|

시장보고서

상품코드

1850014

백신 면역 증강제 : 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Vaccine Adjuvants - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

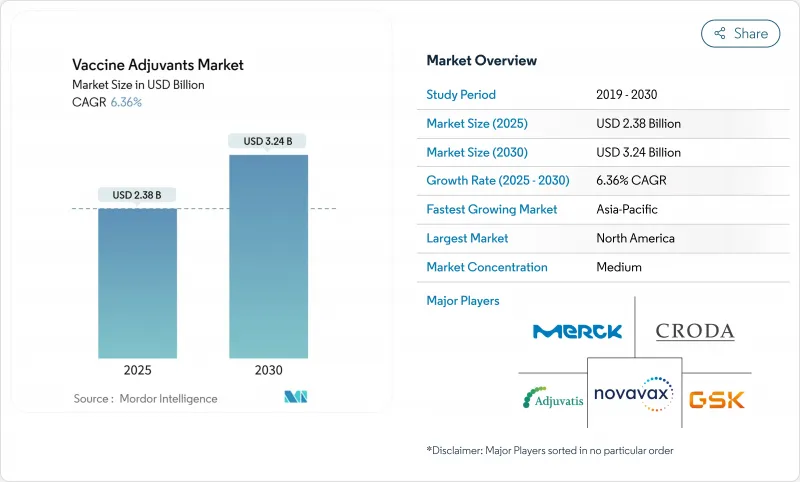

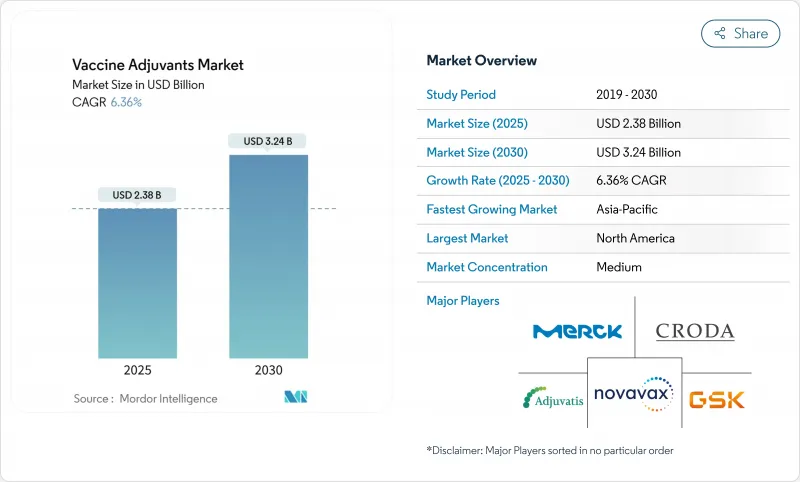

백신 면역 증강제 시장은 2025년에 23억 8,000만 달러로 평가되었고, 2030년에 32억 4,000만 달러로 성장할 전망입니다.

이러한 지속적인 확장은 면역 반응 증폭, 새로운 항원 형식 구현, 내열성 제형 지원을 위해 정교한 보조제 기술이 필요한 차세대 면역 플랫폼으로의 제약 업계 전환을 반영합니다. 팬데믹 대비를 위한 정부의 약속은 예측 가능한 구매량을 추가하는 한편, AI 기반 설계는 제형 개발 주기를 단축하고 콜드체인 의존도를 낮춰 유통 비용을 절감하고 글로벌 접근성을 확대합니다. mRNA, 자가 증폭 RNA, 바이러스 유사 입자(VLP) 백신에 대한 연구 강화는 정제되거나 합성된 항원의 낮은 본질적 면역원성을 상쇄하기 위해 강력한 보조제에 의존하는 이러한 플랫폼으로 인해 수요를 더욱 끌어올립니다. 사포닌 및 트리테르페노이드 원료의 공급 안정성과 STING 작용제와 같은 새로운 경로의 규제 명확성은 여전히 주목할 점이지만, 바이오테크 혁신에 대한 지속적인 자본 유입은 백신 면역 증강제 시장의 장기적인 매력에 대한 신뢰를 나타냅니다.

세계의 백신 면역 증강제 시장 동향 및 인사이트

확대되는 정부 예방접종 권고

국가별 백신 접종 일정이 청소년, 성인, 노년층으로 확대되면서 보조제 제품의 대상 기반이 꾸준히 넓어지고 있습니다. 2024년 팬데믹 비축용 보조제가 포함된 H5N1 백신의 FDA 승인 및 65세 이상 성인을 위한 MF59 강화 인플루엔자 제형에 대한 EMA의 권고는 제조업체에 안정적인 물량 구매를 보장하는 정책 추진력을 보여줍니다. 공중보건 당국은 또한 입원률 감소와 연계된 비용 절감 효과를 강조하여 보조제 함유 제품에 대한 예산 배정을 강화하고 있습니다. 이러한 보건 경제학과 조달 정책의 조화는 백신 면역 증강제 시장에 안정적인 수요 기반을 형성합니다.

신종 인수공통감염병에 대한 미충족 백신 수요

기후 변화에 따른 서식지 이동, 도시와 야생동물 간 접촉 증가, 글로벌 무역 확대는 감염 확산 사건을 촉진하며, 신속한 면역원성을 위해 강력한 보조제가 필요한 신속 작용 백신에 대한 수요를 높입니다. 자기 증폭 RNA 후보물질은 최적화된 보조제와 결합 시 항원 용량을 최대 40배까지 감소시켜 긴급 대량 생산을 가능케 합니다. WHO의 ‘질병 X(Disease X)’ 프레임워크는 광범위 스펙트럼 보조제 플랫폼을 우선 기술로 명시하며, 다자간 자금 지원을 통해 단기 구매 확실성을 높이고 있습니다.

지역적 및 전신적 독성 우려

시판 후 모니터링를 통해 희귀 염증 사건이 점차 더 많이 발견되면서 규제 당국이 데이터 요구 사항을 강화하고 있습니다. 예를 들어, B급 CpG 구조체는 단백질 항원을 불안정하게 하고 표적 외 반응성을 높일 수 있어 독성학 패널과 약물모니터링 범위를 확대하게 합니다. 강화된 안전 기준은 개발 기간을 연장하고 자본 수요를 증가시켜 백신 면역 증강제 시장의 단기 성장을 억제합니다.

부문 분석

사포닌 및 트리테르페노이드 시스템은 2024년 백신 면역 증강제 시장 규모의 26.78%를 차지했으며, 대상포진, 말라리아, 결핵 프로그램에서 QS-21 및 AS01 적용이 이를 주도했습니다. 체액성 및 세포성 면역의 이중 유도가 수요를 유지하지만, 천연 원료 추출 위험과 지속가능성 요구 증가로 인해 반합성 유사체에 대한 투자가 촉진되고 있습니다. 바이러스 유사 입자(VLP)는 기반이 작지만, 규모 확대를 단순화하는 BacFreets 오염 감소 기술에 힘입어 2030년까지 연평균 7.12% 성장률을 보일 전망입니다.

제조사들은 사포닌 수확 변동성 완화를 위해 공급원 다각화를 검토하는 한편, 합성생물학 연구실에서는 다가 항원과 고유 패턴인식 모티프를 동시에 발현하는 VLP 스캐폴드를 개선하여 별도의 보조제 성분을 대체할 가능성을 모색 중입니다. 알루미늄염, 유제, 리포좀 제형은 소아 정기 예방접종 일정의 핵심으로 자리매김하고 있는 반면, 탄수화물 및 박테리아 유래 TLR 작용제는 맞춤형 면역 편극화가 필요한 틈새 적응증을 해결합니다. 기존 기술과 혁신적 기술의 공존은 백신 면역 증강제 시장이 이질적인 제품 환경을 유지하도록 보장합니다.

2024년 백신 면역 증강제 시장 점유율의 47.89%를 차지한 활성 면역 자극제는 다이나백스의 CpG 1018 및 GSK의 MPL과 같은 기전적으로 정의된 제제에 기반합니다. 이러한 경로에 대한 규제 당국의 친숙도는 심사 기간을 단축시키고 다중 항원에 걸친 플랫폼 승인을 촉진합니다. 지질 나노입자 및 고분자 운반체를 포괄하는 운반체 보조제는 개발사들이 통합 전달-자극 솔루션을 요구함에 따라 2030년까지 연평균 7.04% 성장할 것으로 전망됩니다.

백신 면역 증강제 시장은 항원과 면역 증강제를 함께 캡슐화하면서도 온도 변동 시에도 콜로이드 안정성을 유지하는 운반체를 점점 더 중요하게 평가하고 있습니다. 최근 개발된 망간-지질 하이브리드 입자는 알루미늄 비교군 대비 수두-대상포진 바이러스에 대한 CD8+ 반응이 더 강력함을 입증하여, 대체 물결을 주도하는 기능적 이점을 부각시켰습니다. 운반체 보조제는 점막 또는 서방형 적용 분야에서 여전히 중요성을 유지하며, 각 방식이 광범위한 백신 면역 증강제 시장 내에서 명확한 기회 영역을 확보하도록 합니다.

지역 분석

북미는 성숙한 제조 역량, 공중보건 조달 예산, 플랫폼 검토를 간소화하는 FDA 규제 선례에 힘입어 2024년 41.12% 점유율로 선도적 위치를 유지했습니다. 워프 스피드 작전 및 후속 계획 하에서 연방 자금 지원으로 mRNA 최적화 보조제 시스템의 규모 확대가 이루어지며 지역적 우위를 더욱 공고히 하고 있습니다. 보스턴, 샌프란시스코, 토론토에 집적된 학술 센터들은 상업적 포트폴리오로 이어지는 전환 파이프라인을 구축하여 백신 면역 증강제 시장이 해당 지역에 계속 기반을 두도록 보장합니다.

아시아태평양 지역은 중국의 바이오의약품 생산 능력 증대, 인도의 계약 제조 규모의 경제, 아세안(ASEAN)의 예방접종 프로그램 확장에 힘입어 2030년까지 연평균 7.45%의 성장률을 기록할 것으로 전망됩니다. 열안정성 보조제 연구개발에 대한 정부 보조금은 열대 지역의 콜드체인 제약을 해결하는 한편, 일본의 화학 산업 강점은 지질 나노입자 혁신을 가속화합니다. 아세안 백신 규제 메커니즘(VRM) 하의 지역 규제 조화는 승인 중복을 줄여 지역 개발사의 시장 출시 속도를 개선하고 아시아태평양 지역 백신 면역 증강제 시장을 성장시키고 있습니다.

유럽은 EMA의 적응형 승인 경로 프레임워크가 우선순위 보조제 플랫폼에 대한 조건부 허가를 지원함에 따라 꾸준한 한 자릿수 중반 성장세를 유지하고 있습니다. EU 공동 조달 협정 하의 국경 간 조달 메커니즘은 수요를 집약하여 공급업체에 예측 가능한 물량을 제공함과 동시에 마진 규율을 유지하는 가격 협상을 가능하게 합니다. 독일과 네덜란드의 화학 전문 인프라가 고순도 부형제 공급을 지속하여 다른 지역으로의 보조제 중간체 수출을 지원합니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

목차

제1장 서론

- 조사의 전제조건과 시장의 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 정부의 예방접종 권장 확대

- 신종 인수공통전염병에 대한 미충족 백신 수요

- 재조합 및 합성 항원의 채택 증가

- 신규 면역 증강제에 대한 MRNA 플랫폼 수요 가속

- 미생물 유래 TLR 효능제 파이프라인의 확대

- AI 설계 나노-알루미늄 제형으로 냉장 유통 불필요

- 시장 성장 억제요인

- 국소 및 전신 독성 우려

- 높은 신약 개발 및 전임상 스크리닝 비용

- 스쿠알렌 및 QS-21 공급망의 규모 확대 과제

- 신종 STING 작용제에 대한 규제 불확실성

- 규제 상황

- Porter's Five Forces 분석

- 신규 참가업체의 위협

- 구매자의 협상력

- 공급기업의 협상력

- 대체품의 위협

- 라이벌 관계의 격렬

제5장 시장 규모와 성장 예측

- 제품 유형별

- 무기염 보조제

- 사포닌 및 트리테르페노이드

- 에멀젼 기반

- 리포솜과 빌로솜

- 탄수화물과 다당류

- 세균 유래 TLR 작용제

- 바이러스 유사 입자

- 기타 제품 유형

- 사용 유형별

- 활성 면역 자극제

- 운반체

- 면역 증강제

- 질환 유형별

- 감염증

- 암

- 기타

- 용도별

- 연구 용도

- 상업 용도

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 기타 유럽

- 아시아태평양

- 중국

- 일본

- 인도

- 호주

- 한국

- 기타 아시아태평양

- 중동 및 아프리카

- GCC

- 남아프리카

- 기타 중동 및 아프리카

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 북미

제6장 경쟁 구도

- 시장 집중도

- 시장 점유율 분석

- 기업 프로파일

- GlaxoSmithKline plc

- Seppic(Air Liquide)

- Dynavax Technologies Corp.

- Croda International plc(Croda Pharma)

- CSL Limited(BioCSL, Seqirus)

- Merck KGaA(Sigma-Aldrich)

- Novavax Inc.

- Thermo Fisher Scientific Inc.

- Agenus Inc.

- Adjuvatis SAS

- InvivoGen

- SPI Pharma(ABF plc)

- Vertellus

- Pacific GeneTech Ltd.

- OZ Biosciences

- Adjuvance Technologies Inc.

- Valneva SE

- Bavarian Nordic A/S

- Pfizer Inc.

- AstraZeneca plc

- Avanti Polar Lipids(Croda)

제7장 시장 기회와 장래의 전망

HBR 25.11.14The vaccine adjuvants market stands at USD 2.38 billion in 2025 and is forecast to reach USD 3.24 billion by 2030, advancing at a 6.36% CAGR.

This sustained expansion reflects the pharmaceutical sector's pivot toward next-generation immunization platforms that need sophisticated adjuvant technologies to amplify immune responses, enable novel antigen formats, and support thermostable formulations. Government commitments to pandemic preparedness add predictable purchase volumes, while AI-guided design shortens formulation cycles and reduces cold-chain dependence, lowering distribution costs and widening global access. Intensifying research into mRNA, self-amplifying RNA, and virus-like particle (VLP) vaccines further lifts demand, as these platforms rely on potent adjuvants to offset the low intrinsic immunogenicity of purified or synthetic antigens . Supply security for saponin and triterpenoid inputs and regulatory clarity for novel pathways such as STING agonism remain watchpoints, yet continued capital inflows into biotech innovation signal confidence in the long-term attractiveness of the vaccine adjuvants market.

Global Vaccine Adjuvants Market Trends and Insights

Expanding Government Immunization Recommendations

Broader national vaccine schedules now target adolescents, adults, and the elderly, steadily enlarging the eligible base for adjuvanted products. The 2024 FDA approval of an adjuvanted H5N1 vaccine for pandemic stockpiling and the EMA's recommendation of MF59-enhanced influenza formulations for adults over 65 illustrate policy momentum that rewards manufacturers with reliable volume offtake . Public-health authorities also highlight cost-avoidance benefits tied to reduced hospitalization rates, reinforcing budget allocations for adjuvant-rich products. This alignment between health economics and procurement creates a stable demand floor for the vaccine adjuvants market.

Unmet Vaccine Needs for Emerging Zoonoses

Climate-linked habitat shifts, intensified urban-wildlife interfaces, and global trade facilitate spillover events, heightening demand for fast-acting vaccines that rely on potent adjuvants for rapid immunogenicity. Self-amplifying RNA candidates show antigen-dose reductions of up to 40-fold when paired with optimized adjuvants, enabling emergency surge manufacturing . The WHO's Disease X framework explicitly lists broad-spectrum adjuvant platforms as priority technologies, signaling multi-lateral funding support that lifts near-term purchase certainty.

Local & Systemic Toxicity Concerns

Post-marketing surveillance increasingly detects rare inflammatory events, compelling regulators to tighten data requirements. Class B CpG constructs, for instance, destabilize protein antigens and may heighten off-target reactivity, prompting extended toxicology panels and pharmacovigilance. Heightened safety thresholds elongate timelines and raise capital demands, tempering the vaccine adjuvants market's near-term growth.

Other drivers and restraints analyzed in the detailed report include:

- Rising Adoption of Recombinant & Synthetic Antigens

- Accelerating mRNA-Platform Demand for Novel Adjuvants

- High Discovery & Pre-Clinical Screening Costs

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Saponin and triterpenoid systems controlled 26.78% of the vaccine adjuvants market size in 2024, anchored by QS-21 and AS01 deployments in shingles, malaria, and tuberculosis programs. Their dual induction of humoral and cellular immunity sustains demand, yet natural-source extraction risks and rising sustainability mandates propel investment in semi-synthetic analogs. Virus-like particles, though holding a smaller base, will rise at a 7.12% CAGR through 2030, propelled by BacFreets contamination-reduction technology that simplifies scale-up.

Manufacturers increasingly assess supply diversification to mitigate saponin harvest volatility, while synthetic biology labs refine VLP scaffolds that co-display multivalent antigens and intrinsic pattern-recognition motifs, potentially sidelining separate adjuvant components. Aluminum-salt, emulsion, and liposome formulations continue anchoring routine pediatric schedules, whereas carbohydrate and bacterial-derived TLR agonists address niche indications that require tailored immune polarization. This coexistence of legacy and disruptive technologies ensures the vaccine adjuvants market retains a heterogeneous product landscape.

Active immunostimulants secured 47.89% of the vaccine adjuvants market share in 2024, underpinned by mechanistically defined agents such as Dynavax's CpG 1018 and GSK's MPL. Regulatory familiarity with these pathways accelerates review timelines and fosters platform approvals across multiple antigens. Vehicle adjuvants, encompassing lipid nanoparticles and polymeric carriers, are projected to grow at 7.04% CAGR through 2030 as developers demand integrated delivery-stimulation solutions.

The vaccine adjuvants market increasingly values vehicles that co-encapsulate antigens and immunopotentiators, maintaining colloidal stability across temperature excursions. Recent manganese-lipid hybrid particles demonstrated stronger CD8+ responses against varicella-zoster versus alum comparators, highlighting functional gains that drive substitution waves. Carrier adjuvants maintain relevance for mucosal or slow-release applications, ensuring each modality retains a defined opportunity space within the broader vaccine adjuvants market.

The Vaccine Adjuvants Market is Segmented by Product Type (Mineral Salt-Based Adjuvant, Saponin and Triterpenoid, Emulsion-Based, and More), Usage Type (Active Immunostimulants, Carriers, and More), Disease Type (Infectious Disease, Cancer, and More), Application (Research Applications and Commercial Applications), and Geography (North America, Europe, and More). The Market and Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America preserved its leadership with 41.12% share in 2024, supported by mature manufacturing capacity, public-health procurement budgets, and FDA regulatory precedents that streamline platform reviews. Under Operation Warp Speed and successor initiatives, federal funding subsidizes scale-up of mRNA-optimized adjuvant systems, further entrenching regional dominance. Clustered academic centers in Boston, San Francisco, and Toronto forge translational pipelines that feed commercial portfolios, ensuring the vaccine adjuvants market remains anchored in the region.

Asia-Pacific is projected to record a 7.45% CAGR through 2030, propelled by China's biopharma capacity additions, India's contract-manufacturing economies of scale, and ASEAN immunization-program expansions. Government subsidies for thermostable adjuvant R&D address tropical cold-chain constraints, while Japan's chemical-industry strength accelerates lipid-nanoparticle innovations. Local regulatory harmonization under ASEAN's Vaccine Regulatory Mechanism reduces approval redundancies, improving speed-to-market for regional developers and elevating the vaccine adjuvants market in Asia-Pacific.

Europe maintains steady mid-single-digit growth as the EMA's adaptive-pathways framework supports conditional licensing for priority adjuvant platforms. Cross-border procurement mechanisms under the EU Joint Procurement Agreement aggregate demand, giving suppliers predictable volumes while enabling price negotiations that preserve margin discipline. Chemical-specialty infrastructure in Germany and the Netherlands sustains high-purity excipient supply, supporting export of adjuvant intermediates to other regions.

- GlaxoSmithKline

- Seppic (Air Liquide)

- Dynavax Technologies Corp.

- Croda International plc (Croda Pharma)

- CSL Limited (BioCSL, Seqirus)

- Merck

- Novavax

- Thermo Fisher Scientific

- Agenus

- Adjuvatis SAS

- InvivoGen

- SPI Pharma (ABF plc)

- Vertellus

- Pacific GeneTech Ltd.

- OZ Biosciences

- Adjuvance Technologies Inc.

- Valneva

- Bavarian Nordic

- Pfizer

- AstraZeneca

- Avanti Polar Lipids (Croda)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Expanding Government Immunization Recommendations

- 4.2.2 Unmet Vaccine Needs for Emerging Zoonoses

- 4.2.3 Rising Adoption of Recombinant & Synthetic Antigens

- 4.2.4 Accelerating Mrna-Platform Demand for Novel Adjuvants

- 4.2.5 Expansion of Microbial-Derived TLR Agonist Pipelines

- 4.2.6 AI-Designed Nano-Alum Formulations Enabling Cold-Chain Free Distribution

- 4.3 Market Restraints

- 4.3.1 Local & Systemic Toxicity Concerns

- 4.3.2 High Discovery & Pre-Clinical Screening Costs

- 4.3.3 Scale-Up Challenges for Squalene & QS-21 Supply Chains

- 4.3.4 Regulatory Uncertainty Around Novel STING Agonists

- 4.4 Regulatory Landscape

- 4.5 Porters Five Forces Analysis

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Bargaining Power of Suppliers

- 4.5.4 Threat of Substitutes

- 4.5.5 Intensity of Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Product Type

- 5.1.1 Mineral-salt Adjuvants

- 5.1.2 Saponin and Triterpenoid

- 5.1.3 Emulsion-based

- 5.1.4 Liposome and Virosome

- 5.1.5 Carbohydrate & Polysaccharide

- 5.1.6 Bacteria-derived TLR agonists

- 5.1.7 Virus-Like Particles

- 5.1.8 Other Product Types

- 5.2 By Usage Type

- 5.2.1 Active Immunostimulants

- 5.2.2 Carriers

- 5.2.3 Vehicle Adjuvants

- 5.3 By Disease Type

- 5.3.1 Infectious Diseases

- 5.3.2 Cancer

- 5.3.3 Others

- 5.4 By Application

- 5.4.1 Research Applications

- 5.4.2 Commercial Applications

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 Australia

- 5.5.3.5 South Korea

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 Middle East and Africa

- 5.5.4.1 GCC

- 5.5.4.2 South Africa

- 5.5.4.3 Rest of Middle East and Africa

- 5.5.5 South America

- 5.5.5.1 Brazil

- 5.5.5.2 Argentina

- 5.5.5.3 Rest of South America

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.3.1 GlaxoSmithKline plc

- 6.3.2 Seppic (Air Liquide)

- 6.3.3 Dynavax Technologies Corp.

- 6.3.4 Croda International plc (Croda Pharma)

- 6.3.5 CSL Limited (BioCSL, Seqirus)

- 6.3.6 Merck KGaA (Sigma-Aldrich)

- 6.3.7 Novavax Inc.

- 6.3.8 Thermo Fisher Scientific Inc.

- 6.3.9 Agenus Inc.

- 6.3.10 Adjuvatis SAS

- 6.3.11 InvivoGen

- 6.3.12 SPI Pharma (ABF plc)

- 6.3.13 Vertellus

- 6.3.14 Pacific GeneTech Ltd.

- 6.3.15 OZ Biosciences

- 6.3.16 Adjuvance Technologies Inc.

- 6.3.17 Valneva SE

- 6.3.18 Bavarian Nordic A/S

- 6.3.19 Pfizer Inc.

- 6.3.20 AstraZeneca plc

- 6.3.21 Avanti Polar Lipids (Croda)

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment