|

시장보고서

상품코드

1849932

혈당 검사 스트립 : 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Blood Glucose Test Strips - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

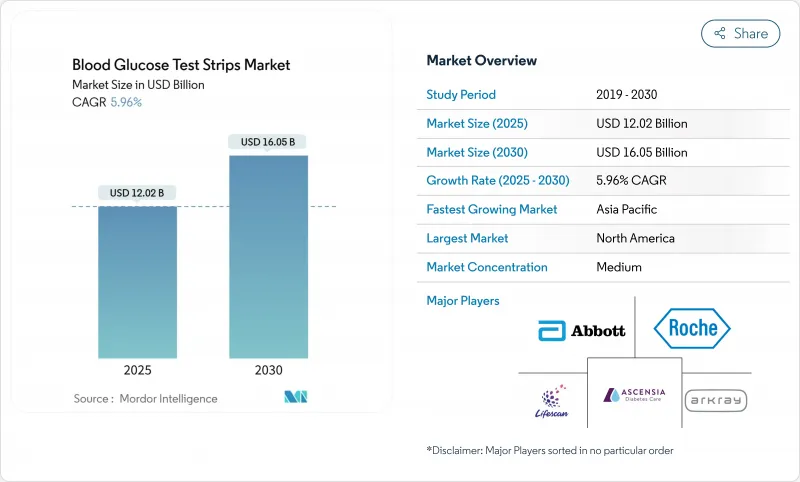

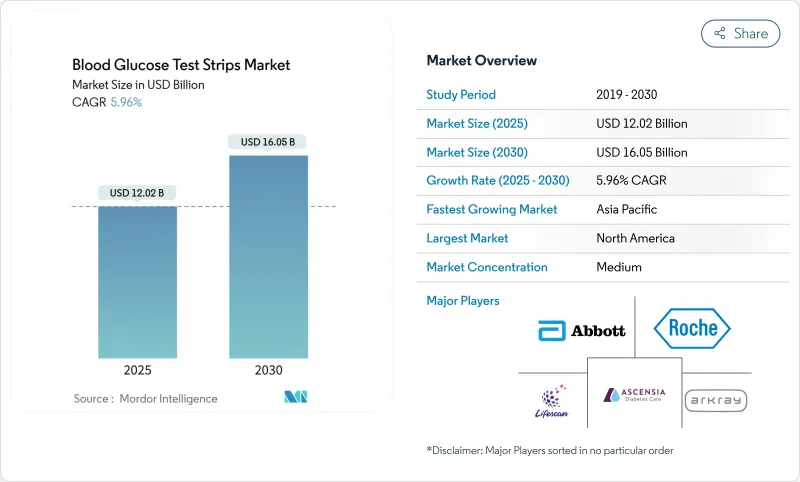

혈당 검사 스트립 시장 규모는 2025년에 120억 2,000만 달러로 평가되었고, 예측 기간(2025-2030년)의 CAGR은 5.96%를 나타낼 것으로 예측되며 2030년에 160억 5,000만 달러에 달할 전망입니다.

성장은 주로 당뇨병 유병률의 지속적인 증가, 확대되는 보험 적용 범위, 그리고 신기술이 등장하는 가운데에도 손가락 채혈 모니터링의 필요성을 유지하는 지속적인 제품 개선에서 비롯됩니다. 기업들은 미국 식품의약국(FDA)의 2024년 강화된 정확도 지침을 충족하기 위해 나노물질 강화 전극에 막대한 투자를 진행 중이며, 이를 통해 검출 한계를 0.01mM까지 낮추면서도 일상 사용자들이 부담 가능한 소매 가격을 유지하고 있습니다. 동시에, 연속 혈당 모니터링(CGM)의 파괴적 매력은 기존 업체들로 하여금 편의성, 정확성 및 다중 채널 접근성을 강화하여 혈당 검사 스트립 시장을 방어하도록 강요하고 있습니다.

세계의 혈당 검사 스트립 시장 동향 및 인사이트

당뇨병 유병률 증가

기록적인 당뇨병 발생률은 혈당 검사 스트립 시장을 근본적으로 재편하고 있습니다. 1억 4,100만 명을 대상으로 한 1,108건의 인구 대표 연구를 통합 분석한 결과, 제2형 당뇨병이 전체 사례의 96%를 차지하며 서태평양 지역 국가들은 2050년까지 유병률이 추가로 17.82% 증가할 수 있는 것으로 나타났습니다. 이러한 역학적 급증은 많은 의료 시스템에서 손가락 채혈 검사가 여전히 가장 접근 가능한 일상 모니터링 도구로 남아 있기 때문에 지속적인 스트립 수요를 촉진합니다. 전 세계 성인 당뇨병 환자 수가 2050년까지 8억 5,250만 명에 달할 것으로 예상되는 가운데, 제조사들은 변화하는 발병 중심지에 대응하기 위해 도시, 도시 근교, 농촌 지역 클리닉 모두에 맞춤형 유통 전략을 수립하고 있습니다.

인식 제고 및 자가 모니터링 확대

임상 증거에 따르면 매일 추가적인 자가혈당측정(SMBG)은 의미 있는 당화혈색소(A1c) 감소를 가져와, 의사들이 더 빈번한 자가검사 일정을 처방하도록 장려합니다. 보건 기관 및 옹호 단체가 지원하는 교육 프로그램은 환자 자신감을 높여 약국 내 검사 스트립 소비량을 증가시킵니다. 미국당뇨병협회(ADA)가 권장하는 개인별 목표 범위는 인슐린 투여량 조절을 위한 일상적 모니터링의 중요성을 더욱 부각시킵니다. 이러한 임상적 권위와 환자 역량 강화라는 두 가지 동력은 디지털 선진국에서도 혈당 검사 스트립 시장의 회복탄력성을 강화합니다.

검사 스트립의 높은 비용

스트립당 0.50-1.00달러의 가격은 적어 보이지만, 하루에 네 번 이상 검사하는 환자, 특히 보험 안전망 밖에서는 비용이 급증합니다. 민간 보험이 드문 개발도상국에서는 많은 사용자가 스트립을 절약하여 혈당 조절이 불충분해지고 의료 지침이 훼손됩니다. 이로 인한 수요 감소는 저소득층 시장에서 혈당 측정 스트립 성장 전망을 축소시키고, 더 저렴한 대체품이나 번들 구독 패키지에 대한 수요를 높입니다.

부문 분석

두꺼운 필름 스트립은 생산 비용이 박막 및 광도계 방식 대비 30-40% 저렴하여 소매 가격 경쟁력을 확보, 검사량 유지를 가능케 함에 따라 2024년 매출의 55.83%를 차지했습니다. 농촌 지역 의료기관과 가격 중심 소비자들이 검증된 저가형 디자인을 선호함에 따라 두꺼운 필름 혈당 측정 스트립 시장 규모는 안정적인 성장세를 보일 전망입니다. 광학/광측정 방식은 규모는 작지만 2030년까지 7.23%의 가장 높은 연평균 성장률(CAGR)을 기록할 전망입니다. 포토다이오드 리더기가 환경 간섭을 줄이고 기술에 익숙한 사용자에게 어필하는 색상 측정 피드백을 제공하기 때문입니다. 제조사들은 현재 초기 도입자를 겨냥한 연결형 스타터 키트에 광측정 카트리지를 포함시켜 CGM(지속적 혈당 모니터링)으로의 완전한 전환을 막으면서도 광범위한 혈당 검사 스트립 시장 내 프리미엄 영역을 창출하고 있습니다.

나노코팅 및 미세유체 채널의 향후 업그레이드는 정확도를 더욱 높일 것이나, 규모의 경제는 아시아와 동유럽 전역에 두꺼운 필름 제조 라인을 계속 유지시킬 것입니다. 공급업체들이 저가 스트립 번들에 블루투스 지원 측정기를 추가함에 따라, 비용 리더십이 디지털 편의성과 수렴하면서 두꺼운 필름에 지속적인 경쟁 우위를 제공할 것입니다. 한편 광학 전문업체와 측정기 OEM 간의 합작 투자는 광도계 기술의 시장 침투를 가속화할 수 있으나, 공급망 복잡성과 높은 단위당 비용으로 인해 예측 기간 동안 혈당 검사 스트립 시장 점유율은 20% 미만에 머무를 전망입니다.

2형 당뇨병 환자가 2024년 스트립 판매량의 86.14%를 차지하며, 사용 편의성, 대량 포장, 검사당 비용을 절감하는 로열티 프로그램으로 연구개발 방향을 이끌고 있습니다. 이 집단은 하루에 한두 번 혈당을 측정하므로 주머니에 들어가는 신뢰할 수 있는 랜싯-스트립 키트가 여전히 설계 우선순위입니다. 반대로 1형 당뇨병 환자는 비율은 작지만 하루 6-10회 측정하며 집중적인 인슐린 요법을 미세 조정하기 위해 실험실 수준의 정밀도를 요구합니다. 소아 및 청년 환자들이 저혈당 추세를 실시간으로 경고하는 앱 연동 측정기를 수용함에 따라 1형 당뇨병용 혈당 측정 스트립 시장 규모는 연간 6.43% 성장하고 있습니다.

제조사들은 제2형 유지 관리를 위한 가치 번들 제품과 제1형 정밀 투약용 프리미엄 나노 강화 스트립으로 구성된 이중 포트폴리오를 제공하여 이러한 시장 분할에 대응하고 있습니다. 프리미엄 마진에 대한 교차 보조금은 개발도상국에서 공격적인 가격 프로모션을 가능케 하여, CGM(지속적 포도당 모니터링)의 시장 침투에도 불구하고 혈당 측정 스트립 시장이 강물처럼 넓은 폭을 유지하도록 보장합니다.

지역 분석

북미는 2024년 글로벌 매출의 35.47%를 차지했으며, 이는 높은 보험 보급률과 노년층의 정기적 모니터링 비용을 보상하는 메디케어 정책에 힘입은 결과입니다. 국가임상치료위원회(NCCC) 연구에 따르면, 보상 체계 조정 후 수혜자 대상 정기 자가 검사가 27% 증가하여, 포괄적인 보험 적용이 스트립의 꾸준한 수요를 뒷받침함을 입증했습니다. 지속적 포도당 모니터링(CGM)에 대한 열의에도 불구하고, 많은 일차 진료 클리닉은 여전히 기본 도구로 손가락 채혈 혈당계를 처방하여 혈당 검사 스트립 시장을 긍정적인 영역에 유지하고 있습니다.

아시아태평양 지역은 성장 동력으로, 중국과 인도가 급증하는 진단 사례와 탄수화물 위주의 식단을 부추기는 도시 생활 방식에 직면하면서 6.86%의 연평균 성장률(CAGR)로 발전하고 있습니다. 인도에서만 당뇨병 성인 환자가 2024년 8,980만 명에서 2050년 1억 5,670만 명으로 증가할 전망이며, 이로 인해 연방 및 주 정부는 필수 모니터링 용품에 대한 보조금을 지급해야 할 것입니다. 시노케어(Sinocare)와 같은 현지 제조업체들은 비용 우위를 바탕으로 2, 3선 도시에 저렴한 키트를 공급하고 있지만, 프리미엄 다국적 기업들은 여전히 도시 병원 계약을 확보하며 지역 내 혈당 검사 스트립 시장의 계층화된 경쟁 구조를 유지하고 있습니다.

유럽은 국가 건강보험이 정기 검사를 지원하고 엄격한 CE 인증 요건을 부과하는 덕분에 상당한 시장 점유율을 유지하고 있습니다. 이러한 규제는 진입 장벽을 높여 공급업체들이 정밀 공학에 투자하도록 유도합니다. 라틴 아메리카와 중동·아프리카 지역은 뒤처져 있지만, 인식 제고 캠페인과 소액보험 프로그램이 자가혈당측정(SMBG) 접근성을 확대함에 따라 매년 성장하고 있습니다. 이 지역의 가격 민감형 소비자들은 두꺼운 필름 방식 키트를 선호하여, 혈당 검사 스트립 시장의 글로벌 영향력을 유지하는 비용 주도 전략을 강화하고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

목차

제1장 서론

- 조사의 전제조건과 시장의 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 당뇨병 유병률 증가

- 인식 제고 및 자가 모니터링 확산

- 기술 발전

- 정부의 대처와 보험 적용 범위

- 온라인 및 소매 유통 채널 성장

- 고령화 인구 및 이에 따른 가정 기반 만성 질환 관리로의 전환

- 시장 성장 억제요인

- 검사 스트립의 고비용

- CGM 시스템의 보급의 급증

- 엄격한 규제 요건

- 증가하는 환경 및 생물학적 위험 폐기물 처리 문제

- 공급망 분석

- 규제 전망

- 기술의 전망

- Porter's Five Forces 분석

- 공급기업의 협상력

- 소비자의 협상력

- 신규 참가업체의 위협

- 대체품의 위협

- 경쟁 기업간 경쟁 관계

제5장 시장 규모와 성장 예측

- 제품 유형별

- 두꺼운 필름 스트립

- 얇은 필름 스트립

- 광학/광측정 스트립

- 당뇨병 유형별

- 1형 당뇨병

- 2형 당뇨병

- 임신과 기타

- 최종 사용자별

- 병원 및 진료소

- 재택 케어 및 개인용

- 진단실험실

- 유통 채널별

- 병원 약국

- 소매 약국

- 온라인 약국

- 지역별

- 북미

- 미국

- 캐나다

- 기타 북미

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 러시아

- 기타 유럽

- 아시아태평양

- 중국

- 일본

- 인도

- 호주

- 한국

- 베트남

- 말레이시아

- 인도네시아

- 태국

- 기타 아시아태평양

- 중동 및 아프리카

- 사우디아라비아

- 이란

- 이집트

- 오만

- 남아프리카

- 기타 중동 및 아프리카

- 라틴아메리카

- 멕시코

- 브라질

- 기타 남미

- 북미

제6장 경쟁 구도

- 시장 집중도

- 시장 점유율 분석

- 기업 프로파일

- Abbott Laboratories

- F. Hoffmann-La Roche Ltd

- LifeScan IP Holdings, LLC.

- Ascensia Diabetes Care Holdings AG.

- ARKRAY Inc.

- AgaMatrix

- Bionime Corporation

- Sinocare Inc.

- Trividia Health Inc.

- Rossmax International Ltd

- Ypsomed AG

- SD Biosensor Inc.

- TaiDoc Technology Corporation

- i-SENS Inc.

- Omron Healthcare Co. Ltd.

- Nova Biomedical

- 77 Elektronika Kft.

- OK Biotech Co. Ltd.

- ACON Laboratories Inc.

- Prodigy Diabetes Care, LLC

제7장 시장 기회와 장래의 전망

HBR 25.11.14The blood glucose test strips market size is estimated at USD 12.02 billion in 2025, and is expected to reach USD 16.05 billion by 2030, at a CAGR of 5.96% during the forecast period (2025-2030).

Growth stems mainly from the relentless rise in diabetes prevalence, widening insurance coverage, and continuous product refinement that keeps finger-stick monitoring relevant even as newer technologies emerge. Companies are investing heavily in nanomaterial-enhanced electrodes to meet the United States Food and Drug Administration's tighter 2024 accuracy guidance, bringing detection limits down to 0.01 mM while holding retail prices within reach for daily users. At the same time, the disruptive appeal of continuous glucose monitoring (CGM) is forcing incumbents to defend the blood glucose test strips market by doubling down on convenience, accuracy and omnichannel reach.

Global Blood Glucose Test Strips Market Trends and Insights

Rising Prevalence of Diabetes

Record diabetes incidence is fundamentally redrawing the blood glucose test strips market. A pooled analysis of 1,108 population-representative studies covering 141 million participants found type 2 diabetes already represents 96% of all cases, and Western Pacific nations could see prevalence jump another 17.82% by 2050. This epidemiological surge fuels sustained strip demand because finger-stick testing remains the single most accessible daily monitoring tool in many health systems. As national diabetes counts climb, reaching a projected 852.5 million adults globally by 2050, manufacturers are tailoring distribution strategies for urban, peri-urban, and rural clinics alike to keep pace with shifting hot-spots.

Increasing Awareness and Self-Monitoring

Clinical evidence shows every additional daily SMBG measurement delivers meaningful A1c reductions, encouraging physicians to prescribe tighter self-testing schedules. Education programs funded by public-health agencies and advocacy groups boost patient confidence, which in turn lifts test-strip throughput in pharmacies. Personalized target ranges endorsed by the American Diabetes Association place further emphasis on routine monitoring for insulin titration. These twin forces-clinical endorsement and patient empowerment-reinforce the blood glucose test strips market's resilience even in digitally advanced economies.

High Cost of Test Strips

Prices in the USD 0.50-1.00 range per strip sound modest, yet multiply quickly for patients who test four or more times a day, especially outside the safety net of insurance. In developing economies where private coverage is rare, many users ration strips, leaving glucose control sub-optimal and undermining medical guidelines. The consequent volume shortfall trims the blood glucose test strips market growth outlook in low-income segments and heightens demand for cheaper alternatives or bundled subscription packs.

Other drivers and restraints analyzed in the detailed report include:

- Technology Advancements

- Government Initiatives and Insurance Coverage

- Surge in Uptake of CGM Systems

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Thick film strips delivered 55.83% of 2024 revenue thanks to production costs running 30-40% below thin-film and photometric alternatives, translating into retail affordability that keeps testing volumes high. The blood glucose test strips market size for thick film will climb at a measured pace as rural clinics and value-oriented consumers continue favoring proven, inexpensive designs. Optical/photometric formats, while small in volume, post the strongest 7.23% CAGR to 2030 because photodiode readers dampen environmental interference and offer colorimetric feedback that appeals to tech-savvy users. Manufacturers now position photometric cartridges in connected starter kits aimed at early adopters, preventing outright migration to CGM while creating a premium pocket inside the broader blood glucose test strips market.

Future upgrades in nanocoatings and microfluidic channels will further push accuracy, but economies of scale continue to anchor thick film manufacturing lines across Asia and Eastern Europe. As vendors add Bluetooth-enabled meters to low-cost strip bundles, cost leadership converges with digital convenience, giving thick film an enduring moat. Meanwhile, joint ventures between optics specialists and meter OEMs could speed photometric penetration, yet supply chain complexity and higher per-unit costs may cap its blood glucose test strips market share below 20% through the forecast window.

Type 2 users generate 86.14% of 2024 strip sales, steering R&D toward ease of use, bulk packaging and loyalty programs that reduce per-test costs. This cohort often checks glucose once or twice daily, so reliable lancet-strip kits that fit into pockets remain the design priority. Conversely, Type 1 consumers, though representing a smaller slice, test 6-10 times every day and demand near-laboratory precision to fine-tune intensive insulin regimens. The blood glucose test strips market size for Type 1 is expanding 6.43% annually as pediatric and young adult patients embrace app-integrated meters that flag hypoglycemia trends in real time.

Manufacturers cater to this split by offering double-wide portfolios-value bundles for Type 2 maintenance and premium nano-enhanced strips for Type 1 fine dosing. Cross-subsidizing premium margins funds aggressive price promotions in developing economies, ensuring the blood glucose test strips market keeps river-like breadth even in the face of CGM encroachment.

The Blood Glucose Test Strips Market Report is Segmented by Product Type (Thick Film Strips, Thin Film Strips, and Optical / Photometric Strips), Diabetes Type (Type 1 Diabetes, Type 2 Diabetes, and More), End User (Hospitals and Clinics, Homecare / Personal Use and More) Distribution Channel (Hospital Pharmacies, and More) and Geography (North America, Europe, and More). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America generated 35.47% of global 2024 revenue, underpinned by high insurance penetration and Medicare policies that reimburse routine monitoring for seniors. A National Clinical Care Commission study showed regular self-testing rose 27% among beneficiaries after reimbursement tweaks, demonstrating how robust coverage underwrites steady strip turnover. Despite CGM enthusiasm, many primary-care clinics still prescribe finger-stick meters as baseline tools, keeping the blood glucose test strips market in positive territory.

Asia Pacific is the growth engine, advancing at 6.86% CAGR as China and India grapple with soaring diagnoses and urban lifestyles that spur carbohydrate-heavy diets. India alone could see diabetic adults rise from 89.8 million in 2024 to 156.7 million by 2050, forcing federal and state governments to subsidize essential monitoring supplies. Local manufacturers such as Sinocare ride cost advantages to flood tier-2 and tier-3 cities with affordable kits, yet premium multinationals still capture urban hospital contracts, preserving stratified competition inside the region's blood glucose test strips market.

Europe retains sizable share on the back of national health systems that fund routine testing and impose stringent CE marking requirements. These regulations create higher entry barriers, pushing suppliers to invest in precision engineering. Latin America and the Middle East & Africa trails but expands year after year as awareness campaigns and micro-insurance programs widen access to SMBG. Price-sensitive consumers in these areas favor thick-film kits, reinforcing cost-leadership strategies that maintain global reach for the blood glucose test strips market.

- Abbott Laboratories

- Roche

- LifeScan IP Holdings, LLC.

- Ascensia Diabetes Care Holdings AG.

- Arkray

- AgaMatrix

- Bionime

- Sinocare

- Trividia Health

- Rossmax

- Ypsomed

- SD Biosensor Inc.

- TaiDoc Technology

- i-SENS Inc.

- Omron Healthcare Co. Ltd.

- Nova Biomedical

- 77 Elektronika Kft.

- OK Biotech Co. Ltd.

- Acon Laboratories

- Prodigy Diabetes Care, LLC

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Prevalence of Diabetes

- 4.2.2 Increasing Awareness and Self-Monitoring

- 4.2.3 Technology Advancements

- 4.2.4 Government Initiatives and Insurance Coverage

- 4.2.5 Growth in Online and Retail Distribution Channels

- 4.2.6 Aging Populations and the Associated Shift toward Home-based Chronic-disease Management

- 4.3 Market Restraints

- 4.3.1 High Cost of Test Strips

- 4.3.2 Surge in Uptake of CGM Systems

- 4.3.3 Stringent Regulatory Requirements

- 4.3.4 Growing Environmental and Biohazard Disposal Concerns

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Outlook

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Consumers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitute Products

- 4.7.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value)

- 5.1 By Product Type

- 5.1.1 Thick Film Strips

- 5.1.2 Thin Film Strips

- 5.1.3 Optical / Photometric Strips

- 5.2 By Diabetes Type

- 5.2.1 Type 1 Diabetes

- 5.2.2 Type 2 Diabetes

- 5.2.3 Gestational and Others

- 5.3 By End User

- 5.3.1 Hospitals and Clinics

- 5.3.2 Homecare / Personal Use

- 5.3.3 Diagnostic Laboratories

- 5.4 By Distribution Channel

- 5.4.1 Hospital Pharmacies

- 5.4.2 Retail Pharmacies

- 5.4.3 Online Pharmacies

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Rest of North America

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Russia

- 5.5.2.7 Rest of Europe

- 5.5.3 Asia Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 Australia

- 5.5.3.5 South Korea

- 5.5.3.6 Vietnam

- 5.5.3.7 Malaysia

- 5.5.3.8 Indonesia

- 5.5.3.9 Thailand

- 5.5.3.10 Rest of Asia Pacific

- 5.5.4 Middle East and Africa

- 5.5.4.1 Saudi Arabia

- 5.5.4.2 Iran

- 5.5.4.3 Egypt

- 5.5.4.4 Oman

- 5.5.4.5 South Africa

- 5.5.4.6 Rest of Middle East and Africa

- 5.5.5 Latin America

- 5.5.5.1 Mexico

- 5.5.5.2 Brazil

- 5.5.5.3 Rest of South America

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles ((includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.3.1 Abbott Laboratories

- 6.3.2 F. Hoffmann-La Roche Ltd

- 6.3.3 LifeScan IP Holdings, LLC.

- 6.3.4 Ascensia Diabetes Care Holdings AG.

- 6.3.5 ARKRAY Inc.

- 6.3.6 AgaMatrix

- 6.3.7 Bionime Corporation

- 6.3.8 Sinocare Inc.

- 6.3.9 Trividia Health Inc.

- 6.3.10 Rossmax International Ltd

- 6.3.11 Ypsomed AG

- 6.3.12 SD Biosensor Inc.

- 6.3.13 TaiDoc Technology Corporation

- 6.3.14 i-SENS Inc.

- 6.3.15 Omron Healthcare Co. Ltd.

- 6.3.16 Nova Biomedical

- 6.3.17 77 Elektronika Kft.

- 6.3.18 OK Biotech Co. Ltd.

- 6.3.19 ACON Laboratories Inc.

- 6.3.20 Prodigy Diabetes Care, LLC

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment