|

시장보고서

상품코드

1849875

인도의 농약 산업 : 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Agrochemical Industry In India - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

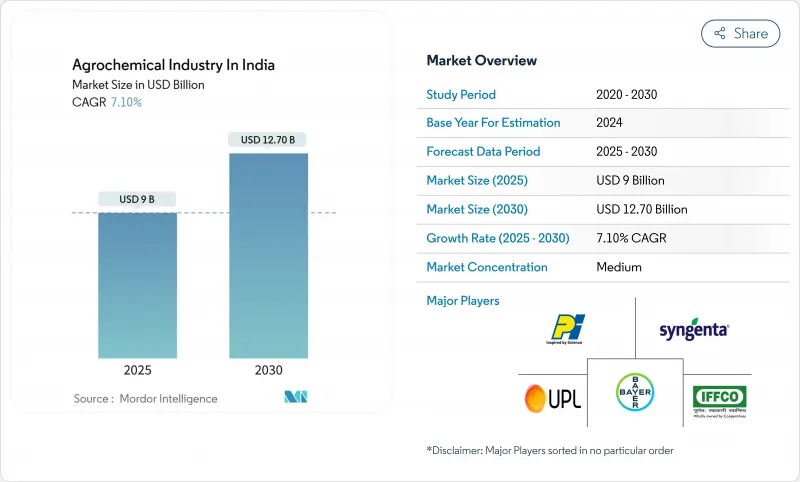

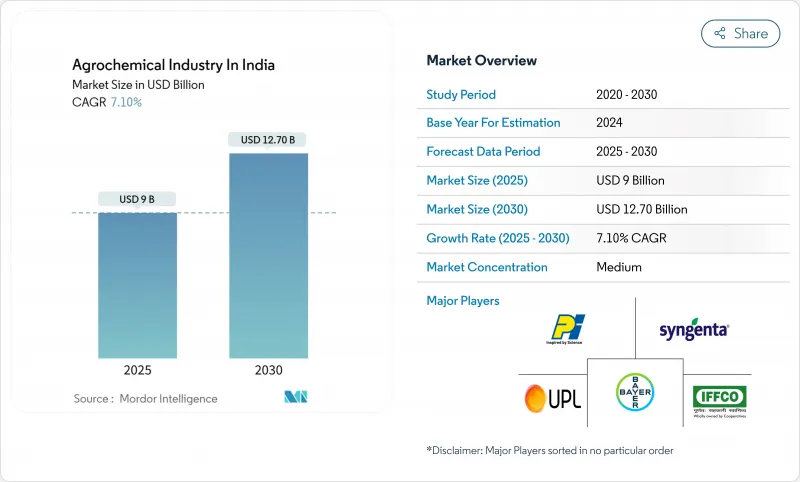

인도의 농약 산업 시장 규모는 2025년에 90억 달러로 추정되고 예측기간 중 CAGR은 7.10%를 나타낼 전망이며, 2030년에는 127억 달러에 달할 것으로 예상됩니다.

강력한 국내 생산능력, 수출 파이프라인 확대, 지속 가능한 투입물을 우월한 정책적인센티브가 이 기세를 뒷받침하고 있습니다. 인도는 여전히 세계 4위의 생산국이며, 매년 50억 달러 상당의 완제품을 유럽, 동남아시아, 서아프리카에 수출하고 있습니다. 제제과학도 진화하고 있으며, 나노영양액과 수분산성 입제는 복용량을 삭감하고 농장의 안전성을 향상시키기 위해 농가들에게 받아들여지고 있습니다. 그럼에도 불구하고 중국의 원재료 의존성과 국가 수준의 독성 금지 패치워크는 인도 농약 시장에 비용 변동과 컴플라이언스의 복잡성을 이어가고 있습니다.

인도의 농약 산업 시장 동향과 인사이트

정부 보조금 합리화가 바이오인풋 채용에 박차를 가한다.

새로운 보조금의 틀은 각 주의 비료 소비의 억제에 보상하는 것으로, 퇴비, 바이오 비료, 나노영양액에 예산 지원을 돌이키는 것입니다. 2025년 연방예산에서는 농업을 위한 예산이 확보되어, 다르다냐 크리시 요자나 총리가 발족해, 인증된 바이오비료로 전환한 농가에게 환불을 실시하는 공식적인 구조가 생겼습니다. PM-PRANAM과 같은 병행 프로그램은 지출을 화학물질 감소 목표에 연결하고 관리자에게 교육 모듈과 현장 실증을 신속하게 진행하도록 촉구합니다.

디지털화된 어그리 크레딧과 전자상거래 네트워크가 라스트원 마일을 확대

정부 출자의 디지털 인프라는 토지 기록, 토양 건강 카드, 크산 신용 카드의 한도를 통일 농가 등록에 통합하여 투입 자재 회사가 몇 분 안에 신용 프로파일을 검토하고 앱 기반 플랫폼을 통해 주문을 발송할 수 있게 되었습니다. 예를 들어, IFFCO의 e-Bazar는 작년에 20만 건 이상의 온라인 거래에 대응하여 27,000개의 핀코드로 배송했습니다. 인도 농약 시장에서 이러한 디지털 레일은 특히 구색의 풍부함이 오랜 제약이었던 제 2 차 산업 지구에서 프리미엄 제제의 판매량 증가로 이어집니다.

원자재의 중국 의존이 비용 변동을 증가

인도 공장은 중국공급업체로부터 비스무트, 텔루르 및 흑연과 같은 기술 중간체의 대부분을 수입하고 있으며, 지정 학적 위기 상황에서 가격 변동 및 출하 지연에 국내 제제 제조업체가 노출되었습니다. 국내 생산자는 더 높은 안전 재고를 가져야 하며 운전자금이 고정되어 세계적인 운임이 상승할 때 금리가 손상됩니다. 정부의 태스크포스는 인도가 100% 수입에 의존하는 10가지 중요한 광물을 확인하고 대체 소스의 신속한 도입을 위한 인센티브 패키지를 초안하고 있습니다.

부문 분석

비료는 인도 농약 시장 규모의 55.2%를 차지하며, 쌀, 밀, 사탕수수 시스템의 식량안전 정책을 계속 지원하고 있습니다. 인산이암모늄과 우레아가 압도적인 점유율을 차지하고 있지만 보조금 제도 개혁이 진행됨에 따라 생산자는 지하수 오염을 최소화하는 미량 영양소 혼합 비료나 나노액비를 요구하게 되었습니다.

생물학적 제제는 베이스는 작은 것, 퇴비 장려책, 잔류물 연동 수출 기준, 유기 인증 면적의 확대에 지지되어, CAGR 10.52%로 2030년까지 매출이 거 증가할 것으로 예측됩니다. 미생물 컨소시엄과 해초 기반의 자극제의 인기가 높아지고 있기 때문에 종래의 비료 제조업체가 바이오 전용 부문을 시작하게 되어 있습니다. 유통기한의 연장, 콜드체인에 의존하지 않는 패키징, 농가 교육 등을 자랑하는 생산자는 선행자 이익을 획득할 수 있다고 생각됩니다.

2024년 인도 농약 시장 규모의 47.3%를 곡물 및 곡류가 차지했지만, 이는 인도·간디케이트 평야의 벼, 밀, 옥수수의 제작 면적의 규모를 반영했습니다. 정부 조달의 프라이스 플로어는 생산자를 주기적인 침체로부터 보호하고, 몬순이 평년 수준의 해에도 투입 자재 수요를 유지합니다. 과일 및 채소는 현재는 수익에 차지하는 비율이 작지만 수출 클래스의 망고, 포도, 바나나가 트렐리스, 관개, 공조 관리 환경으로 이행하여 투입 자재의 집약도가 높아짐에 따라 CAGR 9.13%를 나타낼 것으로 예측됩니다.

푸네, 벵갈루루, 나식 주변의 온실 클러스터에서는 잔류 농약에 대응하는 살균제와 생물화 살충제에 대한 수요가 증가하고 있습니다. 유채종자과 맥박의 제작 면적은 상대적으로 가격에 민감하지만, 황을 많이 포함하는 비료와 생물학적 질소 고정제에 보조금을 내는 국가 자급 미션의 혜택을 받고 있습니다.

인도의 농약 산업 보고서는 제품 유형별(비료, 농약, 기타), 용도별(작물 기반, 비작물 기반), 제형별(액체, 기타), 유통 채널별(농가에 직접 판매, 기타)으로 분류됩니다. 시장 예측은 금액(달러)으로 제공됩니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

목차

제1장 서론

- 조사 전제조건과 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 정부의 보조금 합리화가 바이오 인풋의 도입을 촉진

- 디지털화된 농업신용 및 전자상거래 플랫폼이 화학제품의 도달범위를 확대

- 드론에 의한 정밀 살포가 소규모 농가의 미개척 수요를 해방

- 특허 끊어진 분자의 물결이 수출 파이프라인을 확대

- 기후와 관련된 해충의 발생에 의해 농약 사용량이 증가

- 국내 제조능력을 높이는 정부의 계획

- 시장 성장 억제요인

- 중국에의 원재료의 파괴적 의존이 비용 변동을 증대

- 주 레벨에서의 고독성 활성 물질의 금지를 가속

- 위조품 유통 경로 증가가 브랜드품의 유통량을 감소

- 종래의 살충제에 대한 내성의 강화

- 규제 상황

- 기술 전망

- Porter's Five Forces 분석

- 공급기업의 협상력

- 소비자의 협상력

- 신규 참가업체의 위협

- 대체품의 위협

- 경쟁 기업 간 경쟁 관계

제5장 시장 규모와 성장 예측

- 제품 유형별

- 비료

- 농약

- 살충제

- 제초제

- 살균제

- 보조제

- 식물 생장 조절제

- 용도별

- 작물 기반

- 곡물 및 잡곡

- 유채종자 및 콩류

- 과일 및 채소

- 비작물 기반

- 잔디 및 관상용 식물

- 임업 및 기타

- 작물 기반

- 처방별

- 액체

- 과립/분말

- 나노/마이크로 캡슐화

- 유통 채널별

- 농가 직거래

- 농업 투입재 소매업체

- 전자상거래 플랫폼

제6장 경쟁 구도

- 시장 집중도

- 전략적 동향

- 시장 점유율 분석

- 기업 프로파일

- Bayer AG

- BASF SE

- Syngenta India Private Limited

- UPL

- Corteva Agriscience

- PI Industries

- IFFCO

- Coromandel International Ltd.

- Chambal Fertilisers and Chemicals Limited

- Rallis India Limited

- Deepak Fertilisers and Petrochemicals Corporation Limited(DFPCL)

- Crystal Crop Protection Ltd.

- Sumitomo Chemical India Ltd.

- Dhanuka Agritech Ltd.

- Indofil Industries Limited(Modi Enterprises)

제7장 시장 기회와 향후 전망

KTH 25.11.03The Agrochemical Industry in India Market size is estimated at USD 9 billion in 2025, and is anticipated to reach USD 12.70 billion by 2030, at a CAGR of 7.10% during the forecast period.

Strong domestic manufacturing capacity, expanding export pipelines, and policy incentives that favor sustainable inputs are propelling this momentum. India remains the fourth-largest global producer, shipping finished products worth USD 5 billion each year to destinations in Europe, Southeast Asia, and West Africa. Formulation science is also evolving, nano-nutrient liquids and water-dispersible granules are gaining farmer acceptance because they cut dosage rates and improve field safety. Nonetheless, raw-material dependence on China and a patchwork of state-level toxicity bans continue to inject cost volatility and compliance complexity into the India agrochemicals market.

Agrochemical Industry In India Market Trends and Insights

Government Subsidy Rationalization Spurring Bio-inputs Adoption

New subsidy frameworks reward states for curbing blanket fertilizer consumption and channel budgetary support toward compost, biofertilizers, and nano-nutrient liquids. The 2025 Union Budget set aside for agriculture and launched the Prime Minister Dhan-Dhanya Krishi Yojana, creating a formal mechanism to reimburse farmers who switch to certified biologicals. Parallel programs such as PM-PRANAM link disbursements to chemical reduction targets, encouraging administrators to fast-track training modules and field demonstrations.

Digitized Agri-credit and E-commerce Networks Widening Last-mile Reach

Government-funded digital infrastructure now integrates land records, soil health cards, and Kisan Credit Card limits into a unified farmer registry, allowing input companies to vet credit profiles in minutes and dispatch orders through app-based platforms. IFFCO e-Bazar, for example, fulfilled more than 200,000 online transactions in the past fiscal year and delivered to 27,000 pin codes, a scale previously unimaginable for bulk inputs. For the India agrochemicals market, these digital rails translate into higher off-take of premium formulations, especially in tier-II districts where assortment depth had long been a constraint.

Disruptive Raw-material Dependence on China Raising Cost Volatility

Indian plants import a bulk of technical intermediates such as bismuth, tellurium, and graphite from Chinese suppliers, leaving local formulators exposed to price swings and shipping delays during geopolitical flashpoints. Domestic producers must carry higher safety stocks, locking working capital and eroding margins when global freight rates spike. Government task forces have identified 10 critical minerals where India is 100% import-dependent and are drafting incentive packages to fast-track alternative sources.

Other drivers and restraints analyzed in the detailed report include:

- Drone-based Precision Spraying Unlocking Smallholder Demand

- Off-patent Molecule Wave Expanding Export Pipeline

- Accelerating State-level Bans on High-toxicity Actives

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Fertilizers captured 55.2% of the India agrochemicals market size, and continue to anchor food security policies for rice, wheat, and sugarcane systems. Di-ammonium phosphate and urea dominate volumes, yet escalating subsidy reforms are nudging growers toward micronutrient blends and nano-liquids that minimize groundwater contamination.

Biologicals, though starting from a smaller base, are projected to add nearly incremental sales by 2030 at a 10.52% CAGR, underpinned by compost incentives, residue-linked export standards, and expanding organic certification acreage. The rising popularity of microbial consortia and seaweed-based stimulants is encouraging conventional fertilizer majors to launch dedicated bio-divisions. Producers that master shelf-life extension, cold-chain independent packaging, and farmer education stand to capture early mover loyalty.

Grains and cereals commanded 47.3% of the India agrochemicals market size in 2024, reflecting the scale of paddy, wheat, and maize acreage across the Indo-Gangetic plain. Government procurement price floors insulate growers from cyclical dips and sustain input demand even in sub-normal monsoon years. Fruits and vegetables, while contributing a smaller revenue share today, are projected to expand at a 9.13% CAGR as export-class mangoes, grapes, and bananas shift to trellis, fertigation, and climate-controlled environments that lift input intensity.

Demand for residue-compliant fungicides and biorational insecticides is rising in greenhouse clusters around Pune, Bengaluru, and Nashik. Oilseed and pulse acreage are relatively price-sensitive but benefit from national self-sufficiency missions that subsidize sulfur-rich fertilizers and bio-nitrogen fixers.

The Agrochemical Industry in India Report is Segmented by Product Type (Fertilizers, Pesticides, and More), by Application (Crop-Based and Non-Crop-Based), by Formulation (Liquid, and More), and by Distribution Channel (Direct To Farmer, and More). The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- Bayer AG

- BASF SE

- Syngenta India Private Limited

- UPL

- Corteva Agriscience

- PI Industries

- IFFCO

- Coromandel International Ltd.

- Chambal Fertilisers and Chemicals Limited

- Rallis India Limited

- Deepak Fertilisers and Petrochemicals Corporation Limited (DFPCL)

- Crystal Crop Protection Ltd.

- Sumitomo Chemical India Ltd.

- Dhanuka Agritech Ltd.

- Indofil Industries Limited (Modi Enterprises)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Government subsidy rationalization spurring bio-inputs adoption

- 4.2.2 Digitized agri-credit and e-commerce platforms expanding chemical reach

- 4.2.3 Drone-based precision spraying unlocking untapped smallholder demand

- 4.2.4 Off-patent molecule wave enlarges export pipeline

- 4.2.5 Climate-linked pest outbreaks increasing pesticide intensity

- 4.2.6 Government schemes boosting domestic manufacturing capacity

- 4.3 Market Restraints

- 4.3.1 Disruptive raw-material dependence on China raising cost volatility

- 4.3.2 Accelerating state-level bans on high-toxicity actives

- 4.3.3 Growing counterfeit channel eroding branded volumes

- 4.3.4 Intensifying resistance to legacy insecticides

- 4.4 Regulatory Landscape

- 4.5 Technological Outlook

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Bargaining Power of Suppliers

- 4.6.2 Bargaining Power of Consumers

- 4.6.3 Threat of New Entrants

- 4.6.4 Threat of Substitute Products

- 4.6.5 Intensity of Competitive Rivalry

5 Market Size and Growth Forecasts (Value, USD)

- 5.1 By Product Type

- 5.1.1 Fertilizers

- 5.1.2 Pesticides

- 5.1.2.1 Insecticides

- 5.1.2.2 Herbicides

- 5.1.2.3 Fungicides

- 5.1.3 Adjuvants

- 5.1.4 Plant Growth Regulators

- 5.2 By Application

- 5.2.1 Crop-based

- 5.2.1.1 Grains and Cereals

- 5.2.1.2 Oilseeds and Pulses

- 5.2.1.3 Fruits and Vegetables

- 5.2.2 Non-crop-based

- 5.2.2.1 Turf and Ornamental

- 5.2.2.2 Forestry and Other

- 5.2.1 Crop-based

- 5.3 By Formulation

- 5.3.1 Liquid

- 5.3.2 Granular/Powder

- 5.3.3 Nano/Micro-encapsulated

- 5.4 By Distribution Channel

- 5.4.1 Direct to Farmer

- 5.4.2 Agri-input Retailers

- 5.4.3 E-commerce Platforms

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Bayer AG

- 6.4.2 BASF SE

- 6.4.3 Syngenta India Private Limited

- 6.4.4 UPL

- 6.4.5 Corteva Agriscience

- 6.4.6 PI Industries

- 6.4.7 IFFCO

- 6.4.8 Coromandel International Ltd.

- 6.4.9 Chambal Fertilisers and Chemicals Limited

- 6.4.10 Rallis India Limited

- 6.4.11 Deepak Fertilisers and Petrochemicals Corporation Limited (DFPCL)

- 6.4.12 Crystal Crop Protection Ltd.

- 6.4.13 Sumitomo Chemical India Ltd.

- 6.4.14 Dhanuka Agritech Ltd.

- 6.4.15 Indofil Industries Limited (Modi Enterprises)