|

시장보고서

상품코드

1849901

양자점(QD) : 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Quantum Dots (QD) - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

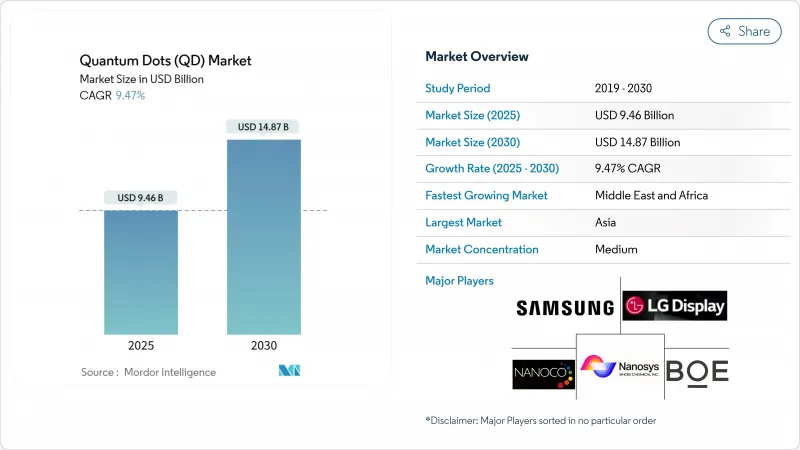

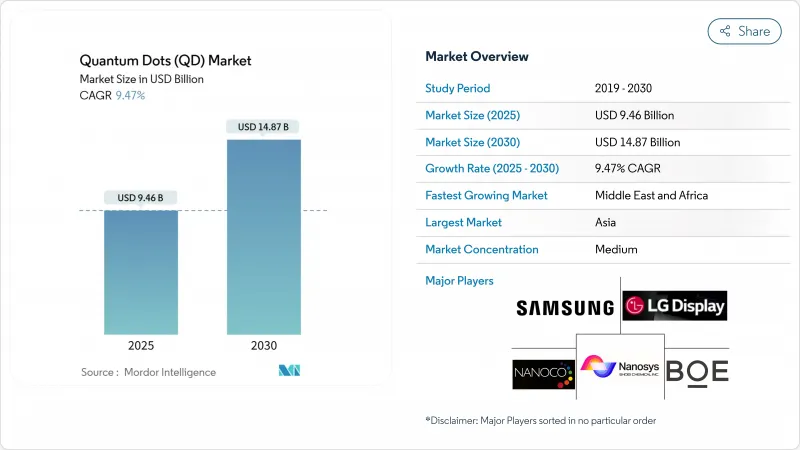

세계의 양자점(QD) 시장은 2025년에 94억 6,000만 달러로 평가되었고, 2030년에 148억 7,000만 달러에 이를 전망입니다.

상업적 성숙도가 가속화되고 있으며, 해당 기술은 실험실 단계에서 초고화질 디스플레이, 양자 보안 통신 노드, 차세대 생체 영상 플랫폼용 대량 생산 부품으로 전환되고 있습니다. 중국의 양자점 TV 급속한 보급, EU RoHS 제한을 준수하는 카드뮴 프리 화학물질의 등장, 아시아 및 중동 지역의 지속적인 정부 지원이 장기적 수요를 유지하고 있습니다. 아시아태평양 지역의 제조 규모 이점과 효율성 및 색 순도를 높이는 페로브스카이트 기술의 돌파구가 결합되어 기존 OLED 대안보다 단위 비용을 더 빠르게 낮추며 대중적 소비자 가격대를 열어가고 있습니다. 동시에 반도체 양자점을 기반으로 한 양자 컴퓨팅 아키텍처와 암 진단에서 5배 향상된 감도는 디스플레이를 훨씬 넘어선 총 잠재 시장 기회를 확장하고 있습니다.

세계의 양자점(QD) 시장 동향 및 인사이트

중국이 주도하는 초고화질 TV 패널에 양자점(QD) 채택

국내 패널 제조사들은 100% 이상의 NTSC 색 영역을 구현하는 고용량 양자점 필름 라인을 설치했으며, TCL의 QM6K 시리즈는 슈퍼 하이 에너지 LED 백라이트를 통해 98% 이상의 DCI-P3 커버리지와 53% 향상된 밝기를 달성했습니다. 2026년 가동 예정인 BOE의 90억 달러 규모 Gen-8.6 AMOLED 공장은 비용 경쟁력을 강화하고 지역 브랜드의 공급을 확보합니다. RGB OLED에서 QD-OLED 아키텍처로의 전환은 제조 공정을 단순화하여 4K 및 8K 스크린의 수율 향상과 평방미터당 자본 지출(Capex) 절감을 가져옵니다.

EU 소비자용 전자기기에서 카드뮴 프리 양자점(QD)의 규제 추진

RoHS 기준 EU의 0.01wt% 카드뮴 상한선으로 선행 기업들은 구리-인듐 및 인듐-인화물 제형으로 전환 중입니다. UbiQD의 2천만 달러 규모 시리즈 B 투자 유치로 카드뮴 프리 생산이 확대될 예정이며, 애플라이드 머티리얼즈는 색 변환층에서 카드뮴 성능을 대체하는 무연 디바이스 구현을 입증했습니다. 대학들은 유기 용매를 제거하고 공정 배출을 줄이는 수성 합성 경로를 상용화하여 도입 기업에 비용 및 규정 준수 이점을 창출하고 있습니다.

고순도 인화 인듐 전구체 공급 체인 병목

6G 인프라 수요로 인한 인듐 소비량은 연간 생산량의 4%를 차지할 것으로 예상되어, 인듐 인화물 양자점 공급을 압박하고 가격 상승을 부추길 전망입니다. 소주대학교의 잉크 엔지니어링 공정은 태양광 발전 비용을 0.06달러/와트피로 낮추지만, 소수 정제업체 외에는 여전히 희소한 인듐의 일관된 순도에 의존합니다. 마이크로웨이브 보조 및 이온성 액체 합성은 유해 시약을 줄이지만 여전히 안정적인 금속 원료 공급이 필요하여, 적어도 2028년까지 공급 리스크가 높게 유지될 전망입니다.

부문 분석

카드뮴 기반 II-VI 화합물은 2024년 매출의 48.3%를 차지하며, 확립된 공급망과 높은 양자 수율을 바탕으로 양자점 시장을 주도했습니다. 그러나 EU와 캘리포니아 정책이 경원소 화학 물질로 전환되면서 규제 노출로 인해 전망이 위축되고 있습니다. 11.7% CAGR로 성장하는 페로브스카이트 변종은 실험실 신기술에서 생산 가능한 발광체로 진화하며, 카드뮴의 밝기를 따라잡고 상온에서 단일 광자 순도를 달성해 보안 통신 분야의 활용성을 확대하고 있습니다. 인듐 인화물 플랫폼은 UbiQD의 규모 확대 자금과 Applied Materials의 공정 최적화로 혜택을 보지만, 전구체 부족으로 단기 보급이 제한됩니다. 실리콘 및 탄소 양자점은 생의학적 틈새 시장을 개척 중이며, 임상적 관련 용량에서 무시할 만한 세포 독성을 보이며 형광 유도 수술을 가능케 합니다. 역사적 데이터에 따르면 2020-2024년 동안 카드뮴 대체재는 연간 15-20% 성장한 반면 기존 카드뮴 소재는 5% 미만 성장해 양자점 시장의 구조적 전환을 시사합니다.

2세대 소재는 최종 사용처 다각화를 이끕니다. 실리콘 나노쉘과 융합된 그래핀 양자점은 진딧물 개체군을 71% 억제하여 디스플레이를 넘어 정밀 농업용 나노소재로 자리매김했습니다. 페로브스카이트 발광층은 이제 140 PPI로 인쇄 가능해 중형 모니터 통합이 용이해졌으며, 실리콘 도트는 웨어러블 바이오센서에 필수적인 안정적인 적외선 광발광을 제공합니다. 카드뮴 프리 부문의 양자점 시장 규모는 두 자릿수 성장률을 보일 것으로 전망되며, 이는 공급업체들의 저독성 화학물질 전환을 가속화할 것입니다. 강화된 기업 ESG 목표와 다가오는 RoHS 면제 종료 시한은 전환 경로를 확고히 합니다.

QD 필름은 2024년 72.1% 점유율로 여전히 매출 주축을 이루며, 기존 LCD 스택에 간편하게 적용 가능한 플러그 앤 플레이 컬러 컨버터를 찾는 TV OEM 업체들의 선호를 받고 있습니다. 그러나 반도체 파브가 파운드리 플랫폼에 직접 광자 방출체를 구현함에 따라 온칩 양자점은 12.7%라는 가장 높은 연평균 성장률(CAGR)을 보입니다. 케임브리지 대학의 13,000스핀 양자 레지스터는 130μs 코히런스에서 69% 정확도를 달성하며 칩 규모 양자 노드의 도약 가능성을 입증했습니다. 마이크로플루이딕 반응기를 통해 성장된 코어-쉘 나노필러는 이제 5% 미만의 크기 분산을 보여 코히런트 방출에 필수적입니다. 골판지 웨이퍼에 전기영동 증착을 적용해 균열 없는 근적외선 검출기를 생산함으로써 자동차용 LiDAR 및 의료용 내시경 시장이 열렸다. 선폭 축소 한계에 도달한 가운데, 통합 광학 기술은 실리콘 광학 로드맵에서 누락된 단일 광자 소스를 양자점이 공급함으로써 ‘무어의 법칙을 뛰어넘는’ 확장성을 제공합니다.

스케일링 경로는 갈라집니다. 잉크젯 프린팅 QD-OLED 패널은 상용 수율로 이미 31.5인치 대각선을 달성한 반면, 전기수력학 제팅은 마이크로LED 어레이용 마이크론 규모 RGB 픽셀을 생산합니다. 양자 컴퓨팅 성능 향상으로 ASP 상승이 정당화됨에 따라 온칩 형식이 차지하는 양자점 시장 규모는 확대될 전망입니다. 원자층 증착 및 원자 정밀도 리소그래피에 대한 투자는 도트 배치를 트랜지스터 게이트와 더욱 정밀하게 정렬시켜 양자 버스 내 상호연결 지연을 축소할 것입니다. 장치 OEM 업체들은 패키징, 열 관리, 리소그래피 정렬 분야의 지적재산권을 묶어 새로운 방위적 경쟁 우위를 구축 중입니다.

지역 분석

아시아태평양 지역은 수직 통합형 패널 제조사와 국가 차원의 연구개발(R&D) 투자로 2024년 매출의 38.4%를 차지하며 선도적 위치를 유지합니다. 삼성디스플레이의 109억 달러 규모 QD-OLED 라인 전환과 한국의 491조 원 규모 양자 프로그램이 생태계를 공고히 하는 한편, 중국의 BOE는 현지 공급망을 주도하는 8.6세대 생산라인에 90억 달러를 투자하고 있습니다. 일본은 공정 혁신으로 제조 역량을 보완하며 독성 및 내구성 병목 현상 해결을 위한 세미나를 개최합니다. 아시아의 양자점 시장 규모는 프리미엄 TV에 대한 내수 수요와 북미 및 유럽으로의 수출 흐름에 의해 지속적으로 뒷받침됩니다.

북미에서는 캠브리지 대학(캠브리지와 미국의 공동 연구), MIT 링컨 연구소, 로스앨러모스 국립연구소의 심층 연구 자산으로 양자 보안 링크 및 고효율 태양광 발전 분야를 주도합니다. 벤처 캐피털 유치 동향은 우비큐디(UbiQD)의 2천만 달러 자금 조달과 이온큐(IonQ)의 주요 인수 사례로 입증되며 견고합니다. 강력한 지적 재산권 보호와 연방 자금 지원이 상용화 파이프라인을 보장하며, 카드뮴 화합물에 대한 미국의 수출 통제 심사는 공급업체들을 인듐 인화물 기반 생산으로 전환시키고 있습니다. 유럽은 규제 영향력을 활용한다. RoHS(유해물질제한지침) 준수가 카드뮴 프리 채택을 촉진하는 한편, 리에주 대학의 수성 합성법은 유해 폐기물을 줄입니다. 정부 그린딜 기금은 에너지 플러스 건물용 양자점 창문 필름을 도입합니다.

중동 및 아프리카 지역은 10.6%의 가장 빠른 연평균 성장률(CAGR)을 기록합니다. UAE의 노르마 센터, 카타르의 1천만 달러 프로그램, 사우디 R&D 기금은 석유 경제 다각화를 목표로 양자점 컴퓨팅 클러스터를 육성합니다. 수입 대체 정책으로 양자점 강화 태양광 패널 및 의료 기기의 현지 조립이 촉진됩니다. 라틴아메리카에서는 양자점 온실 시트가 고지대 농장의 과일 수확량을 향상시키는 농업 기술 분야에서 초기 수요가 나타나고 있으나 시장 침투율은 여전히 3% 미만입니다. 전반적으로 지역별 매출 분산이 집중 위험을 완화한다. 중동 및 아프리카가 투자 흐름을 흡수하고 서구 지역이 핵심 소재 가공을 현지화함에 따라 아시아의 점유율은 2030년까지 35%로 점차 하락할 전망입니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

목차

제1장 서론

- 조사의 전제조건과 시장의 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 중국이 주도하는 초고화질 TV 패널에 양자점(QD) 채택

- EU의 소비자용 전자 기기에서 카드뮴 프리 양자 도트(QD)의 규제 추진

- 디스플레이 백라이트용 페로브스카이트 양자점의 급속한 상용화

- 의료 응용 분야에서 양자점 기반 생체 영상 제제의 급증

- 한국의 정부 지원 양자 소재 연구개발 프로그램

- 시장 성장 억제요인

- 고순도 인화 인듐 전구체공급 체인의 병목

- 습기 노출 시 페로브스카이트 QD의 성능 저하

- 유럽의 카드뮴 규제에 따른 환경 규정 준수 비용

- QD 마이크로 LED 통합을 위한 제한된 대량 생산 인프라

- 업계 생태계 분석

- 기술 전망(생산 기술)

- Porter's Five Forces 분석

- 공급기업의 협상력

- 구매자의 협상력

- 신규 참가업체의 위협

- 대체품의 위협

- 경쟁도

- 투자분석

제5장 시장 규모와 성장 예측

- 소재 유형별

- 카드뮴 기반 II-VI족(CdSe, CdS, CdTe)

- 카드뮴 프리 III-V족(InP, GaAs)

- 페로브스카이트 양자점(QD)

- 실리콘 양자점(QD)

- 그래핀과 탄소 양자점(QD)

- 장치 형태별

- QD 필름

- 온칩 양자점(QD)

- 코어-쉘 및 인-쉘 구조

- 용도별

- 디스플레이

- QD-LCD

- QD-OLED

- 마이크로 LED 통합

- 조명

- 일반 조명

- 특수 조명

- 태양전지 및 태양광 발전

- 의료 화상 진단

- 약물전달 및 테라노스틱스

- 센서 및 기기

- 양자 컴퓨팅 및 보안

- 농업 및 식품

- 기타

- 디스플레이

- 최종 이용 산업별

- 소비자 가전

- 헬스케어 및 생명과학

- 에너지 및 전력

- 방위와 안보

- 농업

- 기타

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 북유럽 국가

- 기타 유럽

- 남미

- 브라질

- 기타 남미

- 아시아태평양

- 중국

- 일본

- 인도

- 동남아시아

- 기타 아시아태평양

- 중동 및 아프리카

- 중동

- GCC

- 튀르키예

- 기타 중동

- 아프리카

- 남아프리카

- 기타 아프리카

- 북미

제6장 경쟁 구도

- 시장 집중도

- 전략적 동향

- 시장 점유율 분석

- 기업 프로파일

- Samsung Electronics Co., Ltd.

- Nanosys Inc.

- LG Display Co., Ltd.

- BOE Technology Group Co., Ltd.

- Nanoco Group PLC

- Quantum Materials Corporation

- UbiQD, Inc.

- Ocean NanoTech LLC

- Thermo Fisher Scientific Inc.

- Merck KGaA

- Avantama AG

- Quantum Solutions Inc.

- QD Laser, Inc.

- OSRAM Licht AG

- Sony Corporation

- TCL CSOT

- Crystalplex Corporation

- Evident Technologies

- NN-Labs(NNCrystal US Corp.)

- Nanophotonica Inc.

- Quantum Science Ltd.

- Toray Industries, Inc.

제7장 시장 기회와 장래의 전망

HBR 25.11.14The global quantum dots market stood at USD 9.46 billion in 2025 and is forecast to reach USD 14.87 billion by 2030, reflecting a 9.47% CAGR over the period.

Commercial maturity is accelerating as the technology migrates from laboratory discovery to mass-produced components in ultra-high-definition displays, quantum-secure communication nodes, and next-generation bio-imaging platforms. China's rapid uptake of quantum-dot televisions, the emergence of cadmium-free chemistries that comply with EU RoHS limits, and sustained government funding in Asia and the Middle East are sustaining long-term demand. Manufacturing scale advantages in Asia-Pacific, combined with perovskite breakthroughs that lift efficiency and color purity, are lowering unit costs faster than legacy OLED alternatives, opening mainstream consumer price points. In parallel, quantum computing architectures based on semiconductor quantum dots, and five-fold sensitivity gains in cancer diagnostics, are expanding total addressable opportunities well beyond displays.

Global Quantum Dots (QD) Market Trends and Insights

Quantum-dot adoption in ultra-high-definition television panels, led by China

Domestic panel makers have installed high-capacity quantum-dot film lines that deliver more than 100% NTSC color gamut, while TCL's QM6K series achieves 98%+ DCI-P3 coverage and 53% higher brightness through Super High Energy LED back-lights. BOE's USD 9 billion Gen-8.6 AMOLED facility, coming online in 2026, reinforces cost leadership and secures supply for regional brands. The shift from RGB OLED to QD-OLED architectures simplifies manufacturing, enhancing yield and lowering capex per square meter for 4K and 8K screens.

Regulatory push for cadmium-free quantum dots in EU consumer electronics

The EU's 0.01 wt% cadmium cap under RoHS is driving early movers toward copper-indium and indium-phosphide formulations. UbiQD's USD 20 million Series B round will scale cadmium-free production, while Applied Materials has proven lead-free devices matching cadmium performance in color conversion layers. Universities are commercializing aqueous synthesis routes that remove organic solvents and cut process emissions, creating cost and compliance advantages for adopters.

Supply-chain bottlenecks for high-purity indium-phosphide precursors

Indium demand from 6G infrastructure is projected to consume 4% of annual production, squeezing availability for indium-phosphide quantum dots and pushing prices higher. Soochow University's ink-engineering route lowers photovoltaic costs to USD 0.06/Wp but relies on consistent indium purity, which remains scarce outside a handful of refiners. Microwave-assisted and ionic-liquid syntheses reduce hazardous reagents yet still require secure metal feedstocks, keeping supply risk elevated through at least 2028.

Other drivers and restraints analyzed in the detailed report include:

- Rapid commercialization of perovskite quantum dots in display back-lighting

- Surge in quantum-dot bio-imaging agents in healthcare applications

- Performance degradation of perovskite quantum dots under moisture exposure

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Cadmium-based II-VI compounds held 48.3% of 2024 revenues, anchoring the quantum dots market through well-established supply chains and high quantum yields. Regulatory exposure, however, compresses their outlook as EU and California policies converge on lighter-element chemistries. Perovskite variants, supported by 11.7% CAGR, move from lab novelty to production-ready emitters that match cadmium brightness and achieve room-temperature single-photon purity, broadening relevance for secure communications. Indium-phosphide platforms benefit from UbiQD's scale-up funding and Applied Materials' process optimization, yet precursor shortages temper near-term penetration. Silicon and carbon quantum dots are carving biomedical niches, showing negligible cytotoxicity at clinically relevant doses and enabling fluorescence-guided surgery. Historic data reveal cadmium alternatives growing 15-20% annually versus sub-5% for cadmium incumbents from 2020-2024, signaling a structural pivot in the quantum dots market.

Second-generation materials diversify end-use reach. Graphene quantum dots fused with silicon nanoshells achieve 71% aphid-population suppression, positioning nanomaterials for precision agriculture beyond displays. Perovskite glow layers are now printable at 140 PPI, easing integration into mid-sized monitors, while silicon dots deliver stable infrared photoluminescence critical for wearable biosensors. The quantum dots market size for cadmium-free segments is projected to rise at double-digit rates, reinforcing supplier pivots toward low-toxicity chemistries. Heightened corporate ESG targets, plus upcoming RoHS exemptions sunsets, cement the transition path.

QD films remain revenue mainstays with 72.1% share in 2024, favored by television OEMs seeking plug-and-play color converters that slip into existing LCD stacks. Yet on-chip quantum dots display the highest 12.7% CAGR as semiconductor fabs capture photonic emitters directly on foundry platforms. University of Cambridge's 13,000-spin quantum register, achieving 69% fidelity at 130 µs coherence, underscores leapfrog potential for chip-scale quantum nodes. Core-shell nanopillars grown through microfluidic reactors now exhibit sub-5% size dispersion, crucial for coherent emission. Electrophoretic deposition on corrugated wafers yields crack-free near-infrared detectors, opening automotive LiDAR and medical endoscope markets. As line width reductions plateau, integrated photonics offers Moore-than-More scaling, with quantum dots supplying the single-photon sources missing from silicon photonics roadmaps.

Scaling pathways diverge. Inkjet printed QD-OLED panels already hit 31.5-inch diagonals at commercial yield, while electrohydrodynamic jetting produces micron-scale RGB pixels for microLED arrays. The quantum dots market size captured by on-chip formats is set to widen as performance gains in quantum computing justify higher ASPs. Investments in atomic-layer deposition and atomic-precision lithography will further align dot placement with transistor gateways, shrinking interconnect delays in quantum buses. Device OEMs are bundling intellectual property around packaging, thermal management, and lithographic alignment, creating new defensible moats.

The Quantum Dots (QD) Market is Segmented by Material Type (Cadmium-Based II-VI (CdSe, Cds, Cdte), Cadmium-Free III-V (InP, Gaas), and More), Device Form Factor (QD Films, On-Chip Quantum Dots, and More), Application (Displays, Lighting, Solar Cells and Photovoltaics, and More), End-Use Industry (Consumer Electronics, Healthcare and Life Sciences, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific maintains leadership with 38.4% of 2024 revenue due to vertically integrated panel makers and deliberate national R&D funding. Samsung Display's USD 10.9 billion conversion to QD-OLED lines and South Korea's KRW 491 billion quantum program cement the ecosystem, while China's BOE invests USD 9 billion in Gen-8.6 capacity that anchors local supply chains. Japan complements manufacturing heft with process innovation, hosting seminars to solve toxicity and durability bottlenecks. The quantum dots market size in Asia remains underpinned by domestic demand for premium TVs and by export flows into North America and Europe.

North America follows with deep research assets at University of Cambridge (Cambridge-US collaborations), MIT Lincoln Laboratory, and Los Alamos National Laboratory driving quantum-secure links and high-efficiency photovoltaics. Venture capital traction is robust, proven by UbiQD's USD 20 million raise and IonQ's headline acquisitions. Strong IP protection and federal funding ensure commercialization pipelines, and US export-control scrutiny over cadmium compounds nudges suppliers toward indium-phosphide builds. Europe leverages regulatory influence: RoHS compliance sparks cadmium-free adoption, while University of Liege's aqueous syntheses cut hazardous waste. Government green-deal funds deploy quantum-dot window films for energy-positive buildings.

The Middle East and Africa record the fastest 10.6% CAGR. UAE's Norma Center, Qatar's USD 10 million program, and Saudi R&D funds foster quantum-dot computing clusters, aiming to diversify oil economies. Import substitution policies encourage local assembly of QD-enhanced solar panels and medical devices. Latin America sees nascent demand in agrotechnology, where quantum-dot greenhouse sheets improve fruit yield in high-altitude farms, yet market penetration remains under 3%. Overall, geographic revenue dispersion reduces concentration risk: Asia's share inches lower toward 35% by 2030 as Middle East and Africa capture investment flows and as Western regions on-shore critical materials processing.

- Samsung Electronics Co., Ltd.

- Nanosys Inc.

- LG Display Co., Ltd.

- BOE Technology Group Co., Ltd.

- Nanoco Group PLC

- Quantum Materials Corporation

- UbiQD, Inc.

- Ocean NanoTech LLC

- Thermo Fisher Scientific Inc.

- Merck KGaA

- Avantama AG

- Quantum Solutions Inc.

- QD Laser, Inc.

- OSRAM Licht AG

- Sony Corporation

- TCL CSOT

- Crystalplex Corporation

- Evident Technologies

- NN-Labs (NNCrystal US Corp.)

- Nanophotonica Inc.

- Quantum Science Ltd.

- Toray Industries, Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Quantum Dot Adoption in Ultra-High-Definition Television Panels, Led by China

- 4.2.2 Regulatory Push for Cadmium-Free Quantum Dots in EU Consumer Electronics

- 4.2.3 Rapid Commercialization of Perovskite Quantum Dots in Display Back-Lighting

- 4.2.4 Surge in Quantum Dot-Based Bio-Imaging Agents in Healthcare Applications

- 4.2.5 Government-Funded Quantum-Materials R&D Programs in South Korea

- 4.3 Market Restraints

- 4.3.1 Supply-Chain Bottlenecks for High-Purity Indium-Phosphide Precursors

- 4.3.2 Performance Degradation of Perovskite QDs Under Moisture Exposure

- 4.3.3 Environmental-Compliance Costs of Cadmium Regulations in Europe

- 4.3.4 Limited Mass-Manufacturing Infrastructure for QD Micro-LED Integration

- 4.4 Industry Ecosystem Analysis

- 4.5 Technological Outlook (Production Technology)

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Bargaining Power of Suppliers

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Threat of New Entrants

- 4.6.4 Threat of Substitutes

- 4.6.5 Degree of Competition

- 4.7 Investment Analysis

5 MARKET SIZE AND GROWTH FORECASTS (VALUES)

- 5.1 By Material Type

- 5.1.1 Cadmium-based II-VI (CdSe, CdS, CdTe)

- 5.1.2 Cadmium-Free III-V (InP, GaAs)

- 5.1.3 Perovskite Quantum Dots

- 5.1.4 Silicon Quantum Dots

- 5.1.5 Graphene and Carbon Quantum Dots

- 5.2 By Device Form Factor

- 5.2.1 QD Films

- 5.2.2 On-Chip Quantum Dots

- 5.2.3 Core-Shell and In-Shell Architectures

- 5.3 By Application

- 5.3.1 Displays

- 5.3.1.1 QD-LCD

- 5.3.1.2 QD-OLED

- 5.3.1.3 Micro-LED Integration

- 5.3.2 Lighting

- 5.3.2.1 General Illumination

- 5.3.2.2 Specialty Lighting

- 5.3.3 Solar Cells and Photovoltaics

- 5.3.4 Medical Imaging and Diagnostics

- 5.3.5 Drug Delivery and Theranostics

- 5.3.6 Sensors and Instruments

- 5.3.7 Quantum Computing and Security

- 5.3.8 Agriculture and Food

- 5.3.9 Others

- 5.3.1 Displays

- 5.4 By End-Use Industry

- 5.4.1 Consumer Electronics

- 5.4.2 Healthcare and Life Sciences

- 5.4.3 Energy and Power

- 5.4.4 Defense and Security

- 5.4.5 Agriculture

- 5.4.6 Others

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Nordics

- 5.5.2.5 Rest of Europe

- 5.5.3 South America

- 5.5.3.1 Brazil

- 5.5.3.2 Rest of South America

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 India

- 5.5.4.4 South-East Asia

- 5.5.4.5 Rest of Asia-Pacific

- 5.5.5 Middle East and Africa

- 5.5.5.1 Middle East

- 5.5.5.1.1 Gulf Cooperation Council Countries

- 5.5.5.1.2 Turkey

- 5.5.5.1.3 Rest of Middle East

- 5.5.5.2 Africa

- 5.5.5.2.1 South Africa

- 5.5.5.2.2 Rest of Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Samsung Electronics Co., Ltd.

- 6.4.2 Nanosys Inc.

- 6.4.3 LG Display Co., Ltd.

- 6.4.4 BOE Technology Group Co., Ltd.

- 6.4.5 Nanoco Group PLC

- 6.4.6 Quantum Materials Corporation

- 6.4.7 UbiQD, Inc.

- 6.4.8 Ocean NanoTech LLC

- 6.4.9 Thermo Fisher Scientific Inc.

- 6.4.10 Merck KGaA

- 6.4.11 Avantama AG

- 6.4.12 Quantum Solutions Inc.

- 6.4.13 QD Laser, Inc.

- 6.4.14 OSRAM Licht AG

- 6.4.15 Sony Corporation

- 6.4.16 TCL CSOT

- 6.4.17 Crystalplex Corporation

- 6.4.18 Evident Technologies

- 6.4.19 NN-Labs (NNCrystal US Corp.)

- 6.4.20 Nanophotonica Inc.

- 6.4.21 Quantum Science Ltd.

- 6.4.22 Toray Industries, Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment