|

시장보고서

상품코드

1850106

탄약 시장 : 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Ammunition - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

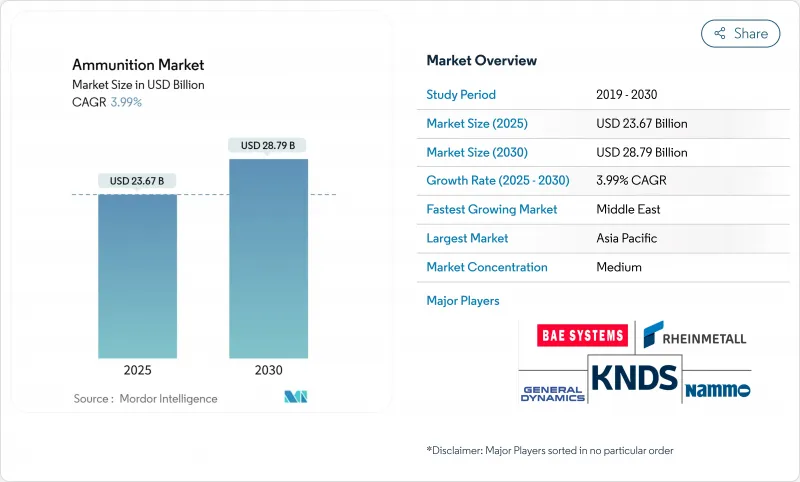

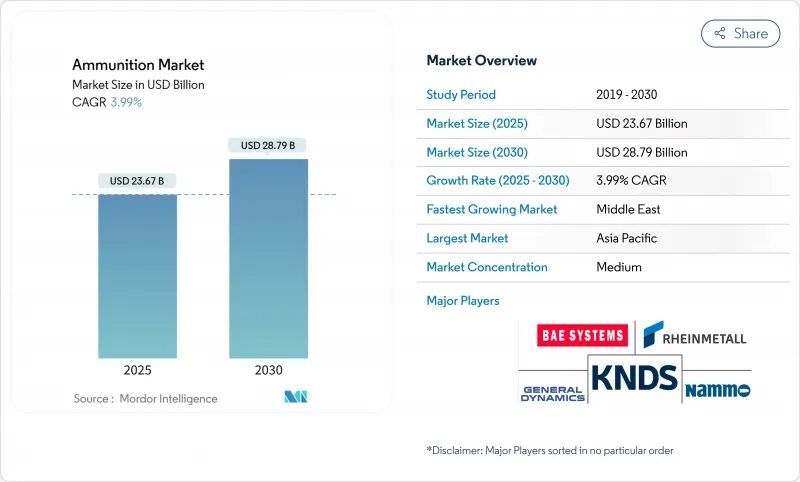

탄약 시장 규모는 2025년에 236억 7,000만 달러, 2030년에는 287억 9,000만 달러에 이르고 CAGR 3.99%로 성장할 것으로 예측됩니다.

NATO 전체의 비축 재구축, 인도 태평양 근대화 프로그램의 강화, 대량 조달에서 정밀 조달로의 전환이 지출의 우선순위를 재구축하고 있습니다. 지휘관이 물류 실적를 줄이는 효과 기반의 사격을 요구하고 있기 때문에 스마트포, 프로그램 가능한 에어 버스트탄, 근접탄약이 현재 조달을 지원하고 있습니다. 납, 니트로셀룰로오스 및 안티몬 공급 중단을 금지하는 환경 규칙이 설계 변경을 가속화하고 있습니다. 동시에 미국과 동유럽에서는 민간인의 휴대총 휴대가 증가하고 있기 때문에 소구경총 생산라인은 풀 가동을 계속하고 있습니다. 신속하게 규모를 확대하고 유도 기술을 통합하고 환경에 적합한 화학물질을 검증할 수 있는 공급업체는 경쟁이 심한 탄약 시장에서 프리미엄 계약을 획득하고 있습니다.

세계 탄약시장 동향과 통찰

우크라이나 전쟁 후 NATO 비축 보충 강화

유럽 국가들은 8억 유로(9억 2,500만 달러)의 포탄을 키예프로 이전하여 평시 생산량이 불충분함을 드러냈습니다. 2024년까지 연간 생산량을 70,000발에서 700,000발로 확대하는 라인 메탈 결정은 현재 진행중인 긴급 규모 확대를 보여줍니다. 다년간 계약은 생산 능력을 고정하고 탄약 시장을 스팟 구매에서 전략적 비축으로 이행시킵니다. 예산 재분배는 현재 새로운 플랫폼보다 탄약에 유리합니다. 이 피벗은 폭약, 신관 및 에너지 물질을 신속하게 공급할 수 있는 신뢰할 수 있는 생산자의 수익 기반을 구축합니다.

인도 태평양 방어의 현대화와 공동 훈련 탄약 수요

8억 5,000만 달러에 해당하는 인도의 K9 Vajra-T 프로그램(200 유닛)은 이 지역의 대포 업데이트를 보여줍니다. 도쿄가 워싱턴과 AIM-120의 공동 생산을 모색하고 있다는 것은 탄력적인 공급 라인을 확보하기 위해 산업계가 더 깊게 협력하고 있음을 보여줍니다. 현재 진행 중인 양국간 및 다국간 연습은 그 어느 때보다도 대규모 실전적 재고를 소모하여 정밀탄의 지속적인 인양을 촉진하고 있습니다. 정부가 오프셋 크레딧을 현지 부품 제조에 연결함으로써 국산 생산 능력도 병행하여 향상하고 있습니다. 기술 이전과 확장 가능한 조립 라인을 제공하는 공급업체는 혼잡한 시장 경쟁에서 우위를 유지하고 있습니다.

국방부 및 국방부 예산을 비승무원 시스템으로 재우선화

미 국방부가 2025년 무인 차량에 매년 10억 달러 증가한 101억 달러를 할당하는 것은 전략적 재구성의 한 예입니다. 독일의 1,000억 유로(1,150억 달러)의 재군비 계획도 비슷한 논리를 적용하고 있으며, 탄약의 소비 패턴을 변경하는 부유 탄약으로 자원을 유도하고 있습니다. 무인 항공기는 여전히 탄약을 발사하고 있지만 탄창이 작고 조준 프로파일이 더 똑똑하기 때문에 총 탄수가 줄어들 수 있습니다. 레거시 캘리버에만 묶여있는 제조업체는 탄약 시장 내에서 무인 항공기와 호환되는 페이로드 형식으로 전환하지 않는 한 충분히 활용되지 않을 위험이 있습니다.

부문 분석

5.56mm에서 12.7mm의 작은 구경은 2024년 탄약 시장 점유율의 46.35%를 유지하고 여러 국가에서 조달을 간소화하는 표준화된 NATO 사양의 혜택을 누리고 있습니다. 신규 무기 휴대 허가 취득자가 방위용 탄환을 비싼 가격으로 구입하기 때문에 민간의 풍부한 섭취가 수량을 더욱 안정시킵니다. 이 분야는 예측 가능한 재주문율을 즐길 수 있기 때문에 고속 생산 라인은 일년 내내 회전하고 있습니다. 스케일 메리트에 의해 기존 기업이 코스트 리더십을 발휘하고 있지만, 환경 규제에 의해 코팅제나 프라이머는 무연의 배합으로 이행하고 있습니다.

유도식 155mm포는 CAGR 5.85%로 가장 급속한 상승을 나타내며 집단 일제사격보다 정밀사격으로의 교리상의 시프트를 반영하고 있습니다. 라인메탈은 2025년까지 연간 70만발의 포탄을 생산할 계획으로 업계가 보다 대형 스마트탄에 의욕을 보이고 있습니다. 미국 육군의 사거리 연장 포병 계획에서는 사거리 65-70km가 지정되어 있기 때문에 공급업체는 에너제틱, 글라이드 키트, 베이스 블리드 모듈의 공동 개발을 강요하고 있습니다. 그 결과 선진적인 대구경 제품 시장 규모가 확대되어 기존의 댐 포탄에 대해 2자리 가격 프리미엄이 붙게 되었습니다.

포탄은 2030년까지 CAGR 6.91%로 성장하고 장거리 정밀 사격이 동료와의 분쟁 계획에서 다시 우위를 되찾고 있습니다. 멀티 모드 퓨즈, GPS 시커, 글라이드 바디는 1발당 명목 비용은 증가하지만 효과에 필요한 총 발사수는 감소시킵니다. 스페인 같은 나라들이 엑스칼리버 S의 조달을 약속하고 있으며, 유도탄의 세계적인 분위기를 뒷받침하고 있습니다.

2024년 탄약 시장 규모의 39.08%를 총알과 카트리지가 차지하고, 세계적인 소화기 업그레이드와 지속적인 스포츠 수요에 지지되고 있습니다. 로켓탄, 미사일 탄두, 공중폭탄은 전술적인 심부공격을 가능하게 하는 작지만 중요한 트랜시를 형성합니다. 미사일에서 포탄으로의 기술 파급은 기존 제품의 경계를 모호하게 해 탄약 업계 전체의 기술 혁신을 격화시킵니다.

지역 분석

아시아태평양은 2024년 매출의 35.25%를 차지했으며 인도의 수출 확대와 견고한 국내 생산이 그 원동력이 되었습니다. 인도는 2023-24년에 26억 3,000만 달러의 군수품을 출하하고, 2029년까지 60억 달러를 목표로 하고 있습니다. 한국은 K9 Vajra-T 기술이전을 활용해 제휴처를 확대하고, 일본은 공동생산협의를 통해 공급체인의 탄력성을 높입니다. 중국은 주요 투입물에 대한 수출 제한으로 동맹국에 추진제 공장의 육상화를 강요하고 탄약 시장의 중기적 성장을 확고하게 하고 있습니다.

중동은 사우디아라비아의 780억 달러의 국방 할당으로 지역 예산이 증가하고 2030년까지 연평균 복합 성장률(CAGR) 7.45%로 성장할 것으로 예상됩니다. 리야드의 '비전 2030'은 국방의 50% 국산화를 의무화하고 있으며 국내 포탄 및 폭탄 공장을 2018년 생산고의 4%에서 2024년에는 19.35%로 늘렸습니다. UAE와 걸프 국가의 동료들은 이 궤적을 반영하여 기술 패키지와 턴키 라인 수입을 추진하고 있습니다. 지속적인 지역 분쟁은 소비를 유지하고 탄약 시장 전체공급업체의 예측 가능한 견인력을 보장합니다.

유럽은 NATO의 기준과 보충 압력으로 인해 매우 중요합니다. 독일의 1,000억 유로 규모의 재군비와 리투아니아, 루마니아, 우크라이나에 있는 라인메탈 공장은 유럽권이 전략적 두께를 회복할 의향을 보여줍니다. 북미는 최첨단 스마트 퓨즈를 공급하며 세계 최대의 민간 스포츠 사격 기지로부터 혜택을 누리고 있습니다. 무연 탄환에 대한 환경지령은 환경에 적합한 화학물질을 다루는 기업의 선행자 이익을 강화하고 세계 탄약시장에서 차별화를 도모합니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 서포트

목차

제1장 서론

- 조사의 전제조건과 시장의 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- NATO 비축 보충의 강화

- 인도 태평양 방위 근대화와 공동 훈련 탄약 수요

- 도시 작전에 있어서의 프로그램 가능한 공중 작렬탄과 근접 신관탄의 급속한 도입

- 미국과 동유럽에서 민간인의 은닉 소지 급증

- 기존 155mm 추진제 충전의 가속화된 수명 주기 교체

- 티어-1 군대의 친환경 무연탄 전환

- 시장 성장 억제요인

- 무인 시스템에 대한 국방부 및 국방부 예산 재조정

- 면화 공급 충격에 의한 니트로셀룰로오스 가격 상승

- 훈련장에서의 중금속 배출에 관한 ESG 감시 강화

- 미국 OEM의 LATAM 판매에 영향을 미치는 민간 수출 금지

- 밸류체인 분석

- 규제와 기술의 전망

- Porter's Five Forces 분석

- 신규 참가업체의 위협

- 구매자의 협상력

- 공급기업의 협상력

- 대체품의 위협

- 경쟁 기업간 경쟁 관계

제5장 시장 규모와 성장 예측

- 칼리버

- 소구경(5.56-12.7 mm)

- 중구경(13-40 mm)

- 대구경(40mm 이상)

- 제품별

- 총알과 탄약

- 포탄

- 로켓과 미사일 탄두

- 공중폭탄

- 지침에 따라

- 가이드 첨부

- 가이드 없음

- 최종 사용자별

- 군

- 법 집행 기관

- 민간 및 스포츠 사격

- 플랫폼별

- 온쇼어 플랫폼

- 해군 플랫폼

- 공중 플랫폼

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 영국

- 프랑스

- 독일

- 러시아

- 기타 유럽

- 아시아태평양

- 중국

- 인도

- 일본

- 한국

- 기타 아시아태평양

- 남미

- 브라질

- 기타 남미

- 중동 및 아프리카

- 중동

- 사우디아라비아

- 아랍에미리트(UAE)

- 튀르키예

- 기타 중동

- 아프리카

- 남아프리카

- 기타 아프리카

- 북미

제6장 경쟁 구도

- 시장 집중도

- 전략적 동향

- 시장 점유율 분석

- 기업 프로파일

- BAE Systems plc

- Rheinmetall AG

- Elbit Systems Ltd.

- KNDS NV

- General Dynamics Corporation

- Nammo AS

- Singapore Technologies Engineering Ltd.(ST Engineering)

- Denel SOC Ltd.

- Northrop Grumman Corporation

- MESKO SA

- CBC Global Ammunition

- Directorate of Ordnance(Coordination and Services)

- Saab AB

- Hanwha Corporation

- ARSENAL JSCo.

- ASELSAN AS

- Winchester Ammunition(Olin Corporation)

- Poongsan Corporation

- Fiocchi Munizioni SpA

- FN Browning Group

- CZECHOSLOVAK GROUP as(CSG Group)

제7장 시장 기회와 장래의 전망

SHW 25.11.07The ammunition market size stands at USD 23.67 billion in 2025 and is projected to climb to USD 28.79 billion by 2030, registering a 3.99% CAGR.

Stockpile rebuilding across NATO, intensifying Indo-Pacific modernization programs, and shifting from volume to precision procurement are reshaping spending priorities. Smart artillery, programmable air-burst rounds, and proximity-fuzed munitions now underpin procurement as commanders demand effects-based fires that reduce logistics footprints. Environmental rules banning lead, nitrocellulose, and antimony supply disruptions are accelerating design changes. At the same time, civilian concealed-carry growth in the United States and Eastern Europe keeps small-caliber lines operating at capacity. Suppliers able to scale quickly, embed guidance technologies, and validate eco-compliant chemistries are capturing premium contracts in the highly contested ammunition market.

Global Ammunition Market Trends and Insights

Intensified NATO Stockpile Replenishment Post-Ukraine War

European nations transferred EUR 800 million (USD 925 million) in shells to Kyiv, exposing inadequate peacetime production rates. Rheinmetall's decision to expand annual output from 70,000 to 700,000 rounds by 2024 illustrates the emergency scaling underway. Multi-year contracts lock in capacity, moving the ammunition market away from spot buying and toward strategic stockpiling. Budget reallocations now favor ammunition over new platforms because advanced weapons deliver little value without a sustained supply. This pivot creates a dependable producer revenue base that can quickly ramp explosives, fuzes, and energetic materials.

Indo-Pacific Defense Modernization and Joint-Training Ammunition Demand

India's 200-unit K9 Vajra-T program, worth USD 850 million, exemplifies regional artillery renewal. Tokyo's exploration of AIM-120 co-production with Washington shows deeper industrial teaming to secure resilient supply lines. Ongoing bilateral and multilateral exercises consume ever-larger live-fire inventories, driving sustainable pull for precision rounds. Indigenous capacity is rising parallel, with governments tying offset credits to local component manufacture. Suppliers offering technology transfer and scalable assembly lines maintain a competitive edge in the crowded ammunition market.

DoD and MoD Budget Re-prioritization Toward Un-crewed Systems

The Pentagon's USD 10.1 billion allocation for unmanned vehicles in 2025, up USD 1 billion annually, exemplifies a strategic realignment. Germany's EUR 100 billion (USD 115 billion) rearmament plan applies similar logic, steering resources into loitering munitions that alter ammunition consumption patterns. Although drones still fire ordnance, their smaller magazines and smarter targeting profiles can dampen aggregate round volumes. Producers tied exclusively to legacy calibers risk under-utilization unless they pivot toward drone-compatible payload formats within the ammunition market.

Other drivers and restraints analyzed in the detailed report include:

- Rapid Adoption of Programmable Air-Burst and Proximity-Fuzed Rounds in Urban Ops

- Civilian Concealed-Carry Boom in US and Eastern Europe Fueling Small-Caliber Sales

- Soaring Nitrocellulose Prices Due to Cotton Supply Shocks

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Small calibers between 5.56 mm and 12.7 mm retained 46.35% of the ammunition market share in 2024, benefiting from standardized NATO specifications that streamline multi-country procurement. Abundant civilian uptake further stabilizes volumes as new concealed-carry licensees purchase defensive rounds at premium prices. The segment enjoys predictable reorder rates that keep high-speed production lines turning year-round. Economies of scale give incumbents cost leadership, though environmental mandates push firms to transition coatings and primers to lead-free formulations.

Guided 155 mm artillery registers the quickest ascent at a 5.85% CAGR, reflecting doctrinal shifts toward precision fires rather than massed salvos. Rheinmetall plans to output 700,000 shells annually by 2025, evidencing industry appetite for larger smart rounds. The United States Army Extended Range Cannon Artillery program specifies 65-70 km reach, forcing suppliers to co-develop energetics, glide kits, and base-bleed modules. The result is an ammunition market size expansion for advanced large-caliber products that can command double-digit price premiums versus legacy dumb shells.

Artillery shells post a 6.91% CAGR to 2030 as long-range precision fires regain primacy in peer-conflict planning. Multi-mode fuzes, GPS seekers, and glide bodies increase the nominal per-round cost but reduce total shots required for effect. Nations like Spain have committed to Excalibur-S procurement, underlining a global uptick for guided projectiles.

Bullets and cartridges controlled 39.08% of the ammunition market size in 2024, underpinned by global small-arms upgrades and sustained sporting demand. Rockets, missile warheads, and aerial bombs form a smaller yet vital tranche that enables tactical deep-strike. Technology spill-over from missiles into artillery shells blurs traditional product boundaries, intensifying innovation across the ammunition industry.

The Ammunition Market Report is Segmented by Caliber (Small Caliber, and More), Product (Bullets and Cartridges, and More), Guidance (Guided and Unguided), End-User (Military, and More), Platform (Land, Naval and Airborne) and Geography (North America, Europe, Asia-Pacific, South America, and the Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific controlled 35.25% of 2024 revenue, powered by India's scaling exports and robust local production. India shipped USD 2.63 billion of munitions in 2023-24 and aims for USD 6 billion by 2029. South Korea leverages K9 Vajra-T technology transfers to widen partner reach, while Japan's co-production talks build supply-chain resilience. China's export limits on key inputs compel allied states to onshore propellant factories, cementing medium-term growth in the ammunition market.

The Middle East is expanding at a 7.45% CAGR to 2030 as Saudi Arabia's USD 78 billion defense allotment lifts regional budgets. Riyadh's Vision 2030 mandates 50% defense localization, raising domestic shell and bomb plants from 4% output in 2018 to 19.35% in 2024. UAE and Gulf peers mirror this trajectory, driving imports of technology packages and turnkey lines. Persistent regional conflicts sustain consumption, ensuring a predictable pull for suppliers across the ammunition market.

Europe remains pivotal owing to NATO standards and replenishment pressures. Germany's EUR 100 billion rearmament and Rheinmetall's factories in Lithuania, Romania, and Ukraine demonstrate the bloc's intent to restore strategic depth. North America supplies cutting-edge smart fuzes and benefits from the world's largest civilian sport-shooting base. Environmental mandates for lead-free rounds reinforce first-mover advantages for firms mastering eco-compliant chemistries, differentiating them in the global ammunition market.

- BAE Systems plc

- Rheinmetall AG

- Elbit Systems Ltd.

- KNDS N.V.

- General Dynamics Corporation

- Nammo AS

- Singapore Technologies Engineering Ltd. (ST Engineering)

- Denel SOC Ltd.

- Northrop Grumman Corporation

- MESKO S.A.

- CBC Global Ammunition

- Directorate of Ordnance (Coordination and Services)

- Saab AB

- Hanwha Corporation

- ARSENAL JSCo.

- ASELSAN A.S.

- Winchester Ammunition (Olin Corporation)

- Poongsan Corporation

- Fiocchi Munizioni S.p.A.

- FN Browning Group

- CZECHOSLOVAK GROUP a.s.(CSG Group)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Intensified NATO stockpile replenishment

- 4.2.2 Indo-Pacific defense modernization and joint-training ammunition demand

- 4.2.3 Rapid adoption of programmable air-burst and proximity-fuzed rounds in urban ops

- 4.2.4 Civilian concealed-carry boom in US and Eastern Europe

- 4.2.5 Accelerated lifecycle replacement of legacy 155 mm propellant charges

- 4.2.6 Tier-1 militaries' transition to environment-friendly lead-free bullets

- 4.3 Market Restraints

- 4.3.1 DoD and MoD budget re-prioritisation toward un-crewed systems

- 4.3.2 Soaring nitrocellulose prices due to cotton supply shocks

- 4.3.3 Heightened ESG scrutiny on heavy-metal discharge at training grounds

- 4.3.4 Civil export bans impacting US OEM sales to LATAM

- 4.4 Value Chain Analysis

- 4.5 Regulatory and Technological Outlook

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Bargaining Power of Suppliers

- 4.6.4 Threat of Substitutes

- 4.6.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Caliber

- 5.1.1 Small Caliber (5.56 to12.7 mm)

- 5.1.2 Medium Caliber (13 to 40 mm)

- 5.1.3 Large Caliber (Above 40 mm)

- 5.2 By Product

- 5.2.1 Bullets and Cartridges

- 5.2.2 Artillery Shells

- 5.2.3 Rockets and Missile Warheads

- 5.2.4 Aerial Bombs

- 5.3 By Guidance

- 5.3.1 Guided

- 5.3.2 Unguided

- 5.4 By End-User

- 5.4.1 Military

- 5.4.2 Law-Enforcement

- 5.4.3 Civil and Sport Shooting

- 5.5 By Platform

- 5.5.1 Land Platform

- 5.5.2 Naval Platform

- 5.5.3 Airborne Platform

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 Europe

- 5.6.2.1 United Kingdom

- 5.6.2.2 France

- 5.6.2.3 Germany

- 5.6.2.4 Russia

- 5.6.2.5 Rest of Europe

- 5.6.3 Asia-Pacific

- 5.6.3.1 China

- 5.6.3.2 India

- 5.6.3.3 Japan

- 5.6.3.4 South Korea

- 5.6.3.5 Rest of Asia-Pacific

- 5.6.4 South America

- 5.6.4.1 Brazil

- 5.6.4.2 Rest of South America

- 5.6.5 Middle East and Africa

- 5.6.5.1 Middle East

- 5.6.5.1.1 Saudi Arabia

- 5.6.5.1.2 United Arab Emirates

- 5.6.5.1.3 Turkey

- 5.6.5.1.4 Rest of Middle East

- 5.6.5.2 Africa

- 5.6.5.2.1 South Africa

- 5.6.5.2.2 Rest of Africa

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 BAE Systems plc

- 6.4.2 Rheinmetall AG

- 6.4.3 Elbit Systems Ltd.

- 6.4.4 KNDS N.V.

- 6.4.5 General Dynamics Corporation

- 6.4.6 Nammo AS

- 6.4.7 Singapore Technologies Engineering Ltd. (ST Engineering)

- 6.4.8 Denel SOC Ltd.

- 6.4.9 Northrop Grumman Corporation

- 6.4.10 MESKO S.A.

- 6.4.11 CBC Global Ammunition

- 6.4.12 Directorate of Ordnance (Coordination and Services)

- 6.4.13 Saab AB

- 6.4.14 Hanwha Corporation

- 6.4.15 ARSENAL JSCo.

- 6.4.16 ASELSAN A.S.

- 6.4.17 Winchester Ammunition (Olin Corporation)

- 6.4.18 Poongsan Corporation

- 6.4.19 Fiocchi Munizioni S.p.A.

- 6.4.20 FN Browning Group

- 6.4.21 CZECHOSLOVAK GROUP a.s.(CSG Group)

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment