|

시장보고서

상품코드

1849915

생분해성 고분자 : 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Bio-degradable Polymers - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

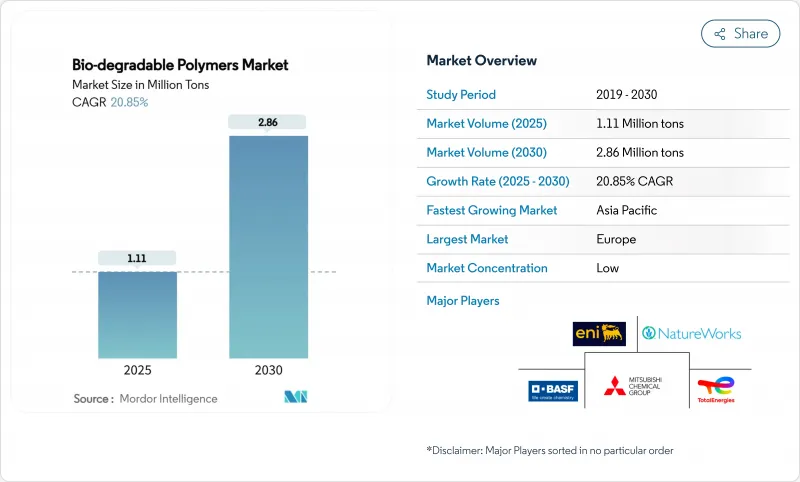

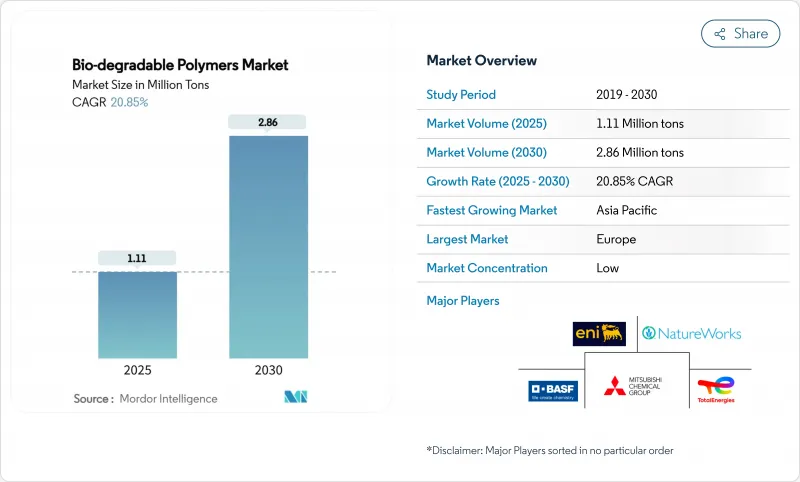

생분해성 고분자 시장 규모는 2025년에 111만톤으로 평가되었고, 2030년에 286만톤에 이를 것으로 예측되며, 예측기간(2025-2030년)의 CAGR은 20.85%를 나타낼 전망입니다.

규제 압박 강화, 기업의 지속가능성 목표 확대, 미생물 생산 기술의 급속한 발전이 고성능 저탄소 소재 수요를 주도하고 있습니다. 유럽은 여전히 최대 지역 소비국이지만, 산업 규모 확대와 지원 정책으로 아시아태평양 지역이 가장 빠르게 성장하고 있습니다. 제품 혁신은 현재 해양 분해성 등급과 비용 효율적인 PHA에 집중되고 있으며, 석유화학 대기업, 특수 바이오플라스틱 기업, 스타트업이 동시에 생산 능력과 연구 개발에 투자하면서 경쟁이 심화되고 있습니다.

세계의 생분해성 고분자 시장 동향 및 인사이트

일회용 플라스틱에 대한 정부 규정

글로벌 규제 제정이 소재 흐름을 재편하고 있습니다. 2024년 확정된 유럽연합(EU)의 '포장재 및 포장 폐기물 규정'은 EU 내에서 판매되는 모든 포장재의 재활용을 의무화하고 단계적 폐기물 감축 목표를 설정함으로써, 가공업체들이 즉시 인증된 퇴비화 가능 또는 재활용 등급 소재로 전환하도록 유도하고 있습니다. 2024년 4월 도입된 영국의 플라스틱 함유 물티슈 금지 조치는 위생 제품 시장의 기회를 더욱 확대합니다. 홍콩의 2024년 빨대 및 EPS 용기 등 일회용품 금지 조치는 아시아에서도 유사한 추세를 예고합니다. 이러한 조치들은 종합적으로 신규 폴리머 공장 투자 회수 기간을 단축하고, 공급 계약을 가속화하며, 하류 브랜드의 채택을 촉진하고 있습니다.

지속 가능한 포장에 대한 수요 증가

브랜드 소유자들은 이제 지속가능성을 단순한 규정 준수 활동이 아닌 성장 동력으로 간주합니다. 프리미엄 식품 및 음료 제조업체들은 수명 종료 시 배출량을 줄이는 PLA, PHA 및 코팅 종이 구조로 전환하고 있습니다. 포츠머스 대학의 실험실 증거에 따르면 PLA는 해수-햇빛 노출 시 기존 PP보다 9배 적은 미세플라스틱을 배출하여 해양 환경을 중시하는 소비자들 사이에서 브랜드 평판을 개선합니다. 재활용 가능성 설계 지침과 전자상거래 확장은 수요를 더욱 촉진하여 필름, 트레이, 경질 용기에 대한 대량 수요 포켓을 창출합니다.

높은 생산 비용

장비 감가상각, 특수 원료, 소규모 공장 규모로 인해 평균 판매 가격이 일반 PE 및 PP보다 높게 유지됩니다. 2025년 Danimer Scientific의 파산 신청은 기술 선도 기업조차도 수익성 악화에 직면했음을 보여줍니다. 생산 능력 증대와 공정 고도화로 비용이 감소하고 있지만, 많은 가공업체들은 여전히 대중 시장 포장 분야 진출을 주저하고 있습니다.

부문 분석

전분 기반 등급은 풍부한 원료 공급과 기존 블로운 필름 및 열성형 라인과 호환성 덕분에 생분해성 폴리머 시장 점유율의 41.05%를 차지합니다. PLA는 경질 포장재 및 의료 기기 분야에서 견고한 입지를 유지하고 있습니다. PHA의 생분해성 폴리머 시장 규모는 빠른 해양 분해 특성 및 미생물 발효 수율 개선에 힘입어 23.49%의 연평균 복합 성장률(CAGR)로 성장할 것으로 전망됩니다. PBS 및 PBAT와 같은 폴리에스터 계열은 접착 필름 및 위생용 백시트 시장에서 점유율을 확대하고 있으며, 셀룰로오스 유도체는 코팅 및 종이컵 분야에 활용되고 있습니다.

비용 균등화는 여전히 달성하기 어렵습니다. 전분 블렌드는 농업 보조금과 단순한 복합 가공의 이점을 누리지만, PHA 개발사는 탄소 포집 크레딧과 고마진 의료 판매로 이익을 얻습니다. 예측 가능한 블렌드 시스템으로의 수렴은 균형 잡힌 비용-성능을 제공할 수 있습니다.

지역 분석

유럽의 39.19% 시장 점유율 우위는 정책 명확성과 소비자 환경 의식에서 비롯됩니다. 2024년 확정된 EU 규정은 재활용 가능 또는 퇴비화 가능한 포장재를 의무화하며, 핀란드 포튬(Fortum)의 CO2-폴리머 전환 플랜트와 같은 획기적 프로젝트는 탄소 포집 기술이 바이오 기반 생산과 어떻게 통합되는지 보여줍니다.

아시아태평양 지역은 29.44%의 연평균 복합 성장률(CAGR)로 가장 빠르게 성장하는 지역입니다. 중국은 국가 플라스틱 금지 시한을 맞추고 농업용 필름을 공급하기 위해 PHA 및 PBAT 공장을 확대하고 있습니다. 일본은 해양 부표 적용을 위해 이황화 결합을 도입한 해양 분해성 PBS를 혁신하고 있습니다.

북미는 기술 혁신과 자발적 기업 목표를 결합합니다. 다우(Dow)와 뉴에너지블루(New Energy Blue)의 협약은 옥수수 줄기를 활용해 PE 자산용 바이오 에틸렌을 생산함으로써 저탄소 대체 경로를 열었습니다. 남미와 중동은 아직 초기 단계이지만, 밭소각을 줄이기 위한 생분해성 멀칭에 관심을 보이고 있습니다. 산업용 퇴비화 시설 부족으로 즉각적인 도입은 제한되나 장기적 인프라 기회를 시사합니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

목차

제1장 서론

- 조사의 전제조건과 시장의 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 일회용 플라스틱 사용에 대한 정부 규제

- 지속 가능하고 환경 친화적인 포장에 대한 수요 증가

- 의료 산업에서 생분해성 플라스틱 채택 증가

- 농업 산업에서 생분해성 필름 사용 급증

- 생분해성 폴리머 제조 공정 혁신으로 수율 향상

- 시장 성장 억제요인

- 기존 플라스틱 대비 높은 생산 비용

- 자동차 산업에서 소비 제한을 초래하는 제한된 기계적 성능

- 산업용 퇴비화 시설의 부족

- 밸류체인 분석

- 규제 전망

- Porter's Five Forces

- 공급기업의 협상력

- 구매자의 협상력

- 신규 참가업체의 위협

- 대체품의 위협

- 경쟁도

제5장 시장 규모와 성장 예측

- 유형별

- 전분 기반 플라스틱

- 폴리유산(PLA)

- 폴리하이드록시알칸산(PHA)

- 폴리에스테르(PBS, PBAT, PCL)

- 셀룰로오스 유도체

- 원료별

- 사탕수수와 사탕

- 옥수수 및 기타 전분 작물

- 셀룰로오스와 목질 바이오매스

- 폐기 식물 유지

- 조류 및 미생물 바이오매스

- 최종 사용자 업계별

- 포장

- 소비재

- 섬유

- 농업

- 헬스케어

- 기타(자동차, 건설 등)

- 지역별

- 아시아태평양

- 중국

- 인도

- 일본

- 한국

- ASEAN

- 기타 아시아태평양

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 기타 유럽

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 중동 및 아프리카

- 사우디아라비아

- 남아프리카

- 기타 중동 및 아프리카

- 아시아태평양

제6장 경쟁 구도

- 시장 집중도

- 전략적 동향

- 시장 점유율(%)/랭킹 분석

- 기업 프로파일

- BASF

- Biome Bioplastics

- BIOTEC Biologische Naturverpackungen GmbH & Co. KG.

- Braskem

- CJ CheilJedang Corp

- Danimer Scientific

- DuPont

- Evonik Industries AG

- FKuR

- GENECIS

- Mitsubishi Chemical Group Corporation

- NatureWorks LLC

- Eni SpA(Novamont)

- Plantic

- PTT MCC Biochem Co., Ltd.

- BEWI

- TEIJIN LIMITED

- TORAY INDUSTRIES, INC.

- TotalEnergies(Total Corbion)

- Zhejiang Hisun Biomaterials Co., Ltd.

제7장 시장 기회와 장래의 전망

HBR 25.11.14The Bio-degradable Polymers Market size is estimated at 1.11 Million tons in 2025, and is expected to reach 2.86 Million tons by 2030, at a CAGR of 20.85% during the forecast period (2025-2030).

Heightened regulatory pressure, widening corporate sustainability goals, and rapid progress in microbial production technologies steer demand toward high-performance, low-carbon materials. Europe remains the largest regional consumer, while Asia-Pacific is advancing fastest due to industrial scale-up and supportive legislation. Product innovation now centers on marine-degradable grades and cost-efficient PHA, and competition is intensifying as petrochemical majors, specialty bioplastic firms, and start-ups invest simultaneously in capacity and research and development.

Global Bio-degradable Polymers Market Trends and Insights

Government Regulations Against Single-Use Plastics

Global rulemaking is reshaping material flows. The European Union's Packaging and Packaging Waste Regulation, finalized in 2024, obliges all packaging sold in the bloc to be recyclable and sets stepwise waste-reduction targets, immediately directing converters toward certified compostable or recyclable grades. The UK's ban on wet wipes containing plastic, introduced in April 2024, further enlarges the hygiene-product opportunity. Hong Kong's 2024 prohibition on single-use items such as straws and EPS containers signals similar momentum in Asia. Together, these measures are shortening payback periods for new polymer plants, accelerating off-take agreements, and incentivizing downstream brand adoption.

Growing Demand for Sustainable Packaging

Brand owners now treat sustainability as a growth driver rather than a compliance exercise. Premium food and beverage producers are shifting to PLA, PHA, and coated paper structures that lower end-of-life emissions. Laboratory evidence from the University of Portsmouth shows PLA emits nine times fewer microplastics under seawater-sunlight exposure than conventional PP, improving brand reputations among ocean-minded consumers. Design-for-recyclability guidelines and e-commerce expansion add to the pull, creating high-volume demand pockets for films, trays, and rigid containers.

High Production Cost

Equipment amortization, specialty feedstocks, and modest plant scales keep average selling prices above commodity PE and PP. The bankruptcy filing of Danimer Scientific in 2025 underscores profitability headwinds even for technology leaders. While increased capacity and process intensification are driving costs down, many converters still hesitate to commit to mass-market packaging segments.

Other drivers and restraints analyzed in the detailed report include:

- Increasing Adoption in the Healthcare Industry

- Surge in Agricultural Films Usage

- Limited Mechanical Performance

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Starch-based grades hold 41.05% of the bio-degradable polymers market share due to abundant feedstock and compatibility with existing blown-film and thermoforming lines. PLA maintains a robust position in rigid packaging and medical devices. The bio-degradable polymers market size for PHA is projected to grow at a 23.49% CAGR, aided by its rapid marine degradation profile and improvements in microbial fermentation yields. Polyester families such as PBS and PBAT are gaining share in cling films and hygiene backsheets, while cellulosic derivatives serve coatings and paper cups.

Cost parity remains elusive. Starch blends enjoy agricultural subsidies and simpler compounding, but PHA developers benefit from carbon-capture credits and high-margin medical sales. A foreseeable convergence toward blended systems may deliver balanced cost-performance.

The Biodegradable Polymers Market Report Segments the Industry by Type (Starch-Based Plastics, Polylactic Acid (PLA), Polyhydroxy Alkanoates (PHA), and More), Feedstock (Sugarcane and Sugar Beets, Corn and Other Starch Crops, and More), End-User Industry (Packaging, Consumer Goods, Textile, and More), and Geography (Asia-Pacific, North America, Europe, and More). The Market Forecasts are Provided in Terms of Volume (Tons).

Geography Analysis

Europe's 39.19% leadership stems from policy clarity and consumer eco-awareness. The EU regulation finalized in 2024 forces recyclable or compostable packaging, and landmark projects such as Fortum's CO2-to-polymer plant in Finland illustrate how carbon capture integrates with bio-based production.

Asia-Pacific is the fastest-growing region at 29.44% CAGR. China ramps up PHA and PBAT plants to meet national plastic-ban deadlines and to supply agriculture films. Japan innovates marine-degradable PBS incorporating disulfide bonds for ocean buoy applications.

North America combines technological innovation with voluntary corporate targets. Dow's agreement with New Energy Blue uses corn stover to make bio-ethylene for PE assets, opening a low-carbon drop-in path. South America and the Middle East remain nascent but show interest in biodegradable mulch to reduce field-burning. Lack of industrial composting facilities curbs immediate uptake yet signals long-term infrastructure opportunities.

- BASF

- Biome Bioplastics

- BIOTEC Biologische Naturverpackungen GmbH & Co. KG.

- Braskem

- CJ CheilJedang Corp

- Danimer Scientific

- DuPont

- Evonik Industries AG

- FKuR

- GENECIS

- Mitsubishi Chemical Group Corporation

- NatureWorks LLC

- Eni S.p.A. (Novamont)

- Plantic

- PTT MCC Biochem Co., Ltd.

- BEWI

- TEIJIN LIMITED

- TORAY INDUSTRIES, INC.

- TotalEnergies (Total Corbion)

- Zhejiang Hisun Biomaterials Co., Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Government Regulations Againts the usage of SingleUse Plastics

- 4.2.2 Growing Demand for Sustainable and Eco-Friendly Packaging

- 4.2.3 Increasing Adoption of Bio Degradable Plastics in the Healthcare Industry

- 4.2.4 Surge in the Usage of Bio-Degradable Films in the Agricultural Industry

- 4.2.5 Growing Innovations in the Manufacturing Processes of Bio-Degradable Polymers Improving its Yield

- 4.3 Market Restraints

- 4.3.1 High Production Cost with Respect to Conventional Plastics

- 4.3.2 Limited Mechanical Performance Restricting Consumption in Automotive

- 4.3.3 Lack of Industrial Composting Facilities

- 4.4 Value Chain Analysis

- 4.5 Regulatory Outlook

- 4.6 Porter's Five Forces

- 4.6.1 Bargaining Power of Suppliers

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Threat of New Entrants

- 4.6.4 Threat of Substitutes

- 4.6.5 Degree of Competition

5 Market Size and Growth Forecasts (Volume)

- 5.1 By Type

- 5.1.1 Starch-Based Plastics

- 5.1.2 Polylactic Acid (PLA)

- 5.1.3 Polyhydroxyalkanoates (PHA)

- 5.1.4 Polyesters (PBS, PBAT and PCL)

- 5.1.5 Cellulosic Derivatives

- 5.2 By Feedstock

- 5.2.1 Sugarcane and Sugar Beets

- 5.2.2 Corn and Other Starch Crops

- 5.2.3 Cellulose and Wood Biomass

- 5.2.4 Waste Vegetable Oils and Fats

- 5.2.5 Algal and Microbial Biomass

- 5.3 By End-user Industry

- 5.3.1 Packaging

- 5.3.2 Consumer Goods

- 5.3.3 Textile

- 5.3.4 Agriculture

- 5.3.5 Healthcare

- 5.3.6 Others (Automotive, Construction, etc.)

- 5.4 By Geography

- 5.4.1 Asia-Pacific

- 5.4.1.1 China

- 5.4.1.2 India

- 5.4.1.3 Japan

- 5.4.1.4 South Korea

- 5.4.1.5 ASEAN

- 5.4.1.6 Rest of Asia-Pacific

- 5.4.2 North America

- 5.4.2.1 United States

- 5.4.2.2 Canada

- 5.4.2.3 Mexico

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 France

- 5.4.3.4 Italy

- 5.4.3.5 Rest of Europe

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Rest of South America

- 5.4.5 Middle-East and Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 South Africa

- 5.4.5.3 Rest of Middle-East and Africa

- 5.4.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share (%)/Ranking Analysis

- 6.4 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, Recent Developments)}

- 6.4.1 BASF

- 6.4.2 Biome Bioplastics

- 6.4.3 BIOTEC Biologische Naturverpackungen GmbH & Co. KG.

- 6.4.4 Braskem

- 6.4.5 CJ CheilJedang Corp

- 6.4.6 Danimer Scientific

- 6.4.7 DuPont

- 6.4.8 Evonik Industries AG

- 6.4.9 FKuR

- 6.4.10 GENECIS

- 6.4.11 Mitsubishi Chemical Group Corporation

- 6.4.12 NatureWorks LLC

- 6.4.13 Eni S.p.A. (Novamont)

- 6.4.14 Plantic

- 6.4.15 PTT MCC Biochem Co., Ltd.

- 6.4.16 BEWI

- 6.4.17 TEIJIN LIMITED

- 6.4.18 TORAY INDUSTRIES, INC.

- 6.4.19 TotalEnergies (Total Corbion)

- 6.4.20 Zhejiang Hisun Biomaterials Co., Ltd.

7 Market Opportunities and Future Outlook

- 7.1 White-Space and Unmet-Need Assessment

- 7.2 Growing Inclination for Marine Degradable Polymers for Ocean Cleanups