|

시장보고서

상품코드

1849916

자동차용 에어백 인플레이터 : 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Automotive Airbag Inflator - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

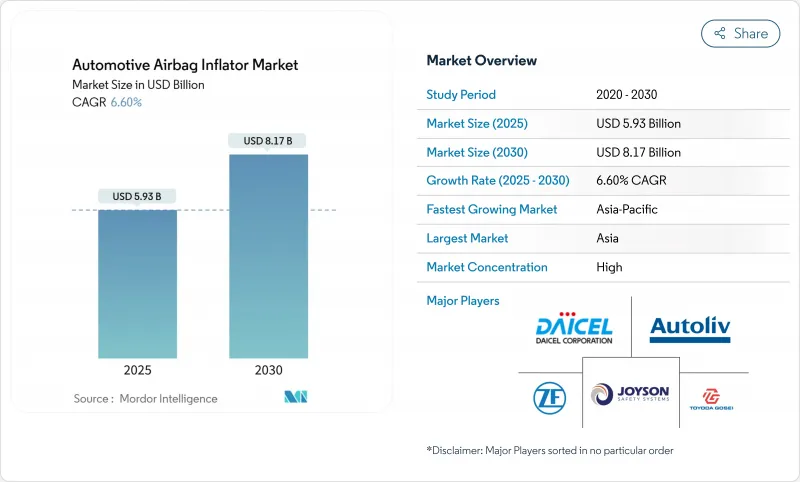

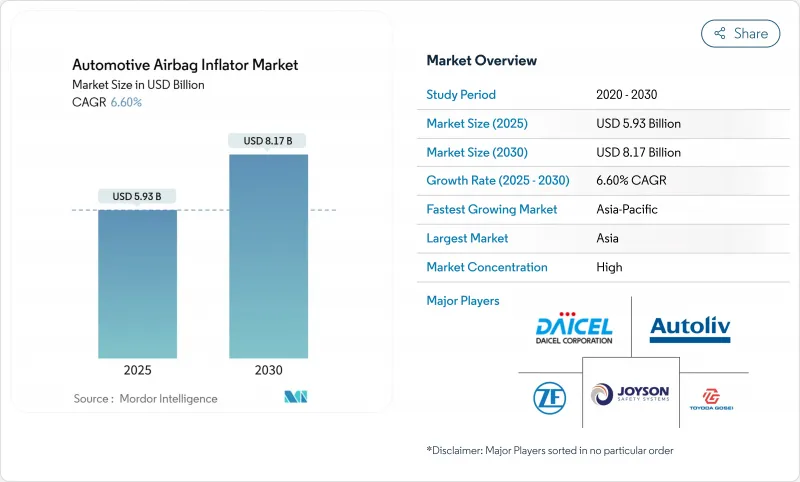

자동차용 에어백 인플레이터 시장 규모는 2025년에 59억 3,000만 달러로 평가되었고, 2030년에 81억 7,000만 달러에 이를 것으로 예측되며, 2025-2030년까지 연평균 복합 성장률(CAGR)은 6.60%를 나타낼 전망입니다.

강화된 충돌 안전 법규, 승객 보호에 대한 소비자 관심 증대, 인플레이터 화학 및 패키징 기술의 지속적인 발전이 자동차용 에어백 인플레이터 시장 성장을 뒷받침하고 있습니다. 설계부터 제조까지의 워크플로우를 통제하는 공급업체들은 계약 조립업체에 의존하는 기업들보다 새로운 규제 테스트에 더 빠르게 대응함으로써 더 높은 마진을 확보합니다. 북미 및 유럽 규제 기관들은 향후 측면 충돌 및 사이버 보안 감사를 예고했으며, 이는 비용 증가와 교체 물량 확대를 초래하여 차량 생산 주기가 정체된 시기에도 자동차용 에어백 인플레이터 시장을 지탱할 것입니다. 아시아태평양 지역은 이미 7.50%의 연평균 성장률(CAGR)을 보이고 있으며, 기술 집약적인 중국 중형 SUV 프로그램과 인도의 급속히 확장되는 수출 허브가 주도하고 있어, 이 지역이 10년 말까지 신규 인플레이터 장치의 거의 절반을 차지할 수 있음을 시사합니다.

세계의 자동차용 에어백 인플레이터 시장 동향 및 인사이트

충돌안전규제 강화

전면, 측면 충돌 및 보행자 보호 규정이 강화되면서 자동차 제조사들은 고성능 안전 장치 시스템을 채택해야 하며, 이는 자동차용 에어백 인플레이터 시장을 확대시키고 있습니다. 북미 FMVSS(연방자동차안전기준) 개정과 유럽의 일반 안전 규정(GSR)은 측면-몸통 및 커튼 솔루션의 기본 장착 기준을 높였습니다. OEM(원조제조사)들은 이제 규정 준수 문서를 갖춘 인플레이터를 입찰하며, 이는 설계 기간을 단축시키고 수직 통합 공급업체를 선호하게 만듭니다. 감사 빈도 증가로 최종 조립 라인 인근에 현장 추진제 테스트 셀이 설치되어 인증 주기가 최대 4주 단축되었습니다. 교체량 증가는 비용 전가를 부분적으로 상쇄하여 인플레이터 수요를 전반적으로 견인하고 있습니다. 규제 기관들은 가스 배출량 지표와 함께 사이버 보안 준비 상태를 참조하기 시작하여 업계가 스마트 인플레이터 모듈로 전환하도록 유도하고 있습니다.

ADAS 주도 다단계 인플레이터 채택

중국 브랜드의 센서 집약형 중형 SUV는 충돌 심각도 데이터를 인플레이터 로직과 융합해 더 넓은 승객 범위를 보호하는 맞춤형 가스 방출을 구현합니다. 5성급 신차평가프로그램(NCAP) 점수는 전시실 매력을 뒷받침하며, 다단계 인플레이터를 ADAS 가치의 가시적 증거로 부각시킵니다. 다단계 인플레이터 도입이 뒤처진 자동차 제조사들은 전시실 비교에서 불리한 평가를 받을 위험이 있어 후발주자 압박이 가속화됩니다. 소프트웨어 업데이트를 통한 향후 보정 조정이 가능해 OEM의 재공구 비용 부담을 줄여줍니다. 부품 공급업체들은 이 추세를 활용해 펌웨어 유지보수 계약을 추가 판매함으로써 연금형 수익 구조를 확보합니다. 따라서 센서 융합과 인플레이터 제어 기술의 융합은 자동차용 에어백 인플레이터 시장에서 프리미엄 가격대를 유지하는 요인으로 작용합니다.

헬륨 공급 부족

지정학적 혼란으로 산업용 헬륨 현물 가격이 급등하면서 저장 가스 인플레이터의 부품 비용이 증가하고 마진이 압박받고 있습니다. 탄자니아에서 진행 중인 탐사 캠페인은 친환경 헬륨을 목표로 하며, 초기 유량 데이터는 안전 시스템 제조사에 상업적 공급이 가능함을 시사합니다. OEM들은 화약 가스로 헬륨 사용량을 희석하는 하이브리드 인플레이터로 조달을 전환하며 대응 중입니다. 계약 조항에는 이제 헬륨 가격 조정 공식이 포함되어 위험의 일부를 공급업체로 이전하고 있습니다. 일시적이지만, 비용 급등은 이미 새로운 저장 가스 설계 반복을 늦추고 있어 자동차용 에어백 인플레이터 시장의 해당 하위 부문의 단기 성장을 완화시키고 있습니다.

부문 분석

커튼 에어백은 자동차용 에어백 인플레이터 시장 점유율의 34.10%를 차지합니다. 이들의 우위는 강력한 측면 충돌 보호를 의무화하는 별점 등급 프로토콜에 기반합니다. 최근 업데이트된 모델에서는 좁은 루프 레일에서 충전 균일성을 높이는 분할 가스 채널에 대한 관심이 드러납니다. 신흥 전기차의 기가 캐스트 프레임은 더 얇은 레일을 생성하므로, 타원형 실린더는 루프 높이 제약 없이 가스 용량을 유지합니다. 자동차용 에어백 인플레이터 시장은 형태 혁신과 신뢰성 있는 화학 기술을 결합한 플랫폼에 지속적으로 보상을 주고 있습니다.

무릎 에어백은 8.60%의 가장 빠른 연평균 성장률(CAGR) 전망을 기록 중입니다. 하체 부상 평가 비중이 높아진 충돌 테스트 더미와 보험 점수 모델이 도입을 촉진하고 있습니다. 공급업체들은 기존 대시보드 하부 빔에 클립으로 고정되는 일체형 하우징을 제공하여 라인사이드 조립 시간을 단축하고 있습니다. 차량 구매처들은 무릎 보호 장치가 있을 때 근로자 보상 청구 건수가 감소한다고 강조하며, 이는 사양 채택률을 높이는 요인입니다. 이러한 성장 동력은 자동차용 에어백 인플레이터 산업의 장기적 다양성을 강화하며, 단일 주류 카테고리보다 다중 성장 벡터의 혜택을 누리게 합니다.

2024년 화약식 인플레이터 매출은 32억 8,000만 달러로, 자동차용 에어백 인플레이터 시장 규모의 59.25%를 차지했습니다. 컴팩트한 형태, 입증된 신뢰성, 헬륨 공급 변동에 대한 내성으로 인해 운전석 에어백의 기본 선택으로 자리매김하고 있습니다. 비아지드 화합물은 금속 벽 두께를 얇게 만들어 무게를 절감하고 차량 평균 배출 목표 달성을 지원합니다. 공장 데이터에 따르면 구아니딘-질산염 혼합물이 기존 혼합물을 대체할 경우 전개 후 미립자 배출량이 감소하여 클린룸 유지보수가 용이해집니다.

하이브리드 인플레이터는 연평균 7.90% 성장률이 예상됩니다. 소형 저장 가스 챔버와 화약식 주 충전부를 결합한 설계로 헬륨 사용량을 줄이면서도 조절 범위를 유지합니다. OEM 업체들은 하이브리드 어셈블리를 조달 헤지 수단으로 간주하며, 이중 화학 라인으로 공급망 충격을 완화할 수 있다고 지적합니다. 개발 로드맵은 이중 단계 커튼 에어백 및 반대측 에어백에서의 광범위한 적용을 시사합니다. 따라서 자동차용 에어백 인플레이터 업계는 하이브리드 생산 능력을 향후 원자재 가격 변동에 대비한 보험 정책으로 간주합니다.

지역 분석

북미는 2024년 글로벌 매출의 약 31.10%를 차지했습니다. 미국 고속도로 교통 안전청(NHTSA)의 특정 인플레이터 변종에 대한 조사는 법적 위험에 초점을 맞춰 OEM이 검증된 설계와 추적 가능한 제조 기록을 선호하도록 유도하고 있습니다. UN-R155 규정을 준수하는 사이버 보안 인플레이터 모듈이 주목받으며 지역 공급망에 소프트웨어 검증 계층이 추가되고 있습니다. 높은 시장 성숙도는 경쟁을 충돌 데이터 분석과 같은 라이프사이클 서비스로 전환시켜 하드웨어 가격 책정에서 부가가치 지원으로 중점을 이동시키고 있습니다.

아시아태평양 지역은 중국, 인도, 아세안 경제권의 견인으로 7.50%의 가장 높은 연평균 성장률(CAGR)을 기록 중입니다. 중국산 중형 SUV 플랫폼에 적용된 2단계 인플레이터는 현지 혁신이 글로벌 기준을 충족하는 사례를 보여주며, 5성급 안전 등급 획득으로 수출 경쟁력이 강화되었습니다. 인도 제조 허브는 비용 우위와 현지 공급업체 단지를 활용해 타 지역의 생산 능력 공백을 메움으로써 자동차 에어백 인플레이터 시장 점유율을 확대하고 있습니다. 첸나이 및 푸네 인근에 추진제 연구소와 시험 장비를 공동 배치한 공급업체들은 물류 리스크를 줄이고 인증 주기를 단축합니다.

유럽은 규정 준수에 중점을 둔 꾸준한 수요를 보입니다. 비아지드 화학으로의 거의 완전한 전환은 개조 프로그램을 통해 애프터마켓 물량을 안정적으로 유지합니다. 탄소 중립 약속은 인플레이터 케이싱에 알루미늄 재활용재 채택을 촉진하여 소재 선택을 기업의 지속가능성 목표와 일치시킵니다. 보행자 안전 요건은 외부 에어백 연구를 촉진하며, 이는 인플레이터 대상 시장을 점진적으로 확대할 수 있습니다. 탄소 국경세는 단가만큼 조달에 영향을 미쳐 가공 공정의 동유럽 이전을 점진적으로 촉진하고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

목차

제1장 서론

- 조사의 전제조건과 시장의 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 성장 촉진요인

- 아지드 추진제 단계적 폐지로 인한 EU 및 일본 개조 수요 증가

- ADAS 주도형 중국 중형 SUV의 다단계 인플레이터 채택

- 인도 수출 허브 부상으로 인한 인플레이터 수요 증가

- 전기차 기가 캐스팅 섀시, 초슬림 커튼 인플레이터 수요 창출

- UN-R155 사이버 보안 규정 준수, 북미 스마트 인플레이터 모듈 수요 증대

- L4/L5 자율주행차 도입, 고급 다방향 인플레이터 어레이 수요 증가

- 시장 성장 억제요인

- 저장 가스 인플레이터 가격 상승을 부추기는 헬륨 공급 부족

- 아시아산 인플레이터 수입 비용 증가를 초래하는 EU 탄소 국경세

- 중동 및 아프리카 지역에서 OEM 프로그램 약화를 초래하는 위조 인플레이터 확산

- 전기차 에어백 시스템 통합 지연을 초래하는 리튬이온 배터리 화재 위험

- 가치/공급망 분석

- 규제 또는 기술 전망

- Porter's Five Forces

- 신규 참가업체의 위협

- 구매자의 협상력/소비자

- 공급기업의 협상력

- 대체품의 위협

- 경쟁 기업간 경쟁 관계

제5장 시장 규모와 성장 예측(가치 및 양)

- 에어백 유형별

- 승객용

- 커튼

- 무릎

- 측면

- 보행자 보호

- 인플레이터 유형별

- 화약식

- 저장 가스

- 하이브리드

- 차량 유형별

- 승용차

- 소형 상용차

- 대형 상용차

- 추진제 화학 성분별

- 아지드 기반

- 비아지드

- 기술 단계별

- 단일 단계

- 이중 단계 및 다중 단계

- 판매 채널별

- OEM 장착

- 애프터마켓/리콜 교환

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 기타 북미

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 유럽

- 독일

- 영국

- 프랑스

- 북유럽 국가

- 기타 유럽

- 아시아태평양

- 중국

- 일본

- 인도

- 한국

- 기타 아시아태평양

- 중동

- 걸프 협력 회의

- 기타 중동

- 아프리카

- 남아프리카

- 나이지리아

- 기타 아프리카

- 북미

제6장 경쟁 구도

- 시장 집중도

- 전략적 동향

- 시장 점유율 분석

- 기업 프로파일

- Autoliv Inc.

- ZF Friedrichshafen AG

- Joyson Safety Systems(Key SS)

- Daicel Corporation

- Nippon Kayaku Co.

- ARC Automotive Inc.

- Toyoda Gosei Co.

- 현대모비스 Co.

- Continental AG

- Denso Corporation

- Yanfeng Safety Systems

- Nihon Plast Co.

- Ashimori Industry Co.

- Takata(Residual Recall Operations)

- Kolon Industries Inc.

- GWR Safety Systems

- ARC China Ltd.

- Tenaris Inflators

- Jinzhou Jinheng Automotive

제7장 시장 기회와 장래의 전망

HBR 25.11.10The automotive airbag inflator market size stands at USD 5.93 billion in 2025 and is forecast to touch USD 8.17 billion by 2030, advancing at a 6.60% CAGR between 2025 and 2030.

Stronger crash-safety legislation, heightened consumer attention to occupant protection, and continuous inflator chemistry and packaging gains underpin the automotive airbag inflator market climb. Suppliers that control design-to-manufacture workflows secure higher margins because they answer new regulatory tests faster than firms that rely on contract assemblers. Regulators in North America and Europe have signalled upcoming side-impact and cybersecurity audits, which will raise costs and lift replacement volumes, sustaining the automotive airbag inflator market even during flat vehicle-production cycles. The Asia-Pacific region already shows a 7.50% CAGR, led by technology-rich Chinese mid-SUV programs and India's fast-scaling export hubs, suggesting the region could represent nearly half of new inflator units by the decade's close

Global Automotive Airbag Inflator Market Trends and Insights

Stricter Crash-Safety Mandates

Upgraded frontal, side-impact, and pedestrian-protection protocols push automakers to adopt higher-performance restraint systems, expanding the automotive airbag inflator market. North American FMVSS updates and Europe's General Safety Regulation lift baseline fitment for side-torso and curtain solutions. OEMs now tender inflators with compliance documentation, compressing design windows, and favouring vertically integrated suppliers. Increased audit frequency has prompted on-site propellant test cells near final assembly lines, shortening certification loops by up to four weeks. Higher replacement volumes partially offset cost pass-through, keeping overall inflator demand buoyant. Regulators have begun referencing cybersecurity readiness alongside gas-output metrics, nudging the industry toward smart inflator modules.

ADAS-Led Adoption of Multi-Stage Inflators

Sensor-rich mid-SUVs manufactured by Chinese brands fuse crash-severity data with inflator logic, allowing tailored gas releases that protect a wider occupant range. Five-star New Car Assessment Program scores support showroom appeal and showcase multi-stage inflators as visible proof of ADAS value. Automakers that lag in multi-stage deployment risk negative showroom comparisons, creating fast-follower pressure. Software updates allow future calibration tweaks, shielding OEMs from retooling costs. Component suppliers leverage the trend to upsell firmware maintenance contracts, adding an annuity-style revenue layer. Therefore, the convergence of sensor fusion and inflator modulation sustains premium price points within the automotive airbag inflator market.

Helium Supply Crunch

Geopolitical disruptions lifted industrial-grade helium spot prices, inflating the bill of materials for stored-gas inflators and squeezing margins. Exploration campaigns in Tanzania seek green helium, with preliminary flow-rate data suggesting a viable commercial supply for safety-system producers. OEMs react by shifting procurements toward hybrid inflators that dilute helium use with pyrotechnic gas. Contract clauses now include helium-price adjustment formulas, transferring part of the risk back to suppliers. While temporary, cost spikes have already slowed new stored-gas design iterations, moderating near-term growth for that sub-segment of the automotive airbag inflator market.

Other drivers and restraints analyzed in the detailed report include:

- Phase-Out of Azide Propellants

- Emergence of Indian Export Hubs

- EU Carbon Border Tariff

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Curtain airbags representing 34.10% of the automotive airbag inflator market share. Their dominance rests on star-rating protocols that mandate robust side-impact protection. Recent refreshes reveal interest in segmented gas channels that enhance fill uniformity along narrow roof rails. Emerging giga-cast EV frames create slimmer rails, so oval-section cylinders preserve gas volume without raising roof-height constraints. The automotive airbag inflator market continues to reward platforms that mix shape innovation with reliable chemistry.

Knee airbags register the fastest 8.60% CAGR outlook. Crash dummies that weigh more on lower-leg injuries and insurance scoring models reinforce uptake. Suppliers now offer one-piece housings that clip into existing under-dash beams, trimming line-side assembly minutes. Fleet buyers highlight lower worker-compensation claims when knee protection is present, boosting specification rates. Growing traction strengthens the long-term diversity of the automotive airbag inflator industry, which benefits from multiple growth vectors rather than a single dominant category.

Pyrotechnic inflators earned USD 3.28 billion in revenue during 2024, equal to 59.25% of the automotive airbag inflator market size. Their compact form, proven reliability, and immunity to helium supply swings keep them the default for driver airbags. Non-azide compounds let engineers thin metal walls, saving grams and supporting fleet-average emissions objectives. Plant data show particulate emissions after deployment drop when guanidine-nitrate blends replace legacy mixes, easing clean-room maintenance.

Hybrid inflators are forecast for a 7.90% CAGR. Their design marries a small stored-gas chamber with a pyrotechnic main charge, cutting helium volumes while retaining modulation latitude. OEMs view hybrid assemblies as procurement hedges, noting that dual-chemistry lines dampen supply-chain shocks. Development road maps point to wider use in dual-stage curtain and far-side airbags. The automotive airbag inflator industry, therefore, treats hybrid capacity as an insurance policy against future commodity swings.

The Automotive Airbag Inflator Market Report is Segmented by Airbag Type (Driver, Passenger, and More), Inflator Type (Pyrotechnic, Stored Gas, Hybrid), Vehicle Type (Passenger Cars, LCV, and More), Propellent Chemistry (Azide-Based, Non-Azide), Technology Stage ( Single Stage and Multi-Stage), Sales Channel (OEM Fitted and Aftermarket) and Geography. The Market Forecasts are Provided in Terms of Value (USD) and Volume (Units).

Geography Analysis

North America contributed nearly 31.10% of global revenue in 2024. The National Highway Traffic Safety Administration's probe into specific inflator variants focuses on legal exposure, motivating OEMs to favour proven designs and traceable manufacturing records. Cyber-secure inflator modules that comply with UN-R155 have gained traction, adding software validation layers to the regional supply chain. High market maturity channels competition toward lifecycle services such as crash-data analytics, shifting emphasis from hardware pricing to value-added support.

Asia-Pacific records the strongest 7.50% CAGR, driven by China, India, and ASEAN economies. Chinese mid-SUV platforms with dual-stage inflators demonstrate how local innovations meet global benchmarks, and five-star safety ratings raise export appeal. Indian manufacturing hubs leverage cost advantages and local supplier parks to backfill capacity gaps elsewhere, thereby capturing a larger slice of the automotive airbag inflator market. Suppliers that co-locate propellant labs and test rigs near Chennai and Pune compress logistics risk and win shorter certification cycles.

Europe shows steady, compliance-centred demand. The region's near-complete shift to non-azide chemistry keeps aftermarket volumes healthy through retrofit programs. Carbon-neutrality pledges drive aluminium recyclate adoption for inflator casings, aligning material choices with corporate sustainability goals. Pedestrian safety requirements encourage research into external airbags, which could incrementally widen the inflator addressable market.Carbon border tariffs influence sourcing as much as unit price, prompting a gradual relocation of machining steps to Eastern Europe.

- Autoliv Inc.

- ZF Friedrichshafen AG

- Joyson Safety Systems (Key SS)

- Daicel Corporation

- Nippon Kayaku Co.

- ARC Automotive Inc.

- Toyoda Gosei Co.

- Hyundai Mobis Co.

- Continental AG

- Denso Corporation

- Yanfeng Safety Systems

- Nihon Plast Co.

- Ashimori Industry Co.

- Takata (Residual Recall Operations)

- Kolon Industries Inc.

- GWR Safety Systems

- ARC China Ltd.

- Tenaris Inflators

- Jinzhou Jinheng Automotive

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Drivers

- 4.1.1 Phase-out of Azide Propellants Driving EU & Japan Retrofit Demand

- 4.1.2 ADAS-Led Adoption of Multi-Stage Inflators in Chinese Mid-SUVs

- 4.1.3 Emergence of Indian Export Hubs Elevating Captive Inflator Off-take

- 4.1.4 EV Giga-Casting Chassis Creating Need for Ultra-Slim Curtain Inflators

- 4.1.5 UN-R155 Cyber-Security Compliance Boosting Smart Inflator Modules in NA

- 4.1.6 L4/L5 Autonomous Vehicle Rollout Demanding Advanced Multi-Directional Inflator Arrays

- 4.2 Market Restraints

- 4.2.1 Helium Supply Crunch Inflating Stored-Gas Inflator Pricing

- 4.2.2 EU Carbon Border Tariff Raising Cost of Asian Inflator Imports

- 4.2.3 Proliferation of Counterfeit Inflators in MEA Eroding OEM Programs

- 4.2.4 Lithium-ion Battery Fire Risks Delaying EV Airbag System Integration

- 4.3 Value / Supply-Chain Analysis

- 4.4 Regulatory or Technological Outlook

- 4.5 Porter's Five Forces

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Buyers/Consumers

- 4.5.3 Bargaining Power of Suppliers

- 4.5.4 Threat of Substitute Products

- 4.5.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value & Volume)

- 5.1 By Airbag Type

- 5.1.1 Passenger

- 5.1.2 Curtain

- 5.1.3 Knee

- 5.1.4 Side

- 5.1.5 Pedestrian Protection

- 5.2 By Inflator Type

- 5.2.1 Pyrotechnic

- 5.2.2 Stored-Gas

- 5.2.3 Hybrid

- 5.3 By Vehicle Type

- 5.3.1 Passenger Cars

- 5.3.2 Light Commercial Vehicles

- 5.3.3 Heavy Commercial Vehicles

- 5.4 By Propellant Chemistry

- 5.4.1 Azide-Based

- 5.4.2 Non-Azide (e.g., Guanidine Nitrate)

- 5.5 By Technology Stage

- 5.5.1 Single-Stage

- 5.5.2 Dual-Stage & Multi-Stage

- 5.6 By Sales Channel

- 5.6.1 OEM Fitted

- 5.6.2 Aftermarket / Recall Replacement

- 5.7 By Geography

- 5.7.1 North America

- 5.7.1.1 United States

- 5.7.1.2 Canada

- 5.7.1.3 Mexico

- 5.7.1.4 Rest of North America

- 5.7.2 South America

- 5.7.2.1 Brazil

- 5.7.2.2 Argentina

- 5.7.2.3 Rest of South America

- 5.7.3 Europe

- 5.7.3.1 Germany

- 5.7.3.2 United Kingdom

- 5.7.3.3 France

- 5.7.3.4 Nordics

- 5.7.3.5 Rest of Europe

- 5.7.4 Asia-Pacific

- 5.7.4.1 China

- 5.7.4.2 Japan

- 5.7.4.3 India

- 5.7.4.4 South Korea

- 5.7.4.5 Rest of Asia-Pacific

- 5.7.5 Middle East

- 5.7.5.1 Gulf Cooperation Council

- 5.7.5.2 Rest of Middle East

- 5.7.6 Africa

- 5.7.6.1 South Africa

- 5.7.6.2 Nigeria

- 5.7.6.3 Rest of Africa

- 5.7.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)}

- 6.4.1 Autoliv Inc.

- 6.4.2 ZF Friedrichshafen AG

- 6.4.3 Joyson Safety Systems (Key SS)

- 6.4.4 Daicel Corporation

- 6.4.5 Nippon Kayaku Co.

- 6.4.6 ARC Automotive Inc.

- 6.4.7 Toyoda Gosei Co.

- 6.4.8 Hyundai Mobis Co.

- 6.4.9 Continental AG

- 6.4.10 Denso Corporation

- 6.4.11 Yanfeng Safety Systems

- 6.4.12 Nihon Plast Co.

- 6.4.13 Ashimori Industry Co.

- 6.4.14 Takata (Residual Recall Operations)

- 6.4.15 Kolon Industries Inc.

- 6.4.16 GWR Safety Systems

- 6.4.17 ARC China Ltd.

- 6.4.18 Tenaris Inflators

- 6.4.19 Jinzhou Jinheng Automotive