|

시장보고서

상품코드

1850104

단열 콘크리트 폼(ICF) 시장 : 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Insulated Concrete Form (ICF) - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

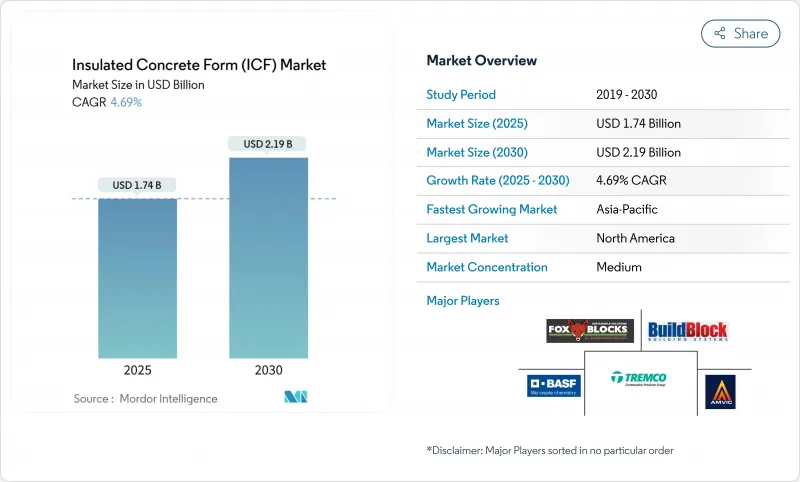

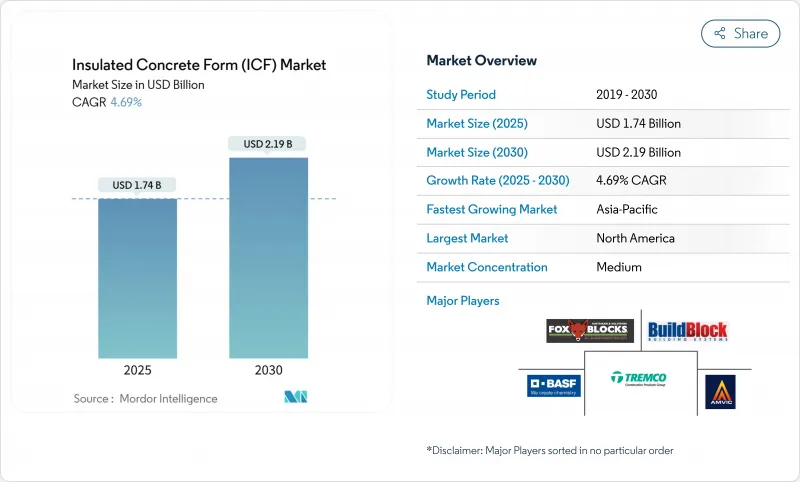

단열 콘크리트 폼 시장의 2025년 시장 규모는 17억 4,000만 달러, 2030년에는 21억 9,000만 달러에 이르고, CAGR 4.69%로 성장할 것으로 예측됩니다.

이 꾸준한 확대는 건설 부문이 평생 운영 비용을 낮추면서 엄격한 법규를 충족하는 에너지 효율적인 건물 외벽으로 전환을 반영합니다. 강력한 정책 지원, 에너지 가격 상승, 기후 회복력에 대한 의식이 높아지면서 특히 허리케인, 산불, 기온의 극단적인 변화로 인해 전통적인 벽이 위험에 처하는 장소에서의 채택을 가속화하고 있습니다. 주택 프로젝트가 여전히 대부분을 차지하고 있지만, 상업 개발자와 공공 기관은 인터넷 제로 및 방음 목표를 달성하기 위해 주문을 확대하고 있습니다. 북미는 여전히 가장 큰 구매 지역이지만 중국과 인도는 국가 건축법에 높은 단열 수준을 통합하기 때문에 아시아태평양이 가장 빠른 비율로 증가하고 있습니다.

세계 단열 콘크리트 폼(ICF) 시장 동향과 통찰

에너지 효율이 높은 고층 빌딩에 대한 수요 증가

2024년 국제 에너지 절약 기준에서는 기후 구역 4와 5에서의 외부 단열이 의무화되었으며, 단열 콘크리트 폼은 다층 프로젝트의 컴플라이언스 솔루션으로 자리매김하고 있습니다. 개발자는 콘크리트 코어가 단열재로 싸여 있기 때문에 법규를 충족하고 한 단계로 열교를 줄일 수 있습니다. 광열비 상승은 투자 회수액을 더욱 증가시키고 소유자가 수십년동안 성능을 유지할 수 있는 벽을 선택하도록 격려하고 있습니다. 이 기준을 채택한 관할구역은 고층건축이 토지이용계획의 주류가 되고 있는 대도시권에 집중하고 있기 때문에 수요는 점점 높아질 것으로 보입니다.

혁신적인 시공 방법 채택 증가

지속적인 기술 노동력 부족으로 계약자는 기존의 틀 공법에 대한 의존도를 낮추는 공법을 선택하게 되었습니다. 단열 콘크리트 폼을 조립하는 작업자는 스택의 단순화와 콜백 감소로 일정을 최대 30% 절약할 수 있었습니다고 보고했습니다. 블록형 모듈은 조립식 및 반복 가능한 워크플로우에 적합하기 때문에 기업은 품질을 희생하지 않고 노동력 풀을 확장할 수 있습니다. 노동력이 고령화되고 채택이 어려운 상황이 계속되는 가운데 설치의 간소화는 장기적인 매력을 높입니다.

목조 축조 공법과 비교했을 때의 초기 비용의 높이

목재 가격이 상승한 후에도 건축업자는 단열 콘크리트 폼을 선택할 때 3-8%의 할증 가격에 직면하고, 중소기업은 콘크리트 펌프를 대여하여 구조 엔지니어링 검토에 지불해야 합니다. 이러한 비용은 평생 광열비가 저렴함에도 불구하고 예산에 제약이 있는 프로젝트를 방해합니다. 장려금제도와 에너지요금의 상승에 의해 그 차이는 점차 상쇄되고 있지만, 퍼스트 코스트 감응도가 여전히 장애물이 되고 있습니다.

부문 분석

폴리스티렌 블록은 2024년 단열 콘크리트 폼 시장 점유율의 88.60%를 차지하며, 2030년까지 매년 4.72%로 확대될 것으로 예측됩니다. 콘크리트 타설시의 습기에 견디면서 R-22-R-26을 실현하는 EPS 패널이 이 점유율을 지지하고 있습니다. 난연성 첨가제는 법규에 맞는 데 도움이되며 재활용 프로그램은 순환 경제를 목표로하는 지자체에 호소합니다.

폴리 우레탄, 시멘트 접착 나무 섬유, 비드 강화 혼합물은 전문적인 틈새 시장을 차지합니다. 폴리우레탄은 좁은 부지에서도인치당 R 값이 높고 시멘트와 목재 섬유 블록은 지역별 기준과 조달 선호도를 충족합니다. 바이오 원료를 5% 포함한 바이오 폴리이소는 2024년에 데뷔하여 그린 케미컬의 새로운 방향을 보여줍니다. 구체화 탄소에 대한 규제가 강화됨에 따라 대체 발포체가 점유율을 확대 할 수 있지만 폴리스티렌의 스케일링 우위는 그 리더십을 지원합니다.

플랫월 폼웍은 2024년 매출의 54.17%를 차지했으며, 제네콘의 기본 옵션이 되었습니다. 플랫월 솔루션의 단열 콘크리트 폼 시장 규모는 꾸준히 확대될 것으로 예상되지만, CAGR 5.32%로 성장하는 스크린 그리드 제품은 내하중을 희생하지 않고 콘크리트 양을 줄임으로써 설득력 있는 경제성을 제공합니다. 계약자는 리프트가 가벼워지고 타설이 빨라지고 중공 웹 그리드를 쌓을 때의 블로우 아웃의 위험이 줄어드는 것을 높이 평가했습니다.

와플 그리드 패널은 두꺼운 발포체를 필요로 하는 고단열 공사에 대응하고, 포스트 앤 빔 형식은 콘크리트 리브의 노출을 요구하는 건축가에게 여전히 인기가 있습니다. 연결 브래킷, 유틸리티 케이스, 얼라인먼트 브레이싱도 진화를 계속하고 있어, 사용의 용이성을 추구하는 경쟁력이 높아지고 있습니다. 엔지니어링의 신뢰성이 높아짐에 따라 설계 팀은 성능과 미적 유연성을 결합한 하이브리드 그리드를 지정할 수 있습니다.

지역 분석

북미는 2024년 세계 매출의 39.50%를 차지하고 단열 콘크리트 폼을 참조하는 모델 에너지 규범과 공인 시공업체의 밀집된 네트워크에 지지를 받고 있습니다. 미국 연방 정부의 인프라 자금은 극단적인 바람과 산불에 견딜 수 있는 탄력적인 건설을 중시하고 있으며, 이 시스템은 추가적인 층을 제공하지 않고 이점을 제공합니다.

아시아태평양은 가장 빠르게 성장하고 있으며 2030년까지 연평균 복합 성장률(CAGR)은 5.03%를 나타낼 전망입니다. 인도의 에너지 절약 건축 기준법은 25-50%의 에너지 절약을 목표로 하고 있으며 커튼월의 세부 사항에 익숙하지 않은 개발자에게는 곧바로도 도입할 수 있는 방법입니다.

유럽에서는 가장 까다로운 탄소와 에너지 벤치마킹이 진행되고 있지만, 석조 전통은 채택 속도를 늦춥니다. 남미나 중동에서는 전기요금의 급등과 도시의 고밀도화에 의해 가능성이 넓어지고 있지만, 계약자의 지식이 부족하고, 경쟁하는 저비용의 공법도 있기 때문에 지금까지 보급은 한정적입니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월의 애널리스트 서포트

목차

제1장 서론

- 조사의 전제조건과 시장의 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 에너지 효율이 높은 고층 빌딩 수요 증가

- 혁신적인 건설 절차 채택 증가

- 보다 엄격한 친환경 빌딩 규제와 인센티브

- 밀집한 도시의 충전재에 있어서의 방음재 수요 증가

- 지속 가능한 건축자재에 대한 의식의 고조

- 시장 성장 억제요인

- 목조 건축에 비해 높은 초기 비용

- 계약자의 지식 부족과 숙련 노동자의 부족

- VOC 배출규제

- 밸류체인 분석

- Porter's Five Forces

- 공급기업의 협상력

- 구매자의 협상력

- 신규 참가업체의 위협

- 대체품의 위협

- 경쟁도

제5장 시장 규모와 성장 예측

- 소재의 유형

- 폴리스티렌 폼

- 폴리우레탄 폼

- 시멘트 결합 목질 섬유

- 시멘트 결합 폴리스티렌 비드

- 시스템 유형

- 플랫월시스템

- 와플 그리드 시스템

- 스크린 그리드 시스템

- 기둥 접합 시스템

- 건설 유형

- 신축

- 개조/리모델링

- 용도

- 주택용

- 상업용

- 기관

- 지역

- 아시아태평양

- 중국

- 일본

- 인도

- 한국

- ASEAN 국가

- 기타 아시아태평양

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 프랑스

- 영국

- 이탈리아

- 기타 유럽

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 중동 및 아프리카

- 사우디아라비아

- 남아프리카

- 기타 중동 및 아프리카

- 아시아태평양

제6장 경쟁 구도

- 시장 집중도

- 전략적 동향

- 시장 점유율(%)/랭킹 분석

- 기업 프로파일

- Airlite Plastics Company & Fox Blocks(Fox Blocks)

- Alleguard

- Amvic Ireland LTD

- BASF

- Beco Products Ltd

- BuildBlock Building Systems LLC

- Carlisle Construction Materials(Carlisle Companies Inc.)

- Durisol

- Future Foam Inc.

- INTEGRASPEC

- LiteForm

- Logix Brands Ltd.

- Polycrete International

- Quad-Lock Building Systems

- RASTRA

- RPM International Inc.

- Sismo Building Technology

- SuperForm

- TF System

- Tremco CPG Inc.

제7장 시장 기회와 장래의 전망

SHW 25.11.07The insulated concrete forms market is valued at USD 1.74 billion in 2025 and is forecast to reach USD 2.19 billion by 2030, advancing at a 4.69% CAGR.

The steady expansion reflects the construction sector's pivot toward energy-efficient building envelopes that satisfy tightening codes while lowering lifetime operating costs. Strong policy support, rising energy prices, and heightened awareness of climate resilience are amplifying adoption, especially where hurricanes, wildfires, or temperature extremes put conventional walls at risk. Residential projects still account for most placements, yet commercial developers and public agencies are scaling up orders to meet net-zero and acoustic targets. North America remains the largest regional buyer, but Asia-Pacific is logging the fastest percentage gains as China and India embed higher insulation levels in national building laws.

Global Insulated Concrete Form (ICF) Market Trends and Insights

Rising Demand for Energy-Efficient High-rise Buildings

The 2024 International Energy Conservation Code now mandates exterior continuous insulation in Climate Zones 4 and 5, positioning insulated concrete forms as a compliance solution for multi-story projects. Developers can satisfy code rules and cut thermal bridging within a single step because the concrete core is wrapped by insulation. Higher utility prices further increase the payback value, encouraging owners to select walls that lock in performance for decades. Jurisdictions adopting the code are clustered in metropolitan areas where high-rise construction dominates land-use planning, so demand is likely to intensify.

Increased Adoption of Innovative Construction Procedures

A persistent skilled-labor shortfall is prompting contractors to choose methods that reduce reliance on traditional framing crews. Crews assembling insulated concrete forms report up to 30% schedule savings thanks to simplified stacking and reduced call-backs. The block-like modules lend themselves to prefabrication and repeatable workflows, allowing firms to enlarge their labor pool without sacrificing quality. As the workforce ages and recruitment remains challenging, simplified installation strengthens long-term appeal.

High Upfront Cost Versus Wood Framing

Even after lumber price spikes, builders face a 3-8% premium when choosing insulated concrete forms, and smaller firms must rent concrete pumps and pay for structural engineering reviews. These expenses deter budget-constrained projects despite lower lifetime utility bills. Incentive programs and rising energy tariffs are gradually offsetting the difference, but first-cost sensitivity remains a hurdle.

Other drivers and restraints analyzed in the detailed report include:

- Stricter Green-building Codes and Incentives

- Growing Demand for Acoustic Insulation in Dense Urban Infill

- Limited Contractor Familiarity and Skilled Labor Gap

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Polystyrene blocks controlled 88.60% of the insulated concrete forms market share in 2024, and the segment is forecast to expand at 4.72% annually to 2030. This command rests on EPS panels that deliver R-22 to R-26 while resisting moisture during concrete placement. Flame-retardant additives help meet code, and recycling programs appeal to municipalities pursuing circular-economy goals.

Polyurethane, cement-bonded wood fiber, and bead-enhanced mixes occupy specialist niches. Polyurethane delivers higher R-values per inch for tight sites, whereas cement, wood fiber blocks satisfy regional code or sourcing preferences. Bio-based polyiso containing 5% bio-circular feedstock debuted in 2024 and signals an emerging green-chemistry direction. As mandates on embodied carbon tighten, alternative foams could gain share, yet polystyrene's scaling advantages support its leadership.

Flat-wall assemblies captured 54.17% of 2024 revenues, confirming their position as the default choice for general contractors. The insulated concrete forms market size for flat-wall solutions is projected to rise steadily, but screen-grid products, growing at 5.32% CAGR, offer compelling economics by trimming concrete volumes without sacrificing load capacity. Contractors appreciate lighter lifts, faster pours, and fewer blow-out risks when stacking hollow-web grids.

Waffle-grid panels serve high-insulation jobs that demand thicker foam, while post-and-beam formats remain popular with architects who want exposed concrete ribs. Connection hardware, utility chases, and alignment bracing continue to evolve, signaling a competitive push toward ease-of-use. As engineering confidence broadens, design teams may specify hybrid grids that merge performance and aesthetic flexibility.

The Insulated Concrete Forms Market Report Segments the Industry by Material Type (Polystyrene Foam, Polyurethane Foam, and More), System Type (Flat-Wall Systems, Waffle-Grid Systems, and More), Construction Type (New-Build and Retrofit / Remodeling), Application (Residential, Commercial, and Institutional), and Geography (Asia-Pacific, North America, Europe, South America, and Middle-East and Africa).

Geography Analysis

North America generated 39.50% of global revenue in 2024, underpinned by model energy codes that reference insulated concrete forms and a dense network of certified installers. US federal infrastructure funding emphasizes resilient construction that withstands extreme wind and wildfire, benefits that the system delivers without extra layers.

Asia-Pacific is the fastest climber, expected to post a 5.03% CAGR to 2030. India's Energy Conservation Building Code, targeting 25-50% energy savings, positions forms as a ready path for developers unfamiliar with curtain-wall detailing.

Europe enforces some of the strictest carbon and energy benchmarks, yet masonry traditions slow adoption. In South America and the Middle East, rising electricity tariffs and urban densification open potential, but limited contractor familiarity and competing low-cost methods keep penetration modest for now.

- Airlite Plastics Company & Fox Blocks (Fox Blocks)

- Alleguard

- Amvic Ireland LTD

- BASF

- Beco Products Ltd

- BuildBlock Building Systems LLC

- Carlisle Construction Materials (Carlisle Companies Inc.)

- Durisol

- Future Foam Inc.

- INTEGRASPEC

- LiteForm

- Logix Brands Ltd.

- Polycrete International

- Quad-Lock Building Systems

- RASTRA

- RPM International Inc.

- Sismo Building Technology

- SuperForm

- TF System

- Tremco CPG Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Demand for Energy-efficient High-rise Buildings

- 4.2.2 Increased Adoption of Innovative Construction Procedures

- 4.2.3 Stricter Green-building Codes and Incentives

- 4.2.4 Growing Demand for Acoustic Insulation in Dense Urban Infill

- 4.2.5 Rising Awareness of Sustainable Construction Materials

- 4.3 Market Restraints

- 4.3.1 High Upfront Cost Versus Wood Framing

- 4.3.2 Limited Contractor Familiarity and Skilled Labor Gap

- 4.3.3 Regulations for VOC Emission

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Degree of Competition

5 Market Size and Growth Forecasts (Value)

- 5.1 Material Type

- 5.1.1 Polystyrene Foam

- 5.1.2 Polyurethane Foam

- 5.1.3 Cement-Bonded Wood Fiber

- 5.1.4 Cement-Bonded Polystyrene Beads

- 5.2 System Type

- 5.2.1 Flat-Wall Systems

- 5.2.2 Waffle-Grid Systems

- 5.2.3 Screen-Grid Systems

- 5.2.4 Post-and-Beam Systems

- 5.3 Construction Type

- 5.3.1 New-build

- 5.3.2 Retrofit / Remodelling

- 5.4 Application

- 5.4.1 Residential

- 5.4.2 Commercial

- 5.4.3 Institutional

- 5.5 Geography

- 5.5.1 Asia-Pacific

- 5.5.1.1 China

- 5.5.1.2 Japan

- 5.5.1.3 India

- 5.5.1.4 South Korea

- 5.5.1.5 ASEAN Countries

- 5.5.1.6 Rest of Asia-Pacific

- 5.5.2 North America

- 5.5.2.1 United States

- 5.5.2.2 Canada

- 5.5.2.3 Mexico

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 France

- 5.5.3.3 United Kingdom

- 5.5.3.4 Italy

- 5.5.3.5 Rest of Europe

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Argentina

- 5.5.4.3 Rest of South America

- 5.5.5 Middle-East and Africa

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 South Africa

- 5.5.5.3 Rest of Middle-East and Africa

- 5.5.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share (%)/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Airlite Plastics Company & Fox Blocks (Fox Blocks)

- 6.4.2 Alleguard

- 6.4.3 Amvic Ireland LTD

- 6.4.4 BASF

- 6.4.5 Beco Products Ltd

- 6.4.6 BuildBlock Building Systems LLC

- 6.4.7 Carlisle Construction Materials (Carlisle Companies Inc.)

- 6.4.8 Durisol

- 6.4.9 Future Foam Inc.

- 6.4.10 INTEGRASPEC

- 6.4.11 LiteForm

- 6.4.12 Logix Brands Ltd.

- 6.4.13 Polycrete International

- 6.4.14 Quad-Lock Building Systems

- 6.4.15 RASTRA

- 6.4.16 RPM International Inc.

- 6.4.17 Sismo Building Technology

- 6.4.18 SuperForm

- 6.4.19 TF System

- 6.4.20 Tremco CPG Inc.

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-need Assessment