|

시장보고서

상품코드

1850013

분체 코팅 : 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Powder Coatings - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

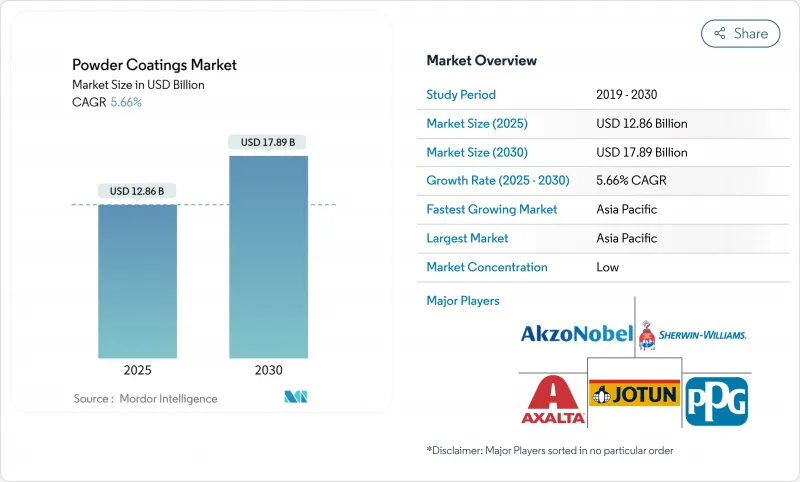

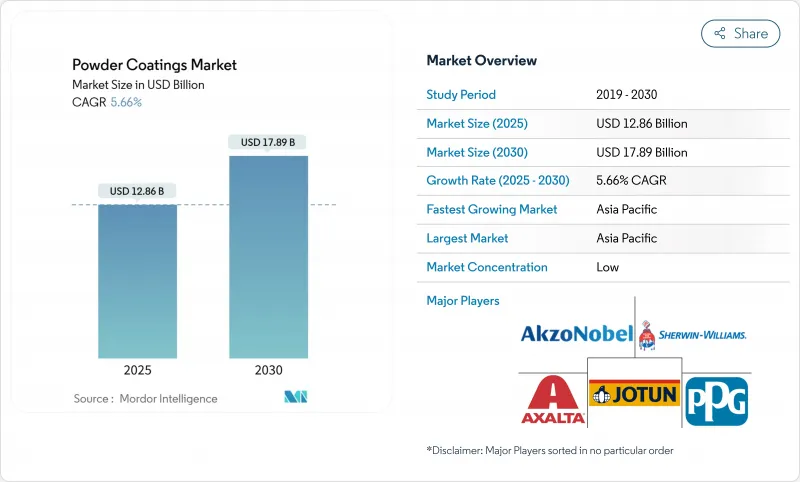

분체 코팅 시장 규모는 2025년에 128억 6,000만 달러로 추정되고, 예측 기간(2025-2030년)의 CAGR은 5.66%를 나타내, 2030년에는 178억 9,000만 달러에 달할 것으로 예상됩니다.

이 기술은 생산 폐기물을 최소화하면서 VOC 규제 강화를 준수하는 무용제 싱글 코트 마감재를 제공하므로 수요가 증가하고 있습니다. 아시아태평양의 왕성한 산업 활동, 열에 약한 기재에의 저온 케미스트리의 채용 가속, 공급 체인의 현지화를 목표로 하는 OEM의 대처 등이 분체 코팅 시장을 지지하는 폭넓은 동향이 되고 있습니다. 폴리에스터 수지, 저 베이크 처방 및 박막 시스템은 기존의 금속 부품에 그치지 않고 최종 용도 범위를 넓히는 새로운 성능 기준을 설정합니다. 원재료의 변동이나 초박막의 용도 제한이 기세를 약화시키고 있는 것, 효율 향상과 탄소 삭감 의무에 힘입어, 전체적인 상승 기조는 견지되고 있습니다.

세계의 분체 코팅 시장 동향과 인사이트

엄격한 VOC 배출 규제가 코팅 기술을 변경

분체 코팅는 VOC를 거의 배출하지 않고 비용이 많이 드는 용매 회수 공정을 생략할 수 있기 때문에 규제 당국으로부터 가장 저공해의 산업용 마감제로 간주되고 있습니다. 자동차 라이프사이클 연구에 따르면 분체 코팅은 액체 코팅에 비해 자동차당 23.40kg의 CO2와 1.47kg의 VOC를 줄이고 OEM의 탈탄소화 로드맵에 공명하는 측정 가능한 지속가능성 배당을 창출하고 있습니다. 유럽의 녹색 거래 및 미국 EPA의 국가 배출 기준 업데이트는 솔벤트 기반 프라이밍 페인트의 교체를 촉진하기 위해 페인팅 업체에 근무하고 있습니다. 주요 제제 제조업체는 미래의 금지를 예상하는 TGIC 프리 및 크롬 프리 제품을 출시함으로써 규제 강화를 선점하고 있습니다. 탄소 가격 제도 증가는 다단식 액체 부스보다 분말 라인이 에너지 강도가 낮다는 것을 보여주기 때문에 비즈니스 케이스를 더욱 강화합니다. 그 결과, 분체 코팅 시장의 마무리 라인의 세계적인 설치 능력은 다른 기술보다 빠르게 확대되고 있습니다.

응용 가능성을 넓히는 저 베이크 화학

최근의 획기적인 기술은 120℃ 이하에서 완전 경화가 가능하게 되었고, 기존 스케줄에서는 휨이 발생하고 있던 MDF, 플라스틱, 복합재를 사용할 수 있게 되었습니다. 248°F로 처리되는 선구적인 시스템은 조립 가구, 액자, 장식 패널에 광택이 적고 긁히기 어려운 마무리를 가능하게 합니다. 아시아태평양 가구 산업은 여러 번 덧칠하지 않고 VOC 프리로 선명한 색상으로 마무리 할 수 있기 때문에 큰 혜택을 누리고 있습니다. 또한, 정전 도장된 파우더가 오버스프레이를 회수하여 재이용하고, 패스트 패스 반송을 개선하기 위해, 라인 오퍼레이터는 2자리의 재료 절약을 기록하고 있습니다. 실용적인 투자 회수는 오븐의 셋포인트가 낮기 때문에 에너지 수요가 떨어지면 신속하게 이루어집니다. 세계 공급업체는 경화 시간을 단축하기 위해 수지 화학을 지속적으로 개선하고 있으며, 컨베이어의 속도를 높이고 일일 처리 능력을 향상시키고 있습니다.

시장 침투를 제한하는 박막 용도의 과제

울트라 매끄러운 25µm 필름은 특히 날카로운 모서리와 오목 부에 균일 한 성막이 어렵습니다. 코팅의 질량이 감소하면 스크래치 내성과 불투명도가 떨어지므로 박막 파우더는 완벽한 표면이 필요한 고급 전자 장치 하우징에 매력적이지 않습니다. 어플리케이터는 더 까다로운 공정 창과 인라인 막 두께계로 지원되지만 복잡한 모양에서는 변동이 남아 있습니다. 스마트폰과 노트북에서는 분무 페인트가 오렌지 껍질 없이 10µm을 쉽게 달성할 수 있기 때문에 액체 페인트의 대체품이 점유율을 유지합니다. 첨단 코로나건과 유동화 호퍼 등 설비의 개수는 자본 지출을 증가시켜 소규모 가공 공장에서의 채용을 늦추고 있습니다. 그럼에도 불구하고 공급업체는 이러한 차이를 줄이기 위해 보다 미세한 입자 크기 분포와 고유한 유동제를 설계합니다.

부문 분석

폴리에스터 조성물은 2024년의 분체 코팅 시장 점유율의 38%를 차지해 건축, 가전, 자동차의 트림 라인에서 다른 추종을 허락하지 않는 존재가 되었습니다. CAGR 6.25%는 분체 코팅 시장의 폴리에스터 부분이 수지의 내후성 견고성과 폭넓은 컬러 팔레트를 반영하고 있음을 의미합니다. TGIC 프리나 저베이크 가교제로의 개질은 에코 디자인 지령에 합치하고, 안료의 진보는 해안 기후에서도 광택을 유지합니다. 분체 코팅 시장은 폴리 에스테르 블렌드가 경화 속도를 희생하지 않고 스테인 릴리스를 향상시키는 기능성 나노 입자를 통합하기 때문에 계속 혜택을 누릴 수 있습니다.

에폭시 파우더는 뛰어난 내화학성으로 인해 개폐 장치 및 파이프 밸브와 같은 실내의 가혹한 환경에서 전략적 지위를 유지합니다. 그러나 자외선에 약하기 때문에 야외 노출이 제한되어 폴리 에스테르에 비해 판매량이 늘지 않습니다. 에폭시와 폴리에스터의 하이브리드는 초킹을 완화하고, 가전제품 선반에 어필을 확대하고, 아시아의 신흥 생산 기지에서 수요 증가를 촉진합니다. 폴리우레탄 파우더는 내약품성과 내마모성이 비용 증가를 정당화하는 프리미엄 틈새를 개척합니다. 코베스트로의 저온 경화는 복합 휠과 탄소섬유 부품을 이 화학제품에 개방합니다. 아크릴, PVC 및 폴리올레핀 솔루션은 낙서 방지 운송 패널 및 식기 세척기 랙과 같은 특수 요구 사항을 충족하며 수지의 다양한 성장을 지원하는 선택의 폭을 보여줍니다.

열경화성 등급은 자외선, 화학제품, 마모에 견딜 수 있는 돌이킬 수 없는 가교 네트워크를 통해 2024년 분체 코팅 시장의 90%를 차지했습니다. 열가소성 플라스틱은 자동차의 휠, 파이프라인, 건물의 외관 등에서 확고한 지위를 구축하고 있기 때문에 생산량이 많고 생산 규모가 크기 때문에 비용 리더십이 확보되고 있습니다. 그러나 열가소성 플라스틱은 중장비 및 장바구니의 프레임에서 특이한 표면의 재용해 및 보수가 가능한 것으로 가공업자에 의해 평가되어 CAGR 6.01%로 상승 경향이 있습니다. 특히 유연하고 내충격성이 있는 표피가 필수적입니다.

기술 혁신은 이러한 변화의 핵심입니다. IFS Puroplaz PE16은 변성 폴리올레핀이 연성을 유지하면서 강철과 같은 접착력을 실현하여 열가소성 플라스틱이 장식용 울타리와 놀이기구의 구조에 사용되는 범위를 넓히고 있음을 입증합니다. 마찬가지로 나일론 기반 파우더는 해상 패스너의 두꺼운 칩 저항성 필름을 지원합니다. 난연성 처방의 개선으로 열가소성 플라스틱은 전기 하우징에 적합하게 되어 기존의 열경화성 플라스틱의 점유율이 저하되었습니다. 열가소성 플라스틱은 고온에서 용융 흐름을 필요로 하기 때문에 경화 에너지는 여전히 높지만, 유도 가열과 적외선 패널에 대한 조사 강화에 의해 2025-2030년의 전개시에는 이 갭을 줄이는 것을 목표로 하고 있습니다.

지역 분석

아시아태평양은 2024년에 세계 수요의 55%를 차지했고, 2030년까지의 CAGR은 5.89%로, 이 기간의 분체 코팅 시장 규모 증가분의 2분의 1 이상에 상당합니다. 중국 건설업 회복, 인도 자본재 생산 가속화, 아세안 백색 가전 조립의 급증은 모두 이 지역의 소비량이 됩니다. 악조노벨의 구와리올 공장은 2024년 9월에 연산 5,166톤을 가동시켜 국내 수요에 대한 신뢰가 지속되고 있음을 보여주었습니다.

북미는 리쇼어링 정책의 혜택을 받습니다. 미국 환경보호청의 엄격한 VOC 상한규제는 공장 업그레이드를 촉진하고 멕시코의 조립통로에서는 USMCA의 함량규제를 충족시키기 위해 섀시 브라켓과 휠림에 파우더를 지정하게 되었습니다. 지역의 배합 담당자는 고용제 실험실의 안전 관리 없이 파우더를 현지에서 배치 처리할 수 있기 때문에 컬러 매치의 턴어라운드가 빠른 것을 강조하고 있습니다.

유럽의 성숙한 장비 기반은 생산량보다 기술 혁신에 중점을 둡니다. 2025년에 채용된 아시아로부터의 에폭시 수지 수입에 대한 잠정적인 안티 덤핑 관세는 EU의 생산자를 가격 변동으로부터 지켜 국내 파우더 제조업체의 원재료 마진을 안정시킵니다. 지속가능성의 과제는 바이오계 수지와 재생가능에너지를 동력으로 하는 경화시스템의 연구개발에 박차를 가하여 지속적인 저탄소화의 리더십을 확보합니다.

중동 및 아프리카 분체 코팅 시장에서는 NEOM, 도하 지하철 연신, UAE 물류 존 등 10억 달러 규모의 거대 프로젝트에 의한 상승이 현저합니다. Al Taiseer Aluminium은 걸프 지역의 압출 마감 부문에서 21%의 점유율을 차지하고 있으며 지역 챔피언이 어떻게 사양 규범을 형성하는지 명확하게 보여줍니다. 라틴아메리카는 절대적인 규모로 아직 작지만, 브라질과 아르헨티나에서의 자동차 투자는 특히 폴리 에스테르의 탑 코트 소비를 점차 밀어 올리고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

목차

제1장 서론

- 조사 전제조건과 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 엄격한 VOC 배출 규제와 탈탄소화 규제에 의해 무용제 코팅이 가속

- 저온 소성 화학약품에 의해 특히 아시아에서 MDF나 열에 약한 기판의 비즈니스 기회 창출

- ASEAN과 인도에서는 FDI 유입에 힘입어 가전제품의 생산이 급증

- 멕시코와 유럽으로의 자동차 생산 회귀로 OEM 수요 증가

- GCC 인프라의 대규모 프로젝트가 건축용 알루미늄 압출 코팅을 추진

- 시장 성장 억제요인

- 분체 도장의 박막화의 어려움

- 복잡한 형상에 대한 UV 경화성 분말의 적합성 한정

- 휘발성 폴리에스터와 에폭시 원료의 가격이 이익률 저하

- 밸류체인 분석

- Porter's Five Forces 분석

- 공급기업의 협상력

- 구매자의 협상력

- 신규 참가업체의 위협

- 대체품의 위협

- 경쟁 기업 간 경쟁 관계

제5장 시장 규모와 성장 예측(금액)

- 수지 유형별

- 에폭시

- 폴리에스터

- 에폭시 폴리에스터

- 폴리우레탄

- 아크릴

- 기타 수지 유형(폴리염화비닐, 폴리올레핀)

- 코팅 유형별

- 열경화성 분체 코팅

- 열가소성 분체 코팅

- 최종 이용 산업별

- 건축 및 장식

- 자동차

- 산업

- 기타(가구 및 가전 등)

- 기질별

- 금속

- MDF 및 목재

- 플라스틱 및 복합재료

- 유리 및 기타 비전도성 기판

- 지역별

- 아시아태평양

- 중국

- 인도

- 일본

- 한국

- 기타 아시아태평양

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 프랑스

- 영국

- 이탈리아

- 기타 유럽

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 중동 및 아프리카

- 사우디아라비아

- 남아프리카

- 기타 중동 및 아프리카

- 아시아태평양

제6장 경쟁 구도

- 시장 집중도

- 전략적 동향

- 시장 점유율 분석

- 기업 프로파일

- Advanced Powder Coatings

- Akzo Nobel NV

- Asian Paints PPG Pvt. Ltd.

- Axalta Coating Systems, LLC

- BASF

- Berger Paints India

- Cardinal

- Hempel A/S

- IFS Coatings

- IGP Pulvertechnik AG

- Jotun

- Kansai Paint Co.,Ltd.

- NATIONAL PAINTS FACTORIES CO. LTD.

- Nippon Paint Holdings Co., Ltd.

- PPG Industries, Inc.

- RPM International Inc.(TCI Powder Coatings)

- SAK Coat

- Teknos Group

- The Sherwin-Williams Company

- TIGER Coatings GmbH & Co. KG

제7장 시장 기회와 향후 전망

KTH 25.11.04The Powder Coatings Market size is estimated at USD 12.86 billion in 2025, and is expected to reach USD 17.89 billion by 2030, at a CAGR of 5.66% during the forecast period (2025-2030).

Demand is rising as the technology offers solvent-free, single-coat finishes that comply with tightening VOC rules while minimizing production waste. Strong industrial activity across Asia-Pacific, accelerating adoption of low-temperature chemistries for heat-sensitive substrates, and OEM efforts to localize supply chains are broad trends sustaining the powder coatings market. Polyester resins, low-bake formulations, and thin-film systems are setting new performance benchmarks that widen end-use scope beyond traditional metal parts. Although raw-material volatility and application limits on very thin films temper momentum, the overall trajectory remains firmly upward, supported by efficiency gains and carbon-reduction mandates.

Global Powder Coatings Market Trends and Insights

Stringent VOC-Emission Regulations Transforming Coating Technologies

Regulatory agencies now view powder coatings as the lowest-polluting industrial finish because the process emits negligible VOCs and eliminates costly solvent recovery steps. Automotive life-cycle studies show powder conversion cuts 23.40 kg CO2 and 1.47 kg VOCs per vehicle versus liquid paint, creating a measurable sustainability dividend that resonates with OEM decarbonization roadmaps. Europe's Green Deal and the United States EPA's updated National Emission Standards are pushing coaters to accelerate replacement of solventborne primers. Leading formulators have pre-empted tighter limits by launching TGIC-free and chrome-free chemistries that anticipate future bans. Rising carbon-pricing schemes further strengthen the business case, as powder lines demonstrate lower energy intensity than multi-stage liquid booths. As a result, global installed capacity for powder coatings market finishing lines is expanding faster than for any other technology.

Low-Bake Chemistries Expanding Application Possibilities

Recent breakthroughs allow full cure below 120°C, unlocking MDF, plastics, and composites that once warped under conventional schedules. Pioneering systems processed at 248°F enable low-gloss, scratch-resistant finishes on assembled furniture, picture frames, and decorative panels. The Asia-Pacific furniture cluster is the immediate beneficiary, as producers gain a VOC-free route to vibrant colors without multiple topcoats. Line operators also record double-digit material savings because an electrostatically applied powder recovers overspray for reuse, improving first-pass transfer. Practical payback occurs quickly when energy demand falls, given the lower oven set-points. Global suppliers continue to refine resin chemistry to shorten curing time, letting conveyor speeds rise and daily throughput climb.

Thin Film Application Challenges Limiting Market Penetration

Ultra-smooth, 25 µm films remain difficult to deposit uniformly, especially on sharp edges and recessed cavities. Reduced coating mass can lower scratch resistance and opacity, making thin-film powders less attractive for premium electronics housings that demand flawless surfaces. Applicators compensate with tighter process windows and in-line thickness gauges, yet variability persists on intricate geometries. Liquid alternatives keep share in smartphones and laptops because atomized paints easily hit 10 µm without orange peel. Equipment retrofits-such as advanced corona guns and fluidized hoppers-raise capital outlays, slowing adoption among small job shops. Nonetheless, suppliers are engineering finer grind distributions and proprietary flow agents to close the gap.

Other drivers and restraints analyzed in the detailed report include:

- Domestic Appliance Manufacturing Surge in Asia

- Automotive Production Reshoring Driving Regional Demand

- UV-Curable Powder Limitations Constraining Growth

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Polyester compositions account for 38% of the powder coatings market share in 2024, giving the group an unrivaled footprint across architectural, appliance, and automotive trim lines. Their 6.25% CAGR forecast means the polyester portion of the powder coatings market reflects the resin's weather fastness and wide color palette. Reformulation to TGIC-free and low-bake cross-linkers aligns with eco-design directives, while pigmentation advances retain gloss even in coastal climates. The powder coatings market continues to benefit as polyester blends incorporate functional nanoparticles that improve stain release without compromising cure speed.

Epoxy powder retains a strategic position in heavy-duty indoor settings such as switchgear and pipe valves because of superior chemical resistance. Yet UV fragility limits outdoor exposure, capping volume growth versus polyester. Epoxy-polyester hybrids mitigate chalking and expand shelf appeal for home appliances, driving incremental demand in emerging Asian production hubs. Polyurethane powders carve out premium niches where chemical and abrasion resistance justify added cost; Covestro's low-temperature cures open composite wheels and carbon fiber parts to this chemistry. Acrylic, PVC, and polyolefin solutions address specialized requirements such as anti-graffiti transit panels or dishwasher racks, illustrating the breadth of options sustaining resin-diversified growth.

Thermoset grades dominated 90% of the powder coatings market in 2024, thanks to irreversible cross-linked networks that withstand UV, chemicals, and abrasion. Their entrenched position in automotive wheels, pipelines, and building facades keeps volume high, and production scale ensures cost leadership. However, thermoplastics are trending upward at 6.01% CAGR as processors value the ability to remelt or repair surfaces, a feature prized in heavy machinery and shopping-cart frames. Over the forecast horizon, the thermoplastic slice of the powder coatings market size may double, particularly where flexible, impact-resistant skins are essential.

Innovation is central to this shift. IFS Puroplaz PE16 demonstrates how modified polyolefins achieve steel-like adhesion while preserving ductility, broadening thermoplastic reach into decorative fencing and playground structures. Similarly, nylon-based powders support thick, chip-resistant films on offshore fasteners. Improved flame-retardant formulations make thermoplastics compatible with electrical enclosures, eroding legacy thermoset share. While curing energy remains higher because thermoplastics require melt flow at elevated temperatures, intensified research on inductive heating and infrared panels aims to narrow that gap during 2025-2030 deployments.

The Powder Coatings Market Report Segments the Industry by Resin Type (Epoxy, Polyester, and More), Coating Type (Thermoset Powder Coatings and Thermoplastic Powder Coatings), End-Use Industry (Architecture and Decorative, Automotive, and More), Substrate (Metal, Plastics and Composites, and More), and Geography (Asia Pacific, North America, Europe, and More). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific retained 55% of global demand in 2024 and is on track for a 5.89% CAGR to 2030, translating into more than one-half of incremental powder coatings market size growth over the period. China's construction rebound, India's accelerating capital goods output, and ASEAN's surge in white-goods assembly all feed regional consumption. Multinationals continue to add local capacity; AkzoNobel's Gwalior plant brought 5,166 t/y online in September 2024, signaling sustained confidence in domestic appetite.

North America benefits from reshoring policies. The United States Environmental Protection Agency's strict VOC cap catalyzes plant upgrades, and Mexico's assembly corridor now specifies powder on chassis brackets and wheel rims to meet USMCA content rules. Regional formulators highlight faster color-match turnaround because powders can be batched locally without high-solvent lab safety controls.

Europe's mature installation base focuses on innovation rather than volume. The provisional anti-dumping duty on Asian epoxy resin imports adopted in 2025 shields EU producers from price swings, stabilizing raw-material margins for domestic powder makers. Sustainability agendas spur R&D into bio-based resins and renewable-energy-powered cure systems, ensuring continued low-carbon leadership.

The Middle East and Africa powder coatings market sees pronounced upside from billion-dollar megaprojects such as NEOM, Doha Metro extensions, and UAE logistics zones. Al Taiseer Aluminium commands 21% of the Gulf extrusion finishing segment, underscoring how regional champions shape specification norms. Latin America remains smaller in absolute terms, yet automotive investments in Brazil and Argentina gradually lift consumption, particularly of polyester topcoats.

- Advanced Powder Coatings

- Akzo Nobel N.V.

- Asian Paints PPG Pvt. Ltd.

- Axalta Coating Systems, LLC

- BASF

- Berger Paints India

- Cardinal

- Hempel A/S

- IFS Coatings

- IGP Pulvertechnik AG

- Jotun

- Kansai Paint Co.,Ltd.

- NATIONAL PAINTS FACTORIES CO. LTD.

- Nippon Paint Holdings Co., Ltd.

- PPG Industries, Inc.

- RPM International Inc. (TCI Powder Coatings)

- SAK Coat

- Teknos Group

- The Sherwin-Williams Company

- TIGER Coatings GmbH & Co. KG

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Stringent VOC-emission and decarbonization regulations accelerating solvent-free coatings

- 4.2.2 Low-bake chemistries opening MDF and heat-sensitive substrate opportunities, especially in Asia

- 4.2.3 Surging domestic appliance output in ASEAN and India backed by FDI inflows

- 4.2.4 Re-shoring of automotive production in Mexico and Europe boosting OEM demand

- 4.2.5 GCC infrastructure megaprojects driving architectural aluminium extrusion coatings

- 4.3 Market Restraints

- 4.3.1 Difficulty in Obtaining Thin Film of Powder Coating

- 4.3.2 Limited UV-curable powder compatibility with complex geometries

- 4.3.3 Volatile polyester and epoxy feedstock pricing eroding margins

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Intensity of Competitive Rivalry

5 Market Size and Growth Forecasts (Value )

- 5.1 By Resin Type

- 5.1.1 Epoxy

- 5.1.2 Polyester

- 5.1.3 Epoxy-Polyester

- 5.1.4 Polyurethane

- 5.1.5 Acrylic

- 5.1.6 Other Resin Types (Polyvinyl Chloride, Polyolefins)

- 5.2 By Coating Type

- 5.2.1 Thermoset Powder Coatings

- 5.2.2 Thermoplastic Powder Coatings

- 5.3 By End-use Industry

- 5.3.1 Architecture and Decorative

- 5.3.2 Automotive

- 5.3.3 Industrial

- 5.3.4 Others (Furniture, Appliances, etc.)

- 5.4 By Substrate

- 5.4.1 Metal

- 5.4.2 MDF and Wood

- 5.4.3 Plastics and Composites

- 5.4.4 Glass and Other Non-conductive Substrates

- 5.5 By Geography

- 5.5.1 Asia-Pacific

- 5.5.1.1 China

- 5.5.1.2 India

- 5.5.1.3 Japan

- 5.5.1.4 South Korea

- 5.5.1.5 Rest of Asia-Pacific

- 5.5.2 North America

- 5.5.2.1 United States

- 5.5.2.2 Canada

- 5.5.2.3 Mexico

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 France

- 5.5.3.3 United Kingdom

- 5.5.3.4 Italy

- 5.5.3.5 Rest of Europe

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Argentina

- 5.5.4.3 Rest of South America

- 5.5.5 Middle East and Africa

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 South Africa

- 5.5.5.3 Rest of Middle East and Africa

- 5.5.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Advanced Powder Coatings

- 6.4.2 Akzo Nobel N.V.

- 6.4.3 Asian Paints PPG Pvt. Ltd.

- 6.4.4 Axalta Coating Systems, LLC

- 6.4.5 BASF

- 6.4.6 Berger Paints India

- 6.4.7 Cardinal

- 6.4.8 Hempel A/S

- 6.4.9 IFS Coatings

- 6.4.10 IGP Pulvertechnik AG

- 6.4.11 Jotun

- 6.4.12 Kansai Paint Co.,Ltd.

- 6.4.13 NATIONAL PAINTS FACTORIES CO. LTD.

- 6.4.14 Nippon Paint Holdings Co., Ltd.

- 6.4.15 PPG Industries, Inc.

- 6.4.16 RPM International Inc. (TCI Powder Coatings)

- 6.4.17 SAK Coat

- 6.4.18 Teknos Group

- 6.4.19 The Sherwin-Williams Company

- 6.4.20 TIGER Coatings GmbH & Co. KG

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-need Assessment