by Geography (North America, Europe, Asia-Pacific, South America, Middle East, and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific controlled 41.6% of global revenue in 2024 and is projected to grow near 8% CAGR, securing its role as the epicenter of the animal growth promoters market. China's large integrators commit to antibiotic-free pledges aligned with export ambitions, driving steep adoption of probiotics and enzymes. Beijing Scitop Bio-tech alone posted CNY 302.79 million (USD 42.13 million) in probiotic revenue during 2024, underscoring domestic capacity. India's rising middle class promotes chicken and egg demand, while government extension programs teach farmers to curb antibiotic use, creating natural tailwinds for phytogenic and organic-acid categories. Southeast Asian aquaculture unlocks new volumes, with Thailand and Vietnam rapidly installing in-pond sensors that cue adaptive additive dosing, boosting fish survival rates and shading global seafood supplies.

North America remains a technology testbed as stringent customer specifications filter through the meat value chain. AI-linked mills in the United States adjust additive regimens every shift based on incoming corn quality and broiler weight-gain forecasts. Feedlot operators in Canada adopt methane-reduction additives in anticipation of stricter carbon rules, preserving export competitiveness. Although livestock headcounts grow slowly, per-animal additive spending trends upward, reinforcing regional value growth inside the animal growth promoters market.

Europe, a mature but highly regulated arena, continues to ban antimicrobial growth promoters while incentivizing natural solutions. Germany spearheads on-farm sensor usage that links feed conversion gains directly to enzyme cocktails, providing granular proof that fuels repeat purchases. France and Spain champion organic rearing, pushing demand for standardized phytogenic oils free from chemical solvents. Eastern Europe catches up quickly, modernizing feed infrastructure and integrating EU traceability mandates, which embed additive usage as part of compliance protocols. These converging forces keep Europe a steady contributor to the overall animal growth promoters market expansion despite flat livestock numbers.

- DSM-Firmenich

- Cargill, Inc.

- Vetoquinol

- Alltech

- Kemin Industries

- Huvepharma

- Novonesis

- BASF SE

- ADM

- Evonik Industries

- Adisseo

- Phibro Animal Health

- Virbac

- Nutreco

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Drivers

- 4.1.1 Global antibiotic-free meat demand boom

- 4.1.2 Intensifying large-scale livestock production and feed efficiency focus

- 4.1.3 Probiotic manufacturing cost-parity with ionophores

- 4.1.4 Postbiotic gut-microbiome breakthroughs boosting growth performance

- 4.1.5 Carbon-neutral bioreactor technologies slashing Bacillus costs

- 4.1.6 AI-driven precision micro-dosing in feed mills

- 4.2 Market Restraints

- 4.2.1 Feed-grade organic-acid price volatility

- 4.2.2 Rapidly evolving global AGP regulatory restrictions

- 4.2.3 Fermentation-grade sugar supply bottlenecks for probiotics

- 4.2.4 Mycotoxin interactions reducing additive efficacy

- 4.3 Regulatory Landscape

- 4.4 Technological Outlook

- 4.5 Porters Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Intensity of Competitive Rivalry

5 Market Size and Growth Forecasts

- 5.1 By Type (Value)

- 5.1.1 Probiotics

- 5.1.2 Prebiotics

- 5.1.3 Phytogenics

- 5.1.4 Acidifiers

- 5.1.5 Enzymes

- 5.1.6 Antibiotics

- 5.1.7 Other Types (Ionophores, Hormones)

- 5.2 By Animal Type (Value)

- 5.2.1 Poultry

- 5.2.2 Swine

- 5.2.3 Ruminants

- 5.2.4 Aquaculture

- 5.2.5 Other Animals (Equine, Pets)

- 5.3 By Form (Value)

- 5.3.1 Dry

- 5.3.2 Liquid

- 5.4 By Source (Value)

- 5.4.1 Bacterial

- 5.4.2 Yeast

- 5.4.3 Fungal

- 5.5 By Geography (Value)

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.1.4 Rest of North America

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Spain

- 5.5.3.5 Russia

- 5.5.3.6 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 India

- 5.5.4.4 Australia

- 5.5.4.5 Rest of Asia-Pacific

- 5.5.5 Middle East

- 5.5.5.1 Turkey

- 5.5.5.2 Saudi Arabia

- 5.5.5.3 United Arab Emirates

- 5.5.5.4 Rest of Middle East

- 5.5.6 Africa

- 5.5.6.1 South Africa

- 5.5.6.2 Egypt

- 5.5.6.3 Rest of Africa

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 DSM-Firmenich

- 6.4.2 Cargill, Inc.

- 6.4.3 Vetoquinol

- 6.4.4 Alltech

- 6.4.5 Kemin Industries

- 6.4.6 Huvepharma

- 6.4.7 Novonesis

- 6.4.8 BASF SE

- 6.4.9 ADM

- 6.4.10 Evonik Industries

- 6.4.11 Adisseo

- 6.4.12 Phibro Animal Health

- 6.4.13 Virbac

- 6.4.14 Nutreco