|

시장보고서

상품코드

1850027

암 백신 : 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Cancer Vaccines - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

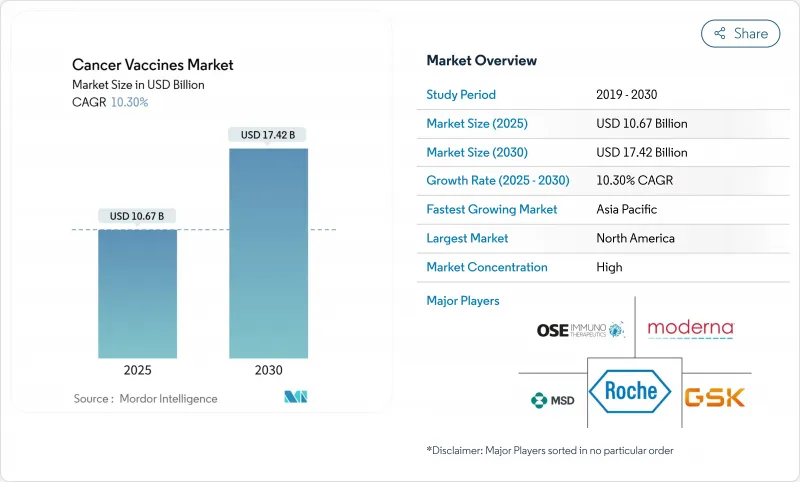

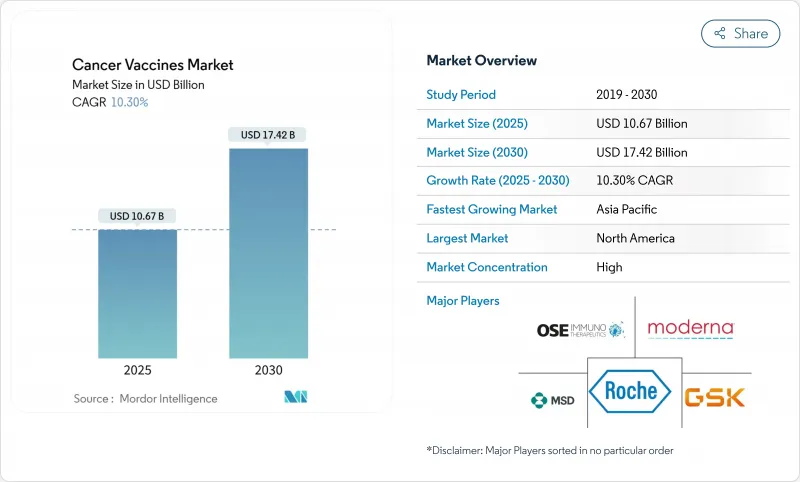

암 백신 시장은 2025년에 106억 7,000만 달러로 평가되었고, 2030년에 174억 2,000만 달러에 이를 것으로 예측되며, 2025-2030년 CAGR은 10.30%를 나타낼 전망입니다.

가속화된 성장은 기존 예방접종에서 환자 맞춤형 신항원을 암호화하는 개인 맞춤형 mRNA 기반 면역치료제로의 전환을 반영하며, 이는 인공지능 항원 예측과 규모 확대 주기를 단축하는 모듈형 마이크로팩토리 제조 기술에 기반합니다. FDA의 획기적 치료제 지정 및 EMA의 PRIME 승인에서 드러나듯 규제 조화는 국경을 넘는 임상시험의 마찰을 줄이는 한편, 파트너십 중심 비즈니스 모델은 단독 제품보다 플랫폼 차별화에 자본을 집중시킵니다. 북미가 주도권을 유지하고 있으나, 중국 개발사들이 서구 수준보다 99% 낮은 비용으로 mRNA 백신을 공급함에 따라 아시아태평양 지역이 가장 빠른 성장세를 보이고 있습니다.

세계의 암 백신 시장 동향 및 인사이트

세계의 암 이환율 증가

2020년부터 2040년까지 암 진단 건수는 47% 증가할 것으로 예상되며, 특히 종합적인 종양학 인프라가 부족한 지역에서 가장 큰 증가세를 보일 전망입니다. 이러한 인구학적 변화는 예방 및 치료용 백신의 대상 환자군을 확대합니다. 고령화 사회는 돌연변이 부하를 증가시키며, 조기 진단 관행은 맞춤형 면역요법 대상 환자 풀을 확대합니다. 외래 환자 중심의 백신 요법은 입원 기반 종양 치료에서 벗어나고 있는 추세와 부합하며, 고소득 시장에서 환자당 15만 달러를 초과할 수 있는 시스템 비용을 절감합니다. 따라서 지불 기관들은 장기적인 전신 치료와 비교할 때 백신을 비용 절감 도구로 인식합니다.

R&D 투자 및 정부 자금 증가

공공-민간 협력 구조가 전통적 보조금을 대체하며 위험 분담과 일정 단축을 실현하고 있습니다. CEPI의 CMC 프레임워크는 이제 암 백신 제조 품질 기준을 제시하여 다중 관할권 허가 절차를 원활하게 합니다. 유럽의 암 기술 특허 출원은 70% 이상 증가했으며, 대학 출원 비중이 상승하여 협력적 혁신 모멘텀을 시사합니다. 영국의 바이오엔테크 프로그램은 2030년까지 1만 명의 환자에게 맞춤형 백신을 제공하겠다고 약속하며, 국가 보건 시스템이 상용화 경로에 직접 투자하는 방식을 보여줍니다. 벤처 캐피털 흐름은 여전히 종양학 분야에 치우쳐 있어, 정부 기금이 점점 더 그 공백을 메우고 있습니다.

엄격한 규제 타임라인과 복잡성

맞춤형 배치 출시 프로토콜과 AI 알고리즘 검증은 표준 생물학적 제제보다 승인 주기를 18-24개월 연장시킵니다. 글로벌 규제 팀이 부족한 중소 기업은 EMA의 PRIME이 임상 데이터 성숙 시 가속화 지위를 부여함에도 불균형적인 부담에 직면합니다. AI 모델 투명성에 대한 공통 기준 부재는 심사 과정을 더욱 불투명하게 만들어 마진을 잠식하는 규정 준수 비용을 추가합니다.

부문 분석

재조합 플랫폼은 2024년 암 백신 시장에서 43.33%의 점유율을 유지했습니다. 기존 생산 기반과 검증된 안전성 기록으로 여전히 유효하나, 개발사들이 다중 항원 인코딩 및 신속 맞춤화를 우선시함에 따라 mRNA/신항원 백신은 2030년까지 연평균 11.21% 성장률로 가속화될 전망입니다. 자가 증폭 구조체는 투여량을 10분의 1로 줄이고 콜드체인 부담을 완화하여 자원 제약 환경에서 경제성을 개선합니다. 바이러스 벡터 및 DNA 방식은 특히 신흥 시장에서 열안정성이 최우선인 틈새 집단을 계속해서 공략하고 있습니다. 전체 세포 및 수지상 세포 백신은 규모는 작지만 고도로 개인화된 요법에서 특수한 역할을 수행합니다. 디아코노스 온콜로지(Diakonos Oncology)가 교모세포종 치료제로 2,000만 달러를 조달한 것은 투자자들의 관심을 반영합니다.

기술 스펙트럼은 몇 주 내에 항원 교체가 가능한 플랫폼 생태계로 수렴하고 있으며, 이는 선점 기업들의 핵심 차별화 요소입니다. 공유 신항원 라이브러리는 맞춤형 제품 이상의 대상 환자군을 확대하여 환자당 비용을 절감하고 규제 심사를 단축합니다. 그 결과, mRNA 구조물에 기인한 암 백신 시장 규모는 특히 실온 제형이 후기 임상시험 단계에 진입하면 선두 격차를 더욱 벌릴 것으로 전망됩니다.

자궁경부암은 광범위한 HPV 예방접종 캠페인의 영향으로 2024년 암 백신 시장 규모의 72.21%를 차지했습니다. 그러나 흑색종 백신은 강력한 바이오마커가 정확한 환자 매칭을 가능하게 하고 규제 당국이 획기적 치료제 지정을 승인함에 따라 11.02%의 연평균 복합 성장률(CAGR)로 발전하고 있습니다. 전립선암 및 교모세포종 프로그램은 수지상 세포 플랫폼을 기반으로 하는 반면, 공유 신항원 전략은 대장암 및 위암에 대한 가능성을 열어줍니다. 흑색종에 대한 긍정적인 결과는 인접한 고형 종양에 대한 위험 인식을 낮추고, 다중 암 플랫폼 시험으로 자본을 끌어모으고 있습니다.

단일 종양 성공 사례에서 플랫폼 기반 다중 암 솔루션으로의 전환은 시간이 지남에 따라 자궁경부암의 우위를 희석시켜 2030년까지 암 백신 시장 점유율이 적응증 전반에 걸쳐 더 균등하게 분배될 것으로 예상됩니다.

지역 분석

2024년 북미의 46.21% 점유율은 성숙한 규제 경로, 광범위한 임상 시험 네트워크, 국립암연구소(NCI)의 250만 달러 규모 전환 연구 지원금과 같은 꾸준한 공공 자금 지원에서 비롯됩니다. USMCA(미국-멕시코-캐나다 협정)는 국경 간 연구를 간소화하여 캐나다 및 멕시코 이해관계자들을 공동 제조 사업으로 끌어들이고 있습니다. 벤처 투자 문화는 고위험 연구개발(R&D)을 지속 가능하게 하여, 비용 압박이 증가함에도 불구하고 해당 지역의 암 백신 시장 성장이 글로벌 평균을 훨씬 상회하도록 유지합니다.

유럽은 공공-민간 협력 사업을 활용합니다. 2030년까지 1만 명 환자를 목표로 하는 영국-바이오엔테크 파트너십은 국가 보건 시스템이 구매력을 활용해 혁신을 촉진하는 방식을 보여줍니다. EMA PRIME은 후기 단계 심사를 가속화하며, 독일, 프랑스, 이탈리아는 학술적 전문성과 GMP 생산 능력을 제공합니다. 환자 중심 결과를 중시하는 보험급여 체계는 맞춤형 솔루션 채택을 촉진해 유럽의 경쟁력을 유지합니다.

아시아태평양 지역은 국가 주도의 바이오테크 프로그램과 서구의 가격 경쟁력을 약화시키는 저비용 제조로 인해 11.38%의 가장 빠른 연평균 성장률(CAGR)을 기록합니다. 중국은 모듈형 마이크로 공장 및 무료 HPV 백신 접종 사업을 지원하며, 일본과 한국은 첨단 공정 기술을 수출합니다. 인도의 계약 제조 역량과 방대한 환자 기반은 핵심 임상 시험 허브로 자리매김하게 합니다. 호주는 ICH 기준과의 규제 조화를 통해 태평양 횡단 상용화를 위한 가교 시장으로 부상합니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월의 애널리스트 지원

목차

제1장 서론

- 조사의 전제조건과 시장의 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 세계의 암 발병률 증가

- 연구개발투자와 정부자금 증가

- mRNA 및 신항원 플랫폼의 발전

- AI에 의한 항원 예측으로 비용 절감

- 모듈형 마이크로 팩토리 제조 허브

- 임상시험 위험을 낮추는 CPI 병용 요법(보고 부족)

- 시장 성장 억제요인

- 엄격한 규제 타임라인과 복잡성

- 대체 면역요법의 가용성

- 맞춤형 물류의 콜드체인 격차

- 신규 진입을 제한하는 신항원 지적재산권 집적

- 규제 상황

- 기술의 전망

- Porter's Five Forces 분석

- 구매자의 협상력

- 공급기업의 협상력

- 신규 참가업체의 위협

- 대체품의 위협

- 경쟁 기업간 경쟁 관계

제5장 시장 규모와 성장 예측

- 기술별

- 재조합 백신

- 바이러스 벡터 백신과 DNA 백신

- mRNA/신항원 백신

- 전세포 백신과 수지상 세포 백신

- 기타 기술

- 치료 방법별

- 예방 백신

- 치료 백신

- 암 유형별

- 자궁경부암(HPV)

- 전립선암

- 흑색종

- 기타 암

- 투여 경로별

- 근육내

- 피내/피하

- 정맥내

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 러시아

- 기타 유럽

- 아시아태평양

- 중국

- 일본

- 인도

- 호주

- 한국

- 기타 아시아태평양

- 중동 및 아프리카

- GCC

- 남아프리카

- 기타 중동 및 아프리카

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 북미

제6장 경쟁 구도

- 시장 집중도

- 시장 점유율 분석

- 기업 프로파일

- Merck & Co., Inc.

- GlaxoSmithKline plc

- Moderna Inc.

- Bristol Myers Squibb Co.

- AstraZeneca plc

- F. Hoffmann-La Roche AG(Genentech)

- BioNTech SE

- Gritstone bio, Inc.

- Vaccitech plc

- OSE Immunotherapeutics SA

- Anixa Biosciences Inc.

- Dendreon Pharmaceuticals LLC

- Providence Therapeutics Holdings

- eTheRNA Immunotherapies NV

- Imugene Ltd.

- Transgene SA

- OncoSec Medical Incorporated

- NantKwest Inc.

- Ultimovacs ASA

- ISA Pharmaceuticals BV

제7장 시장 기회와 장래의 전망

HBR 25.11.14The cancer vaccines market reached USD 10.67 billion in 2025 and is forecast to climb to USD 17.42 billion by 2030, advancing at a 10.30% CAGR during 2025-2030.

Accelerated growth reflects the pivot from conventional prophylaxis toward personalized mRNA-based immunotherapies that encode patient-specific neoantigens, underpinned by artificial-intelligence antigen prediction and modular micro-factory manufacturing that shortens scale-up cycles. Regulatory harmonization-evident in FDA breakthrough designations and EMA PRIME approvals-lowers cross-border trial friction, while partnership-heavy business models channel capital toward platform differentiation rather than stand-alone products. North America retains leadership yet Asia-Pacific shows the fastest uptake as Chinese developers deliver mRNA vaccines at costs 99% below Western levels.

Global Cancer Vaccines Market Trends and Insights

Growing Global Cancer Incidence

Cancer diagnoses are projected to rise 47% between 2020 and 2040, with the sharpest increases in regions lacking comprehensive oncology infrastructure; this demographic shift expands the addressable population for both preventive and therapeutic vaccines. Aging societies bring higher mutation loads, while earlier diagnostic practices enlarge the pool of patients eligible for tailored immunotherapies. Outpatient-friendly vaccine regimens align with the transition away from inpatient oncology care, trimming system costs that can exceed USD 150,000 per patient in high-income markets. Payers therefore see vaccines as cost-containment tools when compared with prolonged systemic therapies.

Increasing R&D Investments & Government Funding

Public-private partnership structures increasingly supplant traditional grants, sharing risk and compressing timelines. CEPI's CMC framework now guides quality standards for cancer vaccine manufacturing, smoothing multi-jurisdictional filings . European patent applications for cancer technologies climbed more than 70%, with universities filing a rising share, signaling collaborative innovation momentum. The UK's BioNTech program pledges personalized vaccines to 10,000 patients by 2030, illustrating how national health systems invest directly in commercialization pathways. Venture capital flows remain skewed toward oncology, leaving a gap that government funds increasingly fill.

Stringent Regulatory Timelines & Complexity

Personalized batch release protocols and AI-algorithm validation stretch approval cycles by 18-24 months beyond standard biologics. Smaller firms lacking global regulatory teams face disproportionate burdens, even though EMA's PRIME gives accelerated status once clinical data mature. Absence of common standards on AI model transparency further clouds review processes, adding compliance costs that erode margins.

Other drivers and restraints analyzed in the detailed report include:

- Advances in mRNA & Neoantigen Platforms

- AI-Driven Antigen Prediction Lowering Cost

- Availability of Alternative Immunotherapies

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Recombinant platforms retained a 43.33% share of the cancer vaccines market in 2024. Their installed manufacturing base and well-known safety records keep them relevant, yet mRNA/neoantigen vaccines are accelerating at an 11.21% CAGR through 2030 as developers prioritize multiplex antigen encoding and rapid customization. Self-amplifying constructs reduce dose volume tenfold and ease cold-chain stress, improving economics for resource-constrained settings. Viral-vector and DNA modalities continue to address niche populations where thermostability is paramount, especially in emerging markets. Whole-cell and dendritic vaccines, though smaller in volume, play specialized roles in highly personalized regimens; Diakonos Oncology's USD 20 million raise for glioblastoma underscores investor interest.

The technology spectrum is converging toward platform ecosystems that allow antigen swapping within weeks, a key differentiation for first movers. Shared-neoantigen libraries expand addressable populations beyond bespoke products, cutting per-patient costs and shortening regulatory reviews. As a result, the cancer vaccines market size attributed to mRNA constructs is forecast to widen its lead, especially once room-temperature formulations enter late-stage trials.

Cervical cancer accounted for 72.21% of the cancer vaccines market size in 2024, a legacy of widespread HPV immunization campaigns. Melanoma vaccines, however, are advancing at an 11.02% CAGR as robust biomarkers facilitate precise patient matching and regulators grant breakthrough designations. Prostate and glioblastoma programs build on dendritic-cell platforms, while shared-neoantigen strategies open doors for colorectal and gastric cancers. Positive melanoma results reduce risk perceptions for adjacent solid tumors, drawing capital toward multi-cancer platform trials.

The transition from single-tumor success stories to platform-based multi-cancer solutions is expected to dilute cervical dominance over time, distributing the cancer vaccines market share more evenly across indications by 2030.

The Cancer Vaccines Market is Segmented by Technology (Recombinant Vaccines, and More), Treatment Method (Preventive Vaccines and Therapeutic Vaccines), Cancer Type (Cervical Cancer (HPV), Melanoma and More), Delivery Route (Intramuscular, Intravenous, and More), and Geography (North America, Europe, Asia-Pacific, and More). The Market and Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America's 46.21% share in 2024 stems from mature regulatory pathways, extensive trial networks, and steady public funding such as the National Cancer Institute's USD 2.5 million translational grants. USMCA streamlines cross-border studies, drawing Canadian and Mexican stakeholders into joint manufacturing ventures. Venture investment culture sustains high-risk R&D, keeping the cancer vaccines market growth in the region well above global averages despite mounting cost pressures.

Europe leverages coordinated public-private initiatives; the UK-BioNTech partnership targeting 10,000 patients by 2030 exemplifies how national health systems deploy purchasing power to spur innovation. EMA PRIME accelerates late-stage reviews, while Germany, France, and Italy supply academic expertise and GMP capacity. Reimbursement frameworks that value patient-centric outcomes favor adoption of personalized solutions, maintaining Europe's competitive weight.

Asia-Pacific posts the fastest 11.38% CAGR owing to state-sponsored biotech programs and low-cost manufacturing that erodes Western price advantages. China funds modular micro-factories and free HPV drives, while Japan and South Korea export advanced process technologies. India's contract-manufacturing depth and expansive patient base make it a pivotal trial hub. Australia's regulatory alignment with ICH standards positions it as a bridge market for trans-Pacific commercialization.

- Merck

- GlaxoSmithKline

- Moderna

- Bristol-Myers Squibb

- AstraZeneca

- F. Hoffmann-La Roche AG (Genentech)

- BioNTech

- Gritstone bio, Inc.

- Vaccitech plc

- OSE Immunotherapeutics SA

- Anixa Biosciences

- Dendreon Pharmaceuticals

- Providence Therapeutics Holdings

- eTheRNA Immunotherapies NV

- Imugene Ltd.

- Transgene

- OncoSec Medical Incorporated

- NantKwest Inc.

- Ultimovacs ASA

- ISA Pharmaceuticals BV

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing global cancer incidence

- 4.2.2 Increasing R&D investments & government funding

- 4.2.3 Advances in mRNA & neoantigen platforms

- 4.2.4 AI-driven antigen prediction lowering cost

- 4.2.5 Modular micro-factory manufacturing hubs

- 4.2.6 Combination regimens with CPIs de-risking trials (under-reported)

- 4.3 Market Restraints

- 4.3.1 Stringent regulatory timelines & complexity

- 4.3.2 Availability of alternative immunotherapies

- 4.3.3 Cold-chain gaps for personalised logistics

- 4.3.4 Neoantigen IP clustering limiting entrants

- 4.4 Regulatory Landscape

- 4.5 Technological Outlook

- 4.6 Porters Five Forces Analysis

- 4.6.1 Bargaining Power of Buyers

- 4.6.2 Bargaining Power of Suppliers

- 4.6.3 Threat of New Entrants

- 4.6.4 Threat of Substitutes

- 4.6.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Technology

- 5.1.1 Recombinant Vaccines

- 5.1.2 Viral Vector & DNA Vaccines

- 5.1.3 mRNA/Neoantigen Personalised Vaccines

- 5.1.4 Whole-cell & Dendritic Cell Vaccines

- 5.1.5 Other Technologies

- 5.2 By Treatment Method

- 5.2.1 Preventive Vaccines

- 5.2.2 Therapeutic Vaccines

- 5.3 By Cancer Type

- 5.3.1 Cervical Cancer (HPV)

- 5.3.2 Prostate Cancer

- 5.3.3 Melanoma

- 5.3.4 Other Cancers

- 5.4 By Delivery Route

- 5.4.1 Intramuscular

- 5.4.2 Intradermal / Sub-cutaneous

- 5.4.3 Intravenous

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Russia

- 5.5.2.7 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 Australia

- 5.5.3.5 South Korea

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 Middle East and Africa

- 5.5.4.1 GCC

- 5.5.4.2 South Africa

- 5.5.4.3 Rest of Middle East and Africa

- 5.5.5 South America

- 5.5.5.1 Brazil

- 5.5.5.2 Argentina

- 5.5.5.3 Rest of South America

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.3.1 Merck & Co., Inc.

- 6.3.2 GlaxoSmithKline plc

- 6.3.3 Moderna Inc.

- 6.3.4 Bristol Myers Squibb Co.

- 6.3.5 AstraZeneca plc

- 6.3.6 F. Hoffmann-La Roche AG (Genentech)

- 6.3.7 BioNTech SE

- 6.3.8 Gritstone bio, Inc.

- 6.3.9 Vaccitech plc

- 6.3.10 OSE Immunotherapeutics SA

- 6.3.11 Anixa Biosciences Inc.

- 6.3.12 Dendreon Pharmaceuticals LLC

- 6.3.13 Providence Therapeutics Holdings

- 6.3.14 eTheRNA Immunotherapies NV

- 6.3.15 Imugene Ltd.

- 6.3.16 Transgene SA

- 6.3.17 OncoSec Medical Incorporated

- 6.3.18 NantKwest Inc.

- 6.3.19 Ultimovacs ASA

- 6.3.20 ISA Pharmaceuticals BV

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment