|

시장보고서

상품코드

1850081

스마트 웨어러블 시장 : 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Smart Wearable - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

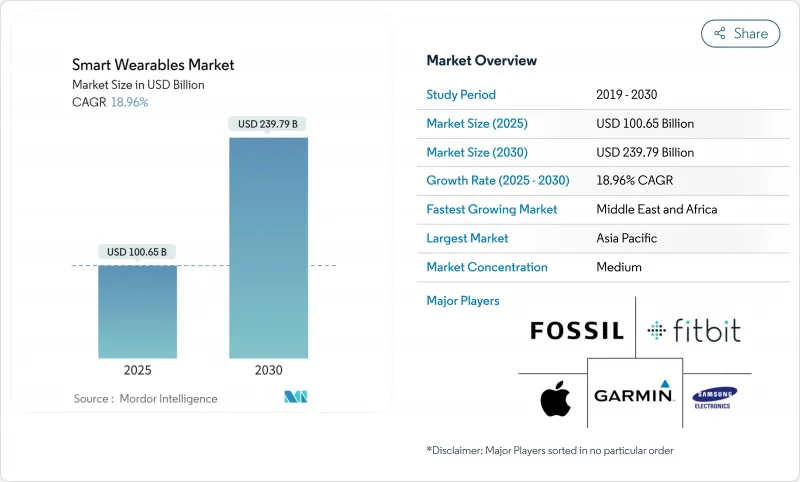

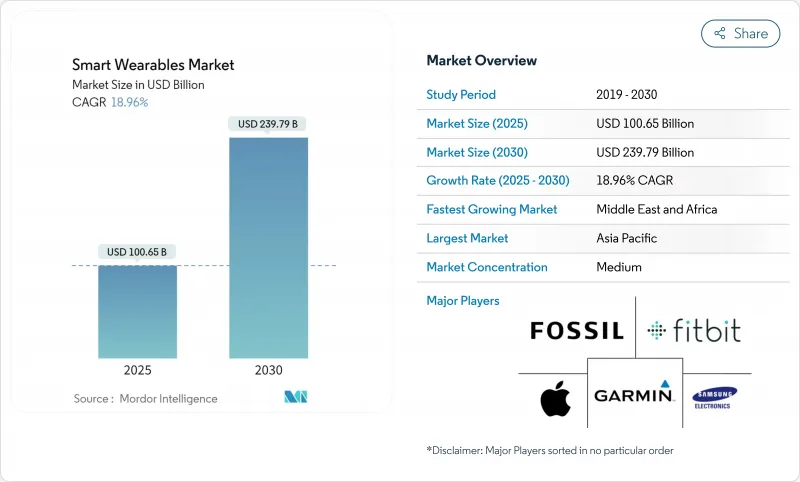

스마트 웨어러블 시장 규모는 2025년에 1,006억 5,000만 달러로 추정되고, 2030년에는 2,397억 9,000만 달러에 이를 것으로 예측되며, CAGR 18.96%로 성장할 전망입니다.

센서의 기술 혁신이 가속화되고, 디바이스의 AI가 향상되며, 휴대폰의 이용 사례가 확대됨으로써, 가벼운 웰니스부터 규제가 있는 헬스케어까지, 이용 사례가 확대되고 있습니다. 원격 모니터링에 대한 보험 회사의 환불 증가, 기업 안전 의무화 증가, 5G 독립 실행형 배치로 새로운 대응 가능한 부문이 개척되고 있습니다. 하드웨어는 여전히 지배적이지만 경상적인 서비스 수입은 공급업체의 경제성을 재구성하고 있습니다. 스마트 웨어러블 시장 전반에 걸쳐 플랫폼 중심의 전략과 크로스 디바이스 에코 시스템이 사용자 유지와 평생 가치의 결정자가 되고 있습니다.

세계의 스마트 웨어러블 시장 동향 및 인사이트

북미에서 심장 원격 모니터링을 위한 웨어러블 보험 승인 획득

2025년 의사 보상 체계에서 원격 환자 모니터링 코드의 급속한 채용이 1차 케어 클리닉에서 ECG 클래스 웨어러블 처방의 동기부여가 되고 있습니다. 환자 1인당 월액 15-110달러의 환불에 의해 의료 제공업체의 비용 장벽이 저하되고, 병원에서는 울혈성 심부전에 의한 재입원이 15% 감소한 것으로 보고되고 있습니다. 미국 클리닉의 거의 3분의 1은 만성기 의료 워크플로우에 지속적인 모니터링을 통합하여 에피소드 데이터 수집에서 종단 데이터 수집으로의 중요한 변화를 반영합니다. 환자 복용 어드히어런스의 향상은 연결되지 않은 폼 팩터와 임상의의 실시간 피드백 루프로 인해 스마트 웨어러블 시장의 성장 전망을 강화하고 있습니다.

'건강 중국 2030'에 근거한 중국의 겸용 스마트 워치 보조금

라이프스타일과 의료 기능을 모두 제공할 수 있는 인증된 기기의 소매 가격 일부를 환불하는 정부의 우대조치는 현지 연구개발과 국내 수요를 자극하고 있습니다. 샤오미와 화웨이와 같은 브랜드는 이 프로그램을 활용하여 출하량을 확대하여 SpO2 등급 센서와 부정맥 검출 알고리즘의 출시 시간을 단축했습니다. 이 정책은 또한 가전 및 의료기기의 표준을 조화시켜 아시아태평양 시장 전체의 수출에 대한 규제 마찰을 완화합니다.

유럽의 클라우드 컴패니언 앱을 제한하는 데이터 상주 의무화

EU의 규제 당국은 현재 의료 데이터를 지역 국경 내에 배치할 것을 의무화하고 있으며, 공급업체는 로컬 처리 스택을 구축하거나 기능 다운등급의 위험을 감수해야 합니다. 중소기업은 컴플라이언스 비용 상승에 직면하지만, 기밀 데이터 공유에 대한 사용자의 의욕은 여전히 낮아 네트워크 효과로 인한 이점이 억제되고 있습니다. 아키텍처가 세분화됨에 따라 업데이트주기가 길어지고 여러 지역의 출시가 복잡해질 수 있으며 유럽에서 스마트 웨어러블 시장의 단기 확장이 억제됩니다.

부문 분석

2024년 매출 점유율은 스마트 워치가 46.5%로 선두를 유지했습니다. 플래그십 모델은 멀티 밴드 GPS, ECG, 의료 등급 광전식 혈압계를 결합하고 저온 폴리실리콘 OLED 패널로 배터리 수명을 향상시키고 있습니다. 듀얼 센서 어레이는 FDA 클래스 Ⅱ 요구 사항을 준수하는 심방 세동 경고를 지원하며 스마트 웨어러블 시장 전체에서 임상 유용성 제안을 강화하고 있습니다.

스마트 링과 보석은 소형화된 MCU 패키지와 솔리드 스테이트 배터리가 3그램 폼 팩터로 지속적인 SpO2 및 심박수 추적을 지원하기 때문에 가장 빠른 성장을 기록합니다. 프리미엄 모델은 수면 최적화를 목표로 하고 있지만 대중 모델은 겸손한 활동 로깅을 강조합니다. 히어러블은 온도 센서와 인지 부하 센서를 통합하여 범주형 실적를 넓히고 직장 안전 프로그램에 오디오 우선 게이트웨이를 생성합니다. 피트니스 트래커는 회복 분석과 VO2 기반 교육 준비로 고급화되고, 헤드 마운트 디스플레이는 수술 지침 및 현장 유지 보수로 지지를 모으고 있습니다. 초기 세대의 스마트 텍스타일은 자세 교정과 스트레스 검출을 위해 신축 가능한 전극을 내장하고 있으며, 스마트 웨어러블 시장의 일상복에 대한 미래의 확대를 시사하고 있습니다.

코어 실리콘, 광학 모듈, 전지가 2024년 매출의 74.1%를 차지했습니다. 공급업체는 부정맥과 혈중 산소 이상 장치에서 분류를 허용하는 신경 가속을 갖춘 6 나노 미터 칩셋을 개발했습니다. 유연한 AMOLED 패널과 저손실 RF 프론트엔드는 효율성을 향상시키고 플래그십 시계는 단일 충전 내구성을 7일로 연장됩니다.

정기적인 서비스는 프리미엄 분석, 개인화된 코칭 및 EHR 통합을 배경으로 성장하고 있습니다. 공급업체는 AI 기반 수면 개선 계획 및 영양 지도를 월별 요금으로 번들하여 사용자당 평균 수익을 높이고 업그레이드 주기를 원활하게 하고 있습니다. 소프트웨어는 여전히 접착제 층이며, 장치의 수명을 연장하고 스마트 웨어러블 시장에서 생태계의 잠금을 강화하는 무선 기능 확장을 지원합니다.

지역 분석

아시아태평양이 2024년 매출의 34.9%를 차지했습니다. 수직 통합 공급망을 통해 급속한 비용 절감과 2개월의 모델 업데이트가 가능합니다. 정부 프로그램에 의한 ECG 대응 웨어러블에 대한 보조금은 최초 구매자와 만성질환 환자에 대한 보급이 진행됩니다.

북미는 조기 의료 자격 증명과 견고한 지불자 참여를 지원하며 여전히 프리미엄의 중심지입니다. 원격 환자 모니터링의 보험 상환은 장치에 대한 액세스를 확대하고 기관 조사를 통해 예측 모델을 검증하고 스마트 웨어러블 시장의 신뢰를 강화합니다.

유럽에서는 왕성한 수요와 엄격한 데이터 주권 규칙의 균형을 맞추고 있습니다. 벤더는 GDPR(EU 개인정보보호규정)을 준수하기 위해 에지 전용 애널리틱스와 지역 내 데이터 레이크를 배포하고 기업의 안전 의무화로 히어러블 배포를 가속화하고 있습니다.

중동 및 아프리카는 CAGR 20.7%로 가장 높은 성장률을 나타내고 있으며, 이는 5G의 고급 보급과 서비스가 부족한 커뮤니티에 대한 케어 확대에 웨어러블을 활용하는 국가적인 e헬스 설계도가 촉매가 되고 있습니다. 남미에서는 환율 변동과 5G의 비용으로 보급에 편차가 보이지만, 브라질과 멕시코에서는 현지화 파트너십 및 웰니스 보조금이 기세를 가져오고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 서포트

목차

제1장 서론

- 조사의 전제조건 및 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 북미의 심장 원격 모니터링용 보험 승인 웨어러블

- 건강 중국 2030을 통한 중국의 듀얼 유스(소비자용+의료용) 스마트 워치 보조금

- EU의 하이브리드 워크 안전 기준이 기업용 히어러블의 도입을 견인(포스트 COVID)

- 바늘을 사용하지 않고 지속적인 혈당 모니터링을 가능하게 하는 AI 온칩 웨어러블의 대두

- 미국 병사 치사성 프로그램에 기초한 방위 외골격의 조달

- 동남아시아 건설 부문에서 종량제 산업용 외골격 임대

- 시장 성장 억제요인

- 유럽의 데이터 레지던시 의무화에 의한 클라우드 컴패니언 앱의 제한

- 초박형 스마트 워치에 있어서 고밀도 배터리의 열폭주의 우려

- 제스처 기반 스마트 링에 대한 특허 라이선스 소송 비용

- 중남미의 낮은 ARPU가 5G 독립형 웨어러블의 전개 제한

- 업계 생태계 분석

- 기술의 전망

- Porter's Five Forces 분석

- 공급기업의 협상력

- 구매자의 협상력

- 신규 참가업체의 위협

- 대체품의 위협

- 경쟁 기업 간 경쟁 관계

- 투자 및 자금 조달 분석

제5장 시장 규모 및 성장 예측(가치)

- 제품별

- 스마트 워치

- 히어러블(귀에 장착하는 유형 및 스마트 이어폰)

- 피트니스 및 액티비티 트래커

- 헤드 마운트 디스플레이(AR/VR/MR)

- 스마트 의류 및 섬유

- 바디 카메라

- 스마트 링 및 보석

- 의료용 웨어러블 패치 및 바이오 센서

- 파워드 엑소 스켈레톤

- 컴포넌트별

- 하드웨어

- 소프트웨어 및 앱

- 서비스 및 구독

- 커넥티비티 테크놀로지별

- Bluetooth

- 셀룰러(3G/4G/LTE-M)

- 5G 독립형

- NFC/RFID

- Wi-Fi/무선 LAN

- 기타(UWB, ANT)

- 용도별

- 가전제품 및 라이프스타일

- 헬스케어 및 의료

- 피트니스 및 스포츠

- 산업 및 기업의 안전

- 군사 및 방위

- 유통 채널별

- 온라인(브랜드 E 스토어, 마켓플레이스)

- 오프라인(가전 양판점, 전문점, 클리닉)

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 기타 유럽

- 아시아태평양

- 중국

- 일본

- 한국

- 인도

- 동남아시아

- 기타 아시아태평양

- 남미

- 브라질

- 기타 남미

- 중동 및 아프리카

- 중동

- 아랍에미리트(UAE)

- 사우디아라비아

- 기타 중동

- 아프리카

- 남아프리카

- 기타 아프리카

- 북미

제6장 경쟁 구도

- 시장 집중도

- 전략적 동향

- 시장 점유율 분석

- 기업 프로파일

- Apple Inc.

- Samsung Electronics Co. Ltd

- Alphabet Inc.(Fitbit and Google Pixel)

- Garmin Ltd

- Huawei Technologies Co. Ltd

- Xiaomi Corp.

- BOBOVR

- Sony Corp.

- Microsoft Corp.

- Meta Platforms Inc.(Oculus)

- Huami Corp.(Zepp Health)

- Withings SA

- Omron Healthcare Inc.

- Cyberdyne Inc.

- Ekso Bionics Holdings Inc.

- GoPro Inc.

- Fossil Group Inc.

- Nuheara Ltd.

- Bragi GmbH

- Sensoria Inc.

- AIQ Smart Clothing Inc.

- Polar Electro Oy

- Coros Wearables Inc.

제7장 시장 기회 및 향후 전망

AJY 25.11.05The smart wearable market size stands at USD 100.65 billion in 2025 and is forecast to reach USD 239.79 billion by 2030, advancing at an 18.96% CAGR.

Accelerating sensor innovation, better on-device AI, and broader cellular coverage are expanding use cases from casual wellness to regulated healthcare. Growing insurer reimbursement for remote monitoring, rising enterprise safety mandates, and 5G Stand-Alone roll-outs are opening new addressable segments. Hardware remains dominant, yet recurring services revenue is reshaping vendor economics. Platform-centric strategies and cross-device ecosystems are becoming decisive for user retention and lifetime value across the smart wearable market.

Global Smart Wearable Market Trends and Insights

Insurance-approved wearables for cardiac remote monitoring in North America

Rapid adoption of remote patient monitoring codes under the 2025 Physician Fee Schedule is motivating primary-care practices to prescribe ECG-class wearables. Monthly reimbursements of USD 15-110 per patient lower cost barriers for providers, and hospitals report 15% fewer readmissions for congestive heart failure.] Nearly one-third of US clinics have already embedded continuous monitoring into chronic-care workflows, reflecting a material shift from episodic to longitudinal data capture. Higher patient adherence stems from untethered form factors and real-time clinician feedback loops, reinforcing the growth outlook of the smart wearable market.

China's dual-use smartwatch subsidies under Healthy China 2030

Government incentives that reimburse part of the retail price for devices certified to deliver both lifestyle and medical functions are stimulating local R&D and domestic demand. Brands such as Xiaomi and Huawei leveraged the program to scale unit shipments, accelerating time-to-market for SpO2-grade sensors and arrhythmia detection algorithms. The policy is also harmonizing consumer electronics and medical device standards, reducing regulatory friction for exports across the wider Asia-Pacific smart wearable market.

Data-residency mandates limiting cloud companion apps in Europe

EU regulators now require health data to reside within regional borders, compelling vendors to build local processing stacks or risk feature downgrades. Smaller players face higher compliance costs, while user willingness to share sensitive data remains low, curbing network-effect benefits. Fragmented architectures can lengthen update cycles and complicate multi-region releases, tempering the near-term expansion of the smart wearable market in Europe.

Other drivers and restraints analyzed in the detailed report include:

- Enterprise-grade hearables shaped by EU hybrid-work norms

- Rise of AI-on-chip wearables enabling non-invasive glucose monitoring

- High-density battery thermal-runaway concerns in ultra-slim smartwatches

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Smartwatches retained clear leadership in 2024 with a 46.5% revenue share. Flagship models combine multi-band GPS, ECG, and medical-grade photoplethysmography while improving battery life through low-temperature poly-silicon OLED panels. Dual-sensor arrays support atrial-fibrillation alerts that comply with FDA Class II requirements, strengthening the clinical utility proposition across the smart wearable market.

Smart rings and jewelry record the fastest growth as miniaturized MCU packages and solid-state batteries support continuous SpO2 and heart-rate tracking in a 3-gram form factor. Premium variants target sleep optimization, whereas mass-market models emphasize discreet activity logging. Hearables broaden the category footprint by integrating temperature and cognitive-load sensors, creating an audio-first gateway into workplace safety programs. Fitness trackers move upscale into recovery analytics and VO2-based training readiness, while head-mounted displays gain traction in surgical guidance and field maintenance. Early-generation smart textiles embed stretchable electrodes for posture correction and stress detection, hinting at future expansion of the smart wearable market into everyday apparel.

Core silicon, optical modules, and batteries accounted for 74.1% of 2024 revenue. Suppliers advance 6-nanometer chipsets with neural acceleration to enable on-device classification for arrhythmia and blood-oxygen anomalies. Flexible AMOLED panels and low-loss RF front ends improve efficiency, extending single-charge endurance to seven days on flagship watches.

Recurring services are growing on the back of premium analytics, personalized coaching, and EHR integration. Vendors bundle AI-based sleep improvement plans or nutrition guidance into monthly tiers, lifting average revenue per user and smoothing upgrade cycles. Software remains the glue layer, supporting over-the-air feature extensions that lengthen device lifetimes and fortify ecosystem lock-in in the smart wearable market.

The Smart Wearable Market Report is Segmented by Product (Smartwatches, Hearables, and More), Component (Hardware, Software and Apps, and Services and Subscriptions), Connectivity Technology (Bluetooth/BLE, Cellular, and More), Application/End-use (Consumer Electronics and Lifestyle, Healthcare and Medical, and More), Distribution Channel (Online, Offline), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia Pacific held 34.9% of 2024 revenue. Vertically integrated supply chains enable rapid cost declines and two-month model refreshes. Government programs subsidize ECG-enabled wearables, raising adoption among first-time buyers and chronic-disease patients.

North America remains the premium epicenter, underpinned by early medical credentialing and robust payer engagement. Reimbursement for remote patient monitoring widens device access, and institutional research validates predictive models, reinforcing trust in the smart wearable market.

Europe balances strong demand with strict data-sovereignty rules. Vendors deploy edge-only analytics and in-region data lakes to comply with GDPR, while corporate safety mandates accelerate hearables roll-outs.

The Middle East and Africa post the highest growth at 20.7% CAGR, catalyzed by 5G Advanced coverage and national e-health blueprints that leverage wearables to extend care to under-served communities. South America sees uneven uptake due to currency swings and 5G cost, but localization partnerships and wellness subsidies in Brazil and Mexico provide momentum.

- Apple Inc.

- Samsung Electronics Co. Ltd

- Alphabet Inc. (Fitbit and Google Pixel)

- Garmin Ltd

- Huawei Technologies Co. Ltd

- Xiaomi Corp.

- BOBOVR

- Sony Corp.

- Microsoft Corp.

- Meta Platforms Inc. (Oculus)

- Huami Corp. (Zepp Health)

- Withings SA

- Omron Healthcare Inc.

- Cyberdyne Inc.

- Ekso Bionics Holdings Inc.

- GoPro Inc.

- Fossil Group Inc.

- Nuheara Ltd.

- Bragi GmbH

- Sensoria Inc.

- AIQ Smart Clothing Inc.

- Polar Electro Oy

- Coros Wearables Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Insurance-approved Wearables for Cardiac Remote Monitoring in North America

- 4.2.2 China's Dual-Use (Consumer + Medical) Smartwatch Subsidies through Healthy China 2030

- 4.2.3 Enterprise-grade Hearables Adoption Driven by EU's Hybrid-Work Safety NormsPost-COVID

- 4.2.4 Rise of AI-on-Chip Wearables Enabling Continuous Glucose Monitoring without Needles

- 4.2.5 Defense Exoskeleton Procurements under United States Soldier Lethality Program

- 4.2.6 Pay-as-you-Lift Industrial Exoskeleton Leasing in South-East Asia's Construction Sector

- 4.3 Market Restraints

- 4.3.1 Data-Residency Mandates Limiting Cloud Companion Apps in Europe

- 4.3.2 High-Density Battery Thermal Runaway Concerns in Ultra-Slim Smartwatches

- 4.3.3 Patent-Licensing Litigation Costs for Gesture-Based Smart Rings

- 4.3.4 Low ARPU in LATAM Limiting 5G Stand-alone Wearable Roll-outs

- 4.4 Industry Ecosystem Analysis

- 4.5 Technological Outlook

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Bargaining Power of Suppliers

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Threat of New Entrants

- 4.6.4 Threat of Substitute Products

- 4.6.5 Intensity of Competitive Rivalry

- 4.7 Investment and Funding Analysis

5 MARKET SIZE AND GROWTH FORECASTS (VALUES)

- 5.1 By Product

- 5.1.1 Smartwatches

- 5.1.2 Hearables (Ear-Worn/Smart Earbuds)

- 5.1.3 Fitness and Activity Trackers

- 5.1.4 Head-Mounted Displays (AR/VR/MR)

- 5.1.5 Smart Clothing and Textiles

- 5.1.6 Body-worn Cameras

- 5.1.7 Smart Rings and Jewelry

- 5.1.8 Medical Wearable Patches and Biosensors

- 5.1.9 Powered Exoskeletons

- 5.2 By Component

- 5.2.1 Hardware

- 5.2.2 Software and Apps

- 5.2.3 Services and Subscriptions

- 5.3 By Connectivity Technology

- 5.3.1 Bluetooth/BLE

- 5.3.2 Cellular (3G/4G/LTE-M)

- 5.3.3 5G Stand-Alone

- 5.3.4 NFC/RFID

- 5.3.5 Wi-Fi/WLAN

- 5.3.6 Others (UWB, ANT+)

- 5.4 By Application/End-use

- 5.4.1 Consumer Electronics and Lifestyle

- 5.4.2 Healthcare and Medical

- 5.4.3 Fitness and Sports

- 5.4.4 Industrial and Enterprise Safety

- 5.4.5 Military and Defense

- 5.5 By Distribution Channel

- 5.5.1 Online (Brand E-store, Marketplaces)

- 5.5.2 Offline (Consumer Electronics Stores, Specialty, Clinics)

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 Europe

- 5.6.2.1 Germany

- 5.6.2.2 United Kingdom

- 5.6.2.3 France

- 5.6.2.4 Italy

- 5.6.2.5 Spain

- 5.6.2.6 Rest of Europe

- 5.6.3 Asia-Pacific

- 5.6.3.1 China

- 5.6.3.2 Japan

- 5.6.3.3 South Korea

- 5.6.3.4 India

- 5.6.3.5 South East Asia

- 5.6.3.6 Rest of Asia-Pacific

- 5.6.4 South America

- 5.6.4.1 Brazil

- 5.6.4.2 Rest of South America

- 5.6.5 Middle East and Africa

- 5.6.5.1 Middle East

- 5.6.5.1.1 United Arab Emirates

- 5.6.5.1.2 Saudi Arabia

- 5.6.5.1.3 Rest of Middle East

- 5.6.5.2 Africa

- 5.6.5.2.1 South Africa

- 5.6.5.2.2 Rest of Africa

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)}

- 6.4.1 Apple Inc.

- 6.4.2 Samsung Electronics Co. Ltd

- 6.4.3 Alphabet Inc. (Fitbit and Google Pixel)

- 6.4.4 Garmin Ltd

- 6.4.5 Huawei Technologies Co. Ltd

- 6.4.6 Xiaomi Corp.

- 6.4.7 BOBOVR

- 6.4.8 Sony Corp.

- 6.4.9 Microsoft Corp.

- 6.4.10 Meta Platforms Inc. (Oculus)

- 6.4.11 Huami Corp. (Zepp Health)

- 6.4.12 Withings SA

- 6.4.13 Omron Healthcare Inc.

- 6.4.14 Cyberdyne Inc.

- 6.4.15 Ekso Bionics Holdings Inc.

- 6.4.16 GoPro Inc.

- 6.4.17 Fossil Group Inc.

- 6.4.18 Nuheara Ltd.

- 6.4.19 Bragi GmbH

- 6.4.20 Sensoria Inc.

- 6.4.21 AIQ Smart Clothing Inc.

- 6.4.22 Polar Electro Oy

- 6.4.23 Coros Wearables Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment