|

시장보고서

상품코드

1849863

음주측정기 : 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Breathalyzers - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

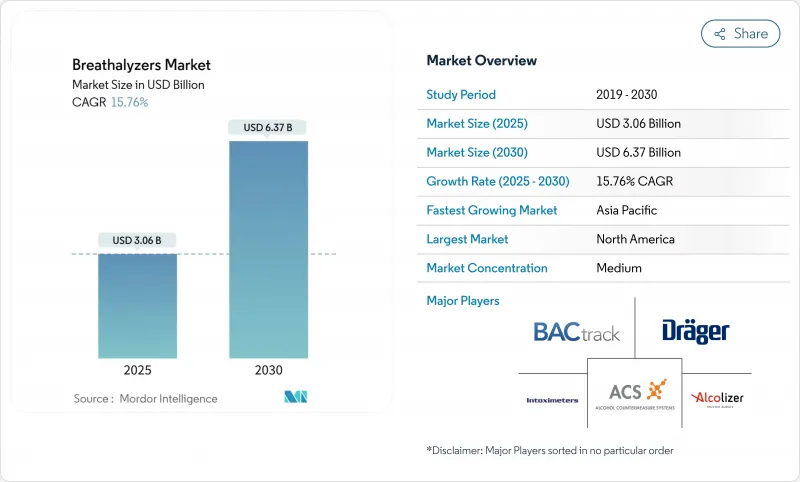

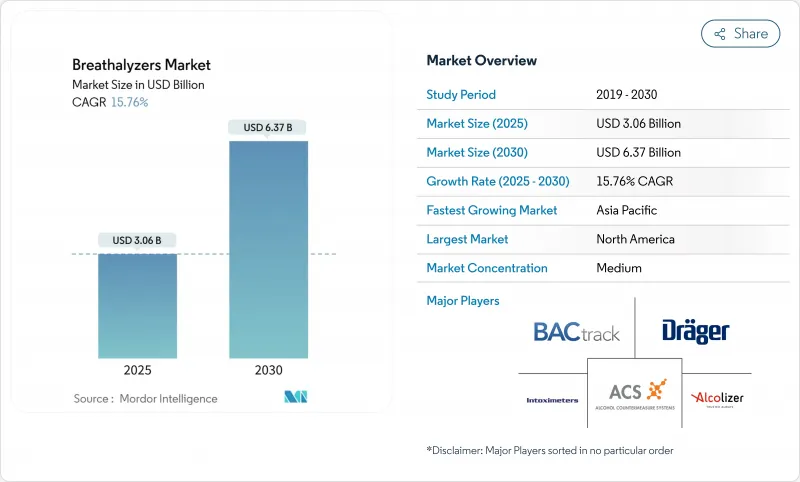

음주측정기 시장 규모는 2025년에 30억 6,000만 달러, 2030년에는 63억 7,000만 달러에 이를 것으로 예상되며, 예측기간 중 CAGR은 15.76%를 나타낼 전망입니다.

주요 경제 지역에서 확장되는 점화 인터록 의무화는 전문 등급 단위로 주문을 안정화하고 재 교정을위한 장기 서비스 계약을 유지합니다. 동시에 소형화된 스마트폰 연동 모델은 시장을 억지에서 일상적인 자기 모니터링으로 전환시키는 소비자 채널을 개척하고 있습니다. 호기 기반 질병 진단이 과학적 뒷받침을 받으면서 제조업체도 건강 관리에 끌려 기존의 안전 기업과 의료기기 전문가와의 새로운 제휴를 촉구하고 있습니다. 이러한 중복 기회는 센서의 정확성, 연결성 및 클라우드 분석에 대한 전략적 투자를 촉구하는 동시에 공공 부문과 소매점 수요의 경계를 모호하게 합니다. 따라서 경쟁사와의 차별화는 하드웨어 단위에서 지속적인 컴플라이언스와 실용적인 데이터를 약속하는 통합 생태계로 전환하고 있습니다.

세계의 음주측정기 시장 동향과 인사이트

음주운전 규제 강화 및 점화 인터록 의무화 확대

국가와 지방자치단체가 허용할 수 있는 혈중 알코올 농도(BAC)의 기준치를 계속 낮추고 있어, 증거가 되는 음주측정기 시장 수요에 기세가 있습니다. 미국에서는 31개 주에서 점화 인터록 의무화가 확대되고 장비의 정기적인 교체 사이클이 확보되고 있습니다. 유타주의 0.05% 규제와 한국 도로 교통법 개정은 보다 광범위한 정책의 축족을 보여줍니다. 법적 틀이 '전범죄자' 점화 인터록 시스템에 수렴함에 따라 범죄자 1인당 장비 수가 증가하고 교정 프로그램의 서비스 수입을 간접적으로 증가시키는 역학이 일하고 있습니다. 실제로 이동식 현장 서비스 밴을 제공하는 판매자는 보호 관찰자의 가동 중지 시간을 줄이고 법원과 범죄자 모두 매력적으로 느끼고 있습니다. 이러한 추세는 견고한 판매 후 네트워크를 가진 판매자가 특히 위반자가 면허 회복 전에 컴플라이언스를 증명해야 하는 경우 불균형 시장 점유율을 얻게 될 수 있음을 시사합니다.

기술 진보와 자금 조달 증가

소형화된 연료전지 센서와 블루투스의 조합은 손바닥 크기의 케이스로 실험실 수준의 정밀도를 실현하여 기술에 익숙하지 않은 소비자의 반복 사용을 촉진합니다. 동시에, 호기 기반 종양학 스크리닝에 대한 벤처 투자가 급증하고, 알코올 검사의 현금 흐름에서 연구 비용을 상호 보조하는 경로가 나타났습니다. 따라서 진단용 IP를 라이선스하는 제조업체는 호기 검사 산업의 정체성을 희박하게 하지 않고 인접한 건강 시장에서 조기 옵셔널리티를 확보할 수 있습니다. 투자 분석가들은 이러한 다각화로 음주 운전 단속 예산과 관련된 수익 순환성이 감소하고 상장하는 공급업체가 기관 투자자들에게 더욱 매력적이 될 것이라고 지적합니다.

높은 수명주기 교정 및 소모품 비용

연 1회의 교정 비용과 교환 가능한 마우스피스는 소규모 플릿이 프로 사양의 유닛으로 업그레이드하는 것을 아직 망설이고 있습니다. 그러나 루이지애나 주에서는 최근 주간이 점화 인터록 요금의 최대 50%를 보조함으로써 공적 자금이 이 장벽을 중화할 수 있음을 입증했습니다. 눈에 보이는 성과는 유지 보수를 매월 정액 요금으로 번들하고 가격에 민감한 구매자의 현금 흐름을 평준화하는 'as-a-service' 모델에 대한 관심이 높아지고 있는 것을 들 수 있습니다. 현재 일부 공급업체는 허용 범위를 벗어나 드리프트할 수 있는 센서에 플래그를 지정하는 예측 유지보수 알고리즘을 채택하여 적극적인 재교정을 가능하게 하고 비용이 많이 드는 증거 분쟁을 줄이고 있습니다.

부문 분석

연료전지 센서는 2024년 음주측정기 시장 점유율의 63.12%를 차지하고 경찰과 재판 시스템의 증거 기준으로서의 지위를 명확히 했습니다. 각 기관은 연료전지 유닛이 아세톤과의 교차 반응성을 거의 나타내지 않는다는 것을 확인합니다. 주목할만한 결과는 예산 감소가이 특수 기술의 교환주기에 영향을 미치지 않으며, 불황 하에서도 공급업체의 수입원이 보호된다는 것입니다. 한편, 산화물 반도체 센서는 초보자의 사용자가 궁극적인 정확도보다 낮은 가격을 중시하기 때문에 관련성을 유지하고,이 카테고리는 소비자 소매로 이익을 올리고 있습니다.

적외선 분광법 시장 규모는 2025년부터 2030년에 걸쳐 CAGR 19.41%를 나타내 연료전지 솔루션과의 과거 차이를 줄일 것으로 예측됩니다. 최근의 비냉각 마이크로 볼로미터 어레이는 전력 소비를 줄이고, 제조업체는 5년 전에 상업적으로 실현 불가능했던 배터리 구동 적외선 핸드헬드를 설계할 수 있게 되었습니다. 이 변화는 다물질 검출을 가능하게 하고, 미래의 장치는 한 번의 호기로 알코올과 규제 약물을 모두 스캔할 가능성을 시사합니다. 탄소나노튜브·코팅을 탐구하는 신흥기업은 빈번한 캘리브레이션 없이 미량 수준의 감도를 제공함으로써 기존의 두 기술을 비약적으로 향상시킬 수 있으며, 개발중인 프로토타입은 이미 12개월의 시험 기간에 걸쳐 유망한 기준선의 안정성을 실증하고 있습니다.

핸드헬드형 음주측정기 시장 규모는 2024년 매출의 54.24%를 차지했습니다. 경찰관은 경량 케이싱이 교통정지시의 처리량을 가속화하고 간접적으로 순찰의 자원을 다른 업무로 돌릴 수 있다는 점에 주목하고 있습니다. 소비자들에게 키체인 모델은 사교 이벤트에서 참신한 아이템이기도 하며 소셜 미디어 플랫폼에서 프리라이드하는 바이럴한 리뷰가 탄생합니다. USB-C 충전에 대한 표준화는 사용자 만족도를 더욱 높여주고, 부속 액세서리 매출(케이블, 파워뱅크)이 하드웨어 채용을 추종한다는 것을 시사합니다.

스마트폰 플러그인 장치는 21.78%의 연평균 복합 성장률(CAGR)을 나타내고 음주측정기 업계의 수익 구성을 대체할 것으로 예측됩니다. 웰니스 앱과의 통합은 일상적인 피트니스 루틴에 알코올 데이터를 통합함으로써 한 번의 읽기가 더 광범위한 건강 대시보드에 공급됨을 의미합니다. 데스크톱 유형은 빈번한 사용을 견디고 안전한 데이터베이스에 연결할 수 있기 때문에 예약 스테이션에 필수적이지만, 그 성장은 공공 기관의 예산주기에 본질적으로 연결되어 있습니다. 경피 손목띠와 같은 연속 장착형 바이오센서는 패시브 대안을 도입하고 있지만, 규제적 익숙성을 고려하여 초기 채용자는 여전히 기존의 호기 장비를 검증을 위한 예비로 구입하고 있습니다.

지역 분석

북미는 2024년에 41.78%의 점유율을 차지해 음주측정기 시장 규모에 가장 크게 공헌하는 지역이었습니다. 이 법은 자동차 제조업체에 음주 운전 방지 기술의 탑재를 의무화하는 것으로, 자동차를 중심으로 하면서도, 알코올의 안전성에 스포트라이트를 맞춘 언설이 퍼짐에 따라, 음주 검출기의 애프터마켓 판매를 간접적으로 자극하고 있습니다. 캐나다가 연구개발의 허브로서 대두하는 것으로, 그 파급효과가 탄생합니다. 국내 공급업체가 조기 도입 시험을 확보하고 나중에 수출 수주로 이어지면 기술 혁신과 상업화 사이의 지역 피드백 루프가 강화됩니다. 이 증거로 양국의 보험사는 텔레매틱스와 연동한 음주운전 할인을 시도하고 있으며, 이 움직임은 소비자 부문의 성장을 유지하고 데이터 분석 수요를 높일 가능성이 높습니다.

음주측정기 업계의 매출은 유럽이 두 번째로 프랑스에서 자동차 운전자에게 일회용 측정기의 휴대를 의무화하고 있으며 정책의 뉘앙스가 대수에 영향을 미칩니다고 이야기하고 있습니다. GDPR(EU 개인정보보호규정)에 대응하면 공급업체는 연결 장치에 고급 익명화 프로토콜을 통합하여 세계 제품 표준을 부주의하게 업그레이드할 수 있습니다. 국경을 넘어선 트럭 플릿이 물류의 혼란을 피하기 위해 범유럽적인 테스트 가이드라인을 채용하고, 다국어 소프트웨어 인터페이스를 가진 제조업체에게 유리한 복수국 일괄 주문을 낳는다는 새로운 관찰도 있습니다. 동지역의 인구동태의 고령화도 조기 발견이 장기적인 헬스케어 비용을 억제하는 예방건강정책의 목표에 부합하기 때문에 호흡진단의 의료 수요를 높여가고 있습니다.

아시아태평양은 가처분 소득 증가와 교통 단속 강화가 결합되어 2030년까지 예측 CAGR이 17.51%를 나타낼 전망입니다. 중국에서는 지명도가 높은 음주운전 박멸 캠페인에 의해 노상 검사가 산발적인 것에서 일상적인 것으로 이행해, 공공 부문으로부터의 수주가 확대하고 있습니다. 일본의 제로 트러런스의 자세는 기술적인 실험을 자극하고 있습니다. 현지 기업은 알코올이 측정되면 점화를 자동으로 잠그는 캐빈 내장 센서를 시험적으로 도입하고 있습니다. 인도에서는 다국적 기업이 현지의 법적 최저 기준을 웃도는 세계 통일된 정책을 적용하고 있으며 직장 안전에 잠재 수요가 있음을 보여줍니다. 이 지역에서는 정부에 의한 저가격 센서의 기술 혁신의 장려도 볼 수 있어 국산 공급업체가 핵심 정밀도를 희생하지 않고 가격면에서 구미의 기존 기업에 과제하고 경쟁방정식을 재구축하는 날이 가까운 것을 시사하고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

목차

제1장 서론

- 조사 전제조건과 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 음주운전에 관한 법률의 강화와 점화 인터록의 의무화 확대

- 기술의 진보와 자금 증가

- 소형화된 스마트폰 접속 디바이스

- 기업 직장에서의 알코올 금지 정책

- 호흡에 근거한 질환 진단에의 자금 제공

- 사용 상황에 근거한 보험에 의한 음주 운전 방지 프로그램

- 시장 성장 억제요인

- 저가격 센서의 정밀도의 편차

- 높은 라이프사이클 교정/소모품 비용

- 데이터 프라이버시와 책임에 대한 우려(GDPR(EU 개인정보보호규정), HIPAA)

- 카메라/웨어러블 장애 기술과의 경쟁

- 공급망 분석

- 기술 전망

- Porter's Five Forces 분석

- 신규 참가업체의 위협

- 구매자의 협상력

- 공급기업의 협상력

- 대체품의 위협

- 경쟁 기업 간 경쟁 관계

제5장 시장 규모와 성장 예측

- 기술별

- 연료전지

- 반도체 산화물 센서

- 적외선 분광법

- 기타

- 제품 유형별

- 핸드헬드/휴대용

- 데스크탑/고정형

- 기타

- 유통 채널별

- 직접 입찰/계약

- 소매점 및 전문점

- 온라인 스토어 및 전자상거래

- 용도별

- 알코올 검출

- 약물 남용 검출

- 질병 진단

- 최종 사용자별

- 법 집행 기관

- 병원 및 클리닉

- 직장/산업

- 개인 소비자

- 기타 최종 사용자

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 기타 유럽

- 아시아태평양

- 중국

- 인도

- 일본

- 호주

- 한국

- 기타 아시아태평양

- 중동 및 아프리카

- GCC

- 남아프리카

- 기타 중동 및 아프리카

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 북미

제6장 경쟁 구도

- 시장 집중도

- 경쟁 벤치마킹

- 시장 점유율 분석

- 기업 프로파일

- Abbott Laboratories

- Alcohol Countermeasure Systems Corp.

- Alcolizer Technology Pty Ltd

- Andatech Pty Ltd

- BACtrack(KHN Solutions)

- Bedfont Scientific Ltd

- CMI, Inc.

- Dragerwerk AG & Co. KGaA

- Giner Labs

- Guardian Interlock Systems

- Hanwei Electronics Group

- Honeywell International(EnviteC)

- Intoximeters Inc.

- Lifeloc Technologies Inc.

- LifeSafer, Inc.

- Lion Laboratories Ltd

- Quest Diagnostics Inc.

- Shenzhen Well Electric Co.

- Smart Start Inc.

- Tokai Denshi Co.

제7장 시장 기회와 향후 전망

KTH 25.11.03The breathalyzers market size is valued at USD 3.06 billion in 2025, is projected to climb to USD 6.37 billion by 2030, and is set to advance at a 15.76% CAGR through the forecast period.

Expanding ignition-interlock mandates across major economies keep a steady flow of orders for professional-grade units and sustain long-term service contracts for recalibration. At the same time, miniaturized, smartphone-linked models are opening a consumer channel that moves the market beyond deterrence and into everyday self-monitoring. Manufacturers are also being pulled toward healthcare as breath-based disease diagnostics gain scientific backing, prompting new partnerships between traditional safety firms and medical-device specialists. These overlapping opportunities are encouraging strategic investments in sensor accuracy, connectivity, and cloud analytics, while also blurring the line between public-sector and retail demand. Competitive differentiation is therefore shifting from hardware alone to integrated ecosystems that promise continuous compliance and actionable data.

Global Breathalyzers Market Trends and Insights

Tightening DUI Legislation and Expansion of Ignition-Interlock Mandates

National and sub-national authorities continue to lower acceptable blood-alcohol content (BAC) thresholds, sustaining demand momentum for evidential Breathalyzer market equipment. Expansion of ignition-interlock mandates in 31 US states ensures a recurring equipment replacement cycle, while similar legal tightening in South Korea and parts of Europe reinforces a dependable order pipeline. Utah's 0.05% limit and South Korea's revised Road Traffic Act illustrate a wider policy pivot. As legal frameworks converge on "all-offender" ignition-interlock schemes, device volume per offender rises, a dynamic that indirectly elevates service revenues from calibration programs. In practice, suppliers that offer mobile field-service vans cut downtime for probationers, which both courts and offenders find appealing. The trend implies that distributors with robust after-sales networks could capture disproportionate breathalyzers market share, especially where offenders must prove compliance before license reinstatement.

Rising Technological Advancements and Increasing Funding

Miniaturized fuel-cell sensors coupled with Bluetooth deliver laboratory-grade accuracy in palm-sized housings, encouraging repeat use by non-technical consumers. Concurrently, venture investment in breath-based oncology screening has surged, signalling a path for cross-subsidizing research costs with alcohol-testing cash flow. Manufacturers that license diagnostic IP therefore secure early optionality in adjacent health markets without diluting their breathalyzer industry identity. Investment analysts note that this diversification reduces revenue cyclicality tied to DUI enforcement budgets, making publicly traded suppliers more attractive to institutional investors.

High Life-Cycle Calibration and Consumable Costs

Annual calibration charges and replaceable mouthpieces still deter small fleets from upgrading to professional-grade units. However, recent state subsidies covering up to 50% of ignition-interlock fees in Louisiana demonstrate that public funding can neutralize this barrier. An observable outcome is rising interest in "as-a-service" models that bundle maintenance into a flat monthly rate, smoothing cash flow for price-sensitive buyers. Some vendors now employ predictive maintenance algorithms that flag sensors likely to drift out of tolerance, allowing proactive recalibration and reducing costly evidence disputes.

Other drivers and restraints analyzed in the detailed report include:

- Corporate Zero-Alcohol Workplace Policies

- Usage-Based-Insurance Sober-Driving Programs

- Competition from Camera / Wearable Impairment Tech

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Fuel cell sensors held 63.12% of the breathalyzers market share in 2024, underscoring their status as the evidential benchmark for police and court systems. Agencies confirm that fuel-cell units show minimal cross-reactivity with acetone, a finding that directly underpins admissibility in legal proceedings. A notable consequence is that budget cuts rarely affect replacement cycles for this specific technology, safeguarding vendor revenue streams even during downturns. Meanwhile, semiconductor oxide sensors retain relevance because novice users value low sticker prices over ultimate precision, keeping this category profitable in consumer retail.

Infrared spectroscopy's market size is forecast to expand by a 19.41% CAGR between 2025-2030, narrowing the historical gap with fuel-cell solutions. Recent uncooled micro-bolometer arrays reduce power draw, letting manufacturers design battery-operated infrared handhelds that were not commercially feasible five years ago. This shift enables multi-substance detection, suggesting future devices may scan for both alcohol and controlled drugs in a single breath. Start-ups exploring carbon-nanotube coatings could leapfrog both incumbent technologies by offering trace-level sensitivity without frequent calibration, and developmental prototypes already demonstrate promising baseline stability over 12-month test horizons.

Hand-held breathalyzers market size accounted for 54.24% of revenue in 2024, thanks to ease of use in roadside scenarios. Police officers note that lightweight casings accelerate traffic-stop throughput, indirectly freeing patrol resources for other duties. For consumers, keychain models double as novelty items at social events, creating viral word-of-mouth that free-rides on social media platforms. Standardization around USB-C charging further lifts user satisfaction, suggesting that ancillary accessory sales (cables, power banks) will follow hardware adoption.

Smartphone plug-in devices are projected to secure a 21.78% CAGR, rewriting the breathalyzers industry revenue mix. Integration with wellness apps means a single reading feeds into broader health dashboards, weaving alcohol data into daily fitness routines. Desktop units remain indispensable in booking stations because they withstand heavy use and connect to secure databases, but their growth is inherently tied to public-sector budget cycles. Continuous-wear biosensors like transdermal wristbands introduce a passive alternative, yet early adopters still purchase traditional breath devices as a verification fallback given regulatory familiarity.

The Breathalyzers Market Report is Segmented by Technology (Fuel Cell, Semiconductor Oxide Sensor, and More), Product Type (Hand-Held / Portable and More), Distribution Channel (Direct Tender / Contracts and More), Application (Alcohol Detection and More), End-User (Law-Enforcement Agencies and More), and Geography (North America, Europe, Asia-Pacific, and More). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America remained the most significant regional contributor to the breathalyzer market size with 41.78% share in 2024, catalyzed by federal infrastructure legislation that obliges automakers to integrate impaired-driving prevention technologies. That mandate, while vehicle-centric, indirectly stimulates aftermarket breathalyzer sales as public discourse spotlights alcohol safety. Canada's emergence as an R&D hub creates spill-over effects: domestic suppliers secure early-adopter trials that later translate to export orders, tightening the regional feedback loop between innovation and commercialization. Evidence suggests that insurers in both countries are experimenting with telematics-linked sober-driving discounts, a move likely to sustain consumer segment growth and elevate data-analytics demand.

Europe ranks second in breathalyzer industry revenue, with France's requirement for motorists to carry disposable testers illustrating how policy nuances influence unit volumes. GDPR compliance pushes vendors to embed advanced anonymization protocols into connected devices, inadvertently upgrading global product standards. A new observation is that cross-border truck fleets adopt pan-European testing guidelines to avoid logistical confusion, creating multi-country bulk orders that favor manufacturers with multilingual software interfaces. The region's aging demographic also elevates medical breath-diagnostics demand, as early detection aligns with preventive-health policy goals that curb long-term healthcare costs.

Asia-Pacific records the fastest forecast CAGR with 17.51% to 2030, as rising disposable incomes intersect with stricter traffic enforcement. China's high-profile anti-drunk-driving campaigns have moved roadside testing from sporadic to routine, swelling public-sector orders. Japan's zero-tolerance stance stimulates technological experimentation; local firms are piloting cabin-embedded sensors that auto-lock ignition if alcohol is detected. India shows latent demand in workplace safety, where multinational corporations apply uniform global policies that exceed local legal minimums. The region is also witnessing government encouragement for low-cost sensor innovation, suggesting that home-grown suppliers may soon challenge Western incumbents on price without sacrificing core accuracy, thereby reshaping competitive equations.

- Abbott Laboratories

- Alcohol Countermeasure Systems Corp.

- Alcolizer Technology

- Andatech

- BACtrack (KHN Solutions)

- Bedfont Scientific

- CMI, Inc.

- Dragerwerk

- Giner Labs

- Guardian Interlock Systems

- Hanwei Electronics Group

- Honeywell International (EnviteC)

- Intoximeters

- Lifeloc Technologies Inc.

- LifeSafer, Inc.

- Lion Laboratories Ltd

- Quest Diagnostics

- Shenzhen Well Electric Co.

- Smart Start Inc.

- Tokai Denshi Co.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Tightening DUI legislation and expansion of ignition-interlock mandates

- 4.2.2 Rising technological advancements and increasing funding

- 4.2.3 Miniaturized smartphone-connected devices

- 4.2.4 Corporate zero-alcohol workplace policies

- 4.2.5 Breath-based disease-diagnostics funding

- 4.2.6 Usage-based-insurance sober-driving programs

- 4.3 Market Restraints

- 4.3.1 Accuracy variability in low-cost sensors

- 4.3.2 High life-cycle calibration/consumable cost

- 4.3.3 Data-privacy & liability concerns (GDPR, HIPAA)

- 4.3.4 Competition from camera / wearable impairment tech

- 4.4 Supply Chain Analysis

- 4.5 Technological Outlook

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Bargaining Power of Suppliers

- 4.6.4 Threat of Substitute Products

- 4.6.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value)

- 5.1 By Technology

- 5.1.1 Fuel Cell

- 5.1.2 Semiconductor Oxide Sensor

- 5.1.3 Infrared Spectroscopy

- 5.1.4 Others

- 5.2 By Product Type

- 5.2.1 Hand-held / Portable

- 5.2.2 Desktop / Stationary

- 5.2.3 Others

- 5.3 By Distribution Channel

- 5.3.1 Direct Tender / Contracts

- 5.3.2 Retail & Specialty Stores

- 5.3.3 Online Stores & E-commerce

- 5.4 By Application

- 5.4.1 Alcohol Detection

- 5.4.2 Drug-abuse Detection

- 5.4.3 Disease Diagnostics

- 5.5 By End-User

- 5.5.1 Law-Enforcement Agencies

- 5.5.2 Hospitals & Clinics

- 5.5.3 Workplace / Industrial

- 5.5.4 Personal Consumers

- 5.5.5 Other End-Users

- 5.6 By Geography (Value)

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 Europe

- 5.6.2.1 Germany

- 5.6.2.2 United Kingdom

- 5.6.2.3 France

- 5.6.2.4 Italy

- 5.6.2.5 Spain

- 5.6.2.6 Rest of Europe

- 5.6.3 Asia-Pacific

- 5.6.3.1 China

- 5.6.3.2 India

- 5.6.3.3 Japan

- 5.6.3.4 Australia

- 5.6.3.5 South Korea

- 5.6.3.6 Rest of Asia-Pacific

- 5.6.4 Middle East & Africa

- 5.6.4.1 GCC

- 5.6.4.2 South Africa

- 5.6.4.3 Rest of Middle East & Africa

- 5.6.5 South America

- 5.6.5.1 Brazil

- 5.6.5.2 Argentina

- 5.6.5.3 Rest of South America

- 5.6.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Competitive Benchmarking

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.4.1 Abbott Laboratories

- 6.4.2 Alcohol Countermeasure Systems Corp.

- 6.4.3 Alcolizer Technology Pty Ltd

- 6.4.4 Andatech Pty Ltd

- 6.4.5 BACtrack (KHN Solutions)

- 6.4.6 Bedfont Scientific Ltd

- 6.4.7 CMI, Inc.

- 6.4.8 Dragerwerk AG & Co. KGaA

- 6.4.9 Giner Labs

- 6.4.10 Guardian Interlock Systems

- 6.4.11 Hanwei Electronics Group

- 6.4.12 Honeywell International (EnviteC)

- 6.4.13 Intoximeters Inc.

- 6.4.14 Lifeloc Technologies Inc.

- 6.4.15 LifeSafer, Inc.

- 6.4.16 Lion Laboratories Ltd

- 6.4.17 Quest Diagnostics Inc.

- 6.4.18 Shenzhen Well Electric Co.

- 6.4.19 Smart Start Inc.

- 6.4.20 Tokai Denshi Co.

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment