|

시장보고서

상품코드

1849918

모듈식 UPS : 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Modular UPS - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

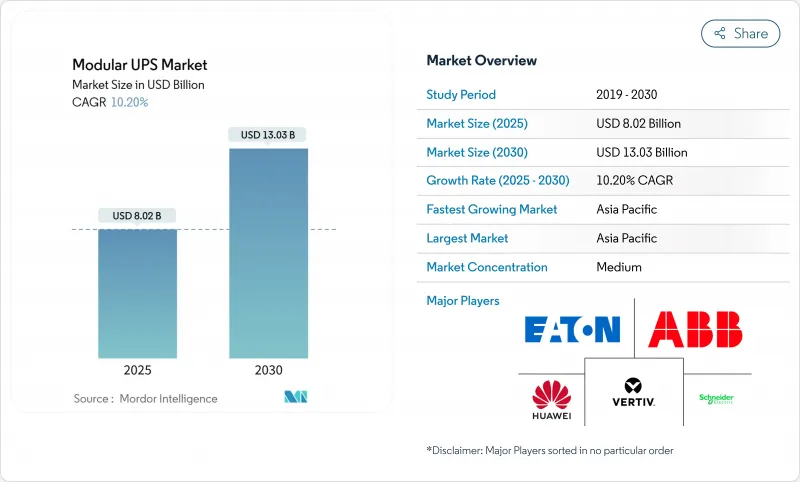

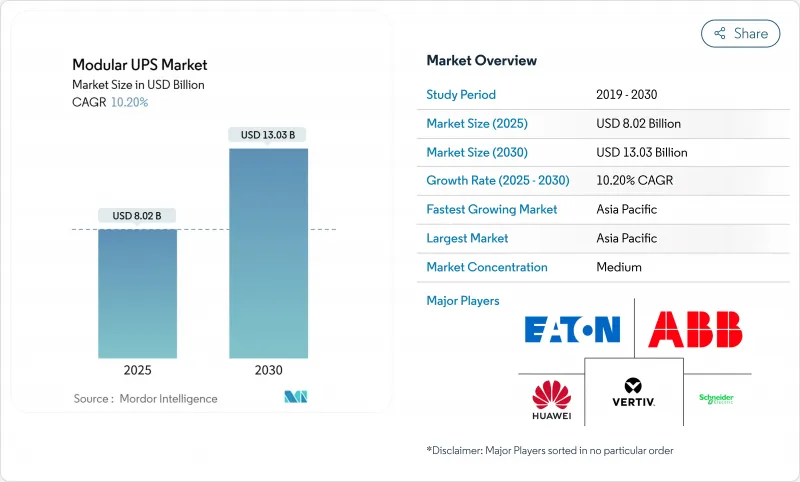

모듈식 UPS 시장 규모는 2025년에 80억 2,000만 달러로 평가되었고, 2030년에는 130억 3,000만 달러에 이를 것으로 추정, 예측되며 예측 기간(2025-2030년)의 CAGR은 10.20%를 나타낼 전망입니다.

데이터센터의 신속한 건설, 엣지 컴퓨팅 도입 확대, 엄격한 가동 시간 요구사항이 수요를 주도하는 가운데, 리튬이온 배터리와 그리드 연동 설계는 시스템 기능을 비상 전원 공급을 넘어 확장합니다. 50kW 단위의 확장성은 유휴 용량을 줄이고 구축 속도를 높여, AI 워크로드가 랙 밀도를 높이는 상황에서 결정적인 이점을 제공합니다. 규제 당국이 2024년 20,000개 이상의 취약한 UPS 모니터링 장치를 지적한 이후, 공급업체들은 사이버 보안 강화로 차별화를 꾀하고 있습니다. 아시아태평양 지역은 최대 시장 점유율을 차지하며 가장 빠르게 성장하고 있으며, 중국, 인도, 일본이 기록적인 속도로 멀티메가와트 캠퍼스를 가동 중입니다.

세계의 모듈식 UPS 시장 동향 및 인사이트

하이퍼스케일, 코로케이션, 클라우드 데이터센터 성장

하이퍼스케일 운영사들은 2024년 글로벌 용량을 5,000MW 추가할 계획이며, 이는 단계별 건설 일정에 부합하는 확장 가능한 전력 블록에 대한 전례 없는 수요를 촉진합니다. AI 훈련 클러스터는 랙 전력 소비량을 10kW에서 40kW로 끌어올려, 설계자들이 단일형 개조 방식의 12-18개월 주기가 아닌 몇 주 만에 확장 가능한 모듈형 스트링을 배치하도록 강제하고 있습니다. 이튼(Eaton)과 지멘스 에너지(Siemens Energy)의 협력은 이러한 시급성을 강조합니다. 양사가 공동 개발한 표준화된 500MW 현장 솔루션은 데이터센터 건설 기간을 2년 단축한다고 주장하며, 소유주들이 이제 전력 아키텍처를 경쟁 우위 요소로 보는 이유를 부각시킵니다. 조달 팀은 사전 제작된 전기 스키드 내부에 장착되어 허가 및 시운전을 간소화하는 모듈식 UPS 시장 제품을 더욱 선호합니다. 이러한 요인들이 합쳐져 2030년까지 전체 연평균 복합 성장률(CAGR)에 약 3.2% 포인트를 추가할 것으로 추정됩니다.

모듈형 아키텍처의 TCO 감소 및 확장성

라이프사이클 연구에 따르면 적정 규모 설계는 유휴 용량을 30-40% 절감하여 모놀리식 프레임 대비 15-25%의 가격 프리미엄을 상쇄합니다. 핫스왑 가능 모듈은 평균 수리 시간(MTTR)을 시간 단위에서 분 단위로 단축시켜 서비스 수준 계약(SLA) 준수를 개선하고 코로케이션 제산업체의 위약금을 낮춥니다. 재무 책임자들은 활용도가 입증될 때까지 자본 지출을 연기하는 '사용량 기반 확장 모델'을 선호합니다. 이는 고금리 환경에서 중요한 헤지 수단입니다. 모듈식 UPS 시장은 자본 지출을 운영 지출로 전환하는 공급업체 금융 운영 리스 채택 증가로도 혜택을 보며 예산 승인을 용이하게 합니다. 종합적으로 점진적 확장성은 예측 성장률에 2.4% 포인트를 기여합니다.

동남아시아 및 라틴아메리카의 가격 민감 구매자들은 여전히 킬로와트당 구매 비용이 15-25% 저렴한 모놀리식 캐비닛을 선호합니다. 수명 주기 분석이 유리함을 입증했음에도 최저 입찰가를 우선시하는 조달 정책으로 인해 도입이 계속 지연되고 있습니다. 공급업체들은 클라우드 과금 방식을 모방한 구독 모델로 모듈 추가가 가능한 사용량 기반 금융으로 대응하고 있습니다. 그럼에도 프리미엄은 여전히 상당한 걸림돌로 작용하여 단기적으로 모듈식 UPS 시장 확장에서 1.2% 포인트를 깎아내리고 있습니다.

부문 분석

51-100kVA 제품군이 2024년 매출의 41%를 차지했음에도, 500kVA 초과 등급이 14% CAGR로 가장 빠른 성장률을 기록했습니다. 이 상위 등급은 각각 40kW를 소비하는 AI 랙을 지원하며, 현재 코로케이션 제산업체들은 유연성 유지를 위해 핫플러그 브릭으로 구성된 2MW 전원실을 표준화하고 있습니다. 이 부문의 모듈식 UPS 시장 규모는 2030년까지 37억 달러에 달할 전망입니다. 운영사들은 모듈 레벨 중복성과 리튬이온 호환성을 주요 선정 기준으로 꼽습니다. 101-500kVA 등급은 비용과 미래 확장성을 균형 있게 고려하는 기업 데이터 센터에 여전히 핵심적입니다. 50kVA 이하 틈새 시장은 벽면 설치 공간이 중요한 통신 쉘터 및 스마트 공장 라인을 대상으로 합니다.

광대역 갭 반도체의 발전으로 변환 효율이 98% 이상으로 향상되어 냉각 설비를 과도하게 확대하지 않고도 열 밀도를 높일 수 있게 되었습니다. Phoenix Contact의 QUINT HP는 UPS IQ 펌웨어로 모니터링되는 5개의 핫스왑 가능 배터리 스트링을 탑재하며, 잔여 수명을 3% 정확도로 예측합니다. 2030년까지 301-500kVA 등급 출하량은 101-300kVA 등급을 추월할 전망입니다. 지역 엣지-코어 시설이 10MW 규모 캠퍼스로 집약되면서 균형 잡힌 수요 곡선이 주기적 지출 감소에도 모듈식 UPS 시장의 회복탄력성을 뒷받침합니다.

2024년 지출의 48%를 차지한 데이터센터는 하이퍼스케일 및 코로케이션 확장을 반영합니다. 산업 플랜트는 인더스트리 4.0 투자가 로봇 생산라인과 웨이퍼 팹에 전력 품질 보증을 적용함에 따라 연평균 12.5% 성장률을 기록합니다. 제조업 내 모듈식 UPS 시장 점유율은 2024년부터 2025년 사이 210bp 상승했습니다. 1밀리초 미만의 무정전 요구사항이 적용되는 반도체 팹은 20분 자율운용이 가능한 중복 N+2 스트링을 구매하며, UPS 용량을 수율 보험으로 간주합니다. 5G 밀집화로 수천 개의 마이크로 데이터 허브가 생겨나며 통신 분야가 확장되었고, 각 허브는 10kVA 벽걸이형 모듈을 주문했습니다.

상업용 건물 및 BFSI(금융 및 보험 및 증권) 분야도 디지털 뱅킹 SLA(서비스 수준 계약)가 가동 중단 시 벌금을 부과하는 방식으로 주도되며 뒤따르고 있습니다. 정부 기관은 복원력 의무를 충족하기 위해 마이크로그리드 지원 설계를 요구하며, 이 추세는 2024년 미 국방부 UFC(Unified Facilities Criteria) 지침에 명문화되었습니다. 의료 시설은 빈번한 유지보수 방문이 어려운 감염 관리 구역에서 핫스왑 배터리를 중요하게 여깁니다. 이러한 확대되는 최종 사용자 기반은 모듈식 UPS 시장이 데이터 센터에만 지나치게 의존하는 것을 방지합니다.

모듈식 UPS 시장은 전력 용량(50KVA 미만, 51-100KVA, 101-300KVA 등), 최종 사용자 산업(데이터센터, 산업용 제조업 등), 위상 유형(단상 및 3상), 구성요소(솔루션 및 서비스), 지역별로 구분됩니다. 시장 예측은 금액(달러)으로 제공됩니다.

지역별 분석

아시아태평양 지역은 2024년 매출의 36%를 차지하며 시장을 주도했으며, 2030년까지 11.2%의 연평균 성장률(CAGR)을 유지하며 타 지역을 압도하고 있습니다. 중국은 지역 전력망 건설 중단 조치를 해제한 후 데이터센터 승인 절차를 가속화했으며, 인도의 디지털 공공 인프라 프로그램은 뭄바이, 하이데라바드, 첸나이 주변에 하이퍼스케일 시설 건설을 촉발했습니다. 일본의 반도체 부흥은 바닥 하중을 줄이기 위해 500kVA 이상의 리튬이온 UPS 스트링을 요구하는 신규 팹 건설에 수십억 달러를 투자하고 있습니다. 선전과 쑤저우에서의 전력 전자 부품 현지 생산은 리드 타임을 단축시켜 글로벌 부품 부족 상황에서 결정적인 경쟁 우위를 제공합니다. 결과적으로 아시아태평양 지역의 모듈식 UPS 시장은 2030년까지 50억 달러를 넘어설 전망입니다.

북미는 버지니아 북부, 댈러스, 피닉스의 성숙한 하이퍼스케일 캠퍼스를 바탕으로 2위를 차지합니다. PJM 및 ERCOT 전역의 전력사는 주파수 조절 서비스를 적극적으로 조달하며, 유휴 배터리 자산을 수익화하는 그리드 연계형 설치를 장려하고 있습니다. 국방부는 임무 핵심 기지에 마이크로그리드 호환 UPS를 의무화하여 블랙스타트 기능이 가능한 내구성 강화 NEMA 인클로저 수요를 높이고 있습니다. 캐나다의 제안된 2단계 에너지 효율 기준은 변압기 없는 고효율 설계 채택을 더욱 촉진합니다.

유럽도 탄소중립 목표와 상승하는 전력 비용으로 99% 효율의 에코 모드 투자수익률(ROI)이 높아지면서 뒤따르고 있습니다. 영국은 지속가능성 평가를 강화하고, 독일의 BaFin은 금융 서비스 제산업체를 위한 데이터센터 복원력을 규제합니다. 양국 운영사들은 IT 부하에 맞춰 모듈을 가동하거나 중단하는 동적 용량 최적화 방식을 도입해 연간 에너지 낭비를 줄이고 있습니다. 프랑스와 북유럽은 재생에너지 공급을 바탕으로 콜로케이션 시장이 급성장하며, 2026년까지 EU로 수출될 예정인 노스캐롤라이나의 네이트론 에너지(Natron Energy) 기가팩토리와 같은 리튬이온 및 나트륨이온 배터리 시범 사업의 발판을 마련하고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

목차

제1장 서론

- 조사의 전제조건과 시장의 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 하이퍼스케일, 코로케이션, 클라우드 데이터센터의 성장

- 모듈형 아키텍처의 TCO 감소 및 확장성

- 엣지 및 5G 마이크로 데이터센터의 신속한 전개

- 고효율 UPS를 촉진하는 친환경 인증 의무화

- 부가 수익원을 위한 그리드 연동형 UPS

- 중요한 인프라용 마이크로그리드 대응 설계

- 시장 성장 억제요인

- 모놀리식 시스템 대비 높은 초기 자본 지출

- IT 분야 외부의 제한된 인식

- 전력 전자 부품 공급망 변동성

- 네트워크형 UPS의 사이버 보안 위험

- 업계 밸류체인 분석

- 규제 상황

- 기술의 전망

- 업계의 매력 - Porter's Five Forces 분석

- 공급기업의 협상력

- 구매자의 협상력/소비자

- 신규 참가업체의 위협

- 대체품의 위협

- 경쟁 기업간 경쟁 관계

- 거시 경제 요인이 시장에 미치는 영향

제5장 시장 규모와 성장 예측

- 전력 용량별

- 50kVA 이하

- 51-100kVA

- 101-300kVA

- 301-500kVA

- 500kVA 초과

- 최종 사용자 업계별

- 데이터 센터

- 산업제조업

- 통신

- 상업 빌딩

- BFSI

- 정부 및 공공 인프라

- 헬스케어

- 기타 최종 사용자 업계

- 위상 유형별

- 단상

- 3상

- 컴포넌트별

- 솔루션(하드웨어)

- 서비스

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 남미

- 브라질

- 아르헨티나

- 칠레

- 기타 남미

- 유럽

- 영국

- 독일

- 프랑스

- 이탈리아

- 스페인

- 러시아

- 기타 유럽

- 아시아태평양

- 중국

- 일본

- 인도

- 한국

- 호주

- 말레이시아

- 싱가포르

- 기타 아시아태평양

- 중동 및 아프리카

- 중동

- 사우디아라비아

- 아랍에미리트(UAE)

- 튀르키예

- 기타 중동

- 아프리카

- 남아프리카

- 나이지리아

- 기타 아프리카

- 북미

제6장 경쟁 구도

- 시장 집중도

- 전략적 동향

- 시장 점유율 분석

- 기업 프로파일

- Schneider Electric SE

- Vertiv Holdings Co.

- Eaton Corporation plc

- ABB Ltd.

- Huawei Technologies Co. Ltd.

- Delta Electronics Inc.

- Riello UPS(Riello Elettronica)

- AEG Power Solutions

- Socomec Group

- Borri SpA

- Kehua Data Co., Ltd.

- KSTAR Science and Technology

- CyberPower Systems, Inc.

- Tripp Lite(by Eaton)

- Gamatronic(SolarEdge)

- Salicru SA

- Piller Power Systems

- Centiel SA

- Hitec Power Protection

- Statron AG

- PowerShield Ltd.

- Fuji Electric Co., Ltd.

- Mitsubishi Electric Corp.

- Toshiba ESS

- Shenzhen Zhicheng Champion Co., Ltd.

- Zhongheng Electric(China UPS)

제7장 투자 분석

제8장 시장 기회와 장래의 동향

- 화이트 스페이스와 미충족 요구 평가

The Modular UPS Market size is estimated at USD 8.02 billion in 2025, and is expected to reach USD 13.03 billion by 2030, at a CAGR of 10.20% during the forecast period (2025-2030).

Rapid data-center construction, edge-computing rollouts, and stringent uptime requirements keep demand strong, while lithium-ion batteries and grid-interactive designs expand system functionality beyond standby power. Scaling in 50 kW building blocks reduces stranded capacity and speeds deployment, a decisive advantage as AI workloads lift rack densities. Vendors also differentiate through cybersecurity hardening after regulators highlighted more than 20,000 vulnerable UPS monitoring devices in 2024. Asia-Pacific commands the largest regional footprint and grows fastest as China, India, and Japan commission multi-megawatt campuses at a record pace.

Global Modular UPS Market Trends and Insights

Growth of Hyperscale, Colocation and Cloud Data Centers

Hyperscale operators plan to add 5,000 MW of global capacity in 2024, driving unprecedented demand for scalable power blocks that align with phased build schedules. AI training clusters raise rack power draw from 10 kW to 40 kW, compelling designers to deploy modular strings that can be expanded in weeks rather than the 12-18-month cycle of monolithic retrofits. Collaboration between Eaton and Siemens Energy underscores the urgency; their standardized 500 MW onsite solution claims to trim data-center construction time by two years and underscores why owners now view power architecture as a competitive lever. Procurement teams further prefer modular UPS market products because they fit inside prefabricated electrical skids, streamlining permitting and commissioning. Together, these forces add an estimated 3.2 percentage points to the overall CAGR through 2030.

Lower TCO and Scalability of Modular Architecture

Lifecycle studies indicate that right-sizing cuts stranded capacity by 30-40%, offsetting the 15-25% price premium versus monolithic frames. Hot-swappable modules slash mean-time-to-repair from hours to minutes, which improves SLA compliance and lowers penalty payments for colocation providers. CFOs favor the pay-as-you-grow model because it defers capital until utilization proves out, a vital hedge in high-interest environments. The modular UPS market also benefits from rising adoption of vendor-financed operating leases that convert capex to opex, easing budget approvals. Collectively, incremental scalability contributes 2.4 percentage points to forecast growth.

High Up-Front Capex Versus Monolithic Systems

Price-sensitive buyers in Southeast Asia and Latin America still favor monolithic cabinets that cost 15-25% less per kilowatt at acquisition. Even though lifecycle analyses prove favorable, procurement policies prioritized around the lowest bid continue to delay adoption. Vendors respond with usage-based financing, allowing clients to add modules under subscription models that mimic cloud billing. Nonetheless, the premium remains a meaningful drag, subtracting 1.2 percentage points from modular UPS market expansion over the near term.

Other drivers and restraints analyzed in the detailed report include:

- Rapid Deployment for Edge and 5 G Micro-Data Centers

- Green-Certification Mandates Driving High-Efficiency UPS

- Cyber-Security Risks in Networked UPS

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

The >500 kVA class generated the fastest growth at 14% CAGR, despite 51-100 kVA units holding 41% of 2024 revenue. This upper tier addresses AI racks drawing 40 kW each, and colocation providers now standardize on 2 MW power rooms filled with hot-plug bricks to maintain flexibility. The modular UPS market size for this slice will reach USD 3.7 billion by 2030. Operators cite module-level redundancy and lithium-ion compatibility as primary selection criteria. The 101-500 kVA tiers remain vital for corporate data halls that balance cost with future expansion. The <=50 kVA niche serves telecom shelters and smart-factory lines where wall-mount footprints matter.

Advancements in wide-band-gap semiconductors lift conversion efficiency above 98%, allowing heat-density gains without oversizing cooling plants. Phoenix Contact's QUINT HP demonstrates five hot-swappable battery strings monitored by UPS IQ firmware that predicts remaining life to within 3% accuracy. By 2030, shipments in the 301-500 kVA cohort will overtake the 101-300 kVA class as regional edge-core facilities aggregate into 10 MW campuses. This balanced demand curve underpins the modular UPS market's resilience against cyclical spending dips.

Data centers accounted for 48% of 2024 spending, reflecting hyperscale and colocation scale-out. Industrial plants post 12.5% CAGR as Industry 4.0 investments attach power-quality guarantees to robotics lines and wafer fabs. The modular UPS market share within manufacturing rose 210 basis points between 2024 and 2025. Semiconductor fabs, subject to sub-millisecond ride-through requirements, purchase redundant N+2 strings with 20-minute autonomy, treating UPS capacity as yield insurance. Telecom expanded after 5 G densification triggered thousands of micro data hubs, each ordering 10 kVA wall-mount modules.

Commercial buildings and BFSI follow, driven by digital-banking SLAs that penalize downtime. Government adopters specify microgrid-ready designs to meet resiliency mandates, a trend codified in the 2024 DoD UFC guideline. Healthcare facilities value hot-swap batteries for infection-control zones where frequent maintenance visits are impractical. This broadening end-user base shields the modular UPS market from over-reliance on data centers alone.

Modular UPS Market is Segmented by Power Capacity (<= 50 KVA, 51 - 100 KVA, 101 - 300 KVA, and More), End User Industry ( Data Centers, Industrial Manufacturing, and More), Phase Type (Single-Phase and Three-Phase), Component (Solutions and Services), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific led the sector with 36% revenue in 2024, and its 11.2% CAGR through 2030 remains unmatched. China accelerated data-center approvals after lifting regional power-grid moratoriums, while India's Digital Public Infrastructure program triggered hyperscale builds around Mumbai, Hyderabad, and Chennai. Japan's semiconductor revival funnels billions into new fabs that specify lithium-ion UPS strings above 500 kVA to cut floor-loading. Local manufacturing of power electronics in Shenzhen and Suzhou reduces lead times, a decisive edge during global component shortages. As a result, the modular UPS market in Asia-Pacific will eclipse USD 5 billion by 2030.

North America ranks second on the back of mature hyperscale campuses in Northern Virginia, Dallas, and Phoenix. Utilities across PJM and ERCOT actively procure frequency-regulation services, encouraging grid-interactive deployments that monetize idle battery assets. The Department of Defense mandates microgrid-compatible UPS for mission-critical bases, elevating demand for ruggedized NEMA enclosures capable of black-start functionality. Canada's proposed Tier 2 energy-efficiency standard further nudges adoption of transformer-less, high-efficiency designs.

Europe follows, propelled by carbon-neutrality targets and rising electricity costs that sharpen the ROI of 99%-efficient eco-modes. The United Kingdom tightens sustainability assessments, and Germany's BaFin regulates data-center resilience for financial services providers. Operators in both nations incorporate dynamic capacity right-sizing that ramps modules on or off to match IT load, cutting annual energy waste. France and the Nordics see brisk colocation growth backed by renewable-energy availability, setting the stage for lithium-ion and sodium-ion battery pilots such as Natron Energy's planned gigafactory in North Carolina, which will ship into the EU by 2026.

- Schneider Electric SE

- Vertiv Holdings Co.

- Eaton Corporation plc

- ABB Ltd.

- Huawei Technologies Co. Ltd.

- Delta Electronics Inc.

- Riello UPS (Riello Elettronica)

- AEG Power Solutions

- Socomec Group

- Borri S.p.A.

- Kehua Data Co., Ltd.

- KSTAR Science and Technology

- CyberPower Systems, Inc.

- Tripp Lite (by Eaton)

- Gamatronic (SolarEdge)

- Salicru S.A.

- Piller Power Systems

- Centiel SA

- Hitec Power Protection

- Statron AG

- PowerShield Ltd.

- Fuji Electric Co., Ltd.

- Mitsubishi Electric Corp.

- Toshiba ESS

- Shenzhen Zhicheng Champion Co., Ltd.

- Zhongheng Electric (China UPS)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growth of Hyperscale, Colocation and Cloud Data Centers

- 4.2.2 Lower TCO and Scalability of Modular Architecture

- 4.2.3 Rapid Deployment for Edge and 5G Micro-Data Centers

- 4.2.4 Green-Certification Mandates Driving High-Efficiency UPS

- 4.2.5 Grid-Interactive UPS for Ancillary Revenue Streams

- 4.2.6 Microgrid-Ready Designs for Critical Infrastructure

- 4.3 Market Restraints

- 4.3.1 High Up-Front Capex Versus Monolithic Systems

- 4.3.2 Limited Awareness Outside IT Verticals

- 4.3.3 Power-Electronics Supply-Chain Volatility

- 4.3.4 Cyber-Security Risks in Networked UPS

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Industry Attractiveness - Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers/Consumers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitute Products

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Impact of Macroeconomic Factors on the Market

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Power Capacity

- 5.1.1 <= 50 kVA

- 5.1.2 51 - 100 kVA

- 5.1.3 101 - 300 kVA

- 5.1.4 301 - 500 kVA

- 5.1.5 > 500 kVA

- 5.2 By End User Industry

- 5.2.1 Data Centers

- 5.2.2 Industrial Manufacturing

- 5.2.3 Telecommunications

- 5.2.4 Commercial Buildings

- 5.2.5 BFSI

- 5.2.6 Government and Public Infrastructure

- 5.2.7 Healthcare

- 5.2.8 Other End User Industries

- 5.3 By Phase Type

- 5.3.1 Single-Phase

- 5.3.2 Three-Phase

- 5.4 By Component

- 5.4.1 Solutions (Hardware)

- 5.4.2 Services

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Chile

- 5.5.2.4 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 United Kingdom

- 5.5.3.2 Germany

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Russia

- 5.5.3.7 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 India

- 5.5.4.4 South Korea

- 5.5.4.5 Australia

- 5.5.4.6 Malaysia

- 5.5.4.7 Singapore

- 5.5.4.8 Rest of Asia-Pacific

- 5.5.5 Middle East and Africa

- 5.5.5.1 Middle East

- 5.5.5.1.1 Saudi Arabia

- 5.5.5.1.2 United Arab Emirates

- 5.5.5.1.3 Turkey

- 5.5.5.1.4 Rest of Middle East

- 5.5.5.2 Africa

- 5.5.5.2.1 South Africa

- 5.5.5.2.2 Nigeria

- 5.5.5.2.3 Rest of Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Overview, Market Overview, Core Segments, Financials, Strategic Info, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Schneider Electric SE

- 6.4.2 Vertiv Holdings Co.

- 6.4.3 Eaton Corporation plc

- 6.4.4 ABB Ltd.

- 6.4.5 Huawei Technologies Co. Ltd.

- 6.4.6 Delta Electronics Inc.

- 6.4.7 Riello UPS (Riello Elettronica)

- 6.4.8 AEG Power Solutions

- 6.4.9 Socomec Group

- 6.4.10 Borri S.p.A.

- 6.4.11 Kehua Data Co., Ltd.

- 6.4.12 KSTAR Science and Technology

- 6.4.13 CyberPower Systems, Inc.

- 6.4.14 Tripp Lite (by Eaton)

- 6.4.15 Gamatronic (SolarEdge)

- 6.4.16 Salicru S.A.

- 6.4.17 Piller Power Systems

- 6.4.18 Centiel SA

- 6.4.19 Hitec Power Protection

- 6.4.20 Statron AG

- 6.4.21 PowerShield Ltd.

- 6.4.22 Fuji Electric Co., Ltd.

- 6.4.23 Mitsubishi Electric Corp.

- 6.4.24 Toshiba ESS

- 6.4.25 Shenzhen Zhicheng Champion Co., Ltd.

- 6.4.26 Zhongheng Electric (China UPS)

7 INVESTMENT ANALYSIS

8 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 8.1 White-Space and Unmet-Need Assessment