|

시장보고서

상품코드

1850110

뇌 모니터링 시장 : 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Brain Monitoring - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

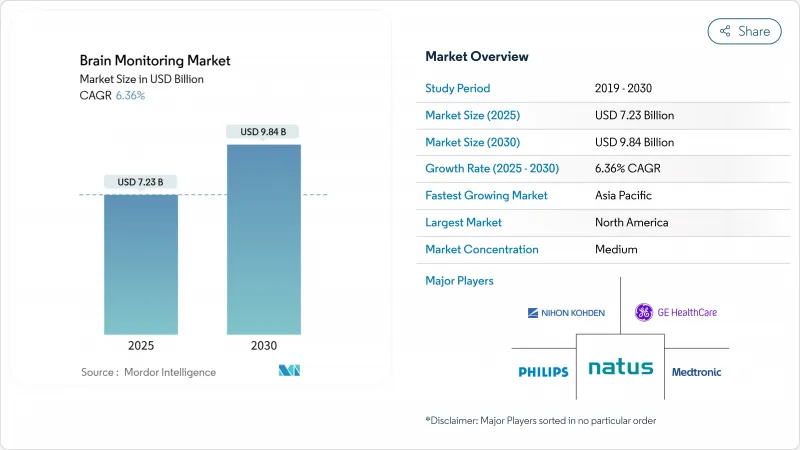

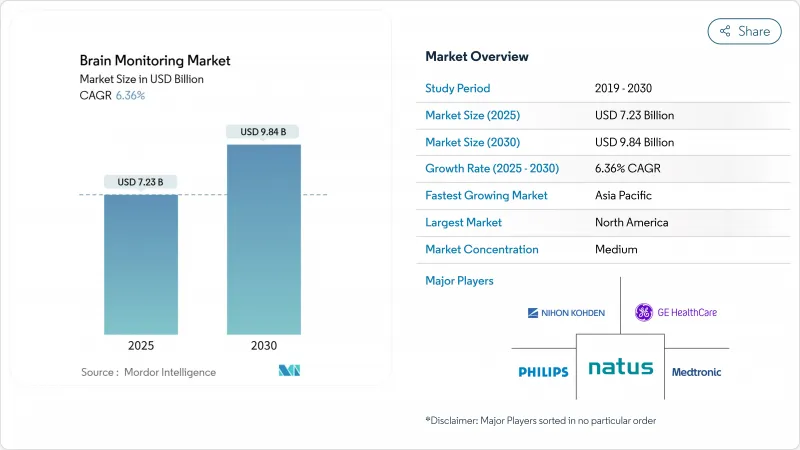

뇌 모니터링 시장 규모는 2025년에 72억 3,000만 달러, 2030년에는 98억 4,000만 달러에 이르고, CAGR은 6.36%를 나타낼 전망입니다.

신경질환이 세계적인 질병 부담의 상위에 부상함에 따라 수요가 확대되고 있으며, 공급자는 보다 빠르고 휴대 가능한 진단 도구에 투자하고 있습니다. 인공지능(AI)의 진보에 의해 멀티모달인 데이터 분석이 개선되는 한편, 저침습으로 웨어러블한 센서에 의해 일상적인 모니터링이 구급 외래, 재활센터, 가정에서 행해지게 되고 있습니다. 병원의 지출은 여전히 고정 시스템이 대부분을 차지하고 있지만, 원격 신경학과 분산 임상시험을 지원하는 소형 클라우드 연결 장비의 성장이 가장 두드러집니다. 벤더는 독립형 하드웨어에서 데이터 분석을 자동화하고, 인력 부족을 완화하고, 분석 구독에서 경상 수익을 창출하는 통합 SaMD(Software-as-a-Medical-Device) 플랫폼으로 초점을 옮기고 있습니다.

세계 뇌 모니터링 시장 동향과 통찰

신경 질환의 유병률 상승

뇌졸중, 치매, 간질, 신경 장애의 증례는 현재 30억명을 넘어 세계 인구의 43%를 차지하고 있습니다. 이러한 질환들은 매년 4억 4,300만 년에 달하는 건강 수명 손실을 초래하며, 보건 체계에 대한 부담을 더욱 가중시키고 있습니다. 장수화에 의해 알츠하이머병 등의 노화에 수반하는 병에 대한 이환율이 악화되고, 당뇨병 등의 대사성 질환은 신경장애의 이환율을 3배로 높입니다. 환자 수요와 신경과 의사공급 사이에 퍼지는 격차는 병원이 고위험 사례를 방어하고 집중적인 해석 허브에 데이터를 공급하는 자동화된 모니터링을 채택하는 것을 뒷받침합니다. 향후 10년간 보편적인 스크리닝 프로그램과 커뮤니티 클리닉은 조기 악화를 잡기 위해 저비용 신경 센서에 의존할 것으로 예상되어 뇌 모니터링 시장의 장기적인 확대를 유지할 예정입니다.

진단 정밀도를 높이는 AI 대응 멀티 모달 분석

머신러닝 알고리즘은 뇌파, 영상, 혈행 동태, 임상 점수를 통합하여 외상성 뇌 손상의 사망률과 예후 불량을 최대 95.6%의 정확도로 예측할 수 있습니다. Ceribell Clarity와 같은 FDA 인증 플랫폼은 침대 측에서 뇌파 검사를 통한 간질 중첩 상태를 몇 분 이내에 감지하여 중요한 치료 팀을 수동 검사에서 해제합니다. 북미 및 유럽 병원에서는 이러한 SaMD 모듈을 기존 모니터에 통합하고 클라우드 분석과 소모품을 번들로 제공하는 서비스 계약을 맺고 있습니다. 보험 상환 코드에서 알고리즘 지원 해석이 인정됨에 따라 아시아태평양의 도시 지역에서의 채택이 가속화되고 있습니다. 중기적으로는 풍부한 데이터 파이프라인이 뇌졸중과 집중 치료실의 의사결정 시간을 단축하고 뇌 모니터링 시장 전체의 이용률을 높일 것으로 보입니다.

첨단 모달리티의 구입·유지의 높은 비용

자기 뇌파와 fMRI 시스템은 300만 달러를 초과할 수도 있으며, 연간 서비스 계약은 정가의 10-15%를 늘립니다. 주류 EEG 장치조차도 소모품과 교정이 필요하며 병원 운영 예산을 압박합니다. 공급업체가 인공지능 대응 모델을 출시하면 구매 사이클이 가속화되고 재무위원회는 가격에 민감한 시장에서 구매를 연기하도록 촉구됩니다. 오픈소스 웨어러블 fNIRS 프로토타입이 아카데믹 랩에서 발표되고 구제가 기대되고 있지만, 인증 취득에는 아직 수년이 걸리기 때문에 비용이 뇌 모니터링 시장의 중기적인 발판이 되고 있습니다.

부문 분석

EEG 시스템은 2024년 뇌 모니터링 시장에서 30.44%의 매출을 획득하여 가장 큰 슬라이스를 만들어냈습니다. 병원에서는 발작의 진단, 진정의 깊이 체크, 뇌허혈의 감시 등에 이용되고 있습니다. 휴대용 급속 EEG 카트는 현재 침대 옆에서 10분 이내에 발작을 감지하여 응급 작업 흐름을 변화시키고 장비의 회전 속도를 높이고 있습니다. 캡, 건식 전극, 케이블 등의 액세서리는 새 모델이 출시될 때마다 소모품 수요가 증가하기 때문에 CAGR 8.11%로 급성장하고 있습니다. 유연한 고분자 전극은 편안함을 향상시키고 셋업 시간을 단축시켜 소아과 및 원격 모니터링에서 EEG의 용도를 확장합니다. 감염 위험을 줄이기 위해 일회용 캡을 표준화하는 병원이 증가함에 따라 액세서리의 하위 부문이 시장 전체의 뇌 모니터링을 능가하는 것으로 보입니다.

두피 뇌파계, fNIRS, 경두개 도플러 등의 비침습적 모달리티는 저위험과 단순한 인원 배치로 2024년 매출의 73.78%를 차지합니다. 알고리즘을 강화한 시스템이 침습적인 정밀도에 가까워짐에 따라 그 매력이 확산되고 있습니다. 그러나 중요한 치료 병동은 여전히 난치성 사례에 대한 두개 내압(ICP) 프로브와 깊은 전극에 의존하고 있습니다. 새로운 나노 멤브레인 센서가 임상시험에 진입하고 혈관을 통해 공급되고 두개골의 침투가 없어짐에 따라 이러한 침습 도구는 CAGR 6.95%로 확대됩니다. 시간이 지남에 따라 하이브리드 솔루션은 카테고리를 더욱 모호하게 만들고 두뇌 모니터링 시장의 두 코호트에서 성장을 유지할 수 있습니다.

지역 분석

북미는 2024년 세계 매출의 37.75%를 차지했으며 견고한 보험 적용, NIH 보조금, 레벨 1 외상 센터의 치밀한 네트워크에 의해 지원되고 있습니다. 이 지역의 뇌 모니터링 시장 규모는 병원이 차량을 AI 대응 모델로 업데이트하고 외래 공급자가 원격 뇌파 키트를 채택함에 따라 안정적인 CAGR 6.12%로 확대되고 있습니다. 유럽은 성숙하면서도 이로 정연한 조달로 이에 이어집니다. 예산 감시가 느려지면서도 채택이 멈추지 않기 때문에 성장률은 5.87%에 그치고 있습니다. 주목할만한 것은 상처 후 황금 시간에 TBI 바이오 마커를 감지하는 핸드 헬드 안구 레이저로 구급차에서 표준 치료가 될 수 있습니다.

아시아태평양은 CAGR 8.59%로 가장 빠르게 성장하고 있습니다. 중국은 제2급 도시의 뇌졸중센터에 자금을 제공하고, 일본은 가정용 뇌파계의 보험 코드를 시험적으로 도입하고, 인도의 민간 병원은 구급 부문에 신속 뇌파 카트를 수입하고 있습니다. 신경학적 사망의 80%가 중저소득 국가에서 발생하고 있다는 점을 감안할 때, 합리적인 가격으로 유지보수가 적은 장비에 대한 지역 수요는 여전히 높습니다. 현지 제조업체가 비용 효율적인 대체품 공급을 시작하여 뇌 모니터링 시장에서 공급망의 강인성이 강화되었습니다.

중동 및 아프리카와 남미는 걸프 국가들이 신경 치명적 센터를 건설하고 브라질 병원이 원격 뇌졸중 네트워크에 참여함에 따라 소규모 기지에서 확대되고 있습니다. 그러나 환율 변동과 조달 장애물은 시장 가속을 억제하고 있습니다. 다자간 금융기관과 관민 파트너십은 임상적 및 경제적 가치를 입증하는 시험 프로그램을 맡아 미래 시장 성장의 발판을 만들 것으로 예측됩니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 서포트

목차

제1장 서론

- 조사의 전제조건과 시장의 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 신경질환의 유병률 상승

- 진단 정밀도를 높이는 AI 대응의 멀티 모달 분석

- 웨어러블 및 저침습성 뇌 센서의 보급

- 신경 집중 치료 인프라에 대한 투자 급증

- 객관적인 모니터링 바이오마커를 필요로 하는 뇌에 초점을 맞춘 약물시험

- 의료기기용 소프트웨어 모듈의 승인의 신속화

- 시장 성장 억제요인

- 고도의 모달리티의 높은 구매 및 유지 관리 비용

- 훈련을 받은 신경기술자의 세계적 부족

- 연결된 장치에서 상호 운용성과 사이버 보안 위험

- 외래 모니터링 솔루션의 불확실한 상환

- 공급망 분석

- 기술의 전망

- Porter's Five Forces 분석

- 신규 참가업체의 위협

- 구매자의 협상력/소비자

- 공급기업의 협상력

- 대체 제품 및 서비스의 위협

- 경쟁 기업간 경쟁 관계

제5장 시장 규모와 성장 예측

- 제품 유형별

- 자기뇌파(MEG) 시스템

- 뇌파계(EEG) 시스템

- 경두개 도플러(TCD) 초음파

- 뇌산소농도계

- 자기 공명 영상(MRI) 장치

- 두개 내압(ICP) 모니터

- 컴퓨터 단층 촬영(CT) 장치

- 양전자 방출 단층 촬영(PET) 장치

- 액세서리

- 전극

- 센서

- 케이블

- 젤&페이스트

- 기타 액세서리

- 기타 뇌 모니터링 장치

- 순서별

- 침습적 모니터링

- 비침습적 모니터링

- 모달리티별

- 고정/독립형 시스템

- 휴대용 및 웨어러블 시스템

- 용도별

- 외상성 뇌 손상

- 뇌졸중

- 간질

- 파킨슨병

- 알츠하이머병 및 기타 치매

- 수면장애

- 기타 신경질환

- 최종 사용자별

- 병원

- 진단 및 영상 센터

- 외래 수술 및 전문 클리닉

- 재택 케어 환경과 원격 신경학 플랫폼

- 학술연구기관

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 기타 유럽

- 아시아태평양

- 중국

- 인도

- 일본

- 호주

- 한국

- 기타 아시아태평양

- 중동 및 아프리카

- GCC

- 남아프리카

- 기타 중동 및 아프리카

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 북미

제6장 경쟁 구도

- 시장 집중도

- 시장 점유율 분석

- 기업 프로파일

- Abbott Laboratories

- Advanced Brain Monitoring Inc.

- Boston Scientific Corporation

- BrainScope Company Inc.

- Cadwell Industries Inc.

- Cerenion Oy

- Compumedics Limited

- Elekta AB

- EMOTIV Inc.

- GE Healthcare

- Koninklijke Philips NV

- Masimo Corporation

- Medtronic PLC

- Mespere LifeSciences

- Natus Medical Incorporated

- Neurable Inc.

- NeuraSignal, Inc.

- NeuroSky Inc.

- Nihon Kohden Corporation

- Siemens Healthineers AG

- Zeto, Inc.

제7장 시장 기회와 장래의 전망

SHW 25.11.07The brain monitoring market size stands at USD 7.23 billion in 2025 and is on track to reach USD 9.84 billion by 2030, reflecting a 6.36% CAGR.

Demand is expanding as neurological disorders climb to the top of the global disease burden, so providers are investing in faster, more portable diagnostic tools. Advancements in artificial intelligence (AI) are improving multimodal data interpretation, while minimally invasive and wearable sensors are moving routine monitoring into emergency rooms, rehabilitation centers, and homes. Fixed systems still dominate hospital spending, yet growth is strongest in compact and cloud-connected devices that support tele-neurology and decentralized trials. Vendors are refocusing from standalone hardware toward integrated software-as-a-medical-device (SaMD) platforms that automate data analysis, ease staffing gaps, and create recurring revenue from analytics subscriptions.

Global Brain Monitoring Market Trends and Insights

Escalating Prevalence of Neurological Disorders

Cases of stroke, dementia, epilepsy, and neuropathies now affect more than 3 billion individuals-43% of the global population-over 18% jump since 1990. These conditions generate 443 million years of healthy life lost each year, intensifying pressure on health systems. Growing longevity worsens exposure to age-linked illnesses such as Alzheimer's, while metabolic diseases like diabetes triple the incidence of neuropathy. The widening gap between patient demand and neurologist supply pushes hospitals to adopt automated monitoring that triages high-risk cases and feeds data into centralized interpretation hubs. Over the next decade, universal screening programs and community clinics are expected to rely on lower-cost neural sensors to catch early deterioration, sustaining long-run expansion of the brain monitoring market.

AI-Enabled Multimodal Analytics for Enhanced Diagnostic Accuracy

Machine-learning algorithms now integrate EEG, imaging, hemodynamics, and clinical scores to predict mortality or poor outcomes in traumatic brain injury with up to 95.6% accuracy. FDA-cleared platforms such as Ceribell Clarity deliver bedside electrographic status-epilepticus detection within minutes, freeing critical-care teams from manual review. Hospitals in North America and Europe are embedding these SaMD modules into existing monitors, creating service contracts that bundle cloud analytics with consumables. As reimbursement codes recognize algorithm-assisted interpretation, adoption in urban Asia-Pacific centers is accelerating. Over the medium term, richer data pipelines will shorten decision times in stroke and intensive-care units, lifting utilization across the brain monitoring market.

High Purchase and Upkeep Costs for Advanced Modalities

Magnetoencephalography and fMRI systems can exceed USD 3 million, with annual service contracts adding 10-15% of list price. Even mainstream EEG rigs require consumables and calibration that strain hospital operating budgets. Replacement cycles accelerate as vendors launch AI-ready models, prompting finance committees to defer purchases in price-sensitive markets. Open-source wearable fNIRS prototypes from academic labs promise relief, yet certification remains years away, so cost remains a mid-term drag on the brain monitoring market.

Other drivers and restraints analyzed in the detailed report include:

- Proliferation of Wearable and Minimally Invasive Brain Sensors

- Investment Surge in Neuro-Critical-Care Infrastructure

- Global Shortage of Trained Neuro-Technologists

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

EEG systems generated the most significant slice of the brain monitoring market in 2024 by capturing 30.44% revenue. Hospitals rely on them for seizure diagnostics, sedation depth checks, and cerebral ischemia surveillance. Portable rapid-EEG carts now transform emergency workflows by delivering seizure detection within 10 minutes at the bedside, boosting device turnover. Accessories-caps, dry electrodes, cables-grow fastest at an 8.11% CAGR because every new unit drives recurring consumable demand. Flexible polymer electrodes improve comfort and cut setup time, widening EEG use in pediatrics and tele-monitoring. As more hospitals standardize on disposable caps to limit infection risk, the accessories sub-segment will outpace the overall brain monitoring market.

Non-invasive modalities such as scalp EEG, fNIRS, and transcranial Doppler controlled 73.78% of 2024 revenue thanks to lower risk and simpler staffing. Their appeal broadens as algorithm-enhanced systems approximate invasive accuracy. Yet critical-care units still depend on intracranial pressure (ICP) probes and depth electrodes for refractory cases. These invasive tools expand at a 6.95% CAGR as new nanomembrane sensors enter trials, delivered through blood vessels and eliminating skull penetration. Over time, hybrid solutions may blur categories further, sustaining growth in both cohorts of the brain monitoring market.

The Brain Monitoring Market Report is Segmented by Product Type (Magnetoencephalograph (MEG) Systems, Accessories [Electrodes and More], and More), Procedure (Invasive Monitoring and More), Modality (Fixed/Standalone Systems and More), Application (Traumatic Brain Injury and More), End-User (Hospitals and More), and Geography (North America, Europe, Asia-Pacific, and More). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America held 37.75% of global sales in 2024, supported by robust insurance coverage, NIH grants, and a dense network of level-one trauma centers. The brain monitoring market size in the region is expanding at a steady 6.12% CAGR as hospitals refresh fleets to AI-enabled models and outpatient providers embrace remote EEG kits. Europe follows with mature yet methodical procurement; growth runs at 5.87% as budget oversight slows but does not halt adoption. Noteworthy is a handheld ocular laser that detects TBI biomarkers during the golden hour after injury, a potential standard of care in ambulances.

Asia-Pacific posts the quickest gains at an 8.59% CAGR. China funds stroke centers in tier-2 cities; Japan pilots insurance codes for home EEG; India's private hospitals import rapid-EEG carts for emergency departments. Given that 80% of neurological deaths occur in low- and middle-income countries, regional demand for affordable, low-maintenance devices remains high. Local manufacturers have begun supplying cost-effective alternatives, reinforcing supply-chain resilience in the brain monitoring market.

The Middle East & Africa and South America expand from smaller bases as Gulf states build neuro-critical centers and Brazilian hospitals join telestroke networks. However, currency volatility and procurement hurdles temper acceleration. Multilateral lenders and public-private partnerships are expected to underwrite pilot programs that demonstrate clinical and economic value, creating footholds for future market growth.

- Abbott Laboratories

- Advanced Brain Monitoring

- Boston Scientific

- BrainScope Company Inc.

- Cadwell

- Cerenion

- Compumedics

- Elekta

- EMOTIV Inc.

- GE Healthcare

- Koninklijke Philips

- Masimo

- Medtronic

- Mespere LifeSciences

- Natus Medical

- Neurable Inc.

- NeuraSignal, Inc.

- NeuroSky Inc.

- Nihon Kohden

- Siemens Healthineers

- Zeto, Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Escalating prevalence of neurological disorders

- 4.2.2 AI-enabled multimodal analytics that enhance diagnostic accuracy

- 4.2.3 Proliferation of wearable and minimally invasive brain sensors

- 4.2.4 Investment surge in neuro-critical-care infrastructure

- 4.2.5 Brain-focused drug trials requiring objective monitoring biomarkers

- 4.2.6 Accelerated approvals for software-as-a-medical-device modules

- 4.3 Market Restraints

- 4.3.1 High purchase and upkeep costs for advanced modalities

- 4.3.2 Global shortage of trained neuro-technologists

- 4.3.3 Interoperability and cybersecurity risks in connected devices

- 4.3.4 Uncertain reimbursement for ambulatory monitoring solutions

- 4.4 Supply-Chain Analysis

- 4.5 Technological Outlook

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Buyers / Consumers

- 4.6.3 Bargaining Power of Suppliers

- 4.6.4 Threat of Substitute Products & Services

- 4.6.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value)

- 5.1 By Product Type

- 5.1.1 Magnetoencephalograph (MEG) Systems

- 5.1.2 Electroencephalograph (EEG) Systems

- 5.1.3 Transcranial Doppler (TCD) Ultrasound

- 5.1.4 Cerebral Oximeters

- 5.1.5 Magnetic Resonance Imaging (MRI) Devices

- 5.1.6 Intracranial Pressure (ICP) Monitors

- 5.1.7 Computerized Tomography (CT) Devices

- 5.1.8 Positron Emission Tomography (PET) Devices

- 5.1.9 Accessories

- 5.1.9.1 Electrodes

- 5.1.9.2 Sensors

- 5.1.9.3 Cables

- 5.1.9.4 Gels & Pastes

- 5.1.9.5 Other Accessories

- 5.1.10 Other Brain Monitoring Devices

- 5.2 By Procedure

- 5.2.1 Invasive Monitoring

- 5.2.2 Non-invasive Monitoring

- 5.3 By Modality

- 5.3.1 Fixed / Standalone Systems

- 5.3.2 Portable & Wearable Systems

- 5.4 By Application

- 5.4.1 Traumatic Brain Injury

- 5.4.2 Stroke

- 5.4.3 Epilepsy

- 5.4.4 Parkinson's Disease

- 5.4.5 Alzheimer's & Other Dementias

- 5.4.6 Sleep Disorders

- 5.4.7 Other Neurological Conditions

- 5.5 By End-User

- 5.5.1 Hospitals

- 5.5.2 Diagnostic & Imaging Centers

- 5.5.3 Ambulatory Surgical & Specialty Clinics

- 5.5.4 Home-care Settings & Tele-neurology Platforms

- 5.5.5 Academic & Research Institutes

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 Europe

- 5.6.2.1 Germany

- 5.6.2.2 United Kingdom

- 5.6.2.3 France

- 5.6.2.4 Italy

- 5.6.2.5 Spain

- 5.6.2.6 Rest of Europe

- 5.6.3 Asia-Pacific

- 5.6.3.1 China

- 5.6.3.2 India

- 5.6.3.3 Japan

- 5.6.3.4 Australia

- 5.6.3.5 South Korea

- 5.6.3.6 Rest of Asia-Pacific

- 5.6.4 Middle East & Africa

- 5.6.4.1 GCC

- 5.6.4.2 South Africa

- 5.6.4.3 Rest of Middle East & Africa

- 5.6.5 South America

- 5.6.5.1 Brazil

- 5.6.5.2 Argentina

- 5.6.5.3 Rest of South America

- 5.6.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Product Portfolio Analysis

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.4.1 Abbott Laboratories

- 6.4.2 Advanced Brain Monitoring Inc.

- 6.4.3 Boston Scientific Corporation

- 6.4.4 BrainScope Company Inc.

- 6.4.5 Cadwell Industries Inc.

- 6.4.6 Cerenion Oy

- 6.4.7 Compumedics Limited

- 6.4.8 Elekta AB

- 6.4.9 EMOTIV Inc.

- 6.4.10 GE Healthcare

- 6.4.11 Koninklijke Philips N.V.

- 6.4.12 Masimo Corporation

- 6.4.13 Medtronic PLC

- 6.4.14 Mespere LifeSciences

- 6.4.15 Natus Medical Incorporated

- 6.4.16 Neurable Inc.

- 6.4.17 NeuraSignal, Inc.

- 6.4.18 NeuroSky Inc.

- 6.4.19 Nihon Kohden Corporation

- 6.4.20 Siemens Healthineers AG

- 6.4.21 Zeto, Inc.

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment