|

시장보고서

상품코드

1849940

항생제 : 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Antibiotics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

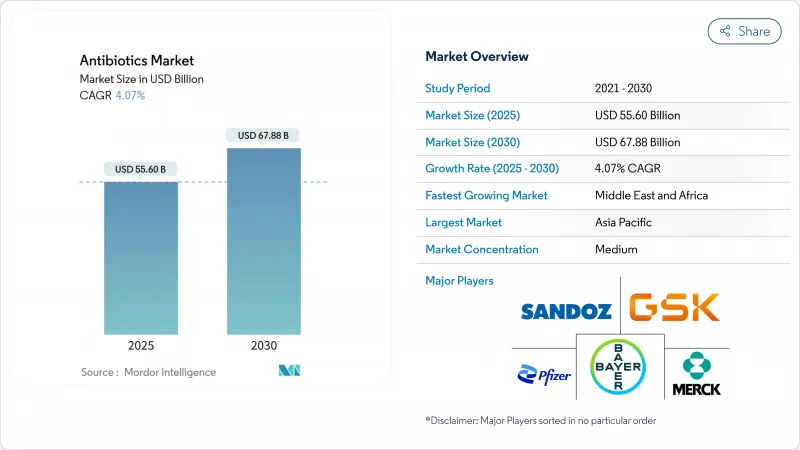

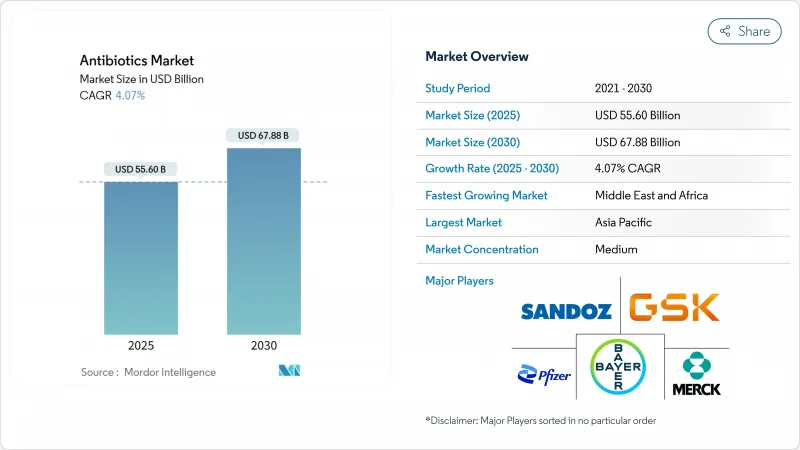

항생제 시장 규모는 2025년에 556억 달러로 평가되었고, 2030년에 678억 8,000만 달러에 이를 것으로 예상되며 CAGR은 4.07%를 나타낼 전망입니다.

이러한 추세는 항생제 내성(AMR)의 급증과 주요 신흥 경제국에서 의료 서비스 범위 확장이 맞서 싸우는 양상을 반영합니다. 병원 수용 능력 투자, 강화된 감염 관리 프로토콜, 혁신적 치료법에 대한 정부의 신규 인센티브가 수요를 끌어올리고 있지만, 각 요인은 동시에 수익 성장을 제약하는 관리 체계의 취약점을 드러내고 있습니다. 따라서 항생제 산업은 치료적 필요성과 책임 있는 사용 사이에서 운영되며, 이 균형은 점차 제품 파이프라인을 표적화되고 미생물군을 보존하는 약물로 재편하고 있습니다. 병원 구매자들의 증가하는 증거는 어려운 병원체에 대한 입증된 활성을 가진 신약에 대한 가격 결정력이 여전히 가장 강력함을 보여주며, 이는 지불 주체가 명확한 임상적 차별화를 보상할 것이라는 신호입니다. 새로운 추론은 수익 모멘텀이 동일한 제품 자료에서 효능과 관리 가치를 모두 입증하는 능력에 점점 더 좌우된다는 점입니다.

세계의 항생제 시장 동향 및 인사이트

항균제 내성균 증가에 의한 지속적인 혁신의 필요성

2024년 8월 WHO 발표에 따르면, 항생제 내성(AMR)은 이미 매년 약 495만 명의 사망에 기여하며, 방치될 경우 2050년까지 1,000만 명에 이를 수 있습니다. 이러한 증가하는 피해는 공공 및 민간 자본을 최초의 분자(first-in-class)로 유도하고 있지만, 파이프라인 분석에 따르면 후기 단계 항생제 32개 중 진정으로 새로운 작용 기전을 도입한 것은 12개에 불과합니다. 모니터링 연구소들은 카르바페넴 내성 아시네토박터 바우마니(Acinetobacter baumannii)가 지역사회 환경에서 나타나고 있다고 보고하여 보건부로 하여금 대체 치료법에 대한 자금 지원을 신속히 추진하도록 강요하고 있습니다. 벤처 자금 동향을 보면 투자자들이 복합 요법 제공이 가능한 플랫폼을 점점 더 선호하는 것으로 나타난다. 이는 진화하는 내성 패턴에 유연하게 대응할 수 있는 접근법입니다. 새로운 추론은 투자 의향이 이제 단일 표적 설계보다는 여러 고우선순위 병원체를 해결할 수 있는 후보 물질의 능력과 밀접하게 연계된다는 점입니다.

3차 의료기관에서 증가하는 병원 내 감염 발생률

OECD(2024년 11월)에 따르면 매년 약 380만 명의 유럽인이 병원 내 감염(HAI)에 걸리며, 이로 인한 사망자는 9만 명에 달합니다. HAI 발생 시 입원 기간은 7일에서 19일로 증가하며, 이로 인한 기회 비용은 사례당 1,000유로(1,120달러)를 초과합니다. 저소득 및 중간소득 국가 병원에서는 특히 침습적 시술이 표준이고 인력 비율이 낮은 중환자실에서 더 높은 발생률을 보고합니다. 재무 모델링에 따르면 감염 관리 예산이 병원 전체 지출보다 빠르게 증가하고 있어, 관리자들이 이제 HAI 감소를 핵심 비용 절감 수단으로 인식하고 있음을 시사합니다. 새로운 관측 결과로, 조달 부서에서 점점 더 저항성 발자국이 작은 항생제를 지정하고 있어, 관리 지표가 구매 가격만큼 중요해지고 있음을 알립니다.

다제내성 병원체의 급속한 확산

22024년 7월 WHO 보고에 따르면, 카르바페넴 내성 유전자를 보유한 초강력 클레브시엘라 폐렴균(Klebsiella pneumoniae) 균주가 2024년 중 등장하여 신생아실 및 중환자실에 대한 새로운 우려를 불러일으켰습니다. 인도 및 사하라 이남 아프리카 전역의 모니터링 결과 세팔로스포린과 플루오로퀴놀론 내성이 급증하는 양상이 관찰되었으며, 이러한 패턴이 지역사회 진료소에서도 나타나기 시작했습니다. 새로운 내성 집단이 발생할 때마다 기존 약물의 상업적 수명이 단축되고, 의료진이 치료 강도를 조기에 높여 치료 비용이 증가합니다. 새롭게 관찰된 점은 보험급여 기관들이 항생제 가격 협상 시 내성 모델링을 고려하기 시작하여, 지급 수준을 예측된 내성 지속 기간과 효과적으로 연계하고 있다는 것입니다.

부문 분석

세팔로스포린계 항생제는 2025년 항생제 시장 점유율 24.2%를 차지하며 시장 규모는 134억 9,000만 달러에 달할 전망입니다. 광범위한 병원체 커버리지와 다수 임상 지침에 포함된 점이 수요를 유지합니다. 미국에서 황색포도상구균 혈류 감염 등 3가지 적응증에 대한 제브테라(Zevtera) 승인은 처방자의 신뢰를 강화합니다. 현재 항생제 관리팀은 세팔로스포린과 신속진단법을 병행하여 경험적 치료 기간을 단축하고 있으며, 이는 판매량 감소 없이 내성 확산을 억제할 수 있는 업무 흐름 변화입니다. 진단법과 기존 약물의 결합은 내성률이 높은 환경에서도 약물의 효용성을 유지한다는 새로운 시사점을 제공합니다.

카바페넴계 항생제는 2030년까지 6.8%라는 가장 높은 연평균 성장률(CAGR)을 보일 것으로 예상되며, 이는 다제내성 감염에 대한 최후의 수단으로서의 지위를 강조합니다. 사용 현황 감사 결과, 의료진이 카바페넴을 배양 확인 사례에 점점 더 제한적으로 사용하는 것으로 나타났으며, 이는 내성 추세를 안정화시킬 수 있는 관행입니다. 제조사들은 외래 환자용 비경구 항생제 치료에 적합한 1일 1회 투여 제형을 출시하여 수요를 지원하고 있습니다. 감염질환 약사들의 증거에 따르면, 지역 항생제 감수성 검사 결과를 바탕으로 할 때 관리 위원회가 카바페넴 요청을 더 쉽게 승인하는 것으로 나타났으며, 이는 사용 제한 하에서도 꾸준한 성장이 가능함을 시사합니다.

지역별 분석

아시아태평양 지역은 2025년 항생제 시장 점유율 34.27%(190억 5천만 달러 규모)를 차지했으며, 2030년까지 연평균 복합 성장률(CAGR) 7.2%를 기록할 것으로 전망됩니다. 이 지역의 대규모 인구, 높은 감염 부담, 확대되는 보험 적용 범위가 이러한 우위를 뒷받침합니다. 인도네시아 등 정부는 2024년 국가 항생제 내성(AMR) 대책과 현지 제조 인센티브를 연계하여 공급 안정성과 품질 개선을 동시에 촉진했습니다. 중국과 인도는 제네릭 의약품의 글로벌 생산 거점 역할을 하면서도 신약 후보물질에 대한 공격적 투자를 병행하고 있으며, 이는 국내 기업들이 가치 사슬 상위로 진출할 수 있는 기반을 마련하고 있습니다. 일본의 정교한 항생제 관리 정책은 성숙한 시장이 접근성을 해치지 않으면서도 과다 사용을 억제할 수 있음을 보여주며, 동종 시장들에게 모범 사례를 제시하고 있습니다. 새로운 관측으로는 해당 지역 공중보건 기관들이 클라우드 기반 모니터링 대시보드를 도입해 신종 내성 집단 발생 시 대응 속도를 가속화하고 있다는 점입니다.

북미는 시장 규모 2위를 차지하며 규제 및 가격 기준을 설정합니다. 미국의 항생제 개발 촉진법(GAIN)은 적격 감염병 치료제의 독점권을 연장하는 도구로, EXBLIFEP 및 ORLYNVAH 같은 제품의 승인을 지원했습니다. 보험사들은 청구서에 내성 증거가 첨부될 경우 이러한 치료제에 대해 프리미엄 요율로 보상하며, 이는 지불 기관들이 구입 가격 이상의 가치를 인정함을 시사합니다. 캐나다의 통합 모니터링 네트워크는 세분화된 내성 데이터를 제공하여 병원이 경험적 프로토콜을 개선하고 불필요한 광범위 항생제 사용을 줄일 수 있게 합니다. 강력한 모니터링 체계를 갖춘 시장은 오용을 제한하면서도 표적화된 보상을 통해 혁신을 장려할 수 있다는 점이 새롭게 도출된 결론입니다.

유럽은 독일, 영국, 프랑스가 주도하는 가운데 견고한 3위 자리를 유지하고 있습니다. 유럽의약품청(EMA)의 미충족 수요 항생제 신속 승인 절차는 신청 기간을 단축시켜 기업들이 유럽연합(EU)에서 먼저 출시하도록 장려합니다. 공공 조달 체계는 최저 단가만이 아닌 입증된 임상적·관리적 혜택에 따라 공급업체를 보상하는 성과 기반 계약으로 전환 중입니다. 한편 중동 지역은 규모는 작지만 걸프 국가들이 3차 의료 인프라를 업그레이드하고 서구식 감염 관리 기준을 도입함에 따라 7.2%라는 가장 빠른 지역 연평균 성장률(CAGR)을 기록하고 있습니다. 아랍에미리트 병원은 고급 카르바페넴과 BLI 조합 항생제 수요가 증가하고 있으며, 이는 해당 지역이 중간 단계 치료법을 건너뛰고 있음을 시사합니다. 새로운 추론으로는 에너지 부국인 걸프 경제권의 다각화된 조달 예산이 인구 규모만으로는 예측할 수 있는 것보다 프리미엄 항생제 도입을 가속화할 수 있다는 점입니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월의 애널리스트 지원

목차

제1장 서론

- 조사의 전제조건과 시장의 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 지속적인 항생제 혁신 및 비축 필요성을 야기하는 전 세계적 항생제 내성(AMR) 증가

- 신흥 경제국 내 3차 의료기관에서 병원 감염 발생률 증가

- 고부담 지역에서 보편적 건강보험 적용 확대 및 필수 항생제에 대한 공공 보험급여 확대

- 치료 성과 향상 위한 베타-락타마제 억제제 복합제 및 신개념 치료법 기술 발전

- 팬데믹 대비 및 국가 전략적 항생제 비축에 대한 관심 증대

- 비축 항생제 확보 및 조달 의무화하는 정부 지원 항생제 관리 프로그램

- 시장 성장 억제요인

- 상업적 개발 일정을 앞지르는 다제내성 병원체의 급속한 확산

- “모니터링” 및 “비축” 등급 항생제 사용을 제한하는 엄격한 관리 및 조달 정책

- 높은 임상 시험 실패율과 불리한 투자 수익률로 인한 민간 연구개발 자금 조달 위축

- 소수 제조 허브에 집중된 원료의약품(API) 공급망 차질

- 밸류체인 분석

- 규제 전망

- Porter's Five Forces 분석

- 신규 참가업체의 위협

- 구매자의 협상력/소비자

- 공급기업의 협상력

- 대체품의 위협

- 경쟁 기업간 경쟁 관계

제5장 시장 규모와 성장 예측

- 제품 유형별

- 세팔로스포린

- 페니실린

- 플루오로퀴놀론

- 마크로라이드

- 카르바페넴

- 아미노글리코시드

- 술폰아미드

- 기타 제품 유형

- 약효 범위별

- 광범위한 항생제

- 좁은 범위의 항생제

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 기타 유럽

- 아시아태평양

- 중국

- 일본

- 인도

- 한국

- 호주

- 기타 아시아

- 중동 및 아프리카

- GCC

- 남아프리카

- 기타 중동 및 아프리카

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 북미

제6장 경쟁 구도

- 시장 집중도

- 시장 점유율 분석

- 기업 프로파일

- Johnson & Johnson

- Merck & Co., Inc.

- Pfizer Inc.

- Bayer AG

- Novartis AG(Sandoz)

- Abbott Laboratories

- Otsuka Pharmaceutical Co., Ltd.

- Eli Lilly and Company

- GlaxoSmithKline plc

- Sanofi

- Teva Pharmaceutical Industries Ltd.

- Lupin Limited

- Sun Pharmaceutical Industries Ltd.

- Cipla Ltd.

- Viatris Inc.(Mylan)

- Hikma Pharmaceuticals PLC

- Shionogi & Co., Ltd.

- Melinta Therapeutics

제7장 시장 기회와 장래의 전망

HBR 25.11.14The antibiotics market size reached USD 55.60 billion in 2025 and is forecast to climb to USD 67.88 billion by 2030, yielding a compound annual growth rate (CAGR) of 4.07%.

This trajectory reflects a tug-of-war between the surge in antimicrobial resistance (AMR) and the steady expansion of healthcare coverage in large emerging economies. Investment in hospital capacity, tighter infection-control protocols, and new government incentives for innovative therapies are lifting demand, yet every driver also exposes stewardship gaps that restrain revenue growth. The antibiotics industry, therefore, operates between therapeutic necessity and responsible use, a balance that is slowly reshaping product pipelines toward targeted, microbiome-sparing drugs. Growing evidence from hospital buyers shows that pricing power remains strongest for newer agents with proven activity against difficult pathogens, a sign that payers will reward clear clinical differentiation. One fresh inference is that revenue momentum increasingly hinges on the ability to demonstrate both efficacy and stewardship value in the same product dossier.

Global Antibiotics Market Trends and Insights

Escalating Antimicrobial Resistance Necessitates Continuous Innovation

AMR already contributes to an estimated 4.95 million deaths each year and could reach 10 million by 2050 if left unchecked, as per the WHO in August 2024. This mounting toll is steering public and private capital toward first-in-class molecules, yet pipeline analysis shows that only 12 of 32 late-stage antibiotics introduce genuinely new mechanisms of action. Surveillance laboratories report that carbapenem-resistant Acinetobacter baumannii is appearing in community settings, forcing health ministries to fast-track funding for alternative treatments. Venture-funding trends reveal that investors increasingly favor platforms capable of delivering combination regimens, an approach that offers flexibility against evolving resistance patterns. A fresh inference is that investment appetites now track closely with a candidate's ability to address multiple high-priority pathogens rather than single-target designs.

Rising Incidence of Hospital-Acquired Infections in Tertiary-Care Settings

Roughly 3.8 million Europeans contract hospital-acquired infections (HAIs) annually, and 90,000 deaths are linked to these events, according to OECD, November 2024. Inpatient stays jump from seven to nineteen days when an HAI occurs, inflating opportunity costs past EUR 1,000 (USD 1,120) per case. Hospitals in low- and middle-income countries report even higher incidence, especially in intensive-care units where invasive procedures are standard and staffing ratios are lower. Financial modeling shows infection-control budgets are rising faster than overall hospital spending, indicating administrators now view HAI reduction as a core cost-containment lever. A new observation is that procurement departments increasingly specify antibiotics with smaller resistance footprints, signaling that stewardship metrics are becoming as important as acquisition price.

Rapid Proliferation of Multidrug-Resistant Pathogens

Hypervirulent Klebsiella pneumoniae strains carrying carbapenem-resistance genes emerged during 2024, according to the WHO in July 2024, raising new concerns for neonatal and intensive-care wards. Surveillance across India and sub-Saharan Africa shows sharp rises in cephalosporin and fluoroquinolone resistance, patterns now cropping up in community clinics as well. Each new resistance cluster compresses the commercial life of established drugs and prompts clinicians to escalate therapy earlier, elevating treatment costs. An emerging observation is that reimbursement agencies are beginning to weigh resistance modeling when negotiating antibiotic prices, effectively linking payment levels to predicted durability.

Other drivers and restraints analyzed in the detailed report include:

- Expansion of Universal Health Coverage Enhances Essential Antibiotics Access

- Technological Advancements in B-lactamase Inhibitor Combinations

- Stringent Stewardship Policies Limit Use of "Watch" and "Reserve" Classes

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Cephalosporins command 24.2% antibiotics market share in 2025, translating to a market size of USD 13.49 billion. Their broad pathogen coverage and inclusion in multiple clinical guidelines sustain demand. The U.S. approval of Zevtera for three indications, including Staphylococcus aureus bloodstream infections, bolsters prescriber trust. Stewardship teams now pair cephalosporins with rapid diagnostics to shorten empiric-therapy windows, a workflow change that can curb resistance without denting unit sales. One fresh inference is that coupling diagnostics with established drugs extends their relevance even in resistance-heavy settings.

Carbapenems reveal the strongest forecast CAGR of 6.8% through 2030, underscoring their status as last-line agents for multidrug-resistant infections. Utilization audits show clinicians increasingly reserve carbapenems for culture-confirmed cases, a practice that can stabilize resistance trends. Manufacturers support demand by launching once-daily formulations suitable for outpatient parenteral-antibiotic therapy. Evidence from infectious-disease pharmacists indicates stewardship committees approve carbapenem requests more readily when bolstered by local antibiograms, implying steady growth even under usage constraints.

The Antibiotics Market is Segmented by Product Type (Cephalosporins, Penicillins, Fluoroquinolones, Macrolides, Carbapenems, Aminoglycosides, Sulfonamides, and Other Product Types), Spectrum (Broad-Spectrum Antibiotics and Narrow-Spectrum Antibiotics), and Geography (North America, Europe, Asia-Pacific, and More). The Market Sizes and Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific held 34.27% antibiotics market share in 2025, worth USD 19.05 billion, and is projected to post a 7.2% CAGR through 2030. The region's large population, high infection burden, and widening insurance coverage underpin this dominance. Governments such as Indonesia paired national AMR plans with local manufacturing incentives in 2024, stimulating both supply security and quality improvements. China and India serve as global production hubs for generics while investing aggressively in novel candidates, an approach that positions domestic firms to ascend the value chain. Japan's sophisticated stewardship policies demonstrate that mature markets can curb overuse without harming access, offering a blueprint for peers. A new observation is that public health agencies in the region now deploy cloud-based surveillance dashboards, accelerating response times to emerging resistance clusters.

North America ranks second in market size and sets regulatory and pricing benchmarks. The U.S. Generating Antibiotic Incentives Now (GAIN) Act extends exclusivity for qualified infectious-disease products, a tool that aided approvals such as EXBLIFEP and ORLYNVAH. Insurers reimburse these therapies at premium rates when resistance documentation accompanies claims, indicating payers see value beyond acquisition price. Canada's coordinated surveillance network supplies granular resistance data, letting hospitals refine empiric protocols and reduce unnecessary broad-spectrum use. An emergent inference is that markets with robust surveillance can both limit misuse and still reward innovation through targeted reimbursement.

Europe maintains a solid third position, led by Germany, the United Kingdom and France. The European Medicines Agency's streamlined routes for unmet-need antibiotics shorten filing timelines, encouraging companies to launch first in the bloc. Public-procurement frameworks move toward outcome-based contracts, rewarding suppliers for demonstrable clinical and stewardship benefits rather than lowest unit cost alone. Meanwhile, the Middle East, albeit smaller, posts the fastest regional CAGR of 7.2% as Gulf states upgrade tertiary infrastructure and adopt Western infection-control standards. Hospitals in the United Arab Emirates increasingly demand advanced carbapenem and BLI combinations, a sign the region is leapfrogging intermediate therapies. A fresh inference is that diversified procurement budgets in energy-rich Gulf economies can accelerate adoption of premium antibiotics faster than population size alone would predict.

- Johnson & Johnson

- Merck

- Pfizer

- Bayer

- Novartis

- Abbott Laboratories

- Otsuka

- Eli Lilly and Company

- GlaxoSmithKline

- Sanofi

- Teva Pharmaceutical Industries

- Lupin

- Sun Pharmaceuticals Industries

- Cipla

- Viatris

- Hikma Pharmaceuticals

- Shionogi & Co., Ltd.

- Melinta Therapeutics

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Escalating Antimicrobial Resistance (AMR) Worldwide Necessitating Continuous Antibiotic Innovation and Stockpiling

- 4.2.2 Rising Incidence of Hospital-Acquired Infections in Tertiary-Care Settings Across Emerging Economies

- 4.2.3 Expansion of Universal Health Coverage and Public Reimbursement for Essential Antibiotics in High-Burden Regions

- 4.2.4 Technological Advancements in Beta-lactamase Inhibitor Combinations and Novel Modalities Enhancing Treatment Outcomes

- 4.2.5 Growing Focus on Pandemic Preparedness and Strategic National Antibiotic Reserves

- 4.2.6 Government-funded Antibiotic Stewardship Programs Mandating Reserve Antibiotic Stockpiling and Procurement

- 4.3 Market Restraints

- 4.3.1 Rapid Proliferation of Multidrug-Resistant Pathogens Outpacing Commercial Development Timelines

- 4.3.2 Stringent Stewardship and Procurement Policies Limiting Use of "Watch" and "Reserve" Classes

- 4.3.3 High Clinical-Trial Failure Rates and Unfavorable Return on Investment Deterring Private R&D Funding

- 4.3.4 Disruptions in Active Pharmaceutical Ingredient (API) Supply Chains Concentrated in Few Manufacturing Hubs

- 4.4 Value Chain Analysis

- 4.5 Regulatory Outlook

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Buyers/Consumers

- 4.6.3 Bargaining Power of Suppliers

- 4.6.4 Threat of Substitute Products

- 4.6.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value)

- 5.1 By Product Type

- 5.1.1 Cephalosporins

- 5.1.2 Penicillins

- 5.1.3 Fluoroquinolones

- 5.1.4 Macrolides

- 5.1.5 Carbapenems

- 5.1.6 Aminoglycosides

- 5.1.7 Sulfonamides

- 5.1.8 Other Product Types

- 5.2 By Spectrum

- 5.2.1 Broad-spectrum Antibiotics

- 5.2.2 Narrow-spectrum Antibiotics

- 5.3 By Geography

- 5.3.1 North America

- 5.3.1.1 United States

- 5.3.1.2 Canada

- 5.3.1.3 Mexico

- 5.3.2 Europe

- 5.3.2.1 Germany

- 5.3.2.2 United Kingdom

- 5.3.2.3 France

- 5.3.2.4 Italy

- 5.3.2.5 Spain

- 5.3.2.6 Rest of Europe

- 5.3.3 Asia Pacific

- 5.3.3.1 China

- 5.3.3.2 Japan

- 5.3.3.3 India

- 5.3.3.4 South Korea

- 5.3.3.5 Australia

- 5.3.3.6 Rest of Asia

- 5.3.4 Middle East and Africa

- 5.3.4.1 GCC

- 5.3.4.2 South Africa

- 5.3.4.3 Rest of Middle East and Africa

- 5.3.5 South America

- 5.3.5.1 Brazil

- 5.3.5.2 Argentina

- 5.3.5.3 Rest of South America

- 5.3.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.3.1 Johnson & Johnson

- 6.3.2 Merck & Co., Inc.

- 6.3.3 Pfizer Inc.

- 6.3.4 Bayer AG

- 6.3.5 Novartis AG (Sandoz)

- 6.3.6 Abbott Laboratories

- 6.3.7 Otsuka Pharmaceutical Co., Ltd.

- 6.3.8 Eli Lilly and Company

- 6.3.9 GlaxoSmithKline plc

- 6.3.10 Sanofi

- 6.3.11 Teva Pharmaceutical Industries Ltd.

- 6.3.12 Lupin Limited

- 6.3.13 Sun Pharmaceutical Industries Ltd.

- 6.3.14 Cipla Ltd.

- 6.3.15 Viatris Inc. (Mylan)

- 6.3.16 Hikma Pharmaceuticals PLC

- 6.3.17 Shionogi & Co., Ltd.

- 6.3.18 Melinta Therapeutics

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment