|

시장보고서

상품코드

1850096

의료용 전원 시장 : 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Medical Power Supply - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

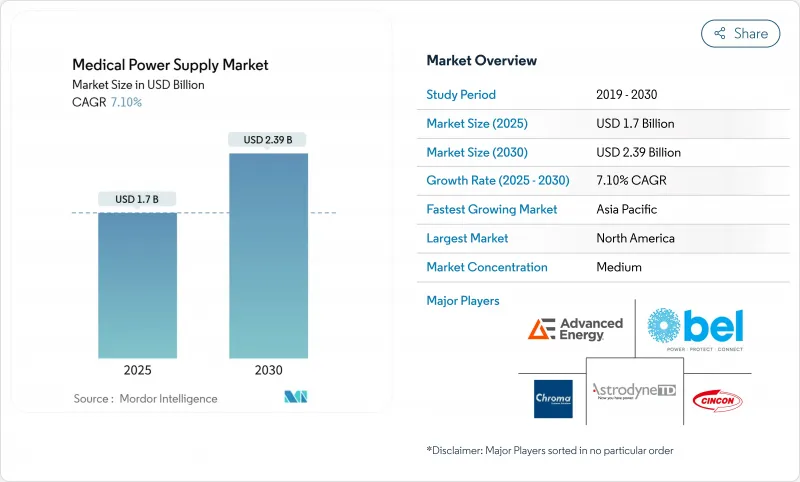

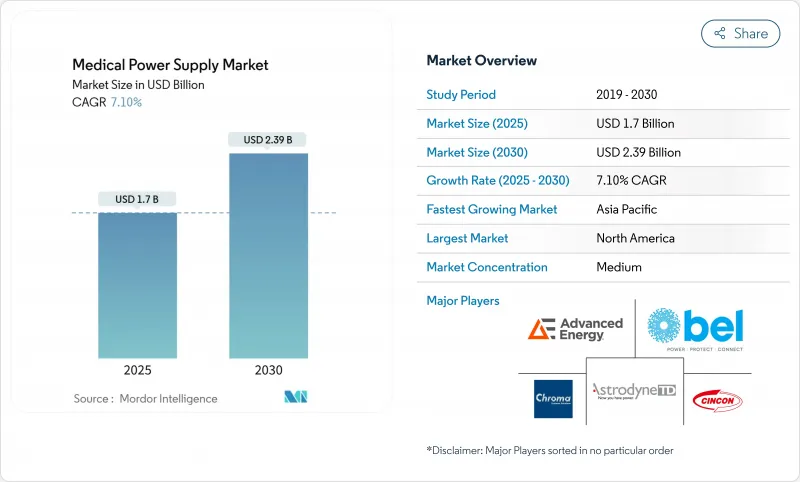

의료용 전원 시장 규모는 2025년에 17억 달러, 2030년에는 23억 9,000만 달러에 이를 것으로 예측되며, 기간 중 CAGR은 7.10%를 나타낼 전망입니다.

이 시장 확대는 건강 관리의 디지털화 가속화, 안전 표준의 엄격화, 휴대용 및 임상 장비의 콤팩트하고 효율적인 아키텍처의 추진을 반영합니다. GaN과 SiC로 대표되는 와이드 밴드갭 반도체의 채택은 95% 이상의 변환 효율과 40% 가까운 설치 면적의 삭감을 가능하게 하고, 공급자에게 측정 가능한 비용과 성능의 이점을 가져옵니다. 90% 이상의 효율 솔루션에 대한 규제 당국의 요구는 외래 환자용 이미지 플릿과 가정용 모니터링 장비 증가와 함께 성숙 경제권과 신흥 경제권 모두에서 기세를 유지하고 있습니다. 북미는 견고한 인프라와 조기 기술 도입을 통해 리더십을 유지하고 아시아태평양은 대규모 제조 인센티브와 정책 지원으로 성장을 이끌고 있습니다.

세계의 의료용 전원 시장 동향과 통찰

GaN 및 SiC 스위칭 디바이스를 통한 신속한 소형화

와이드 밴드갭 반도체는 95% 이상의 변환 효율을 유지하면서 스위칭 주파수를 1MHz 이상으로 끌어올려 임상 기기와 휴대용 기기의 소형 경량화를 가능하게 합니다. 300mm GaN 웨이퍼로 전환하여 제조 비용을 30% 절감하고 프리미엄 플랫폼 이외에의 보급을 촉진합니다. 케임브리지 건 디바이세스가 확보한 3,200만 달러의 시리즈 C와 같은 투자자의 지원은 추가 30%의 에너지 절약 가능성에 대한 자신감을 보여줍니다. 의료기기 OEM은 이러한 이점을 활용하여 제품 설치 면적을 최대 40% 축소하고 소규모 진료소에 적합한 컴팩트한 CT 및 MRI 시스템을 도입함으로써 충분한 서비스를 받지 못한 지역의 진단 액세스를 확대합니다.

외래환자센터에서 영상 진단 장비 확대

병원에서 영상 서비스로의 이전은 가변적인 전기 환경을 위해 설계된 전력 장치에 대한 수요를 증가시킵니다. Vizient에 따르면 외래 센터가 용량을 확장함에 따라 CT 스캔과 PET 스캔 수량이 두 자릿수 성장하고 있다고 합니다. 노스캐롤라이나 침례 병원에서의 최근 조치와 같이 조사용 스캐너를 임상용으로 전환하는 것은 이러한 분산화의 추세를 보여줍니다. 전원 공급 장치는 단계적인 장비 도입 및 AI 지원 이미지 처리 워크플로우를 지원하기 위해 강력한 EMI 억제, 유연한 입력 범위 및 모듈식 확장성을 제공해야 합니다.

IEC 60601-1 "제4판" EMC 업그레이드 비용

강화된 EMC 규칙과 리스크 관리 프로토콜은 컴플라이언스를 매우 복잡하게 만듭니다. 테스트 사이클은 약 3주이며, 유럽 노티파이드 바디의 용량은 드문 일이기 때문에 중소기업의 직접 비용은 15-25% 상승합니다. 많은 OEM들은 제품 출시를 지연시키고 혁신을 저해하는 EU MDR 병목 현상을 헤쳐 나가면서, 미국 시장 진출 경로를 우선시하고 있습니다. 타임라인을 관리하고 금리를 확보하기 위해서는 사내 규제 대응 팀과 조기 적합 설계에 대한 투자가 필수적입니다.

부문 분석

AC-DC 전원은 시설의 주전원을 직접 이용하는 대형 화상 진단 시스템 및 수술 시스템에서 널리 사용되고 있기 때문에 2024년 의료용 전원 시장 점유율의 77.42%를 차지했습니다. DC-DC 전원은 2030년까지 10.7%의 연평균 복합 성장률(CAGR)을 보일 것으로 예측됩니다. 이는 엄격한 효율 예산으로 여러 안정화 레일을 필요로 하는 모듈형 전자기기의 파도를 타고 있기 때문입니다. 의료용 전원 시장은 여전히 AC-DC의 신뢰성을 강조하고 있지만, OEM 로드맵은 전력을 분배하고 열 핫스팟을 완화하기 위해 온보드 DC-DC 스테이지가 점점 통합되어 있습니다. Traco와 Recom의 GaN 기반 DC-DC 컨버터는 현재 95% 이상의 효율과 500kHz 스위칭을 달성하여 기판 면적을 40% 절약하고 있습니다. 휴대용 주입 펌프, 산소 농축기 및 웨어러블 진단이 복잡해짐에 따라 공급업체는 DC-DC 포트폴리오를 확대하고 보다 광범위한 의료용 전원 시장에서 수익원을 확대하고 있습니다.

병원 장비 장비에서 멀티 킬로와트 AC-DC 블록은 여전히 필수적입니다. 그러나 핸드헬드 ECG 및 내시경 시스템을 위한 소형 DC-DC 모듈에 대한 주문 구성은 꾸준히 이동하고 있으며 소형 고주파 설계에 대한 미래 수요가 커지고 있다고 판매자는 보고했습니다. 2030년까지는 DC-DC 유닛의 매출이 30%를 초과할 수 있어 의료용 전원 시장에서의 경쟁적 위치가 재구축됩니다. 지속적인 효율성 향상, 갈바닉 절연 기술 및 디지털 텔레메트릭의 통합은 기존 사업자와 전문 사업자의 차별화를 촉진합니다.

폐쇄형 아키텍처는 2024년에 36.7%의 매출을 획득했는데, 이는 수술실 및 집중 치료실 내에서 엄격한 감염 관리 기준과 EMI 실드의 요구를 반영한 것입니다. 그러나 외부 어댑터는 2025년부터 2030년까지 연평균 복합 성장률(CAGR) 9.6%로 견고합니다. 의료용 전원 시장에서 환자를 고전압으로부터 격리하는 설계가 평가되었으며 OEM은 BF 용도 유형으로 인증된 클래스 II 외장 벽돌을 채택하도록 촉구합니다. SL Power의 ME 시리즈는 어댑터의 진화를 보여주며, 가정용 기기의 2XMOPP 절연과 <50µA 누설 임계값에 적합합니다.

공기 흐름과 인클로저 통합이 인클로저 요구를 상쇄하는 비용에 중점을 둔 분석기에서는 오픈 프레임 보드가 계속되고 있습니다. 구성 가능한 플랫폼은 SKU의 신속한 사용자 정의를 가능하게 하며 특수 이미지 처리 및 실험실 자동화 시스템의 설계 사이클을 단축합니다. 수리 가능성과 재활용 가능성을 장려하는 환경법은 의료용 전원 시장 전체의 모듈 방식을 더욱 강화합니다. 이에 따라 공급업체는 유지보수 대시보드에 공급하는 디지털 텔레메트리 옵션을 확장하고 북미와 유럽에서 시험적으로 배포된 power-as-a-service 모델을 지원합니다.

의료용 전원 시장은 기술별(AC-DC 전원, DC-DC 전원), 유형별(오픈 프레임, 밀폐형, 기타), 전력 범위별(0-50W, 51-200W, 기타), 용도별(진단·이미지 기기, 환자 모니터링, 수술·생명 유지, 기타), 지역별로 분류되어 있습니다. 시장 예측은 금액(달러)으로 제공됩니다.

지역 분석

북미는 2024년에 37.1%의 매출을 유지해 1,560억 달러의 국내 기기 지출과 시장 투입까지의 시간을 단축하는 FDA 경로의 합리화에 뒷받침됩니다. 2025년 국방위생계획에서는 장비의 현대화를 위해 402억 7,000만 달러가 할당되어 수요를 더욱 증가시킵니다. 탈탄소화에 대한 높은 관심은 ESG 스코어카드를 도입한 병원에서 90% 초효율 GaN 공급의 급속한 보급을 촉진합니다.

아시아태평양은 2030년까지 연평균 복합 성장률(CAGR)이 가장 빠른 9.8%를 기록, 인도의 디바이스 시장은 생산 연동 장려금으로 500억 달러의 평가를 목표로 하고 있습니다. 지역의 OEM이 GaN과 SiC의 생산 능력을 확대하는 것도 과제는 남아 있습니다. 연구개발비는 경비의 불과 0.5%에 그치고 정밀 자석과 커패시터의 수입 의존도는 여전히 높습니다. 무역 긴장 시나리오에서는 이 부문의 수익이 연간 236억 달러 감소할 수 있으며 공급망의 탄력성에 대한 필요성이 강조됩니다.

유럽의 엄격한 MDR 프레임워크는 적합성을 복잡하게 하고 있으며, 약 500,000대의 장치를 커버하는 단지 43개의 노티파이드 바디가 있기 때문에 승인에 상당한 지연이 발생하고 있습니다. 그럼에도 불구하고 강력한 지속가능성 지침과 공공 부문의 에너지 목표는 초고효율 의료용 전원 시장 솔루션에 대한 관심을 지속하고 있습니다. MedTech Europe는 그린 인프라에 대한 의료 시스템 투자를 지원하면서 혁신 파이프라인을 유지하기 위한 규제 개혁을 제창하고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 서포트

목차

제1장 서론

- 조사의 전제조건과 시장의 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- GaN 및 SiC 스위칭 디바이스에 의한 급속한 소형화

- 외래 센터에서의 진단 영상 장치의 확장

- 재택 환자 모니터링 기기의 급증

- 탈탄소화, 90% 이상의 전환 효율 PSU 추진 의무화

- 디지털 제어, 원격 감시 공급 유닛(Power-as-a-Service)

- 시장 성장 억제요인

- IEC 60601-1 「제4판」 EMC 업그레이드 비용

- 고전압 MOSFET의 반도체 공급망 불안정성

- 관세에 의한 중국제 자기 부품과 커패시터의 가격 상승

- 1인치 미만의 오픈 프레임 설계에 있어서의 열 관리의 한계

- 업계 밸류체인 분석

- 규제 상황

- 기술의 전망

- 업계의 매력 - Porter's Five Forces 분석

- 신규 참가업체의 위협

- 공급기업의 협상력

- 소비자의 협상력

- 대체품의 위협

- 경쟁 기업간 경쟁 관계

- 거시 경제 요인이 시장에 미치는 영향

제5장 시장 규모와 성장 예측

- 기술별

- AC-DC 전원

- DC-DC 전원

- 유형별

- 오픈 프레임

- 엔클로즈

- 외부/어댑터

- 구성 가능/모듈식

- 파워 레인지별

- 0-50W

- 51-200W

- 201-1000W

- 1000W 이상

- 용도별

- 진단 및 화상 진단 기기

- 환자 모니터링

- 수술과 생명유지

- 가정용 헬스케어 기기

- 기타

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 남미

- 브라질

- 아르헨티나

- 칠레

- 기타 남미

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 러시아

- 기타 유럽

- 아시아태평양

- 중국

- 인도

- 일본

- 한국

- 싱가포르

- 말레이시아

- 호주

- 기타 아시아태평양

- 중동 및 아프리카

- 중동

- 아랍에미리트(UAE)

- 사우디아라비아

- 튀르키예

- 기타 중동

- 아프리카

- 남아프리카

- 나이지리아

- 기타 아프리카

- 북미

제6장 경쟁 구도

- 시장 집중도

- 전략적 동향

- 시장 점유율 분석

- 기업 프로파일

- Advanced Energy Industries Inc.

- Astrodyne TDI Corp.

- Bel Power Solutions(CUI Inc.)

- Chroma Systems Solutions Inc.

- Cincon Electronics Co. Ltd

- Cosel Co. Ltd

- Delta Electronics Inc.

- FRIWO AG

- GlobTek Inc.

- Inventus Power

- Mean Well Enterprises Co. Ltd

- Murata Power Solutions Inc.

- Powerbox International AB

- Power-One Inc.(Bel Fuse)

- Puls GmbH

- RECOM Power GmbH

- Shenzhen Huyssen Power Co. Ltd

- SL Power Electronics

- Spellman High Voltage Electronics Corp.

- SynQor Inc.

- TDK-Lambda Corporation

- Traco Power Group

- TT Electronics plc

- Vitec Power GmbH

- Wall Industries Inc.

제7장 시장 기회와 미래 동향

- 화이트 스페이스와 언멧 요구의 평가

The medical power supply market size is at USD 1.70 billion in 2025 and is forecast to reach USD 2.39 billion by 2030, advancing at a 7.10% CAGR over the period.

Expansion reflects accelerated healthcare digitization, stricter safety codes, and the push for compact, high-efficiency architectures in portable and clinical equipment. Adoption of wide-bandgap semiconductors, notably GaN and SiC, enables conversion efficiencies above 95% and footprint reductions near 40%, giving suppliers measurable cost and performance advantages. Regulatory demands for >90% efficiency solutions, coupled with rising outpatient imaging fleets and home-based monitoring devices, sustain momentum across mature and emerging economies. North America retains leadership due to robust infrastructure and early technology adoption, while Asia-Pacific leads growth, powered by large-scale manufacturing incentives and policy support.

Global Medical Power Supply Market Trends and Insights

Rapid Miniaturisation via GaN and SiC Switching Devices

Wide-bandgap semiconductors raise switching frequencies beyond 1 MHz while sustaining better than 95% conversion efficiency, enabling smaller, lighter supplies for clinical and portable gear. Transitioning to 300 mm GaN wafers trims production cost 30%, encouraging uptake beyond premium platforms. Investor backing, such as the USD 32 million Series C secured by Cambridge GaN Devices, signals confidence in further 30% energy-saving potential. Medical device OEMs leverage these gains to shrink product footprints up to 40% and introduce compact CT and MRI systems suited to smaller clinics, broadening diagnostic access across underserved regions.

Expansion of Diagnostic-Imaging Fleets in Outpatient Centres

Migration of imaging services away from hospitals increases demand for power units designed for variable electrical environments. Vizient reports double-digit volume growth in CT and PET scans as ambulatory centres broaden capacity. Converting research scanners to clinical use, like recent actions at North Carolina Baptist Hospital, illustrates this decentralisation trend. Power supplies must deliver strong EMI suppression, flexible input ranges, and modular scalability to support phased equipment roll-outs and AI-enabled imaging workflows.

IEC 60601-1 "4th-Edition" EMC Upgrade Costs

Enhanced EMC rules and risk-management protocols impose significant compliance complexity. Test cycles of roughly three weeks and sparse notified-body capacity in Europe raise direct costs by 15-25% for smaller firms. Many OEMs prioritise the U.S. route to market while navigating EU MDR bottlenecks that slow product launches and dampen innovation. Investment in in-house regulatory teams and early design-for-compliance practices becomes essential to manage timelines and preserve margin.

Other drivers and restraints analyzed in the detailed report include:

- Surge in Home-Based Patient Monitoring Equipment

- Decarbonisation Mandates Pushing >90% Conversion-Efficiency PSUs

- Semiconductor Supply-Chain Volatility for High-Voltage MOSFETs

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

AC-DC devices accounted for 77.42% of medical power supply market share in 2024 thanks to their ubiquity in large imaging and surgical systems that tap direct facility mains. DC-DC supplies are forecast to post a 10.7% CAGR through 2030, riding the wave of modular electronics that demand multiple regulated rails with tight efficiency budgets. The medical power supply market continues to value AC-DC reliability, yet OEM roadmaps increasingly embed on-board DC-DC stages to distribute power and mitigate thermal hotspots. GaN-based DC-DC converters from Traco and Recom now achieve >95% efficiency and 500 kHz switching, unlocking 40% board-area savings. As portable infusion pumps, oxygen concentrators, and wearable diagnostics gain complexity, suppliers widen DC-DC portfolios to capture incremental revenue streams within the broader medical power supply market.

In hospital capital equipment, multi-kilowatt AC-DC blocks remain indispensable. Yet distributors report a steady shift in order mix toward smaller DC-DC modules for handheld ECG and endoscopy systems, reinforcing future demand for miniature high-frequency designs. By 2030, DC-DC units could exceed 30% revenue, reshaping competitive positioning within the medical power supply market. Continuous efficiency hikes, galvanic isolation techniques, and integration of digital tele-metrics drive differentiation between incumbents and specialist entrants.

Enclosed architectures captured 36.7% revenue in 2024, a reflection of stringent infection-control norms and EMI shielding needs inside operating rooms and intensive care. However, external adapters exhibit a robust 9.6% CAGR between 2025 and 2030 as care settings migrate to homes and community clinics. The medical power supply market rewards designs that isolate patients from high voltages, prompting OEMs to adopt Class II external bricks certified for Type BF applications. SL Power's ME series illustrates adapter evolution, meeting 2XMOPP insulation and <50 µA leakage thresholds for home devices.

Open-frame boards continue in cost-sensitive analyzers where airflow and chassis integration offset enclosure needs. Configurable platforms allow rapid SKU customisation, cutting design cycles for specialty imaging and lab automation systems. Environmental legislation encouraging repairability and recyclability further strengthens modular approaches across the medical power supply market. Suppliers accordingly expand digital telemetry options that feed maintenance dashboards, supporting power-as-a-service models rolled out in pilot schemes across North America and Europe.

Medical Power Supply Market is Segmented by Technology (AC-DC Power Supply and DC-DC Power Supply), Type (Open-Frame, Enclosed, and More), Power Range (0-50 W, 51-200 W, and More), Application (Diagnostic and Imaging Equipment, Patient Monitoring, Surgical and Life-Support, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America retained 37.1% revenue in 2024, supported by USD 156 billion in domestic device spending and streamlined FDA pathways that shorten time to market. The FY 2025 Defense Health Program's USD 40.27 billion allocation for equipment modernisation further boosts demand. High focus on decarbonisation drives rapid uptake of >90% efficient GaN supplies across hospitals implementing ESG scorecards.

Asia-Pacific charts the quickest 9.8% CAGR to 2030 as India's devices market aims for USD 50 billion valuation under Production-Linked Incentive benefits. Regional OEMs expand GaN and SiC capacity, yet challenges persist: R&D outlay sits at only 0.5% of expenses and import reliance remains high for precision magnetics and capacitors. Trade-tension scenarios could subtract USD 23.6 billion from sector revenue yearly, emphasising the need for supply-chain resilience.

Europe's stringent MDR framework complicates conformity, with just 43 notified bodies covering roughly 500,000 devices, creating significant approval delays. Nevertheless, strong sustainability mandates and public-sector energy targets sustain interest in ultra-efficient medical power supply market solutions. MedTech Europe advocates regulatory reform to preserve innovation pipelines while supporting health-system investments in green infrastructure.

- Advanced Energy Industries Inc.

- Astrodyne TDI Corp.

- Bel Power Solutions (CUI Inc.)

- Chroma Systems Solutions Inc.

- Cincon Electronics Co. Ltd

- Cosel Co. Ltd

- Delta Electronics Inc.

- FRIWO AG

- GlobTek Inc.

- Inventus Power

- Mean Well Enterprises Co. Ltd

- Murata Power Solutions Inc.

- Powerbox International AB

- Power-One Inc. (Bel Fuse)

- Puls GmbH

- RECOM Power GmbH

- Shenzhen Huyssen Power Co. Ltd

- SL Power Electronics

- Spellman High Voltage Electronics Corp.

- SynQor Inc.

- TDK-Lambda Corporation

- Traco Power Group

- TT Electronics plc

- Vitec Power GmbH

- Wall Industries Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rapid miniaturisation via GaN and SiC switching devices

- 4.2.2 Expansion of diagnostic-imaging fleets in outpatient centres

- 4.2.3 Surge in home-based patient monitoring equipment

- 4.2.4 Decarbonisation mandates pushing >90 % conversion-efficiency PSUs

- 4.2.5 Digitally-controlled, remotely-monitored supply units (power-as-a-service)

- 4.3 Market Restraints

- 4.3.1 IEC 60601-1 "4th-edition" EMC upgrade costs

- 4.3.2 Semiconductor supply-chain volatility for high-voltage MOSFETs

- 4.3.3 Tariff-driven cost spikes on Chinese magnetics and capacitors

- 4.3.4 Thermal management limits in sub-1-inch open-frame designs

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Industry Attractiveness - Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Consumers

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Impact of Macroeconomic Factors on the Market

5 MARKET SIZE AND GROWTH FORECASTS (VALUES)

- 5.1 By Technology

- 5.1.1 AC-DC Power Supply

- 5.1.2 DC-DC Power Supply

- 5.2 By Type

- 5.2.1 Open-Frame

- 5.2.2 Enclosed

- 5.2.3 External/Adapter

- 5.2.4 Configurable/Modular

- 5.3 By Power Range

- 5.3.1 0-50 W

- 5.3.2 51-200 W

- 5.3.3 201-1000 W

- 5.3.4 >1000 W

- 5.4 By Application

- 5.4.1 Diagnostic and Imaging Equipment

- 5.4.2 Patient Monitoring

- 5.4.3 Surgical and Life-support

- 5.4.4 Home-Healthcare Devices

- 5.4.5 Others

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Chile

- 5.5.2.4 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Russia

- 5.5.3.7 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 India

- 5.5.4.3 Japan

- 5.5.4.4 South Korea

- 5.5.4.5 Singapore

- 5.5.4.6 Malaysia

- 5.5.4.7 Australia

- 5.5.4.8 Rest of Asia-Pacific

- 5.5.5 Middle East and Africa

- 5.5.5.1 Middle East

- 5.5.5.1.1 United Arab Emirates

- 5.5.5.1.2 Saudi Arabia

- 5.5.5.1.3 Turkey

- 5.5.5.1.4 Rest of Middle East

- 5.5.5.2 Africa

- 5.5.5.2.1 South Africa

- 5.5.5.2.2 Nigeria

- 5.5.5.2.3 Rest of Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Advanced Energy Industries Inc.

- 6.4.2 Astrodyne TDI Corp.

- 6.4.3 Bel Power Solutions (CUI Inc.)

- 6.4.4 Chroma Systems Solutions Inc.

- 6.4.5 Cincon Electronics Co. Ltd

- 6.4.6 Cosel Co. Ltd

- 6.4.7 Delta Electronics Inc.

- 6.4.8 FRIWO AG

- 6.4.9 GlobTek Inc.

- 6.4.10 Inventus Power

- 6.4.11 Mean Well Enterprises Co. Ltd

- 6.4.12 Murata Power Solutions Inc.

- 6.4.13 Powerbox International AB

- 6.4.14 Power-One Inc. (Bel Fuse)

- 6.4.15 Puls GmbH

- 6.4.16 RECOM Power GmbH

- 6.4.17 Shenzhen Huyssen Power Co. Ltd

- 6.4.18 SL Power Electronics

- 6.4.19 Spellman High Voltage Electronics Corp.

- 6.4.20 SynQor Inc.

- 6.4.21 TDK-Lambda Corporation

- 6.4.22 Traco Power Group

- 6.4.23 TT Electronics plc

- 6.4.24 Vitec Power GmbH

- 6.4.25 Wall Industries Inc.

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 White-Space and Unmet-Need Assessment