|

시장보고서

상품코드

1850029

매니지드 정보 서비스 : 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Managed Information Services - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

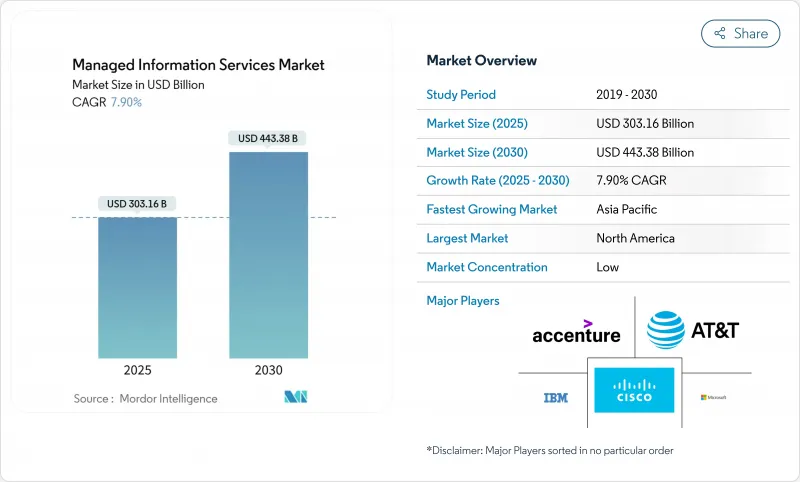

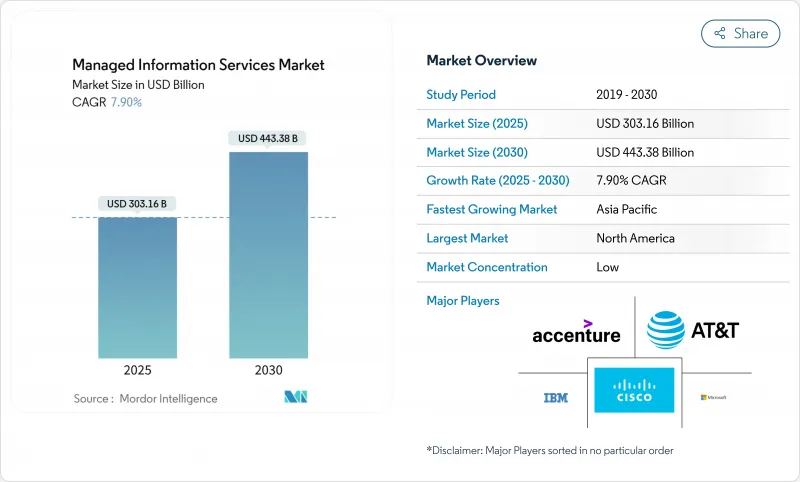

매니지드 정보 서비스 시장은 2025년에 3,031억 6,000만 달러에 이르고, CAGR 7.9%를 나타내, 2030년에는 4,433억 8,000만 달러 시장 규모에 달할 것으로 예상됩니다.

기업이 소유 모델에서 소비 모델로 이행하여 클라우드 퍼스트 로드맵을 가속화하고 자동화와 인공지능을 일상 업무에 통합하는 전문가 파트너를 통해 중요한 인재 갭을 해소하고 있기 때문에 견조한 수요가 지속되고 있습니다. 매니지드 정보 서비스 시장은 또한 사이버 리스크 증가, 규제 압력 증가, 대부분의 내부 IT 팀이 자금을 조달하거나 대규모 직원을 배치할 수 없는 상시 가동 탄력성에 대한 요구로부터 이익을 얻고 있습니다. 아시아태평양의 급속한 디지털화에 의해 그 차이는 줄어들고 있는 것, 북미가 계속해서 세계한 지출의 중심이 되고 있습니다. 경쟁 우위는 성과 기반 계약, 하이브리드 아키텍처의 통합 관리, 진화하는 컴플라이언스에 대응하는 지속적인 보안 운영을 실현할 수 있는 공급자로 옮겨가고 있습니다.

세계의 매니지드 정보 서비스 시장 동향과 인사이트

하이브리드/멀티클라우드 아키텍처로 마이그레이션

하이브리드와 멀티클라우드는 도구 선호도가 아니라 이사회 수준의 필수 사항으로, 2027년까지 90%의 기업이 이 접근법을 채택할 것으로 예측됩니다. 워크로드의 이식성, 데이터 레지던시일, 벤더의 다양화는 운영의 복잡성을 증가시켜 기업이 타사 전문가로부터 통합 관리를 조달하도록 촉구하고 있습니다. 시스코 보고에 따르면 기업의 53%가 매주 On-Premise와 클라우드 환경 간에 워크로드를 이동하고 있으며 오케스트레이션 플랫폼과 크로스 도메인 거버넌스 서비스에 대한 지속적인 수요를 창출하고 있습니다. 서로 다른 플랫폼간에 일관된 정책 구현, 통합 관측 가능성, 자동화된 워크로드 배치를 제공하는 공급업체는 현재 프리미엄 가격을 요구하고 있습니다. 컴플라이언스와 혁신의 목표를 동시에 충족시켜야 하는 고도로 규제된 섹터를 채택하는 것이 가장 눈에 띄고, 로컬 컨트롤과 클라우드의 민첩성을 융합할 수 있는 관리 서비스의 가치 제안이 강화되고 있습니다.

비용 최적화 및 OPEX 선호

경제 불확실성과 급속한 기술 교환은 재무 리더를 예측 가능한 구독 지출로 몰고 있습니다. 매니지드 서비스는 하드웨어의 진부화, 라이선스 관리, 인재 확보 위험을 벤더에게 전가하면서 자본 지출을 영업 비용으로 전환합니다. 중소기업이 이 모델을 가장 빨리 받아들이고 있는 이유는 상당한 선행 투자 없이 엔터프라이즈급 보안 및 애널리틱스를 이용할 수 있기 때문입니다. 또한 공급업체는 컴플라이언스 보고서 및 사고 대응에 대한 책임을 지므로 내부 팀은 누락된 기술을 고객을 위한 혁신으로 돌릴 수 있습니다. 결과적으로 OPEX 주도 계약은 인프라 가용성뿐만 아니라 서비스 수준, 사용자 경험 및 비즈니스 지표와 관련된 성과 보증을 포함하는 경우가 많습니다.

레거시 통합 및 규제의 복잡성

많은 기업들이 수십년전의 시스템에서 핵심 용도를 실행하고 있으며, 최신 관리 플랫폼과의 인터페이스가 쉽지 않습니다. 은행, 유틸리티, 공공기관은 맞춤형 컨트롤, 특수 어댑터, 검증 주기의 연장을 요구하는 엄격한 감사 요구 사항에 직면하고 있습니다. 커스텀 통합은 프로젝트 비용을 팽창시켜 매니지드 서비스의 매력인 스케일 메리트를 손상시킵니다. SOX 및 GDPR(EU 개인정보보호규정)과 같은 컴플라이언스 프레임워크는 On-Premise에서 감사 로깅 및 데이터 분리를 요구하는 경우가 많으며, 공급자는 배달 노력을 늘리는 전용 환경을 도입해야 합니다. 이러한 요인은 특히 다양한 규제 의무를 지닌 세계 기업의 경우 판매주기를 장기화하고 Time-to-Value를 지연시킵니다.

부문 분석

2024년 매니지드 정보 서비스 시장 점유율은 On-Premise 환경이 54.1%를 차지했습니다. 프라이빗 데이터센터에 대한 많은 투자와 대기 시간에 민감한 워크로드가 이 선호도를 더욱 강화하고 있습니다. 하지만 클라우드 기반의 관리형 서비스인 CAGR은 13.8%에 달하는 추세이며, 민첩성과 탄력적인 소비를 중시하는 업계 전반에 걸쳐 워크로드 마이그레이션이 가속화되고 있다고 말합니다. 현재는 하이브리드 환경이 주류가 되고 있으며, 서비스 제공업체는 단일 화면에서의 시각화, 자동화된 구성 드리프트 수정, 양 환경에서의 통일된 보안 관리를 제공해야 합니다.

클라우드의 가속도는 하이퍼스케일 플랫폼에 대한 신뢰 증가를 반영합니다. 하이퍼스케일 플랫폼은 현재 섹터별 컴플라이언스 설계도, 주권 클라우드 영역, 세분화된 암호화 옵션을 제공합니다. 또한 기업은 클라우드의 현대화가 용도의 변화와 불가분임을 인식하고 있으며, 리팩토링, DevSecOps 파이프라인, 지속적인 컴플라이언스 모니터링에 대한 수요를 추진하고 있습니다. 인증된 클라우드 전문 지식, 고유한 마이그레이션 가속기 및 견고한 재무 최적화 도구를 입증하는 관리형 서비스 파트너는 보다 큰 계약 범위를 획득했습니다. 반대로 데이터센터 아웃소싱으로 제한된 공급자는 고객이 클라우드 네이티브 설계 패턴을 채택하고 워크로드 배치의 경제성에 대한 적극적인 지침을 기대하기 때문에 계약 감소의 위험이 있습니다.

매니지드 보안 서비스는 2024년 총 매출의 28.5%를 차지했으며 CAGR 14.7%를 나타낼 전망입니다. 첨단 서비스는 위협 인텔리전스, 행동 분석 및 통합 플랫폼을 통해 수행되는 자동 응답을 통합하여 수작업으로 인한 방어 작업을 완화합니다.

또한 제로 트러스트 네트워크 액세스, 클라우드 워크로드 보호, 공급망 위험 평가에 대한 수요도 높아지고 있습니다. 이와 병행하여, 매니지드 데이터센터와 네트워크 서비스는 예측 가능한 연금 스트림을 계속 제공하고 있지만, 인프라의 자동화에 의해 기존의 티켓량이 압축되기 때문에 그 성장은 보안을 견인하고 있습니다. 따라서 서비스 포트폴리오는 공급업체가 정체성 거버넌스, 데이터 유출 방지 및 컴플라이언스 대시보드를 통합하여 보안 멀티클라우드 지원에 집중되고 있습니다. 카나리스는 보안과 클라우드 최적화를 결합한 서비스는 단독 제안에 비해 크로스셀 수익이 1.6배 높다고 강조하고 있습니다. MDR 플랫폼, 보안 분석, 사고 대응 전문 팀에 투자하는 공급업체는 차별화된 마진을 획득했습니다.

매니지드 정보 서비스 시장은 배치별(클라우드와 On-Premise), 서비스 유형별(매니지드 데이터센터, 매니지드 보안, 매니지드 커뮤니케이션(UC와 VoIP) 등), 최종 사용자 기업 규모별(중소기업과 대기업), 최종 사용자 업종별(IT 및 텔레콤, BFSI), 시장 예측은 금액(달러)으로 제공됩니다.

지역별 분석

북미는 클라우드의 조기 도입, 고급 사이버 보안 규제, 티아완 프로바이더의 생태계 충실로 2024년 매출의 35.4%를 유지했습니다. 미국 기업은 예측 분석, AI 지원 업무, 요금을 비즈니스 KPI에 연결하는 성과 기반 계약을 일상적으로 요구하고 있습니다. 캐나다에서는 연방 정부의 디지털 거버먼트 프로그램과 안전한 멀티 클라우드 탄력성에 의존하는 현대적인 뱅킹 이니셔티브가 기세를 늘리고 있습니다. 많은 공급업체는 낮은 지연 서비스 수준을 유지하면서 진화하는 주 수준의 개인 정보 보호법을 준수하기 위해 지역 전달 허브와 소블린 클라우드 존을 구축하고 있습니다.

아시아태평양은 CAGR 12.9%로 가장 빠르게 성장하고 있으며 기존 지역과의 차이를 줄이고 있습니다. 중국은 에지 오케스트레이션과 안전한 연결성을 요구하는 스마트 시티 투자 및 제조업 업그레이드 정책을 통해 관리 정보 서비스의 규모를 확대하고 있습니다. 동남아시아 국가들은 클라우드 호스팅 용도과 모바일 퍼스트 커머스를 채택하여 레거시 인프라를 구축하고 있으며, 네트워크 최적화 및 규제 준수를 위한 파트너 지원이 필요합니다. 합작투자, 다국어 서비스 데스크, 지역별로 전문화된 가상 솔루션을 설립하는 공급업체는 월렛 점유율을 얻는 데 유리한 위치에 있습니다.

유럽에서는 GDPR(EU 개인정보보호규정), 디지털 운영 탄력성 법, 지속가능성 보고 의무를 뒷받침하는 성숙하면서도 엄격한 수요를 볼 수 있습니다. 독일과 영국은 여전히 최고 수준의 지출국이지만 EU 부흥 기금이 디지털화 프로젝트를 지원하기 때문에 남유럽 지출은 가속화되고 있습니다. 공급자는 측정 가능한 이산화탄소 감축 이니셔티브, EU 한정 데이터 레지던시, 감사 대응 규정 준수 아티팩트를 제공함으로써 차별화를 도모하고 있습니다. 이윽고, 환경규제의 강화에 의해 재생가능에너지의 조달이나 순환형 경제의 하드웨어의 실천에 대해 검증 가능한 진척을 나타내는 파트너로 조달 기준이 변화해 갈 것으로 예측됩니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월의 애널리스트 지원

목차

제1장 서론

- 조사 전제조건과 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 하이브리드/멀티클라우드 아키텍처로의 전환

- 비용 최적화 및 OPEX 우선

- 사이버 위협과 컴플라이언스 압력 증가

- 로컬 MSP 노드가 필요한 엣지 컴퓨팅 배포

- 그린 매니지드 서비스에 있어서의 지속가능성의 의무

- AI 구동형 자율운용(AIOps)의 성숙도

- 시장 성장 억제요인

- 레거시 통합과 규제의 복잡성

- 데이터 주권/프라이버시에 대한 우려

- 숙련 인력 부족이 MSP 비용 상승

- MSP의 범위를 축소하는 서버리스/No-Ops 아키텍처

- 밸류체인 분석

- 규제 상황

- 기술의 전망

- Porter's Five Forces 분석

- 신규 참가업체의 위협

- 구매자의 협상력

- 공급기업의 협상력

- 대체품의 위협

- 경쟁 기업 간 경쟁 관계

- 투자분석

제5장 시장 규모와 성장 예측

- 배포별

- On-Premise

- 클라우드

- 서비스 유형별

- 매니지드 데이터센터

- 매니지드 보안

- 매니지드 커뮤니케이션(UC 및 VoIP)

- 매니지드 네트워크(LAN/WAN/SASE)

- 매니지드 인프라(서버/스토리지)

- 매니지드 모빌리티 및 기기

- 매니지드 애플리케이션 및 DevOps

- 최종 사용자 기업 규모별

- 중소기업

- 대기업

- 최종 사용자별

- BFSI

- IT 및 통신

- 헬스케어

- 미디어 및 엔터테인먼트

- 소매업 및 전자상거래

- 제조

- 정부 및 공공 부문

- 기타 업종

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 러시아

- 스페인

- 스위스

- 기타 유럽

- 아시아태평양

- 중국

- 인도

- 일본

- 한국

- 말레이시아

- 싱가포르

- 베트남

- 인도네시아

- 기타 아시아태평양

- 중동 및 아프리카

- 중동

- 사우디아라비아

- 아랍에미리트(UAE)

- 튀르키예

- 기타 중동

- 아프리카

- 나이지리아

- 남아프리카

- 기타 아프리카

- 북미

제6장 경쟁 구도

- 시장 집중도

- 전략적 동향

- 시장 점유율 분석

- 기업 프로파일

- IBM Corporation

- Accenture plc

- Cisco Systems Inc.

- Microsoft Corporation

- AT&T Inc.

- Fujitsu Ltd

- Hewlett Packard Enterprise(HPE)

- Dell Technologies Inc.

- Verizon Communications Inc.

- Rackspace Technology

- Deutsche Telekom AG(T-Systems)

- Nokia Solutions and Networks

- Telefonaktiebolaget LM Ericsson

- Tata Consultancy Services(TCS)

- Wipro Ltd

- HCL Technologies Ltd

- Cognizant Technology Solutions

- NTT DATA Corporation

- Capgemini SE

- Kyndryl Holdings Inc.

- Orange Business Services

제7장 시장 기회와 향후 전망

KTH 25.11.04The managed information services market reached USD 303.16 billion in 2025 and is forecast to expand at a 7.9% CAGR, delivering a managed information services market size of USD 443.38 billion by 2030.

Robust demand persists because enterprises are shifting from ownership to consumption models, accelerating cloud-first roadmaps, and closing critical talent gaps through specialist partners that embed automation and artificial intelligence into day-to-day operations. The managed information services market also benefits from cyber-risk escalation, mounting regulatory pressure, and the need for always-on resilience that most internal IT teams cannot fund or staff at scale. North America continues to anchor global spending, although rapid digitalization across Asia-Pacific is narrowing the gap. Competitive advantage now flows to providers capable of outcome-based contracts, unified management across hybrid architectures, and continuous security operations that align with evolving compliance mandates.

Global Managed Information Services Market Trends and Insights

Shift to Hybrid / Multi-Cloud Architectures

Hybrid and multi-cloud have become a board-level imperative rather than a tooling preference, with 90% of enterprises projected to adopt the approach by 2027. Workload portability, data residency rules, and vendor diversification multiply operational complexity, prompting organisations to source unified management from third-party specialists. Cisco reports that 53% of firms move workloads between on-premise and cloud environments each week, creating sustained demand for orchestration platforms and cross-domain governance services. Providers that supply consistent policy enforcement, integrated observability, and automated workload placement across dissimilar platforms currently command premium pricing. Adoption is most visible in highly regulated sectors that must simultaneously satisfy compliance and innovation goals, reinforcing the value proposition of managed services that can blend local control with cloud agility.

Cost-Optimization and OPEX Preference

Economic uncertainty and rapid technology churn are driving finance leaders toward predictable subscription spending. Managed services convert capital outlays into operating expenses while transferring hardware obsolescence, licence management, and talent retention risks to the vendor. Small and medium enterprises are embracing the model fastest because it unlocks enterprise-grade security and analytics without heavy up-front investment. Providers also assume compliance reporting and incident response responsibilities, allowing internal teams to redirect scarce skills toward customer-facing innovation. As a result, OPEX-driven contracts increasingly include outcome guarantees tied to service levels, user experience, and business metrics rather than infrastructure availability alone.

Legacy Integration and Regulatory Complexity

Many enterprises run core applications on decades-old systems that cannot easily interface with modern managed platforms. Banking, utilities, and public-sector agencies face stringent audit requirements that demand bespoke controls, specialised adapters, and extended validation cycles. Custom integration inflates project costs and erodes the economies of scale that make managed services attractive. Compliance frameworks such as SOX and GDPR often mandate on-premise audit logging and data segregation, forcing providers to deploy dedicated environments that increase delivery effort. These factors lengthen sales cycles and delay time-to-value, especially for global organisations with diverse regulatory obligations.

Other drivers and restraints analyzed in the detailed report include:

- Escalating Cyber-Threat and Compliance Pressure

- Edge-Computing Roll-Outs Requiring Local MSP Nodes

- Serverless / No-Ops Architectures Reducing MSP Scope

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

On-premise environments retained 54.1% of managed information services market share in 2024 because many highly regulated firms continue to demand direct infrastructure custody. Heavy investments in private data centres and latency-sensitive workloads further anchor this preference. Yet cloud-based managed services are on track for a 13.8% CAGR, underscoring that workload migration is gathering pace across industries that prize agility and elastic consumption. Hybrid estates now prevail, compelling service providers to offer single-pane visibility, automated configuration drift remediation, and uniform security controls across both venues.

Cloud acceleration also reflects growing trust in hyperscale platforms that now provide sector-specific compliance blueprints, sovereign cloud zones, and granular encryption options. Enterprises moreover recognise that cloud modernisation is inseparable from application transformation, driving demand for refactoring, DevSecOps pipelines, and continuous compliance monitoring. Managed services partners that demonstrate certified cloud expertise, proprietary migration accelerators, and robust financial optimisation tooling are winning larger contract scopes. Conversely, providers limited to data-centre outsourcing risk contract attrition as clients adopt cloud-native design patterns and expect proactive guidance on workload placement economics.

Managed security services controlled 28.5% of the total revenue pool in 2024 and are expanding at 14.7% CAGR, reflecting cyber risk's elevation to an enterprise-wide priority. Advanced services now blend threat intelligence, behaviour analytics, and automated response executed through unified platforms, reducing manual triage workloads.

Demand also rises for zero-trust network access, cloud workload protection, and supply-chain risk assessments. In parallel, managed data-centre and network services continue to deliver predictable annuity streams, but their growth trails security because infrastructure automation compresses traditional ticket volumes. Service portfolios are therefore converging around secure multi-cloud enablement, with providers integrating identity governance, data loss prevention, and compliance dashboards. Canalys highlights that combined security and cloud optimisation offerings generate 1.6 times higher cross-sell revenue relative to siloed propositions. Vendors investing in MDR platforms, security analytics, and specialist incident-response teams consequently command differentiated margins.

Managed Information Services Market is Segmented by Deployment (Cloud and On-Premise), Service Type (Managed Data Centre, Managed Security, Managed Communications (UC and VoIP) and More), End-User Enterprise Size (Small and Medium-Sized Enterprises and Large Enterprises), End-User Vertical (IT and Telecom, BFSI, Healthcare, and More) and by Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America retained 35.4% of 2024 revenue due to early cloud adoption, sophisticated cybersecurity regulations, and a deep ecosystem of tier-one providers. Enterprises in the United States routinely demand predictive analytics, AI-assisted operations, and outcome-based contracts that tie fees to business KPIs. Canada adds momentum through federal digital-government programmes and modern banking initiatives that depend on secure multi-cloud elasticity. Many providers deploy regional delivery hubs and sovereign cloud zones to comply with evolving state-level privacy laws while sustaining low-latency service levels.

Asia-Pacific is the fastest-growing theatre at 12.9% CAGR and is closing the gap on incumbent regions. China scales managed information services through smart-city investments and manufacturing upgrade policies that require edge orchestration and secure connectivity. Southeast Asian nations are leapfrogging legacy infrastructure by adopting cloud-hosted applications and mobile-first commerce, necessitating partner support for network optimisation and regulatory compliance. Providers that establish joint ventures, multilingual service desks, and region-specific vertical solutions are well positioned to capture wallet share.

Europe shows mature yet resilient demand anchored in GDPR, the Digital Operational Resilience Act, and sustainability reporting obligations. Germany and the United Kingdom remain top spenders, but southern Europe is accelerating as EU recovery funds support digitisation projects. Providers differentiate by offering measurable carbon-reduction initiatives, EU-only data residency, and audit-ready compliance artefacts. Over time, tighter environmental rules will shift procurement criteria toward partners that demonstrate verifiable progress on renewable energy sourcing and circular-economy hardware practices

- IBM Corporation

- Accenture plc

- Cisco Systems Inc.

- Microsoft Corporation

- AT&T Inc.

- Fujitsu Ltd

- Hewlett Packard Enterprise (HPE)

- Dell Technologies Inc.

- Verizon Communications Inc.

- Rackspace Technology

- Deutsche Telekom AG (T-Systems)

- Nokia Solutions and Networks

- Telefonaktiebolaget LM Ericsson

- Tata Consultancy Services (TCS)

- Wipro Ltd

- HCL Technologies Ltd

- Cognizant Technology Solutions

- NTT DATA Corporation

- Capgemini SE

- Kyndryl Holdings Inc.

- Orange Business Services

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Shift to hybrid / multi-cloud architectures

- 4.2.2 Cost-optimisation and OPEX preference

- 4.2.3 Escalating cyber-threat and compliance pressure

- 4.2.4 Edge-computing roll-outs needing local MSP nodes

- 4.2.5 Sustainability mandates for green managed services

- 4.2.6 AI-driven autonomous operations (AIOps) maturity

- 4.3 Market Restraints

- 4.3.1 Legacy integration and regulatory complexity

- 4.3.2 Data-sovereignty / privacy concerns

- 4.3.3 Skilled-talent crunch inflating MSP costs

- 4.3.4 Serverless / No-Ops architectures reducing MSP scope

- 4.4 Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Investment Analysis

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Deployment

- 5.1.1 On-premise

- 5.1.2 Cloud

- 5.2 By Service Type

- 5.2.1 Managed Data Centre

- 5.2.2 Managed Security

- 5.2.3 Managed Communications (UC and VoIP)

- 5.2.4 Managed Network (LAN/WAN/SASE)

- 5.2.5 Managed Infrastructure (Server / Storage)

- 5.2.6 Managed Mobility and Device

- 5.2.7 Managed Application and DevOps

- 5.3 By End-user Enterprise Size

- 5.3.1 Small and Medium Enterprises (SME)

- 5.3.2 Large Enterprises

- 5.4 By End-user Vertical

- 5.4.1 BFSI

- 5.4.2 IT and Telecom

- 5.4.3 Healthcare

- 5.4.4 Media and Entertainment

- 5.4.5 Retail and E-commerce

- 5.4.6 Manufacturing

- 5.4.7 Government and Public Sector

- 5.4.8 Other Verticals

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Russia

- 5.5.3.6 Spain

- 5.5.3.7 Switzerland

- 5.5.3.8 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 India

- 5.5.4.3 Japan

- 5.5.4.4 South Korea

- 5.5.4.5 Malaysia

- 5.5.4.6 Singapore

- 5.5.4.7 Vietnam

- 5.5.4.8 Indonesia

- 5.5.4.9 Rest of Asia-Pacific

- 5.5.5 Middle East and Africa

- 5.5.5.1 Middle East

- 5.5.5.1.1 Saudi Arabia

- 5.5.5.1.2 United Arab Emirates

- 5.5.5.1.3 Turkey

- 5.5.5.1.4 Rest of Middle East

- 5.5.5.2 Africa

- 5.5.5.2.1 Nigeria

- 5.5.5.2.2 South Africa

- 5.5.5.2.3 Rest of Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 IBM Corporation

- 6.4.2 Accenture plc

- 6.4.3 Cisco Systems Inc.

- 6.4.4 Microsoft Corporation

- 6.4.5 AT&T Inc.

- 6.4.6 Fujitsu Ltd

- 6.4.7 Hewlett Packard Enterprise (HPE)

- 6.4.8 Dell Technologies Inc.

- 6.4.9 Verizon Communications Inc.

- 6.4.10 Rackspace Technology

- 6.4.11 Deutsche Telekom AG (T-Systems)

- 6.4.12 Nokia Solutions and Networks

- 6.4.13 Telefonaktiebolaget LM Ericsson

- 6.4.14 Tata Consultancy Services (TCS)

- 6.4.15 Wipro Ltd

- 6.4.16 HCL Technologies Ltd

- 6.4.17 Cognizant Technology Solutions

- 6.4.18 NTT DATA Corporation

- 6.4.19 Capgemini SE

- 6.4.20 Kyndryl Holdings Inc.

- 6.4.21 Orange Business Services

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment