|

시장보고서

상품코드

1849997

SECaaS : 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)SECaaS - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

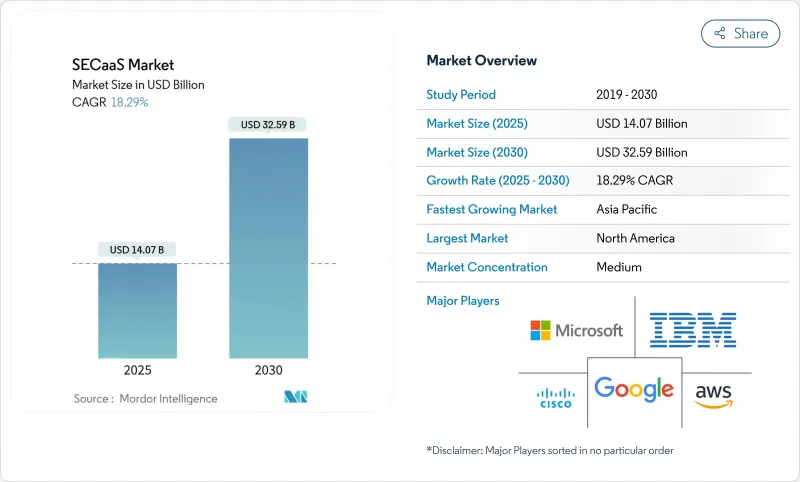

SECaaS 시장 규모는 2025년에 140억 7,000만 달러로 평가되었고, 2030년에 325억 9,000만 달러에 이를 것으로 예측되며, CAGR은 18.3%를 나타낼 전망입니다.

사이버 복원력에 대한 이사회 차원의 관심 증대, 사용량 기반 요금제의 주류화, 그리고 워크로드의 퍼블릭 및 하이브리드 클라우드로의 꾸준한 이전은 조달 예산을 클라우드 기반 보안 제어 수단으로 전환시키고 있습니다. 어플라이언스 중심 방위 체계를 통합형 보안 서비스 엣지(SSE) 플랫폼으로 교체하는 기업들은 사용량 기반 요금제가 실제 트래픽 규모에 맞춰 보호 수준을 유지한다는 점을 발견합니다. 이는 엣지 위치가 확산됨에 따라 결정적인 이점이 됩니다. 원격 근무 정책과 클라우드 네이티브 애플리케이션의 확산으로 신원, 기기, API 트래픽이 단일 정책 프레임워크 아래 통합되면서 수요는 더욱 가속화됩니다. SECaaS 시장은 이제 체류 시간을 단축하고 전체 스택 가시성을 제공하는 AI 기반 분석의 혜택을 누리며, 위협 인텔리전스를 자동화된 폐쇄형 대응으로 전환합니다.

세계의 SECaaS 시장 동향 및 인사이트

중소기업과 기업에서 클라우드 도입 급증

기업들이 경계 중심 기술을 폐기하고 신원 중심 방위 체계로 전환함에 따라 증가하는 클라우드 예산이 SECaaS 시장으로 직접 유입됩니다. 인도의 퍼블릭 클라우드 서비스 시장은 2028년까지 242억 달러를 초과할 것으로 전망되며, 보안 서비스가 연평균 19% 성장률로 가장 빠르게 성장할 것입니다. 중소기업은 전용 SOC 투자 없이도 기업급 보호를 확보하며, 이는 멀티테넌트 플랫폼 공급업체의 파이프라인을 가속화합니다. 금융 기관이 이러한 변화를 보여줍니다. 98%가 이미 최소 한 종류의 클라우드 서비스를 이용 중이며, 대부분은 이제 엄격한 접근 정책 하에 규제 대상 워크로드를 제3자 클라우드로 확장하고 있습니다. 클라우드로 이전되는 각 신규 워크로드는 SECaaS 구독 부가율을 자동으로 확대하여 공급업체 전반에 걸쳐 수익 증대 효과를 창출합니다.

사이버 위협의 고도화

공격자들은 이제 AI 생성 피싱, 자율적 악성코드, 대규모 크리덴셜 스터핑 캠페인을 활용하여 시그니처 기반 도구를 압도하고 있습니다. 은행들은 핵심 SOC 워크플로우에 머신러닝 분석을 내재화하고, 다년간의 사이버 예산 중 점점 더 많은 비중을 클라우드 네이티브 위협 탐지 엔진에 할당함으로써 대응하고 있습니다. 의료 서비스 제공업체들은 해킹 관련 침해 사고가 256% 급증함에 따라, 이제 모든 제3자 서비스의 진입 요건으로 SOC 2 및 HIPAA 준수 사항을 명시하고 있습니다. SECaaS 시장은 대규모 자율성을 제공합니다. 위협 인텔리전스 피드는 중앙 집중화되고, 탐지 모델은 지속적으로 재훈련되며, 자동화된 대응 조치는 전 세계적 포인트 오브 프레즌스(PoP)를 통해 몇 초 만에 조정됩니다.

데이터 거주 및 주권에 대한 우려

국경을 넘는 데이터 흐름 제한은 균일한 클라우드 도입에 도전장을 내밀고 있습니다. 유럽의 GDPR과 시행 예정인 디지털 운영 복원력 법(Digital Operational Resilience Act)은 많은 금융 기관이 고객 데이터를 지역 경계 내에 유지하도록 강제하여 글로벌 클라우드 위치 선택을 제한합니다. 멀티클라우드 전략은 매력적으로 보이지만, 주권 통제의 차이는 비용을 중복시키는 분산된 보안 아키텍처를 초래합니다. 신흥 주권 클라우드 서비스가 현지화된 처리를 약속하지만, 기업들은 잠재적인 벤더 종속성에 대해 여전히 신중한 태도를 유지하고 있습니다.

부문 분석

클라우드 우선 아키텍처가 신원 관리를 기본 제어 평면으로 격상시키면서, 신원 및 접근 관리(IAM)는 2024년 매출의 24.6%를 차지하며 SECaaS 시장의 핵심으로 자리매김하고 있습니다. 이 부문의 지속적인 중요성은 최소 권한 원칙의 강화와 제3자 개발자 계정의 폭발적 증가를 반영합니다. 고급 IAM 제품군은 이제 직원용 SSO를 넘어 컨테이너 오케스트레이터가 생성하는 비인간적 신원을 통제함으로써 라이선스 수와 사용자당 평균 수익을 높이고 있습니다. 덜 눈에 띄지만 더 빠르게 성장하는 클라우드 액세스 보안 브로커(CASB) 부문은 승인되지 않은 SaaS 발견 및 SaaS-to-SaaS 트래픽 내 데이터 유출 방지 규칙 적용 필요성에 힘입어 19.0%의 연평균 성장률(CAGR)을 기록 중입니다. 이러한 솔루션 기둥들은 통합된 보안 서비스 엣지(SSE) 제공으로의 전환을 뒷받침하며, 인라인 검사, 접근 제어, 데이터 분류 기능이 글로벌 엣지 패브릭에 공동 배치됩니다. 보안 이메일 게이트웨이(SEG) 및 보안 웹 게이트웨이(SWG) 기능은 이러한 통합 스택으로 이전 중이며, 차세대 SIEM은 하이퍼스케일러 객체 저장소를 활용하기 위해 수집 파이프라인을 재구성하여 테라바이트당 비용을 대폭 절감하고 전개 마찰을 제거합니다.

2세대 취약점 관리 도구는 CI/CD 파이프라인에 직접 내장되어 코드, 빌드, 런타임 간의 피드백 루프를 닫습니다. 이 전환은 보안 상태를 개발자 워크플로에 긴밀히 연계시키고 SECaaS 시장을 광범위한 플랫폼 엔지니어링 운동과 동맹시킵니다. 벤더들은 이제 사전 승인된 IaC 템플릿, 정책-코드 라이브러리, 파이프라인 플러그인을 패키징하여 위험 가시성이 부가된 기능이 아닌 본질적인 요소가 되도록 합니다. 가장 효과적인 영업 전략은 측정 가능한 MTTD(평균 탐지 시간) 단축, 대시보드 기반 규정 준수, 그리고 5개의 포인트 솔루션을 단일 계약으로 통합함으로써 입증 가능한 ROI(투자 수익률)를 중심으로 전개됩니다.

조직들이 글로벌 포인트 오브 프레즌스(PoP)의 즉시 사용 가능성과 탄력적 확장성을 활용함에 따라, 2024년 SECaaS 시장의 59.8%를 퍼블릭 클라우드 전개가 차지했습니다. 그럼에도 규제 대상 기업들이 데이터 주권 요구사항과 지연 시간 및 성능 기준을 저울질하면서 하이브리드 클라우드 채택률은 연평균 19.8% 성장률을 기록 중입니다. 기업들은 이제 일반적으로 퍼블릭 클라우드에 신원 브로커와 정책 엔진을 배치하는 한편, 민감한 워크로드를 위해 고객 관리 인프라에서 인라인 복호화 노드를 운영합니다. 이러한 아키텍처 다원주의는 정책을 한 번 전파하고 어디서나 적용할 수 있는 오케스트레이션 계층을 요구하며, 이는 벤더 간 경쟁에서 차별화 요소로 부상했습니다.

방위 및 핵심 인프라 운영자는 트래픽 메타데이터를 공유 환경에 노출할 수 없어 프라이빗 클라우드 SECaaS 인스턴스를 계속 사용합니다. 신흥 산업 청사진은 데이터 거주 규칙을 위반하지 않으면서 신뢰 영역 간 침해 지표의 통제된 동기화를 허용하며, 이는 국가 CERT와 협력하는 산업 제어 벤더들이 개척한 접근 방식입니다. 예측 기간 동안 멀티클라우드 정책 자동화는 기본 요소가 되어, 클라우드 플랫폼과 보안 벤더 간의 제휴를 촉진하여 신원 연동, 키 관리, 텔레메트리 표준화를 간소화할 것입니다.

지역 분석

북미는 2024년 글로벌 매출의 37.1%를 차지하며 하이퍼스케일러, 사이버 보안 혁신 기업, 얼리 어답터 기업의 집중도를 반영했습니다. CISA의 연방 지침은 기존 VPN 터널의 단계적 폐지를 촉구하며 제로 트러스트, 클라우드 네이티브 접근 방식을 장려함으로써 수요를 더욱 공고히 하고 있습니다. 금융 기관들은 이제 제3자 실사 검토 과정에서 보안 서비스 엣지(SSE) 통제를 의무화하여 공급망 전반에 걸친 네트워크 효과를 강화하고 있습니다. 캐나다와 멕시코는 이러한 추세를 타고 지역 데이터 보호 법규를 국경 간 데이터 흐름과 통합하여 플랫폼 확장을 촉진하고 있습니다.

아시아태평양 지역은 클라우드 마이그레이션 로드맵이 국가 디지털 경제 목표를 뒷받침함에 따라 2030년까지 연평균 19.4%의 성장률을 보일 전망입니다. 인도의 퍼블릭 클라우드 매출은 이미 세계 최고 성장률을 기록 중이며, 호주의 IRAP 프레임워크는 인증 공급업체에 정부 조달 채널을 개방했습니다. 일본 통신사들은 5G 엣지 구축을 주도하며 산업 고객들이 원격 공장에 인라인 검사 기능을 사전 구축하도록 촉진하고 있습니다. 지역별 데이터 규정은 다양하지만, 일관된 지역 인식 암호화 키 관리를 입증할 수 있는 공급업체가 입찰에서 결정적 우위를 점합니다.

유럽은 GDPR과 금융 기관의 실시간 제어 검증 의무화를 규정한 신생 디지털 운영 복원력 법안(Digital Operational Resilience Act)에 힘입어 견고한 수요를 유지하고 있습니다. 독일과 영국은 클라우드 접근, 이메일 보안, 데이터 유출 방지를 통합하는 융합 플랫폼 투자에서 선도적 위치를 차지하고 있습니다. 프랑스와 이탈리아는 중소기업 도입을 위한 공동 자금 지원을 배정한 국가 사이버 복원력 계획을 통해 조달을 가속화하고 있습니다. 다른 지역인 남미와 중동 및 아프리카는 클라우드 도입 단계가 상대적으로 초기이지만, 인터넷 백본과 규제 프레임워크를 급속히 확장 중이며, 경제 상황이 안정화되면 SECaaS 보급률이 높아질 토대를 마련하고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

목차

제1장 서론

- 조사의 전제조건과 시장의 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 중소기업과 대기업에서 클라우드 도입의 급증

- 사이버 위협의 고도화

- 원격 근무 및 BYOD 환경으로의 전환

- 엄격한 글로벌 데이터 보호 규정

- DevSecOps에서 API 기반 “코드로 구현하는 보안(Security-as-Code)” 수요

- 제로 트러스트 보안 서비스 엣지(SSE)의 신속한 도입

- 시장 성장 억제요인

- 데이터의 소재지와 주권에 관한 우려

- 다중 공급업체 구독 관리의 복잡성

- 지연 시간에 민감한 워크로드가 인라인 클라우드 보안을 우회하는 현상

- 사용량 기반 과금 표준 부재

- 밸류체인 분석

- 규제 상황

- 기술의 전망

- Porter's Five Forces 분석

- 공급기업의 협상력

- 구매자의 협상력

- 신규 참가업체의 위협

- 대체품의 위협

- 경쟁 기업간 경쟁 관계

- 투자분석

- 거시 경제 동향이 시장에 미치는 영향 평가

제5장 시장 규모와 성장 예측

- 솔루션별

- 신원 및 접근 관리(IAM)

- 보안 메일 게이트웨이

- 보안 웹 게이트웨이

- 클라우드 접근 보안 브로커(CASB)

- 보안 정보 및 이벤트 관리(SIEM)

- 취약성 관리

- 기타 솔루션

- 전개 모델별

- 퍼블릭 클라우드

- 프라이빗 클라우드

- 하이브리드 클라우드

- 조직 규모별

- 대기업

- 중소기업

- 최종 사용자 업계별

- BFSI

- IT 및 통신

- 헬스케어 및 생명과학

- 정부 및 방위

- 소매업 및 전자상거래

- 제조업

- 기타

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 기타 유럽

- 아시아태평양

- 중국

- 일본

- 인도

- 한국

- 호주

- 기타 아시아태평양

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 중동 및 아프리카

- 중동

- 사우디아라비아

- 아랍에미리트(UAE)

- 튀르키예

- 기타 중동

- 아프리카

- 남아프리카

- 이집트

- 나이지리아

- 기타 아프리카

- 북미

제6장 경쟁 구도

- 시장 집중도

- 전략적 동향

- 시장 점유율 분석

- 기업 프로파일

- Cisco Systems

- Zscaler

- Palo Alto Networks

- Microsoft

- Trend Micro

- Barracuda Networks

- IBM

- Proofpoint

- Sophos

- Forcepoint

- McAfee

- Symantec(Broadcom)

- Qualys

- Check Point Software

- Fortinet

- Cloudflare

- Okta

- Akamai

- Amazon Web Services

- Google Cloud

- CrowdStrike

- Rapid7

제7장 시장 기회와 장래의 전망

HBR 25.11.14The SECaaS market size stands at USD 14.07 billion in 2025 and is forecast to reach USD 32.59 billion by 2030, expanding at an 18.3% CAGR.

Heightened board-level focus on cyber-resilience, the mainstreaming of consumption-based pricing, and the steady migration of workloads to public and hybrid clouds are steering procurement budgets toward cloud-delivered security controls. Organizations replacing appliance-centric defenses with converged Security Service Edge platforms find that the pay-as-you-go model keeps protection levels aligned with actual traffic volumes, a decisive advantage as edge locations proliferate. Demand accelerates further when remote-work policies and the proliferation of cloud-native applications bring identity, device, and API traffic under one policy framework. The SECaaS market now benefits from AI-infused analytics that shorten dwell time and provide full-stack observability, turning threat intelligence into automated, closed-loop response.

Global SECaaS Market Trends and Insights

Surging Cloud Adoption among SMEs and Enterprises

Growing cloud budgets channel directly into the SECaaS market as firms retire perimeter-centric technologies in favor of identity-first defenses. Public-cloud services in India are forecast to exceed USD 24.2 billion by 2028, with security services advancing the quickest at a 19% CAGR. Small and mid-size businesses gain enterprise-grade protection without dedicated SOC investments, accelerating vendor pipelines for multi-tenant platforms. Financial institutions illustrate the shift: 98% already consume at least one class of cloud service, and most now extend regulated workloads to third-party clouds under tightly governed access policies. Each new workload moved to the cloud automatically expands the attach rate for SECaaS subscriptions, creating a compounding revenue effect across the vendor landscape.

Rising Sophistication of Cyber Threats

Adversaries now wield AI-generated phishing, autonomous malware, and large-scale credential-stuffing campaigns that overwhelm signature-based tools. Banks have responded by embedding machine-learning analytics inside core SOC workflows, dedicating a growing share of multi-year cyber budgets to cloud-native threat detection engines. Healthcare providers, facing a 256% spike in hacking-related breaches, now stipulate SOC 2 and HIPAA alignment as entry requirements for any third-party service. The SECaaS market offers autonomy at scale: threat-intelligence feeds are centralized, detection models are continuously retrained, and automated response actions are orchestrated across global points of presence in seconds.

Data-Residency and Sovereignty Concerns

Cross-border data-flow restrictions challenge uniform cloud adoption. Europe's GDPR and impending Digital Operational Resilience Act compel many financial institutions to maintain customer data within regional boundaries, limiting the choice of global cloud locations. Multi-cloud strategies appear attractive, yet variations in sovereignty controls create fragmented security architectures that duplicate cost. While emerging sovereign-cloud offerings promise localized processing, enterprises remain cautious about potential vendor lock-in.

Other drivers and restraints analyzed in the detailed report include:

- Shift to Remote-Work and BYOD Environments

- Stringent Global Data-Protection Regulations

- Multi-Vendor Subscription-Management Complexity

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Identity-and-Access Management remains the anchor of the SECaaS market, contributing 24.6% of 2024 revenue as cloud-first architectures elevate identity to the default control plane. The segment's enduring relevance reflects tighter least-privilege mandates and the explosion of third-party developer accounts. Advanced IAM suites now extend beyond workforce SSO to govern non-human identities generated by container orchestrators, elevating license counts and average revenue per user. Less visible yet faster moving, the Cloud Access Security Broker segment is growing at a 19.0% CAGR, fueled by the need to discover unsanctioned SaaS and enforce data-loss-prevention rules directly in SaaS-to-SaaS traffic. Combined, these solution pillars underpin the transition toward unified Security Service Edge offerings, where in-line inspection, access control, and data classification co-reside on a global edge fabric. Secure Email Gateway and Secure Web Gateway functions are migrating into these converged stacks, while next-generation SIEM refactors ingestion pipelines to exploit hyperscaler object-storage, thus slashing per-terabyte economics and removing deployment friction.

Second-generation vulnerability-management tools, embedded directly into CI/CD pipelines, close feedback loops between code, build, and runtime. This segue ties security posture tightly to developer workflows and allies the SECaaS market with the broader Platform Engineering movement. Vendors now package pre-approved IaC templates, policy-as-code libraries, and pipeline plugins so that risk visibility becomes intrinsic rather than bolted-on. The most effective sales narratives pivot on measurable MTTD reductions, dashboard-driven compliance, and the demonstrable ROI of consolidating five point solutions into one contract.

Public-cloud deployments represented 59.8% of the 2024 SECaaS market as organizations capitalized on turnkey global points of presence and elastic scale. Nevertheless, hybrid-cloud adoption is posting a 19.8% CAGR as regulated entities weigh data-sovereignty mandates against latency and performance criteria. Enterprises now commonly place identity brokers and policy engines in public cloud while running inline decryption nodes on customer-managed infrastructure for sensitive workloads. Such architectural pluralism requires orchestration layers that can propagate policy once and enforce everywhere-capabilities that have become a differentiator in vendor bake-offs.

Private-cloud SECaaS instances persist for defense and critical-infrastructure operators who cannot expose traffic metadata to shared environments. Emerging industry blueprints allow controlled synchronization of indicators of compromise across trust domains without violating data-residency rules, an approach pioneered by industrial-control vendors working with national CERTs. Over the forecast horizon, multi-cloud policy automation will become table stakes, catalyzing alliances between cloud platforms and security vendors aimed at streamlining identity federation, key management, and telemetry normalization.

The SECaaS Market Report is Segmented by Solution (Identity and Access Management (IAM), Secure Email Gateway, and More), Deployment Model (Public Cloud, Private Cloud, and Hybrid Cloud), Organization Size (Large Enterprises and Small and Medium Enterprises (SMEs)), End-User Industry (BFSI, IT and Telecom, Healthcare and Life Sciences, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America retained 37.1% of global revenue in 2024, reflecting its concentration of hyperscalers, cybersecurity innovators, and early-adopter enterprises. Federal guidance from CISA urging the sunset of legacy VPN tunnels in favor of zero-trust, cloud-native access further cements demand. Financial institutions now mandate Security Service Edge controls during third-party due-diligence reviews, reinforcing network effects across supply chains. Canada and Mexico ride this momentum, integrating regional data-protection statutes with cross-border data flows to spur platform expansion.

Asia-Pacific is advancing at a 19.4% CAGR to 2030 as cloud-migration roadmaps underpin national digital-economy targets. India's public-cloud revenues already rank among the world's fastest-growing, and Australia's IRAP framework has opened government procurement channels for certified providers. Japan's telecom operators spearhead 5G edge rollouts, prompting industrial clients to pre-provision inline inspection to remote factories. Localized data regulations are diverse, but providers that can demonstrate consistent, region-aware encryption-key management gain a decisive bidding advantage.

Europe maintains robust demand, driven by GDPR and the emerging Digital Operational Resilience Act that obliges real-time control validation for financial entities. Germany and the United Kingdom lead investments in converged platforms that unify cloud access, email security, and data-loss prevention. France and Italy accelerate procurement through national cyber-resilience plans that allocate co-funding for SME adoption. Elsewhere, South America and the Middle East and Africa are earlier in their cloud journeys yet rapidly expanding internet backbones and regulatory frameworks, setting the stage for elevated SECaaS penetration rates as economic conditions stabilize.

- Cisco Systems

- Zscaler

- Palo Alto Networks

- Microsoft

- Trend Micro

- Barracuda Networks

- IBM

- Proofpoint

- Sophos

- Forcepoint

- McAfee

- Symantec (Broadcom)

- Qualys

- Check Point Software

- Fortinet

- Cloudflare

- Okta

- Akamai

- Amazon Web Services

- Google Cloud

- CrowdStrike

- Rapid7

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surging cloud adoption among SMEs and enterprises

- 4.2.2 Rising sophistication of cyber threats

- 4.2.3 Shift to remote-work and BYOD environments

- 4.2.4 Stringent global data-protection regulations

- 4.2.5 API-driven "security-as-code" demand in DevSecOps

- 4.2.6 Rapid rollout of zero-trust Security Service Edge

- 4.3 Market Restraints

- 4.3.1 Data-residency and sovereignty concerns

- 4.3.2 Multi-vendor subscription-management complexity

- 4.3.3 Latency-sensitive workloads bypassing inline cloud security

- 4.3.4 Lack of usage-based billing standards

- 4.4 Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Investment Analysis

- 4.9 Assessment of the Impact of Macroeconomic Trends on the Market

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Solution

- 5.1.1 Identity and Access Management (IAM)

- 5.1.2 Secure Email Gateway

- 5.1.3 Secure Web Gateway

- 5.1.4 Cloud Access Security Broker (CASB)

- 5.1.5 Security Information and Event Management (SIEM)

- 5.1.6 Vulnerability Management

- 5.1.7 Other Solutions

- 5.2 By Deployment Model

- 5.2.1 Public Cloud

- 5.2.2 Private Cloud

- 5.2.3 Hybrid Cloud

- 5.3 By Organization Size

- 5.3.1 Large Enterprises

- 5.3.2 Small and Medium Enterprises (SMEs)

- 5.4 By End-User Industry

- 5.4.1 BFSI

- 5.4.2 IT and Telecom

- 5.4.3 Healthcare and Life Sciences

- 5.4.4 Government and Defense

- 5.4.5 Retail and E-commerce

- 5.4.6 Manufacturing

- 5.4.7 Others

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 South Korea

- 5.5.3.5 Australia

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Argentina

- 5.5.4.3 Rest of South America

- 5.5.5 Middle East and Africa

- 5.5.5.1 Middle East

- 5.5.5.1.1 Saudi Arabia

- 5.5.5.1.2 United Arab Emirates

- 5.5.5.1.3 Turkey

- 5.5.5.1.4 Rest of Middle East

- 5.5.5.2 Africa

- 5.5.5.2.1 South Africa

- 5.5.5.2.2 Egypt

- 5.5.5.2.3 Nigeria

- 5.5.5.2.4 Rest of Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global-level Overview, Market-level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Cisco Systems

- 6.4.2 Zscaler

- 6.4.3 Palo Alto Networks

- 6.4.4 Microsoft

- 6.4.5 Trend Micro

- 6.4.6 Barracuda Networks

- 6.4.7 IBM

- 6.4.8 Proofpoint

- 6.4.9 Sophos

- 6.4.10 Forcepoint

- 6.4.11 McAfee

- 6.4.12 Symantec (Broadcom)

- 6.4.13 Qualys

- 6.4.14 Check Point Software

- 6.4.15 Fortinet

- 6.4.16 Cloudflare

- 6.4.17 Okta

- 6.4.18 Akamai

- 6.4.19 Amazon Web Services

- 6.4.20 Google Cloud

- 6.4.21 CrowdStrike

- 6.4.22 Rapid7

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment