|

시장보고서

상품코드

1849887

북미의 카본블랙 : 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)North America Carbon Black - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

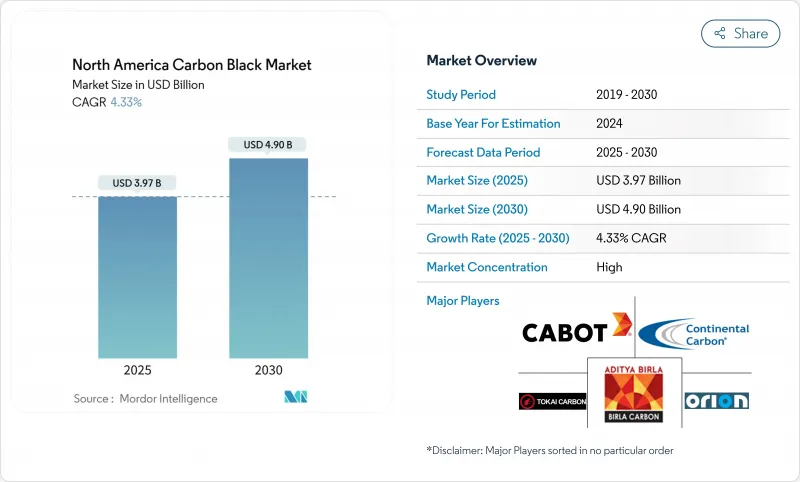

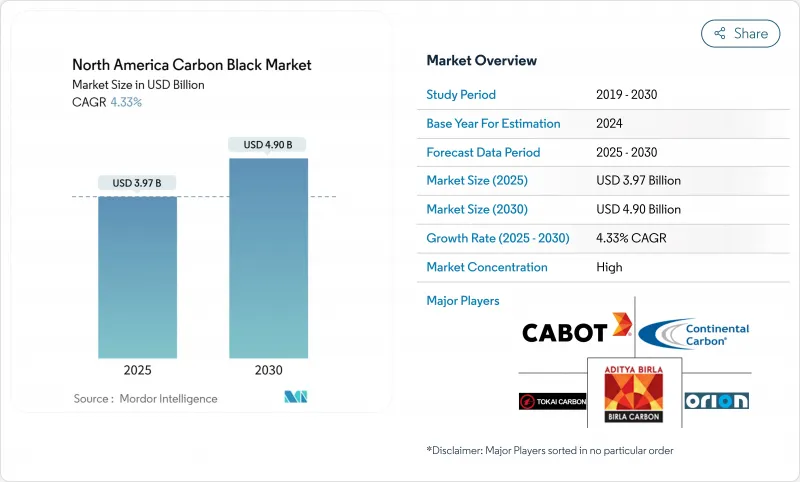

북미의 카본블랙 시장은 2025년 39억 7,000만 달러에 이르고, CAGR 4.33%를 나타내 2030년에는 49억 달러에 달할 것으로 예측됩니다.

이 성장 궤도는 타이어 산업의 전기 이동성으로의 지속적인 이동, 안정적인 플라스틱 수요 및 지역의 지속적인 인프라 투자로부터 혜택을 받는 성숙하지만 탄력적인 분야를 반영합니다. 미국 멕시코만 해안을 따라 견조한 원료 공급력과 에너지 집약도를 낮추는 프로세스 개선으로 생산자의 마진이 강화되어 특수 등급에 대한 적목적 투자가 가능해지고 있습니다. 한편, 캐나다에서는 규제의 추풍이, 멕시코에서는 건설 주도 수요가, 각각 프리미엄화와 최종 용도의 다양화를 촉진하고 있습니다. 경쟁 전략의 중심은 회수 카본블랙의 스케일 업, 독자적인 표면 개질, 타이어 제조업체 및 배터리 제조업체와의 통합 공급 계약이 되어 왔으며, 북미의 카본블랙 시장은 2030년까지 균형 잡힌 성장을 이룰 수 있습니다.

북미의 카본블랙 시장 동향과 인사이트

높은 표면적 퍼니스 블랙을 필요로 하는 와이드 베이스 EV용 타이어 수요 급증

넓은 기반 전기자동차용 타이어는 표준 승용차용 타이어보다 1개당 카본블랙 사용량이 많습니다. 타이어 제조업체는 내구성을 유지하면서 구름 저항을 낮추는 고표면적 퍼니스 블랙을 채용하고 있습니다. 지속가능한 카본블랙 전구체를 배합한 굿이어의 실증 타이어는 그립을 희생하지 않고 구름 저항의 저감을 달성하여 이 재료 전략을 검증하고 있습니다. EV 전용 타이어의 OEM 장착 목표는 스페셜티 블랙의 보급을 가속화하고 북미 카본블랙 시장 전체의 평균 판매 가격을 높일 것으로 예측됩니다. 따라서 첨단 입도 제어 기술을 갖춘 공급업체는 선도적인 EV 타이어 제조업체와 장기 공급 계약을 확보 할 수있는 위치에 있습니다. EV의 성능 기준에 의해 창출된 프리미엄 부문은 기존 타이어 판매량이 두드러지더라도 조율을 높일 것으로 예측됩니다.

미국 멕시코 걸프의 정유소에서 저렴한 비용으로 디캔트 오일이 공급되어 생산자 마진이 향상되었습니다.

2025년 원유 생산량은 1,350만 b/d까지 증가하여 퍼니스 블랙 제조의 주요 원료인 데칸트 오일의 안정 공급이 확보됩니다. 멕시코 걸프의 정유소 인근 생산자는 유럽 및 아시아의 동업자보다 낮은 배송 원료 비용을 누리고 있으며 지속적인 비용 우위를 창출하고 있습니다. 이 차이는 북미 공급업체에게 단기 수익성을 저하시키지 않으면 서 반응로를 에너지 회수 시스템으로 개조하고 회수 카본블랙 파일럿 라인에 자금을 공급하기위한 자본의 유연성을 제공합니다. 그 결과 생산 능력의 합리화 압력은 여전히 낮고, 북미의 카본블랙 시장은 효율적인 사업자에게 유리하고 경쟁적이지만 안정적인 가격 설정 환경의 혜택을 계속 받고 있습니다. 또한 이 비용 쿠션은 바이오 원료와 순환형 원료의 조사를 뒷받침하고, 지역의 생산자를 지속가능성 혁신의 최전선에 서게 하고 있습니다.

걸프 지역 공급 혼란에 따른 원료 가격 변동

허리케인 활동과 정유소의 유지 보수 정지는 정기적으로 데칸트 오일의 유량을 제한하고 스팟 가격의 상승을 일으켜 비 통합 카본블랙 생산자의 마진을 침식하고 있습니다. 미국 에너지 정보국은 멕시코 걸프의 단시간 혼란조차도 지역 원료 시장에 빠르게 파급되고 일부 플랜트는 가동률을 낮추어야 한다고 지적합니다. 공급업체는 저장탱크를 확장하고 상품 헤지 프로그램을 채택하여 변동을 완충하고 있지만, 재고가 늘어나면 운전자금의 필요성이 높아집니다. 균형 시트 능력이 부족한 소규모 기업은 운영 비용의 분산에 직면하여 북미 카본블랙 시장의 통합을 가속화할 수 있습니다. 장기적으로는 대체 슬러리 오일의 사용을 가능하게 하는 다중 원료의 유연성에 대한 투자가 가격 변동을 완화시킬 것이지만, 단기적으로 예측 불가능성은 여전히 역풍이 되고 있습니다.

부문 분석

퍼니스 블랙은 2024년 북미의 카본블랙 시장에서 85%의 점유율을 유지하고 다양한 원료에 대응하는 유연한 반응기 구성을 활용하여 대량 생산 용도로 일관된 품질을 실현했습니다. 이 부문의 점유율 85%는 CAGR 전망 4.71%를 나타내, 북미의 카본블랙 시장 전체의 성장률을 웃돌아 유닛 비용과 배출량을 삭감하는 에너지 회수 업그레이드에 지지되고 있습니다. 열 블랙, 가스 블랙, 램프 블랙은 일반적으로 틈새 부문을 차지하며 특수 플라스틱, 잉크, 배터리 부품 등 독자적인 입자 크기와 순도가 필수적인 것에 공급됩니다. 역량 확장은 타이어 및 기계 고무 제품 제조업체의 왕성한 수요에 힘입어 계속 퍼니스 기술에 집중하고 있습니다.

지속적인 퍼니스의 혁신은 입자 크기 분포의 엄격화와 표면 화학의 맞춤화를 가능하게 하며, 생산자는 고급 배터리 및 경량 복합 부품을 위한 등급을 맞춤화할 수 있습니다. 타이어 열분해 오일과 같은 순환 원료는 처리 능력을 희생하지 않고 노의 작동을 탈탄소화하기 위해 시험적으로 사용됩니다. 이러한 진보는 퍼니스 블랙의 구조적 이점을 강화하고 업계가 지속가능성 요구와 성능 요구사항을 통합하면서 이 프로세스가 리더십을 유지할 수 있도록 합니다.

표준 등급은 2024년 판매량의 78%를 차지했지만 특수 등급은 기준선 시장 성장을 초과하는 5.22%의 연평균 복합 성장률(CAGR) 예측에 도움이 되었으며 이익의 불균형 점유율을 낳았습니다. 전도성 등급과 정전 소산 등급은 전도성이 충전 속도와 사이클 수명을 결정하는 리튬 이온 배터리에서 중요한 역할을 하기 때문에 여전히 작지만 빠르게 확대되고 있습니다.

Journal of Power Sources 잡지에 게재된 설문조사에서는 최적의 전도성 카본블랙의 미세 구조가 더 높은 배터리 에너지 밀도와 관련되어 있으며 배터리 제조업체가 장기 공급 계약을 맺도록 촉구하고 있습니다. 이러한 기술적 의존성은 스위칭 장벽을 높이고 가격 설정의 탄력성을 향상시킵니다. OEM이 보다 높은 재활용률을 추구하는 가운데, rCB와 버진의 스페셜티 블랙을 혼합한 하이브리드 배합은 북미의 카본블랙 업계 전체의 가치 창조를 확대하는 태세를 정돈하고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

목차

제1장 서론

- 조사 전제조건과 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 높은 표면적의 퍼니스 블랙을 필요로 하는 와이드 베이스 EV 타이어 수요 급증

- 미국 걸프의 정유소로부터의 저비용의 디캔트 오일 공급이 생산자의 이익률을 향상

- 캐나다의 타이어 라벨 규제에 의해 특수 그레이드의 채용이 증가

- OEM의 ESG 목표 달성에 의해 회수 카본블랙(rCB) 수요가 증가

- 멕시코의 인프라 건설업의 회복이 플라스틱과 코팅 수요를 자극

- 시장 성장 억제요인

- 멕시코 걸프공급 중단으로 인한 원료 가격 변동

- 승용차 트레드 컴파운드에 있어서의 실리카-실란 치환

- 타이어 열분해 유래 필러와의 경쟁

- 밸류체인 분석

- Porter's Five Forces

- 공급기업의 협상력

- 구매자의 협상력

- 신규 참가업체의 위협

- 대체품의 위협

제5장 시장 규모와 성장 예측(가치와 양)

- 공정 유형별

- 용광로 블랙

- 가스 블랙

- 램프 블랙

- 열 블랙

- 등급별

- 표준 등급 카본블랙

- 특수 카본블랙

- 전도성 및 정전기 방지 카본블랙

- 용도별

- 타이어 및 산업용 고무 제품

- 플라스틱

- 토너 및 인쇄 잉크

- 도료

- 섬유

- 기타 용도

- 최종 사용자 업계별

- 자동차 및 운송

- 포장

- 건축 및 건설

- 전기 및 전자

- 섬유 및 의류

- 기타

- 지역별

- 미국

- 캐나다

- 멕시코

제6장 경쟁 구도

- 시장 집중도

- 전략적 동향

- 시장 점유율 분석

- 기업 프로파일

- Cabot Corporation

- Birla Carbon

- Orion Engineered Carbons SA

- Continental Carbon Company

- Tokai Carbon Co., Ltd.(incl. Cancarb)

- Mitsubishi Chemical Corporation

- OMSK Carbon Group

- PCBL Limited

- Imerys

- Monolith Inc.

- Pyrolyx AG

- Koppers Inc.

- Sid Richardson Carbon & Energy Co.

- International China Rubber Investment Holding Co., Ltd.

제7장 시장 기회와 향후 전망

KTH 25.11.03The North America carbon black market stands at USD 3.97 billion in 2025 and is projected to advance at a 4.33% CAGR to reach USD 4.90 billion by 2030.

This growth trajectory reflects a mature but resilient sector that benefits from the tire industry's ongoing shift toward electric mobility, steady plastics demand, and continued infrastructure spending in the region. Robust feedstock availability along the United States Gulf Coast and process improvements that lower energy intensity are bolstering producer margins and enabling targeted investments in specialty grades. Meanwhile, regulatory tailwinds in Canada and construction-led demand in Mexico are driving premiumization and end-use diversification, respectively. Competitive strategies increasingly center on recovered carbon black scale-up, proprietary surface modifications, and integrated supply agreements with tire and battery makers, positioning the North America carbon black market for balanced growth through 2030.

North America Carbon Black Market Trends and Insights

Surging Demand for Wide-Base EV Tires Requiring High-Surface-Area Furnace Blacks

Wide-base electric vehicle tires use more carbon black per unit than standard passenger tires because higher torque and heavier battery loads accelerate tread wear. Tire makers are deploying high-surface-area furnace blacks that maintain durability while lowering rolling resistance, a balance essential for extending battery range. Goodyear's demonstration tires that blend sustainable carbon black precursors achieved reduced rolling resistance without sacrificing grip, validating this material strategy. OEM fitment targets for EV-specific tires are forecast to accelerate specialty black penetration, enhancing average selling prices across the North America carbon black market. Suppliers with advanced particle-size control technologies are therefore positioned to secure long-term supply contracts with leading EV tire producers. The premium segment created by EV performance standards is expected to lift gross margins even as traditional tire volumes plateau.

Low-Cost Decant Oil Availability from U.S. Gulf Coast Refiners Enhancing Producer Margins

Crude production growth to 13.5 million b/d in 2025 ensures a steady stream of decant oil, the principal feedstock for furnace black manufacturing. Producers near Gulf Coast refineries enjoy lower delivered-feedstock costs than European or Asian peers, creating a durable cost advantage. This differential affords North American suppliers the capital flexibility to retrofit reactors with energy recovery systems and to finance pilot lines for recovered carbon black without eroding near-term profitability. As a result, capacity rationalization pressure remains low, and the North America carbon black market continues to benefit from a competitive but stable pricing environment that favors efficient operators. The cost cushion also underwrites research into bio-based and circular feedstocks, keeping regional producers at the forefront of sustainability innovation.

Feedstock Price Volatility amid Gulf-Coast Supply Disruptions

Hurricane activity and refinery maintenance outages periodically constrain decant oil flow, driving spot price spikes that erode margins for non-integrated carbon black producers. The U.S. Energy Information Administration notes that even brief Gulf Coast disruptions ripple rapidly through regional feedstock markets, forcing some plants to run at reduced rates. Suppliers are expanding storage tanks and adopting commodity hedging programs to buffer volatility, but inventory build-ups raise working capital needs. Smaller firms lacking balance-sheet capacity face higher operating-cost dispersion, potentially accelerating consolidation in the North America carbon black market. Over time, investment in multi-feedstock flexibility, enabling the use of alternative slurry oils, should temper price swings, yet in the near term, unpredictability remains a headwind.

Other drivers and restraints analyzed in the detailed report include:

- Canadian Tire-Label Regulations Boosting Specialty Grade Adoption

- Recovered Carbon Black (rCB) Uptake Driven by OEM ESG Targets

- Silica-Silane Substitution in Passenger-Car Tread Compounds

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Furnace black retained an 85% share of the North America carbon black market in 2024, leveraging flexible reactor configurations that accommodate diverse feedstocks and yield consistent quality across high-volume applications. The segment's 85% shares translates to a 4.71% CAGR outlook, outpacing the overall North America carbon black market size growth, supported by energy recovery upgrades that lower unit costs and emissions. Thermal black, gas black, and lamp black collectively occupy niche segments, supplying specialized plastics, inks, and battery components where unique particle size or purity is essential. Capacity expansions remain concentrated in furnace technology, underpinned by strong demand from tire and mechanical rubber goods producers.

Continued reactor innovation enables tighter particle size distribution and custom surface chemistry, allowing producers to tailor grades for advanced batteries and lightweight composite parts. Circular feedstocks such as tire pyrolysis oil are being piloted to decarbonize furnace operations without sacrificing throughput. These advancements reinforce furnace black's structural advantage, ensuring the process maintains leadership as the North America carbon black industry integrates sustainability imperatives with performance requirements.

Standard grades accounted for 78% of 2024 volume, but specialty grades generated a disproportionate share of profit, aided by a 5.22% CAGR projection that exceeds baseline market growth. Conductive and electrostatic-dissipative grades, while still a smaller slice, are scaling rapidly thanks to their critical role in lithium-ion batteries where conductivity dictates charge rates and cycle life.

Research in the Journal of Power Sources links optimal conductive carbon black micro-structure to higher battery energy density, prompting battery makers to lock in long-term supply contracts. This technical dependency elevates switching barriers and fortifies pricing resilience. As OEMs pursue higher recycled content, hybrid formulations that blend rCB with virgin specialty blacks are poised to extend value creation across the North America carbon black industry.

The North America Carbon Black Market Report Segments the Industry by Process Type (Furnace Black, Gas Black, Lamp Black, and Thermal Black ), Grade (Standard Grade Carbon Black, Specialty Carbon Black, and More), Application (Tires and Industrial Rubber Products, Toners and Printing Inks, and More), End-User Industry (Automotive and Transportation, Packaging, and More), and Geography (United States, Canada, and Mexico).

List of Companies Covered in this Report:

- Cabot Corporation

- Birla Carbon

- Orion Engineered Carbons S.A.

- Continental Carbon Company

- Tokai Carbon Co., Ltd. (incl. Cancarb)

- Mitsubishi Chemical Corporation

- OMSK Carbon Group

- PCBL Limited

- Imerys

- Monolith Inc.

- Pyrolyx AG

- Koppers Inc.

- Sid Richardson Carbon & Energy Co.

- International China Rubber Investment Holding Co., Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surging Demand for Wide-Base EV Tires Requiring High-Surface-Area Furnace Blacks

- 4.2.2 Low-Cost Decant Oil Availability from U.S. Gulf Coast Refiners Enhancing Producer Margins

- 4.2.3 Canadian Tire-Label Regulations Boosting Specialty Grade Adoption

- 4.2.4 Recovered Carbon Black (rCB) Uptake Driven by OEM ESG Targets

- 4.2.5 Infrastructure-Led Construction Rebound in Mexico Spurring Plastics and Coatings Demand

- 4.3 Market Restraints

- 4.3.1 Feedstock Price Volatility Amid Gulf-Coast Supply Disruptions

- 4.3.2 Silica-Silane Substitution in Passenger-Car Tread Compounds

- 4.3.3 Competition from Tire-Pyrolysis Derived Fillers

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

5 Market Size and Growth Forecasts (Value and Volume)

- 5.1 By Process Type

- 5.1.1 Furnace Black

- 5.1.2 Gas Black

- 5.1.3 Lamp Black

- 5.1.4 Thermal Black

- 5.2 By Grade

- 5.2.1 Standard Grade Carbon Black

- 5.2.2 Specialty Carbon Black

- 5.2.3 Conductive and ESD Carbon Black

- 5.3 By Application

- 5.3.1 Tires and Industrial Rubber Products

- 5.3.2 Plastics

- 5.3.3 Toners and Printing Inks

- 5.3.4 Coatings

- 5.3.5 Textile Fibers

- 5.3.6 Other Applications

- 5.4 By End-user Industry

- 5.4.1 Automotive and Transportation

- 5.4.2 Packaging

- 5.4.3 Building and Construction

- 5.4.4 Electrical and Electronics

- 5.4.5 Textile and Apparel

- 5.4.6 Others

- 5.5 By Geography

- 5.5.1 United States

- 5.5.2 Canada

- 5.5.3 Mexico

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)}

- 6.4.1 Cabot Corporation

- 6.4.2 Birla Carbon

- 6.4.3 Orion Engineered Carbons S.A.

- 6.4.4 Continental Carbon Company

- 6.4.5 Tokai Carbon Co., Ltd. (incl. Cancarb)

- 6.4.6 Mitsubishi Chemical Corporation

- 6.4.7 OMSK Carbon Group

- 6.4.8 PCBL Limited

- 6.4.9 Imerys

- 6.4.10 Monolith Inc.

- 6.4.11 Pyrolyx AG

- 6.4.12 Koppers Inc.

- 6.4.13 Sid Richardson Carbon & Energy Co.

- 6.4.14 International China Rubber Investment Holding Co., Ltd.

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment

- 7.2 Growth in the Adoption of Electric Cars