|

시장보고서

상품코드

1850123

항공 관제(ATC) 장비 시장 : 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Air Traffic Control Equipment - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

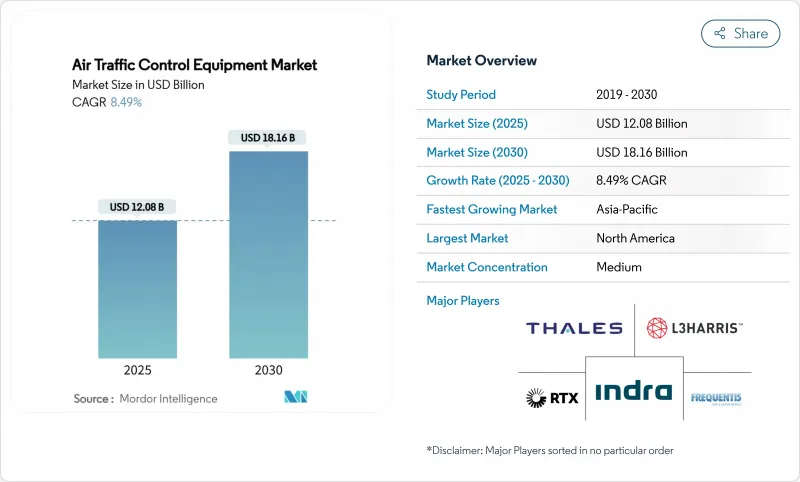

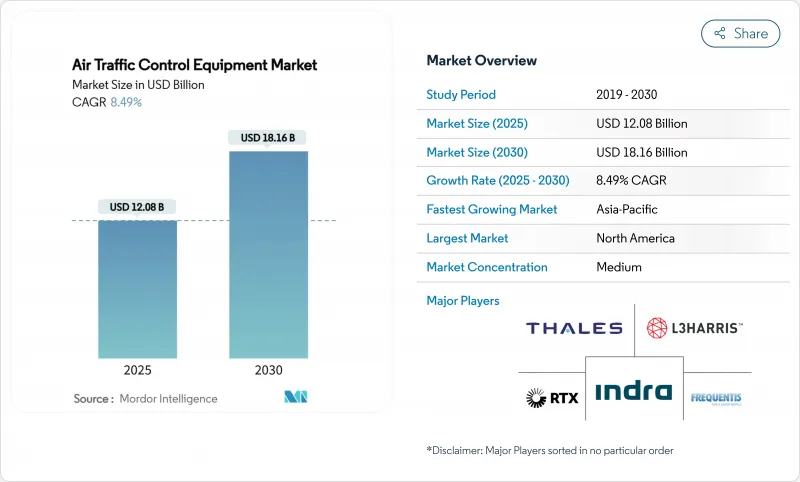

항공 관제(ATC) 장비 시장 규모는 2025년에 120억 8,000만 달러, 2030년에는 181억 6,000만 달러에 이르고, 예측기간의 CAGR은 8.49%를 나타낼 전망입니다.

항공 관제 장비 시장은 각국이 더 많은 교통량을 처리하고 안전을 강화하기 위해 공역 시스템을 업그레이드함에 따라 기세를 늘리고 있습니다. 이 변화의 중심에 있는 것이 공공 투자입니다. 미국 연방 항공국은 노후화된 레이더와 무선을 교환하기 위해 150억 달러를 할당해 차세대 관제 네트워크의 기초를 세웠습니다. 아시아 각지에서도 국가 프로그램이 비슷한 변화를 촉구하고 있습니다. 인도의 'One Airspace'계획은 민간과 군사의 일체화를 목표로 하는 것으로, 중국은 증가하는 비행 수요에 대응하기 위해 고도의 감시와 자동화에 대한 지출을 늘리고 있습니다. 이러한 이니셔티브는 상황 인식을 개선하고 교통 흐름을 원활하게 하는 자동화, 디지털화 및 통합된 모니터링을 위한 광범위한 움직임을 가리킵니다. 민간항공기관과 방위기관 수요는 시장의 꾸준한 성장과 지속적인 혁신을 지원합니다.

세계 항공 관제(ATC) 장비 시장 동향과 통찰

다음과 SESAR에 의한 디지털화 물결

유럽의 ATM 마스터 플랜은 2050년까지 투자 단위당 EUR 17의 수익을 얻는 것으로 평가되었으며, 당국이 클라우드 네이티브 및 상호 운용 가능한 아키텍처에 예산을 돌려주기를 촉구하고 있습니다. 미국의 병렬 NextGen 프로그램은 위성 기반 네비게이션, 시간 기반 흐름 관리 및 디지털 음성 스위칭을 선호하여 플랫폼 공급업체에 여러 해 주문을 확정했습니다. 최상급 공급업체는 소프트웨어 업데이트를 간소화하고 원격 유지보수를 용이하게 하는 Kubernetes 호환 개방형 시스템으로 대응했습니다.

ADS-B Out의 의무화

12개국이 정의된 공역대의 ADS-B를 시행하여 트랜스폰더와 관련된 지상 수신기의 후부 수요를 유지했습니다. FAA는 ADS-B 데이터를 활주로 진입을 줄이는 Surface Awareness Initiative에 활용하여 450개 이상의 공항에서 AeroBOSS를 배포할 권한을 Indra에게 부여했습니다. 유럽에서는 Digital Sky 프레임 워크 하에서 ADS-C 공통 서비스를 진행하여 모니터링 데이터의 생태계를 확대했습니다.

높은 CAPEX와 긴 인증 사이클

미국 정부 책임국은 FAA 시스템의 37%가 지속 불가능하다는 것을 밝혔지만, 리플레이스 프로젝트는 종종 여러 해에 걸친 인증 취득 장애물에 직면하여 지출 연장을 늦추고 있었습니다. 유럽의 EASA 규칙 2023/1769는 ATM 장비에 설계 조직의 승인을 부과하여 소규모 공급업체의 개발 일정을 연장했습니다.

부문 분석

통신 플랫폼은 ATC 장비 시장의 2024년 매출의 42.50%를 차지하며 탄력적인 음성 채널 및 데이터 링크의 중요성을 강조합니다. 인드라가 FAA에서 2억 4,430만 달러를 획득하고 4만 6,000대의 듀얼 모드 디지털 라디오를 공급한 것은 노후화된 아날로그 라디오 교체의 기세를 보여줍니다. Frequentis와 같은 공급업체는 세계 관제관 포지션의 30% 점유율을 차지하고 있으며 기존 공급업체가 즐길 수 있는 규모의 이점을 돋보이게 합니다.

리모트 타워 모듈과 디지털 타워 모듈은 2024년 수익에서 차지하는 비율은 5.3%에 불과하지만, 공항이 여러 공항 센터 아래에 감시를 통합함에 따라 11.20%의 연평균 복합 성장률(CAGR)을 보일 것으로 예측되고 있습니다. 이러한 전환으로 북유럽공항에서는 인건비가 최대 30% 절감되어 투하자본이익률이 향상되어 규제당국이 4K센서를 이용한 저시인성 운항을 인정하게 되었습니다.

민간 항공사는 세계 여객 수요 회복과 ADS-B 장비 의무화로 ATC 장비 시장의 2024년 수익의 66.45%를 창출했습니다. 보잉은 아프리카 항공기가 2043년까지 두 배로 늘어날 것으로 예측하고, 관제탑, 레이더 및 데이터 링크 업그레이드에 대한 하류 수요가 근본적임을 보여줍니다. 동시에 방위기관은 조달을 가속화하고 2025년부터 2030년까지의 CAGR 9.85%로 군사수입을 증가시켰습니다. 미국 공군이 19대의 TPY-4 레이더를 4억 7,200만 달러로 주문한 것은 이 부문으로 흐르는 현대화 계약의 규모를 부각시켰습니다.

군사 용도는 중층 방공 우선 순위를 반영합니다. 사이버 보안, 인공지능, UTM 하드웨어를 둘러싼 민간 및 방어 요건 간의 수렴은 공급업체의 경계를 모호하게 하고 통합 플랫폼 공급업체에게 교차 판매 기회를 계속 열고 있습니다.

지역 분석

북미는 디지털 음성교환, 레이더교환, 관제탑 건설에 관한 FAA의 150억 달러 청사진에 힘입어 ATC 기기 시장의 2024년 수익의 40.54%를 유지했습니다. 나브 캐나다는 고립된 비행장을 원격으로 관리하는 디지털 비행장 항공 교통 서비스에 투자하여 운영 혁신에서 이 지역의 리더십을 강화했습니다.

아시아태평양은 CAGR 10.50%로 가장 높은 성장을 기록했습니다. 인도의 "하나의 공역"구상은 280만 해리 2를 하나의 국가 시스템에 통합하여 중국은 주요 허브 공항의 새로운 활주로와 동시에 CNS/ATM의 전개를 가속화했습니다. 호주는 오프사이트 타워 기술을 조기에 채택하여 지역 기세를 더욱 가속화했습니다.

유럽은 SESAR 3 계획을 예정대로 진행하고 2050년까지 4억톤의 CO2 감축을 약속하는 디지털 스카이 프로젝트에 300억 유로를 투입했습니다. 중동 및 아프리카에서는 두바이, 리야드, 도하에서 1조 달러에 이르는 공항 확장에 견인되어 활발한 지출이 보였습니다. 라틴아메리카는 인드라가 이 지역의 관제 센터의 70%를 근대화함으로써 혜택을 받았지만, 자금 제약으로 성장 궤도가 완만해졌습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 서포트

목차

제1장 서론

- 조사의 전제조건과 시장의 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- NextGen과 SESAR가 자금 제공하는 디지털화의 파

- 의무화된 ADS-B Out 기한

- 2차 공항에서의 리모트/디지털 타워의 도입

- UAS 교통 관리(UTM) 하드웨어 통합

- AI 구동형 예측 공역 관리 플랫폼

- 궤도 기반의 운용에 있어서의 그린 비행 회랑 수요

- 시장 성장 억제요인

- 고액의 설비 투자와 긴 인증 사이클

- 레거시 시스템의 상호 운용성의 병목

- IP 기반 VCS에서 사이버 보안 책임 증가

- 도시 회랑의 RF 스펙트럼의 혼잡

- 밸류체인 분석

- 규제 상황

- 기술의 전망

- Porter's Five Forces 분석

- 구매자의 협상력/소비자

- 공급기업의 협상력

- 신규 참가업체의 위협

- 대체품의 위협

- 경쟁 기업간 경쟁 관계

제5장 시장 규모와 성장 예측

- 기기별

- 통신 기기

- 네비게이션 장비

- 감시/자동화 시스템

- 리모트/디지털 타워 모듈

- 최종 사용자별

- 상업용

- 군

- 공항유형별

- 브라운필드 공항

- 그린필드 공항

- 투자 카테고리별

- 신규 설치

- 근대화와 업그레이드

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 러시아

- 기타 유럽

- 아시아태평양

- 중국

- 일본

- 인도

- 한국

- 호주

- 기타 아시아태평양

- 남미

- 브라질

- 기타 남미

- 중동 및 아프리카

- 중동

- 아랍에미리트(UAE)

- 사우디아라비아

- 튀르키예

- 기타 중동

- 아프리카

- 남아프리카

- 기타 아프리카

- 북미

제6장 경쟁 구도

- 시장 집중도

- 전략적 동향

- 시장 점유율 분석

- 기업 프로파일

- Thales Group

- IndraSistemas SA

- RTX Corporation

- L3Harris Technologies, Inc.

- SITA NV

- Honeywell International Inc.

- Frequentis AG

- ACAMS AS

- Searidge Technologies

- Saab AB

- Rohde & Schwarz USA, Inc.(Rohde & Schwarz GmbH & Co. KG)

- General Dynamics Mission Systems, Inc.(General Dynamics Corporation)

- Leonardo SpA

- NEC Corporation

- Intelcan Technosystems Inc.

- Aquila Air Traffic Management Services Limited

- ARTISYS, sro

- Leidos Holdings, Inc.

제7장 시장 기회와 장래의 전망

SHW 25.11.07The air traffic control equipment market size stood at USD 12.08 billion in 2025 and is projected to reach USD 18.16 billion by 2030, reflecting an 8.49% CAGR over the forecast period.

The air traffic control equipment market is gaining momentum as countries upgrade their airspace systems to handle heavier traffic and strengthen safety. Public investment sits at the center of this shift. The Federal Aviation Administration allocated USD 15 billion in the United States to replace aging radars and radios, laying the groundwork for next-generation control networks. Across Asia, national programs are driving similar change. India's One Airspace plan seeks to unify civil and military operations, while China is increasing spending on advanced surveillance and automation to meet rising flight demand. These initiatives point to a broader move toward automated, digital, and integrated monitoring that improves situational awareness and smooths traffic flows. Demand from civil aviation and defense agencies supports steady growth and continued innovation in the market.

Global Air Traffic Control Equipment Market Trends and Insights

NextGen and SESAR-funded digitalization wave

The European ATM Master Plan estimated a EUR 17 return per unit investment by 2050, encouraging authorities to channel budgets toward cloud-native, interoperable architectures. Parallel US NextGen programs prioritized satellite-based navigation, time-based flow management, and digital voice switching, locking in multiyear orders for platform suppliers. Top-tier vendors responded with Kubernetes-enabled open systems that simplify software updates and facilitate remote maintenance.

Mandated ADS-B Out deadlines

Twelve countries enforced ADS-B for defined airspace bands, sustaining retrofit demand for transponders and associated ground receivers. The FAA leveraged ADS-B data in its Surface Awareness Initiative to cut runway incursions, awarding Indra authority to roll out AeroBOSS at more than 450 airports. Europe advanced ADS-C common services under the Digital Sky framework, widening the surveillance data ecosystem.

High CAPEX and lengthy certification cycles

The US Government Accountability Office found 37% of FAA systems unsustainable, yet replacement projects often faced multi-year certification hurdles that slowed spending draws. European EASA Regulation 2023/1769 imposed design-organization approvals on ATM equipment, extending development timelines for small suppliers.

Other drivers and restraints analyzed in the detailed report include:

- Remote/digital tower adoption at secondary airports

- AI-driven predictive airspace management platforms

- Legacy-system interoperability bottlenecks

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Communication platforms represented 42.50% of 2024 revenue in the ATC equipment market, underlining the centrality of resilient voice channels and data links. Indra's USD 244.3 million FAA award to supply 46,000 dual-mode digital radios illustrated replacement momentum for aging analog fleets. Vendors such as Frequentis controlled a 30% share of global controller positions, highlighting the scale economies enjoyed by established providers.

Although remote and digital tower modules account for only 5.3% of 2024 revenue, they are forecast to post the fastest 11.20% CAGR as airports consolidate surveillance under multi-airport centers. The transition reduced staffing costs by up to 30% at Nordic regional fields, bolstering return on invested capital and encouraging regulators to certify low-visibility operations using 4K sensors.

Commercial carriers generated 66.45% of 2024 revenue for the ATC equipment market thanks to the rebound in global passenger demand and mandatory ADS-B equipage. Boeing projected Africa's fleet to double by 2043, indicating persistent downstream demand for tower, radar, and data-link upgrades. At the same time, defense agencies accelerated procurements, lifting military revenue at a 9.85% CAGR from 2025 to 2030. A USD 472 million US Air Force order for 19 TPY-4 radars underscored the size of modernization contracts flowing into the segment.

Military applications are mirroring layered air defense priorities. Convergence between civil and defense requirements around cybersecurity, artificial intelligence, and UTM hardware continues to blur supplier boundaries and open cross-selling opportunities for integrated platform vendors.

The Air Traffic Control Equipment Market Report is Segmented by Equipment Type (Communication Equipment, Navigation Equipment, and More), End-User (Commercial and Military), Airport Type (Brownfield and Greenfield), Investment (New Installations and Modernization and Upgradation), and Geography (North America, Europe, Asia-Pacific, South America and More). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America retained 40.54% of 2024 revenue in the ATC equipment market, anchored by the FAA's USD 15 billion blueprint for digital voice switching, radar replacement, and tower construction. NAV CANADA invested in Digital Aerodrome Air Traffic Services to remotely manage isolated aerodromes, reinforcing the region's leadership in operational innovation.

Asia-Pacific registered the highest regional growth at 10.50% CAGR. India's "One Airspace" initiative unified 2.8 million nmi2 under a single national system, while China accelerated CNS/ATM roll-outs in tandem with new runways at major hubs. Australia's early adoption of off-site tower technology further boosted regional momentum.

Europe progressed on schedule with the SESAR 3 program, channeling EUR 30 billion into Digital Sky projects that promise 400 million tonnes of CO2 savings by 2050. The Middle East and Africa showed pockets of intense spending, led by USD 1 trillion of airport expansions across Dubai, Riyadh, and Doha. Latin America benefited from Indra's modernization of 70% of the region's control centers, though funding constraints moderated its growth trajectory.

- Thales Group

- IndraSistemas S.A.

- RTX Corporation

- L3Harris Technologies, Inc.

- SITA N.V.

- Honeywell International Inc.

- Frequentis AG

- ACAMS AS

- Searidge Technologies

- Saab AB

- Rohde & Schwarz USA, Inc. (Rohde & Schwarz GmbH & Co. KG)

- General Dynamics Mission Systems, Inc. (General Dynamics Corporation)

- Leonardo S.p.A

- NEC Corporation

- Intelcan Technosystems Inc.

- Aquila Air Traffic Management Services Limited

- ARTISYS, s.r.o.

- Leidos Holdings, Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 NextGen and SESAR-funded digitalization wave

- 4.2.2 Mandated ADS-B Out deadlines

- 4.2.3 Remote/digital tower adoption at secondary airports

- 4.2.4 Integration of UAS-traffic-management (UTM) hardware

- 4.2.5 AI-driven predictive airspace management platforms

- 4.2.6 Green-flight-corridor demand for trajectory-based ops

- 4.3 Market Restraints

- 4.3.1 High CAPEX and lengthy certification cycles

- 4.3.2 Legacy-system interoperability bottlenecks

- 4.3.3 Escalating cyber-security liability on IP-based VCS

- 4.3.4 Urban-corridor RF-spectrum congestion

- 4.4 Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Buyers/Consumers

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Equipment Type

- 5.1.1 Communication Equipment

- 5.1.2 Navigation Equipment

- 5.1.3 Surveillance/Automation Systems

- 5.1.4 Remote / Digital Tower Modules

- 5.2 By End User

- 5.2.1 Commercial

- 5.2.2 Military

- 5.3 By Airport Type

- 5.3.1 Brownfield Airports

- 5.3.2 Greenfield Airports

- 5.4 By Investment Category

- 5.4.1 New Installations

- 5.4.2 Modernization and Upgradation

- 5.5 By Region

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Russia

- 5.5.2.5 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 South Korea

- 5.5.3.5 Australia

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Rest of South America

- 5.5.5 Middle East and Africa

- 5.5.5.1 Middle East

- 5.5.5.1.1 United Arab Emirates

- 5.5.5.1.2 Saudi Arabia

- 5.5.5.1.3 Turkey

- 5.5.5.1.4 Rest of Middle East

- 5.5.5.2 Africa

- 5.5.5.2.1 South Africa

- 5.5.5.2.2 Rest of Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global-level Overview, Market-level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Thales Group

- 6.4.2 IndraSistemas S.A.

- 6.4.3 RTX Corporation

- 6.4.4 L3Harris Technologies, Inc.

- 6.4.5 SITA N.V.

- 6.4.6 Honeywell International Inc.

- 6.4.7 Frequentis AG

- 6.4.8 ACAMS AS

- 6.4.9 Searidge Technologies

- 6.4.10 Saab AB

- 6.4.11 Rohde & Schwarz USA, Inc. (Rohde & Schwarz GmbH & Co. KG)

- 6.4.12 General Dynamics Mission Systems, Inc. (General Dynamics Corporation)

- 6.4.13 Leonardo S.p.A

- 6.4.14 NEC Corporation

- 6.4.15 Intelcan Technosystems Inc.

- 6.4.16 Aquila Air Traffic Management Services Limited

- 6.4.17 ARTISYS, s.r.o.

- 6.4.18 Leidos Holdings, Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment