|

시장보고서

상품코드

1850069

적응형 보안 시장 : 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Adaptive Security - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

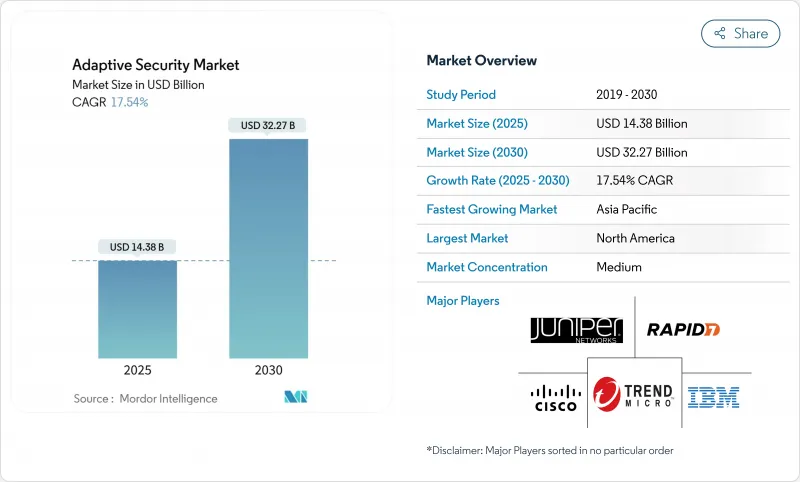

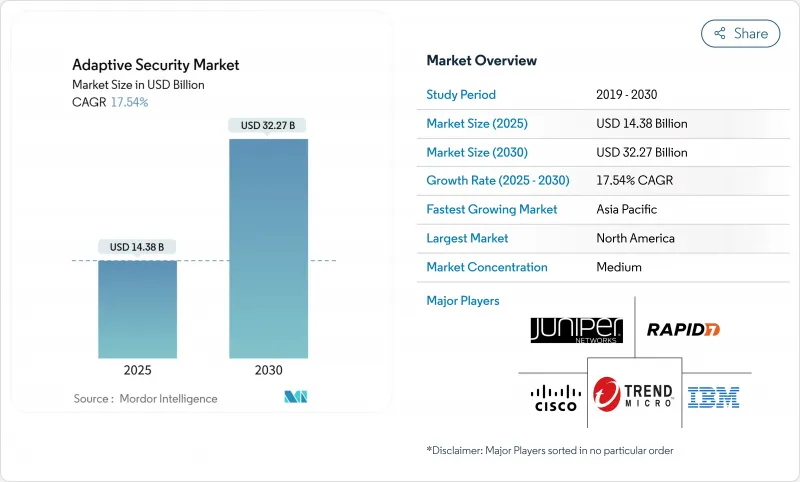

적응형 보안 시장의 2025년 시장 규모는 143억 8,000만 달러로 추정되고, 2030년에는 322억 7,000만 달러에 달할 것으로 예측되며, CAGR 17.54%로 견조하게 추이할 전망입니다.

이 확장은 경계 중심 방어에서 사용자 행동, 자산 컨텍스트 및 위협 인텔리전스를 실시간으로 분석하는 자체 학습 아키텍처로의 급속한 전환을 반영합니다. 정부에 의한 제로 트러스트의 의무화, 규제 당국에 의한 벌칙 강화, AI에 의한 공격 트래픽의 전례없는 증가에 의해 기업은 정적인 컨트롤을 폐지해, 계속적으로 조정되는 세이프 가드의 채용을 강요하고 있습니다. 벤더는 대규모 언어 모델을 통한 추론, 자동화된 정책 오케스트레이션, 행동 분석을 통합 플랫폼에 통합하여 감지 및 대응에 대한 평균 시간을 단축하고 관리 오버헤드를 줄입니다. 브랜드에 대한 손상이나 랜섬웨어에 대한 지불에 대한 이사회 수준의 우려가 높아지고, 능동적인 제어 비용을 초과하는 것이 일상화되어 조직적인 수요가 높아지고 있습니다.

세계의 적응형 보안 시장 동향 및 인사이트

AI가 생성하는 공격 트래픽이 규칙 기반 방어 능가

AI를 사용할 수 있게 된 적은 피싱, 취약성 발견, 가로 움직임을 자동화하고 시그니처 기반 도구를 피하는 트래픽 패턴을 생성합니다. CrowdStrike는 2025년에 에이전트형 AI 모듈을 발표하여 엔드포인트 및 클라우드 워크로드 전체에서 본 적이 없는 악성코드를 자율적으로 사냥하고 봉쇄할 수 있습니다. Darktrace의 자율 응답 엔진은 2025년 ClickFix 피싱 웨이브의 미티게이션과 같은 이미 의심스러운 세션을 미드스트림에서 차단하고 있습니다. 이러한 증거는 실시간 행동 모델이 정적 규칙 세트를 대체하는 방법을 보여주며, 사람의 조정 없이 정책을 개선하는 적응형 보안 시장 솔루션에 대한 수요를 강화합니다.

컴플라이언스 중심의 보안 투자를 촉진하는 규제 의무화

2025년에 시행된 EU의 NIS2 규제와 DORA 규제는 불충분한 사이버 관리에 대해 최대 1,000만 유로 또는 세계 매출의 2%의 제재금을 부과하는 것으로, 은행, 공익 기업, 디지털 서비스 제공업체에게 지속적인 감시와 최소 권한 액세스의 실시를 의무화하고 있습니다. 미국 연방 정부 기관도 대통령령 14028호 하에 유사한 압력에 직면하고 있으며, CISA의 제로 트러스트 성숙도 모델에는 2027년도까지의 단계적인 이정표가 상세하게 설명되어 있습니다. 미국 국방부는 2027년까지 모든 네트워크에 제로 트러스트의 틀을 의무화함으로써 이를 보완하고 있습니다. 이러한 의무화는 기업이 단일 컨트롤을 여러 규제에 대응할 수 있는 통합 플랫폼을 요구하는 가운데 적응형 보안 시장을 뒷받침하는 승수 효과를 창출합니다.

숙련된 사이버 보안 인력 부족

Varonis의 2025년 노동 스냅샷에 따르면 미국에서는 약 600,000명의 사이버 보안 담당자가 미취직이며 경험이 풍부한 실무 담당자의 실업률은 0%입니다. 소규모 기업과 아시아 중소기업이 가장 고전하고 있으며, 일본의 2024년 중소기업 조사에서는 사이버 대응에 대한 장벽의 톱은 인재 부족이라고 합니다. 이 갭은 매니지드 검출 및 대응 서비스를 촉구해, 적응형 보안 시장 서비스 부문의 CAGR 예측 17.8%에 박차를 가하고 있습니다. 포티넷은 FortiAnalyzer 2025에 GenAI 플레이북을 통합하여 기술 부족에 대응하고 이전에는 고급 분석가를 필요로 했던 경보를 희박한 팀에서 수행할 수 있도록 했습니다.

부문 분석

애플리케이션 보안의 적응형 보안 시장 규모는 2024년에는 52억 3,000만 달러로 평가되었고, API 악용이 증가했기 때문에 수익의 36.4%를 차지했습니다. Akamai의 2025 Apps and API 보고서에 따르면 API는 관찰된 모든 트래픽의 57%를 차지하고 점점 무기화되고 있습니다. 따라서 기업은 경계 게이트웨이를 우회하는 주입 공격을 차단하기 위해 런타임 검사, 스키마 검증 및 비헤이비어 기반 라이닝을 도입했습니다. 한편, 클라우드 보안은 제로 트러스트 정책 엔진이 컨테이너 오케스트레이터와 서버리스 런타임에 직접 통합되어 DevOps 팀에게 네이티브 세이프 가드를 제공함으로써 18.1%의 연평균 복합 성장률(CAGR)로 진보하고 있습니다. Syncloop과 같은 공급업체는 Kubernetes 클러스터에서 교사 없이 이상 감지를 수행하여 오감지를 줄이고 SOC의 피로를 줄입니다. 네트워크 및 엔드포인트 제어는 여전히 필수적이지만 플랫폼 번들에 수렴하기 때문에 구매자는 원격 측정 파이프라인을 간소화하고 킬 체인 혁신을 자동화할 수 있습니다.

2024년 매출의 62.6%는 솔루션이 차지했는데, 감지, 대응, 컴플라이언스 보고를 전문가에게 아웃소싱함으로써 서비스의 적응형 보안 시장 규모가 더욱 확대됩니다. 스킬 부족과 24시간 365일의 커버 요구는 포춘 500 기업조차도 매니지드 오케스트레이션으로 향하게 합니다. 광 네트워크 고객에 대한 Ciena 사례 연구는 서비스 제공업체가 AI 주도의 위협 분석을 연결 거래로 패키징하여 산업 고객의 설비 투자 및 기술 부담을 줄일 수 있음을 보여줍니다. 서비스 제공업체는 멀티테넌트 SIEM과 AIOps를 활용하여 고객당 비용을 절감하고 거친 이자율을 확대함으로써 기술 구매자가 툴 소유보다 성과를 선호하는 사이클을 강화하고 있습니다.

적응형 보안 시장은 용도별(애플리케이션 보안, 네트워크 보안 등), 제공 제품별(솔루션 및 서비스), 전개 모델별(온프레미스 및 클라우드 유형), 최종 사용자별(은행, 금융서비스 및 보험(BFSI), 정부 기관, 방위 등), 지역별로 세분화됩니다. 시장 예측은 금액(달러)으로 제공됩니다.

지역별 분석

북미 점유율 32.8%는 초기 제로 트러스트 시험 운영, 벤처 자금 두께, 연방 정부 지출로 인한 것입니다. 대통령령 14028과 CISA 지침은 연방 정부 기관에 지속적인 인증의 도입을 의무화하고 공급망에서 민간 모방에 박차를 가하고 있습니다. Microsoft는 Security Copilot으로 전환하는 정부 기관에 규정된 청사진을 제공하여 지역 전반에 모범 사례의 보급을 가속화하고 있습니다. 현지 인재 풀과 발달한 사이버 보험 시장도 고보장 상품의 프리미엄 가격을 유지하고 있습니다.

아시아태평양의 2030년까지 연평균 복합 성장률(CAGR)은 19.3%로 가장 빠르게 상승할 전망입니다. 일본 사이버 보안 전략 회의는 포스트 양자암호와 위협 정보 공유를 통합하는 국내 벤더를 육성하기 위해 관민의 연구개발 프로그램에 1조 2,000억 엔을 기록했습니다. 싱가포르의 스마트 국가 구상은 AI SOC 자동화에 자금을 투입하는 한편 다국적 제조업체는 동남아시아로 시설을 이전해 스마트 공장에 적응한 세이프 가드를 요구하고 있습니다. AI 보안 특허에서는 중국이 우세하며 2023년 세계 출원 건수의 70%를 차지했고, 인근 국가들에 지역 혁신과 국경을 넘어선 위협 공유 협정의 가속을 육박합니다.

유럽은 규제 강화를 배경으로 견조한 성장을 기록하고 있습니다. NIS2는 에너지, 물, 운송 사업자에게 공급망의 견고화를 검증하도록 강제했으며, DORA는 유사한 규칙을 금융 사업자로 확대했습니다. ENISA의 2025년 조사에서는 정책 채용률은 86%였지만, 예산 배분은 47%에 그쳤고, 턴키 매니지드 서비스에 대한 수요 증가를 시사하고 있습니다. 이번 사이버 레지리언스 법에서는 적용 범위가 모든 디지털 제품으로 확대되기 때문에 가전제품기업 간에 새로운 조달이 활발해지고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 서포트

목차

제1장 서론

- 조사의 전제조건 및 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 사이버 공격의 양과 교묘함 증대

- 규제 의무(GDPR(EU 개인정보보호규정), CCPA, DORA, NIS2 등)

- 엔터프라이즈 클라우드와 SaaS의 확대에는 제로 트러스트 제어 필요

- AI 생성 공격 트래픽이 룰 베이스의 방어 상회

- 지속적인 리스크 스코어링을 필요로 하는 머신 투 머신 ID의 급증

- 5G 네트워크 슬라이싱이 마이크로 세분화 도입 촉진

- 시장 성장 억제요인

- 숙련된 사이버 보안 인력의 부족

- 브라운필드 IT자산의 높은 TCO 및 복잡한 통합

- 독자적인 프로토콜을 갖춘 레거시 OT/ICS 환경

- 멀티 클라우드 배포의 데이터 주권 충돌

- 공급망 분석

- 규제 상황

- 기술 전망(AI, UEBA, SSE, 마이크로 세분화, PQC)

- Porter's Five Forces 분석

- 공급기업의 협상력

- 구매자의 협상력

- 신규 참가업체의 위협

- 대체품의 위협

- 경쟁 기업간 경쟁 관계

- 시장의 거시 경제 동향 평가

제5장 시장 규모 및 성장 예측

- 용도별

- 애플리케이션 보안

- 네트워크 보안

- 엔드포인트 보안

- 클라우드 보안

- 기타

- 제공별

- 솔루션

- 서비스

- 전개 모델별

- 온프레미스

- 클라우드 기반

- 최종 사용자별

- BFSI

- 정부 및 방위

- 제조업(인더스트리 4.0)

- 헬스케어 및 생명과학

- 에너지 및 유틸리티

- 기타

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 유럽

- 영국

- 독일

- 프랑스

- 스웨덴

- 기타 유럽

- 아시아태평양

- 중국

- 일본

- 인도

- 호주

- 한국

- 기타 아시아태평양

- 중동 및 아프리카

- 사우디아라비아

- 아랍에미리트(UAE)

- 튀르키예

- 남아프리카

- 기타 중동 및 아프리카

- 북미

제6장 경쟁 구도

- 시장 집중도

- 전략적 움직임(MandA, 자금 조달, 제품 출시)

- 시장 점유율 분석

- 기업 프로파일

- Cisco Systems

- IBM Corp.

- Fortinet

- Palo Alto Networks

- Trend Micro

- Rapid7

- Check Point Software

- Juniper Networks

- Trellix

- CrowdStrike

- Zscaler

- Illumio

- Lumen Technologies

- Aruba(HPE)

- Microsoft Security

- Okta

- Netskope

- Darktrace

- Akamai/Guardicore

- WatchGuard(Panda)

제7장 시장 기회 및 향후 전망

AJY 25.11.05The adaptive security market is valued at USD 14.38 billion in 2025 and is forecast to reach USD 32.27 billion by 2030, advancing at a robust 17.54% CAGR.

This expansion mirrors the rapid shift from perimeter-centric defenses to self-learning architectures that analyze user behavior, asset context, and threat intelligence in real time. Government zero-trust mandates, sharper regulatory penalties, and an unprecedented rise in AI-driven attack traffic are forcing enterprises to retire static controls and adopt continuously tuned safeguards. Vendors are embedding large-language-model reasoning, automated policy orchestration, and behavior analytics into unified platforms, reducing mean time to detect and respond while lowering administrative overhead. Organic demand is amplified by mounting board-level concern over brand damage and ransomware payouts that routinely exceed the cost of proactive controls.

Global Adaptive Security Market Trends and Insights

AI-Generated Attack Traffic Outpacing Rule-Based Defenses

AI-enabled adversaries now automate phishing, vulnerability discovery, and lateral movement, generating traffic patterns that evade signature-based tools. CrowdStrike launched agentic AI modules in 2025 that autonomously hunt and contain never-seen malware across endpoints and cloud workloads.Darktrace's autonomous response engine already blocks suspicious sessions mid-stream, such as its 2025 mitigation of ClickFix phishing waves. These proof points illustrate how real-time behavior models supersede static rule sets, cementing demand for adaptive security market solutions that refine policies without human tuning.

Regulatory Mandates Driving Compliance-Driven Security Investments

The EU NIS2 and DORA regulations that took effect in 2025 impose fines up to EUR 10 million or 2% of global turnover for inadequate cyber controls, forcing banks, utilities, and digital service providers to implement continuous monitoring and least-privilege access. U.S. federal agencies face identical pressure under Executive Order 14028, with CISA's Zero-Trust Maturity Model detailing phased milestones through fiscal 2027.The U.S. Department of Defense complements this with a mandatory zero-trust framework for all networks by 2027. Together, these mandates create a multiplier effect that boosts the adaptive security market as firms seek unified platforms capable of mapping a single control to multiple regulations.

Shortage of Skilled Cybersecurity Talent

There are nearly 600,000 unfilled U.S. cybersecurity roles, and experienced practitioners enjoy zero percent unemployment, according to Varonis' 2025 labor snapshot. Small firms and Asian SMEs struggle most, with Japan's 2024 SME survey showing staff shortages as the top cyber-readiness barrier. This gap encourages managed detection and response services and fuels the 17.8% CAGR forecast for the Services segment within the adaptive security market. Fortinet answered the skills crunch by embedding GenAI playbooks into FortiAnalyzer 2025, enabling lean teams to triage alerts that formerly required senior analysts.

Other drivers and restraints analyzed in the detailed report include:

- Enterprise Cloud and SaaS Sprawl Necessitating Zero-Trust Controls

- Surge in Machine-to-Machine Identities Requiring Continuous Risk Scoring

- High TCO and Integration Complexity for Brownfield IT Estates

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Adaptive security market size for Application Security stood at USD 5.23 billion in 2024 and preserved a 36.4% slice of revenue owing to heightened API exploitation. Akamai's 2025 Apps and API report revealed that APIs account for 57% of all observed traffic and are increasingly weaponized. Enterprises therefore deploy runtime inspection, schema validation, and behavior baselining to block injection attacks that bypass perimeter gateways. Cloud Security, meanwhile, advances at an 18.1% CAGR as zero-trust policy engines embed directly into container orchestrators and serverless runtimes, giving DevOps teams native safeguards. Vendors such as Syncloop layer unsupervised anomaly detection over Kubernetes clusters, reducing false positives and easing SOC fatigue. Network and endpoint controls remain essential but converge into platform bundles so buyers can streamline telemetry pipelines and automate kill-chain disruption.

Despite Solutions retaining 62.6% of 2024 sales, the adaptive security market size for Services will grow faster as boards outsource detection, response, and compliance reporting to experts. Skills shortages and 24X7 coverage needs push even Fortune 500 firms toward managed orchestration. Ciena's case study on optical network customers shows service providers packaging AI-driven threat analytics into connectivity deals, offloading capex and skill burdens for industrial clients. Service providers leverage multitenant SIEMs and AIOps to reduce per-customer cost and expand gross margin, reinforcing a cycle where technology buyers prefer outcomes over tool ownership.

Adaptive Security Market is Segmented by Application (Application Security, Network Security, and More), Offering (Solutions and Services), Deployment Model (On-Premises and Cloud-Based), End User (BFSI, Government and Defense, and More), and by Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America's 32.8% share stems from early zero-trust pilots, venture funding depth, and federal spending. Executive Order 14028 and CISA guidance obligate federal agencies to deploy continuous authentication, spurring private-sector imitation in supply chains. Microsoft provides prescriptive blueprints for agencies migrating to Security Copilot, accelerating best-practice diffusion across the region. Local talent pools and a well-developed cyber-insurance market also sustain premium pricing for high-assurance products.

Asia-Pacific is set for the fastest climb at a 19.3% CAGR through 2030. Japan's Cybersecurity Strategy Council earmarked JPY 1.2 trillion for public-private R&D programs, fostering domestic vendors that integrate post-quantum cryptography and threat-intel sharing. Singapore's Smart Nation blueprint injects funding for AI SOC automation, while multinational manufacturers relocate facilities to Southeast Asia and demand adaptive safeguards for smart factories. China's dominance in AI security patents, accounting for 70% of 2023 global filings, puts pressure on neighbors to accelerate local innovation and cross-border threat-sharing pacts.

Europe records solid growth on the back of regulatory heft. NIS2 forces energy, water, and transport operators to verify supply-chain hardening, while DORA extends similar rules to financial entities. ENISA's 2025 survey showed 86% policy adoption but only 47% budget allocation, implying pent-up demand for turnkey managed services. The upcoming Cyber Resilience Act broadens coverage to all digital products, fueling fresh procurements among consumer-electronics manufacturers.

- Cisco Systems

- IBM Corp.

- Fortinet

- Palo Alto Networks

- Trend Micro

- Rapid7

- Check Point Software

- Juniper Networks

- Trellix

- CrowdStrike

- Zscaler

- Illumio

- Lumen Technologies

- Aruba (HPE)

- Microsoft Security

- Okta

- Netskope

- Darktrace

- Akamai / Guardicore

- WatchGuard (Panda)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Escalating volume and sophistication of cyber-attacks

- 4.2.2 Regulatory mandates (GDPR, CCPA, DORA, NIS2, etc.)

- 4.2.3 Enterprise cloud and SaaS sprawl needing zero-trust controls

- 4.2.4 AI-generated attack traffic outpacing rule-based defenses

- 4.2.5 Surge in machine-to-machine identities requiring continuous risk scoring

- 4.2.6 5G network-slicing driving micro-segmentation adoption

- 4.3 Market Restraints

- 4.3.1 Shortage of skilled cyber-security talent

- 4.3.2 High TCO and integration complexity for brown-field IT estates

- 4.3.3 Legacy OT/ICS environments with proprietary protocols

- 4.3.4 Data-sovereignty conflicts in multi-cloud deployments

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook (AI, UEBA, SSE, micro-segmentation, PQC)

- 4.7 Porter's Five Force Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

- 4.8 Assesment of Macroeconomic Trends on the Market

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Application

- 5.1.1 Application Security

- 5.1.2 Network Security

- 5.1.3 Endpoint Security

- 5.1.4 Cloud Security

- 5.1.5 Others

- 5.2 By Offering

- 5.2.1 Solutions

- 5.2.2 Services

- 5.3 By Deployment Model

- 5.3.1 On-premise

- 5.3.2 Cloud-based

- 5.4 By End User

- 5.4.1 BFSI

- 5.4.2 Government and Defense

- 5.4.3 Manufacturing (Industry 4.0)

- 5.4.4 Healthcare and Life Sciences

- 5.4.5 Energy and Utilities

- 5.4.6 Others

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 United Kingdom

- 5.5.3.2 Germany

- 5.5.3.3 France

- 5.5.3.4 Sweden

- 5.5.3.5 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 India

- 5.5.4.4 Australia

- 5.5.4.5 South Korea

- 5.5.4.6 Rest of Asia-Pacific

- 5.5.5 Middle East and Africa

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 United Arab Emirates

- 5.5.5.3 Turkey

- 5.5.5.4 South Africa

- 5.5.5.5 Rest of Middle East and Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves (MandA, funding, product launches)

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Cisco Systems

- 6.4.2 IBM Corp.

- 6.4.3 Fortinet

- 6.4.4 Palo Alto Networks

- 6.4.5 Trend Micro

- 6.4.6 Rapid7

- 6.4.7 Check Point Software

- 6.4.8 Juniper Networks

- 6.4.9 Trellix

- 6.4.10 CrowdStrike

- 6.4.11 Zscaler

- 6.4.12 Illumio

- 6.4.13 Lumen Technologies

- 6.4.14 Aruba (HPE)

- 6.4.15 Microsoft Security

- 6.4.16 Okta

- 6.4.17 Netskope

- 6.4.18 Darktrace

- 6.4.19 Akamai / Guardicore

- 6.4.20 WatchGuard (Panda)

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment