|

시장보고서

상품코드

1850045

자기공명영상(MRI) 시장 : 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Magnetic Resonance Imaging - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

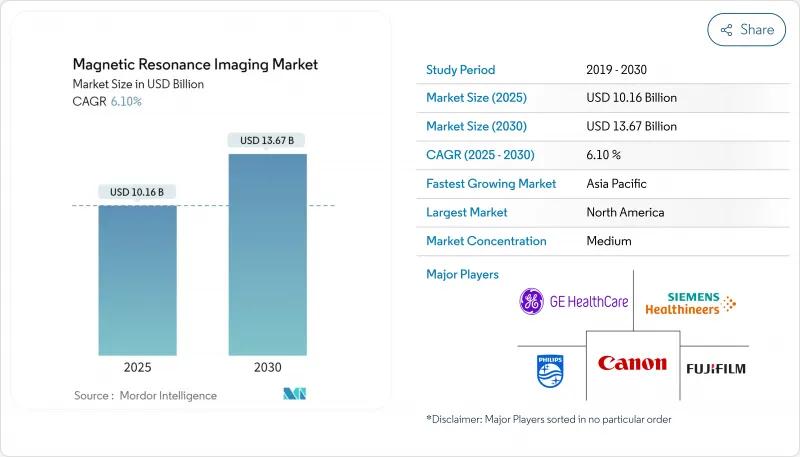

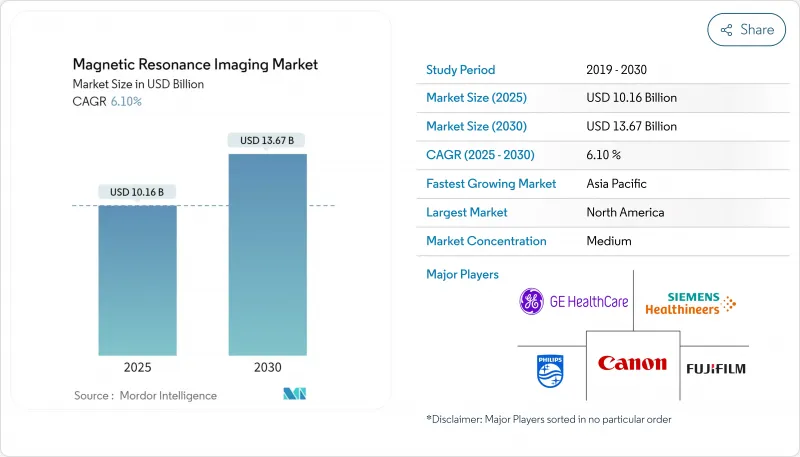

세계의 자기공명영상(MRI) 시장 규모는 2025년 101억 6,000만 달러로, 2030년까지 136억 7,000만 달러에 이를 것으로 예측되고 있으며, 예측기간 중 CAGR은 6.10%로 예상됩니다.

이 전망은 자기공명영상(MRI)이 보다 광범위한 자기공명영상(MRI) 산업에서 어떻게 현대 진단의 필수적인 기둥이 되고 있는지 강조합니다.

세계의 건강 관리를 지원하는 자기공명영상(MRI) 시장 규모는 임상가들이 자기공명영상(MRI)을 신경학, 종양학 및 순환기학의 일상적인 진단 경로에 통합함에 따라 계속 상승하고 있습니다. 병원은 자기공명영상(MRI)의 우수한 연부조직 콘트라스트를 높이 평가하고 있으며, 다른 검사에서 질병의 징후가 모호한 경우에도 보다 명확한 답변을 얻을 수 있습니다. 자기공명영상(MRI)은 환자를 전리 방사선에 노출시키지 않기 때문에 경제적 인센티브가 작동합니다. 설비 투자는 견조하게 추이하고 있어 여러 전문 분야에 걸쳐 스캐너의 가동률이 유지된다는 자신감을 느낄 수 있습니다. 소프트웨어, 특히 인공지능을 이용한 재구성은 구배 강도와 마찬가지로 구매 결정에 영향을 미치게 되었습니다. 휴대용 초저 자기장 장치는 집중 및 응급실에서 새로운 액세스 포인트를 생성합니다. 새로운 수확의 하나는 지불자가 진화하는 상환 정책이 관리자에게 화질과 의료 현장의 경제성의 균형을 잡도록 촉구하고 있다는 것입니다.

지역별 성장 패턴에서는 아시아태평양이 2025년부터 2030년까지 CAGR 8.80%라는 경이적인 성장률로 확대되는 반면, 북미는 2024년에 34%로 최대 시장 점유율을 차지했습니다. 신흥 시장에서는 비용 효율적인 헬륨 라이트 자석을 중시하는 반면 성숙 시장에서는 워크플로우의 자동화에 중점을 두고 있습니다. 미국에서 보고된 공인기사의 결원률 18.1%와 같은 노동력 부족은 하드웨어 용량이 풍부하더라도 스캐닝 룸의 처리능력을 저하시킵니다. 장비 구매 및 세트로 구성된 교육 프로그램은 이 병목 현상을 완화하는 것을 목표로합니다. 보험 확대, 특히 중국과 인도에서는 자기공명영상(MRI)을 3차 소개 영상 진단에서 최전선 진단 도구로 이동시키고 있습니다. 이 추세는 현지 인력 배치 및 진료 보상 실태에 부합하는 유통 전략이 미래의 수익원을 형성할 것임을 시사합니다.

세계의 자기공명영상(MRI) 시장 동향과 통찰

만성 및 노화 질환의 세계적인 증가

신경질환과 암은 상세한 해부학적 및 기능적 정보를 필요로 하기 때문에 자기공명영상(MRI)의 이용이 압도적으로 많습니다. 첨단 지역의 고령화에 의해 촬영률이 상승하고, 자기공명영상(MRI)의 조기 미세 구조 변화를 밝히는 능력이 조기 치료 개입을 촉진합니다. 종양학에서 확산 강조법과 동적 조영법은 침습적인 생검 없이 종양의 특징을 밝히는데 도움이 되었으며, 그 결과 자기공명영상(MRI)은 오늘날의 신경학적 영상 진단의 약 41%를 차지합니다. 대규모 암 센터에서는 병기 분류를 위해 전신 자기공명영상(MRI)이 일상적으로 채용되고 있어, 고채널 코일과 고도의 후처리 소프트웨어에 대한 일관된 수요로 이어지고 있습니다. 의료기관이 예방적 검진에 중점을 두게 되면, 반복 촬영을 실시하는 것으로 예측 가능한 검사 건수 증가가 초래됩니다.

최근 Medicare & Medicaid Service Center(CMS)의 제안에서 자기공명영상(MRI)의 안전 프로토콜을 다루는 6개의 새로운 CPT 코드가 추가되었으며 이전에 청구되지 않은 활동이 지불 가능한 워크플로우에 통합되었습니다. UnitedHealthcare와 같은 민간보험사는 많은 검사를 저비용 외래시설로 유도하는 서비스 시설 규칙을 설정하고 자석 배치 전략을 형성하고 있습니다. 현재 0.3T로 고정된 보험 상환 가능한 최소 자기장 강도는 구식 0.2T 시스템의 교체 사이클을 앞당깁니다. 따라서 관리자는 중자장과 고자장으로의 업그레이드를 정당화하는 재무 체질이 더욱 명확해지고 있습니다. 안전 활동이 수익화되고 시설 선정이 명확해짐에 따라 병원은 예산 편성의 확실성을 얻을 수 있습니다.

자기공명영상(MRI) 시스템의

구매가격은 기본 저자장장치가 15만 달러에서 고급 3T 장치로 300만 달러까지 폭넓습니다. 마그네틱 쉴드, 방진, 구조 보강 등 설치 장소 준비에도 상당한 비용이 듭니다. 헬륨 보충 및 서비스 계약과 같은 운전 비용은 투자 회수 기간을 늘립니다. 헬륨 라이트와 밀폐형 자석은 평생 비용을 낮추고 총 소유 비용 평가를 재구성합니다. 임대 옵션 및 공급업체 관리 서비스는 소규모 병원이 엄청난 초기 투자를 하지 않고 더 높은 사양의 장비를 얻는 데 도움이 됩니다. 이 비용 압력은 건설 비용을 피하는 휴대용 자기공명영상(MRI) 솔루션에 대한 관심을 자극합니다. 논리적 추론에 의하면 임상적으로 요구가 까다로운 환경에서도 경제성을 고려하면 저자장 기술이나 모듈 기술이 촉진된다는 것입니다.

부문 분석

2024년 자기공명영상(MRI) 시장 점유율은 폐쇄 자기공명영상(MRI) 시스템이 78%를 차지하며 고자장 임상 영상 진단의 이점을 반영합니다. 휴대용 스캐너는 2030년까지 연평균 복합 성장률(CAGR) 8.10%로 성장하여 신경 이미징을 침대 옆에 직접 제공합니다. Hyperfine의 FDA 승인 0.064T Swoop은 표준 전원에 연결하여 환자를 운반하지 않고도 신속한 뇌졸중 평가를 가능하게 합니다. AI에 의한 노이즈 제거는 저자장 신호의 한계를 상쇄하고 진단의 질을 유지합니다. 병원에서는 종합적인 검사를 위해 고자장 단위, 시간에 중요한 트리어지에는 휴대용 장비와 자원 할당을 개선하기 위해 혼합 플릿이 점점 도입되고 있습니다. 이러한 하이브리드 접근법은 아키텍처 선택이 화질뿐만 아니라 임상 워크플로우 요구 사항에 의존하는 경향을 강화합니다.

중자장 시스템(1.0-1.5T)은 2024년 자기공명영상(MRI) 시장 규모의 48%를 차지했으며 루틴 검사 비용과 성능의 균형을 맞추고 있습니다. 초고자장 자석(3T 초과)은 CAGR 7.20%로 급성장하여 신경과학과 종양학에 뛰어난 해상도를 제공합니다. United Imaging의 FDA 승인 5T 시스템은 더 높은 자기장 강도의 임상 사용에 대한 규제 기세를 보여줍니다. 초저자장(0.5T 미만) 장치는 휴대성이 S/N의 한계를 웃도는 포인트 오브 케어의 요구를 충족합니다. 최소 0.3T의 자기장 강도를 의무화하는 보험 상환 기준은 구식 0.2T 스캐너의 은퇴를 앞당깁니다. 임상의는 현재 보편적인 기준이 아니라 질병 경과 요건에 따라 필드 강도를 선택하고 있습니다.

지역 분석

2024년 자기공명영상(MRI) 시장 점유율은 북미가 34%로 가장 높았고, 이는 성숙한 보험상환제도와 조기 기술 도입에 뒷받침되었습니다. CMS는 자기공명영상(MRI)의 안전성에 대한 CPT 코드를 추가하여 임플란트 스크리닝 및 자석의 안전성 검사와 같은 작업을 공식화했습니다. 노동력 부족은 계속되고 있으며, 18.1%의 기사 결원이 자동화 투자를 촉구하고 있습니다. GE Healthcare의 SIGNA MAGNUS Head Only 3T 스캐너와 같은 혁신적인 제품이 FDA 허가를 받았으며 이 지역의 제품 리더로서의 입지를 강화하였습니다. 의료기관은 인력 부족을 보완하기 위해 AI 주도 워크플로우 솔루션에 대한 의존을 강화하고 있습니다. 이 역동적인 움직임은 규제, 노동력, 혁신이 일체화되어 지역의 기세를 뒷받침하고 있음을 보여줍니다.

아시아태평양은 2025년부터 2030년까지 지역에서 가장 빠른 CAGR 8.80%를 보일 것으로 예측됩니다. 중국과 인도의 인프라 투자가 스캐너의 설치를 뒷받침하고, 일본과 한국은 연구 및 고급 임상 업무에 초고자장 시스템을 채택합니다. 중국의 2024년 의료기기 및 공급망 혁신 백서는 차별화된 혁신과 비용 관리를 강조하고 있습니다. 인도의 Ayushman Bharat로 대표되는 공공 보험의 확대로 자기공명영상(MRI)의 대상이 되는 환자층이 확대되고 있습니다. 공급업체는 기본 액세스를 위한 헬륨 라이트 자석과 대도시 센터용 프리미엄 플랫폼을 결합한 단계적인 제품을 제공합니다. 이 패턴은 지리적 범위의 확대와 임상적 세련의 심화를 동시에 진행시키는 이중 확대 노선을 보여줍니다.

유럽은 보편적 보험 제도와 강력한 연구 네트워크를 통해 자기공명영상(MRI) 업계에서 여전히 유력한 지역입니다. 도입률은 다양하며 북유럽과 서유럽이 남유럽과 동유럽보다 빨리 신기술을 도입하고 있습니다. Max Plank Institute는 신경 생물학적 발견을 촉진하기 위해 9.4T 및 14.1T 스캐너를 운영합니다. EMA의 하모나이제이션은 회원국 간의 원활한 규제 인가를 촉진하고 기술의 보급을 촉진합니다. Siemens Hertiners가 영국의 초전도 자석 시설에 투자한 것은 유럽 제조 산업의 관련성을 강조합니다. 가치 기반 케어 모델은 의료의 질을 희생하지 않고 효율성을 실현하는 자기공명영상(MRI) 프로토콜의 단순화를 촉진합니다. 그 결과, 과학적 리더십과 광범위한 액세스를 결합한 균형 잡힌 성장이 실현됩니다.

기타 혜택:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 서포트

목차

제1장 서론

- 조사의 전제조건과 시장의 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 만성 질환 및 노화에 따른 질병의 세계 부담 증가

- 고가치 영상 진단 장치에 대한 상환 범위와 정부 지원 확대

- 자기공명영상(MRI)에서의 기술 혁신

- 세계 의료비 지출의 꾸준한 증가와 병원 및 외래환자의 영상 진단 인프라의 현대화

- 자기공명영상(MRI)의 임상 적응 확대

- 환자 중심의 비전리 진단 대체법으로 이행

- 시장 성장 억제요인

- 자기공명영상(MRI) 시스템의 고비용

- 환자의 안전성과 적합성에 대한 우려

- 인정된 자기공명영상(MRI) 기사의 부족

- 중소득국에서의 접근성의 제한

- 공급망 분석

- 규제와 상환의 전망

- 기술의 전망

- Porter's Five Forces 분석

- 신규 참가업체의 위협

- 구매자의 협상력

- 공급기업의 협상력

- 대체품의 위협

- 경쟁 기업간 경쟁 관계

제5장 시장 규모와 성장 예측

- 아키텍처별

- 폐쇄 자기공명영상(MRI) 시스템

- 개방 자기공명영상(MRI) 시스템

- 휴대용 및 포인트 오브 케어 자기공명영상(MRI) 시스템

- 전계 강도별

- 저자장(0.5T 이하) 자기공명영상(MRI) 시스템

- 중자장(1.0-1.5 T) 자기공명영상(MRI) 시스템

- 고자장(3T) 자기공명영상(MRI) 시스템

- 극고자장 및 초고자장(3T 초과) 자기공명영상(MRI) 시스템

- 이동성

- 고정 룸 시스템

- 모바일 트레일러 기반 시스템

- 용도별

- 신경학

- 종양학

- 심장병학

- 근골격

- 소화기내과 및 간장학

- 기타 용도

- 최종 사용자별

- 병원

- 진단 영상 센터

- 외래수술센터(ASC)

- 학술연구기관

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 기타 유럽

- 아시아태평양

- 중국

- 일본

- 인도

- 한국

- 호주

- 기타 아시아태평양

- 중동

- GCC

- 남아프리카

- 기타 중동

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 북미

제6장 경쟁 구도

- 시장 집중도

- 전략적 동향

- 시장 점유율 분석

- 기업 프로파일

- Siemens Healthineers AG

- GE HealthCare Technologies, Inc.

- Koninklijke Philips NV

- Canon Medical Systems Corp.

- Fujifilm Holdings Corp.

- United Imaging Healthcare Co., Ltd.

- Shenzhen Anke High-Tech Co., Ltd.

- Esaote SpA

- Hyperfine, Inc.

- Bruker Corporation

- FONAR Corporation

- Neusoft Medical Systems Co., Ltd.

- Aurora Healthcare US

- Medonica Co., Ltd.

- Time Medical Systems

- Aspect Imaging Ltd.

- IMRIS(Deerfield Imaging)

- Paramed Medical Systems

- Synaptive Medical

제7장 시장 기회와 장래의 전망

JHS 25.11.17The MRI market size is projected at USD 10.16 billion in 2025 and is expected to reach USD 13.67 billion by 2030, reflecting a compound annual growth rate (CAGR) of 6.10 % over the forecast period.

This outlook underscores how magnetic resonance imaging (MRI) is becoming an essential pillar of modern diagnostics within the broader MRI industry.

The MRI market size supporting global healthcare continues to climb as clinicians integrate MRI into routine diagnostic pathways for neurology, oncology, and cardiology. Hospitals value the modality's superior soft-tissue contrast, which delivers clearer answers when disease signs remain ambiguous on other scans. Economic incentives favor MRI because it does not expose patients to ionizing radiation, a growing concern among regulators and providers alike. Capital investment remains steady, showing confidence that scanners will stay busy across multiple specialities. Software-driven gains, especially artificial-intelligence-based reconstruction, now influence purchasing decisions as much as gradient strength. Portable and ultra-low-field devices create new access points inside intensive-care units and emergency rooms. One fresh takeaway is that payers' evolving reimbursement policies are nudging administrators to balance image quality with setting-of-care economics.

Regional growth patterns reveal Asia-Pacific expanding at an impressive 8.80 % CAGR between 2025 and 2030, while North America holds the largest MRI market share at 34 % in 2024. Manufacturers segment their offerings accordingly, emphasizing cost-effective helium-light magnets in emerging markets yet focusing on workflow automation in mature economies. Workforce shortages, such as the 18.1 % vacancy rate for certified technologists reported in the United States, temper scan-room throughput even where hardware capacity is abundant. Training programs bundled with equipment purchases aim to ease this bottleneck. Insurance expansion, especially in China and India, is shifting MRI from tertiary referral imaging toward a frontline diagnostic tool. The trend implies that distribution strategies aligned with local staffing and reimbursement realities will shape future revenue streams.

Global Magnetic Resonance Imaging Market Trends and Insights

Rising Global Burden of Chronic and Age-Related Diseases

Neurological disorders and cancer dominate MRI use because they require detailed anatomical and functional information. Aging populations in developed regions drive higher imaging rates, and MRI's ability to reveal early microstructural changes promotes earlier therapeutic intervention. In oncology, diffusion-weighted and dynamic contrast-enhanced techniques help characterize tumors without invasive biopsies, resulting in MRI commanding roughly 41% of all neurological imaging volumes today. Large cancer centers routinely adopt whole-body MRI for staging, leading to consistent demand for high-channel coils and advanced post-processing software. As institutions pivot toward preventive screening, repeat imaging creates predictable volume growth. An emerging inference is that reliable early detection converts occasional MRI users into regular patients, reinforcing scanner utilization.

Increasing Reimbursement Coverage and Government Support

Recent Centers for Medicare & Medicaid Services (CMS) proposals added six new CPT codes covering MRI safety protocols, embedding formerly unbilled activities into payable workflows . Private insurers such as UnitedHealthcare set site-of-service rules that channel many exams into lower-cost outpatient facilities, shaping magnet placement strategies. Minimum reimbursable field strength, now pegged at 0.3 T, accelerates replacement cycles for older 0.2 T systems. Administrators therefore find clearer financial justification for mid-field or higher-strength upgrades. With safety activities monetized and site selection clarified, hospitals gain budgeting certainty. The practical takeaway is that coding precision now directly influences equipment lifecycles and facility planning.

High Cost of MRI Systems

Purchase prices range from USD 150,000 for basic low-field devices to USD 3 million for advanced 3 T units. Site preparation-covering magnetic shielding, vibration control, and structural reinforcement-adds substantial expense. Operational costs such as helium refills and service contracts lengthen payback periods. Helium-light or sealed magnets lower lifetime costs, reshaping total-cost-of-ownership evaluations. Leasing options and vendor-managed services help smaller hospitals acquire higher-spec equipment without large upfront capital. This cost pressure stimulates interest in portable MRI solutions that bypass construction expenses. A logical inference is that economic considerations can promote lower-field or modular technology even in clinically demanding environments.

Other drivers and restraints analyzed in the detailed report include:

- Technological Breakthroughs in MRI

- Expanding Clinical Indications for MRI

- Shift Toward Patient-Centric, Non-Ionizing Diagnostic Alternatives

- Shortage of Certified MRI Technologists

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Closed MRI systems held 78% MRI market share in 2024, reflecting their dominance in high-field clinical imaging. Portable scanners, advancing at an 8.10% CAGR through 2030, bring neuro-imaging directly to bedside settings. Hyperfine's FDA-cleared 0.064 T Swoop connects to standard power, enabling rapid stroke assessments without patient transport. AI-driven denoising offsets low-field signal limits, sustaining diagnostic quality. Hospitals increasingly deploy mixed fleets-high-field units for comprehensive studies and portable devices for time-critical triage-improving resource allocation. This hybrid approach reinforces the trend that architecture choice now hinges on clinical workflow requirements rather than image quality alone.

Mid-field systems (1.0 T-1.5 T) commanded 48 % MRI market size in 2024, balancing cost and performance for routine exams. Ultra-high-field magnets (>3 T) grow fastest at 7.20 % CAGR, offering superior resolution for neuroscience and oncology. United Imaging's FDA-cleared 5 T system indicates regulatory momentum for clinical use of higher field strengths. Ultra-low-field ( <0.5 T) devices meet point-of-care needs where portability outweighs signal-to-noise limitations. Reimbursement criteria mandating a minimum 0.3 T field strength hasten the retirement of older 0.2 T scanners. Clinicians now select field strength based on disease pathway requirements rather than a universal standard.

The MRI Market Report Segments the Industry Into by Architecture (Closed MRI Systems, Open MRI Systems, and More), by Field Strength (Low Field, High Field, and More), by Mobility (Fixed Room Systems and Mobile Trailer-Based Systems), by Application (Oncology, Neurology, and More), End User (Hospitals, Diagnostic Imaging Centers, and More), and by Geography. The Market Sizes and Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America led with 34% MRI market share in 2024, supported by mature reimbursement frameworks and early technology uptake. CMS added CPT codes for MRI safety, formalizing tasks such as implant screening and magnet safety checks. Labor shortages persist, with an 18.1% technologist vacancy prompting automation investments. FDA clearances for innovations such as GE HealthCare's SIGNA MAGNUS head-only 3 T scanner reinforce the region's product-leadership status. Providers increasingly rely on AI-driven workflow solutions to offset staffing gaps. This dynamic shows that regulation, labor, and innovation collectively sustain regional momentum.

Asia-Pacific is forecast to post the fastest regional CAGR of 8.80% between 2025 and 2030. Infrastructure spending in China and India boosts scanner installations, while Japan and South Korea adopt ultra-high-field systems for research and advanced clinical work. China's 2024 Medical Device and Supply Chain Innovation White Paper emphasizes differentiated innovation and cost control. Expanding public insurance, notably India's Ayushman Bharat, enlarges the patient base eligible for MRI. Vendors offer tiered products, pairing helium-light magnets for basic access with premium platforms for metropolitan centers. The pattern shows dual-track expansion: widening geographic coverage and deepening clinical sophistication simultaneously.

Europe remains a heavyweight in the MRI industry owing to universal health coverage and strong research networks. Adoption rates vary, with Northern and Western Europe embracing new technologies faster than Southern and Eastern regions. The Max Planck Institute operates 9.4 T and 14.1 T scanners to further neuro-biological discovery . EMA harmonization promotes seamless regulatory approval across member states, expediting technology diffusion. Siemens Healthineers' investment in a UK superconducting-magnet facility underscores Europe's manufacturing relevance. Value-based-care models encourage abbreviated MRI protocols that deliver efficiency without sacrificing care quality. The result is balanced growth that couples scientific leadership with broad access.

- Siemens Healthineers

- GE HealthCare Technologies, Inc.

- Koninklijke Philips

- Canon

- Fujifilm Holdings Corp.

- United Imaging Healthcare Co., Ltd.

- Shenzhen Anke High-Tech Co., Ltd.

- Esaote S.p.A.

- Hyperfine, Inc.

- Bruker

- FONAR Corporation

- Neusoft

- Aurora Healthcare U.S.

- Medonica Co., Ltd.

- Time Medical Systems

- Aspect Imaging Ltd.

- IMRIS (Deerfield Imaging)

- Paramed Medical Systems

- Synaptive Medical

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising global burden of chronic and age-related diseases

- 4.2.2 Increasing reimbursement coverage and government support for high-value imaging modalities

- 4.2.3 Technological breakthroughs in MRI

- 4.2.4 Steady growth in healthcare spending and modernization of hospital & outpatient imaging infrastructure worldwide

- 4.2.5 Expanding clinical indications for MRI

- 4.2.6 Shift toward patient-centric, non-ionizing diagnostic alternatives

- 4.3 Market Restraints

- 4.3.1 High cost of MRI Systems

- 4.3.2 Safety and compatibility concerns for patients

- 4.3.3 Shortage of Certified MRI Technologists

- 4.3.4 Limited Accessibility in Middle Income Countries

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory & Reimbursement Outlook

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value)

- 5.1 By Architecture

- 5.1.1 Closed MRI Systems

- 5.1.2 Open MRI Systems

- 5.1.3 Portable / Point-of-Care MRI Systems

- 5.2 By Field Strength

- 5.2.1 Low-Field (<=0.5 T) MRI Systems

- 5.2.2 Mid-Field (1.0 T - 1.5 T) MRI Systems

- 5.2.3 High-Field (3 T) MRI Systems

- 5.2.4 Ultra-High & Very-High (>3 T) MRI Systems

- 5.3 By Mobility

- 5.3.1 Fixed Room Systems

- 5.3.2 Mobile Trailer-based Systems

- 5.4 By Application

- 5.4.1 Neurology

- 5.4.2 Oncology

- 5.4.3 Cardiology

- 5.4.4 Musculoskeletal

- 5.4.5 Gastroenterology & Hepatology

- 5.4.6 Other Applications

- 5.5 By End User

- 5.5.1 Hospitals

- 5.5.2 Diagnostic Imaging Centers

- 5.5.3 Ambulatory Surgery Centers

- 5.5.4 Academic & Research Institutes

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 Europe

- 5.6.2.1 Germany

- 5.6.2.2 United Kingdom

- 5.6.2.3 France

- 5.6.2.4 Italy

- 5.6.2.5 Spain

- 5.6.2.6 Rest of Europe

- 5.6.3 Asia-Pacific

- 5.6.3.1 China

- 5.6.3.2 Japan

- 5.6.3.3 India

- 5.6.3.4 South Korea

- 5.6.3.5 Australia

- 5.6.3.6 Rest of Asia-Pacific

- 5.6.4 Middle East

- 5.6.4.1 GCC

- 5.6.4.2 South Africa

- 5.6.4.3 Rest of Middle East

- 5.6.5 South America

- 5.6.5.1 Brazil

- 5.6.5.2 Argentina

- 5.6.5.3 Rest of South America

- 5.6.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company profiles (includes Global level Overview, Market level overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and analysis of Recent Developments)

- 6.4.1 Siemens Healthineers AG

- 6.4.2 GE HealthCare Technologies, Inc.

- 6.4.3 Koninklijke Philips N.V.

- 6.4.4 Canon Medical Systems Corp.

- 6.4.5 Fujifilm Holdings Corp.

- 6.4.6 United Imaging Healthcare Co., Ltd.

- 6.4.7 Shenzhen Anke High-Tech Co., Ltd.

- 6.4.8 Esaote S.p.A.

- 6.4.9 Hyperfine, Inc.

- 6.4.10 Bruker Corporation

- 6.4.11 FONAR Corporation

- 6.4.12 Neusoft Medical Systems Co., Ltd.

- 6.4.13 Aurora Healthcare U.S.

- 6.4.14 Medonica Co., Ltd.

- 6.4.15 Time Medical Systems

- 6.4.16 Aspect Imaging Ltd.

- 6.4.17 IMRIS (Deerfield Imaging)

- 6.4.18 Paramed Medical Systems

- 6.4.19 Synaptive Medical

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment