|

시장보고서

상품코드

1850126

미국의 당뇨병 기기 시장 : 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)United States Diabetes Devices - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

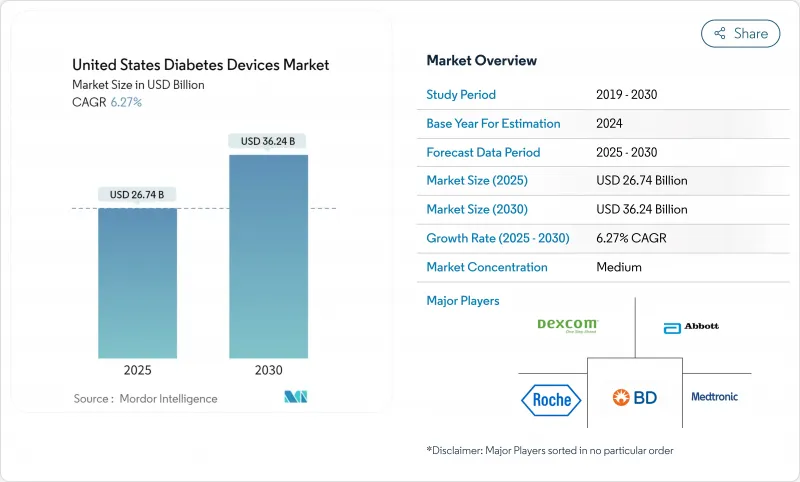

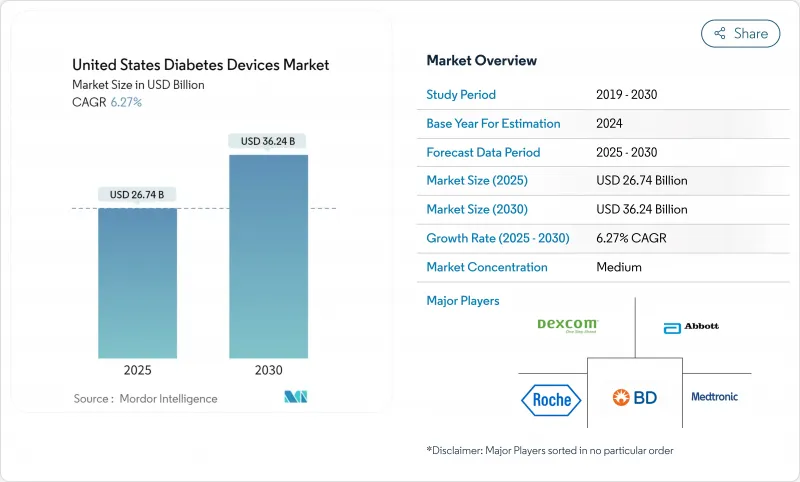

미국 당뇨병 기기 시장 규모는 2025년에 267억 4,000만 달러, 예측되고, 2030년에는 362억 4,000만 달러에 이를 것으로 예측됩니다.

이 궤적은 3,840만명의 미국인이 당뇨병을 앓고 있다는 역학적 배경 하에서 전개되고 있으며, 이 수치는 모니터링과 관리의 두 솔루션에 대한 수요를 계속 추진하고 있습니다. 2022년에 4,130억 달러에 달하는 경제적 부담은 부적절한 관리로 인한 비용을 더욱 드러내고 의료 기술을 정책 논의의 중심에 둡니다. 그 직접적인 결과 중 하나는 연결 장치의 보급 증가이며, 이는 현재 미국의 의료 시스템의 대부분에서 원격 첫 번째 관리 모델을 지원합니다. 만성적인 인구가 많기 때문에 제품 수명주기가 길고 제조업체는 많은 연구비를 회수하면서도 가격을 조사 한도 내로 줄일 수 있습니다. 이러한 지속적인 임상 요구와 정책 지원의 조합으로 미국 당뇨병 기기 산업은 세계적인 제품 상시의 중요한 지표가 되었습니다.

향후 5년간 신규 엔지니어링과 마찬가지로 지불측 규칙이 경쟁 분야를 형성하게 됩니다. Medicare는 지속적인 포도당 모니터링(CGM)의 적용 범위를 인슐린을 사용하는 모든 수혜자로 확장하고 이미 수백만 명의 환자를 대상으로합니다. 이 결정은 또한 연방정부 정책을 늦추면 역선택을 두려워하는 민간보험사의 병행운동을 야기했습니다. 지불자의 자유화에 따라 공급업체는 리필 사이클을 단축하고 서비스 제공을 위한 총 비용을 줄이는 약국과 소비자에게 직접 제제를 선호하도록 워크플로우를 재설계하고 있습니다. 결과적으로 모니터링 및 투약 하드웨어가 앱 기반 생태계에 통합되어 소프트웨어 업그레이드가 센서의 화학적 특성과 마찬가지로 전략적으로 중요해졌습니다. 따라서 CAGR 6.27%라는 소모품의 풀스루 강화는 기본 하드웨어의 평균 판매 가격이 완만한 하락을 계속하더라도 조익률이 확대됨을 시사합니다.

미국 당뇨병 기기 시장 동향과 통찰

메디케어 상환 확대가 뒷받침되는 실시간 CGM 채택 급증

메디케어의 2023년 4월 정책 갱신으로 CGM의 대상이 모든 인슐린 사용자와 문제가 있는 저혈당 환자로 확대되었고, 중요한 접근 장벽이 제거되었습니다. 보험 적용 요건으로 인해 지문 문서가 사라졌기 때문에 처방 포기율이 급격히 떨어졌습니다. 공급자는 현재 자동화된 경고를 사용하여 포도당 상승을 차단하고 많은 일상적인 전화를 데이터 중심의 개입으로 대체하고 있습니다. 이 업무 완화로 클리닉은 인원을 늘리지 않고도 더 많은 환자를 등록할 수 있게 되어 명확한 생산성 배당입니다.

청소년의 비만 증가는 당뇨병의 조기 발병을 증가시킵니다.

소아 비만의 급증은 청소년기의 2형 당뇨병 진단 증가로 이어지고, 평생 동안 장비 치료에 노출될 기회를 확대하고 있습니다. 제조업체 각사는 소형의 온 보디 트랜스미터나 다채로운 유저 인터페이스 등, 청소년을 위한 폼 팩터를 릴리스 하고 있어, 학교 환경에 있어서의 기기의 편견을 완화하는데 도움이 되고 있습니다. 이러한 사용자는 수십년동안 기술을 필요로 할 수 있기 때문에 10대에 설립된 제품 로열티는 비정상적으로 끈질긴 수익원을 창출할 수 있습니다. 이러한 인구 역학의 변화는 또한 장기적인 전망을 보이는 보험 수리 모델이 고급 펌프 및 센서의 최종 설치 대수를 과소평가할 수 있음을 시사합니다.

높은 관련 비용

기술 보급의 가장 큰 장벽은 여전히 비용입니다. 2024년 청구 분석에 따르면 소매 약국에서 CGM 처방을 받은 환자의 연간 의료비는 내구성 의료장비 채널을 사용한 환자보다 53% 높았습니다. 보조 보험이 있더라도, 메디케어의 일반적인 20% 공동 보험은 예산에 제약이 있는 노인의 발목이 됩니다. 따라서 가격에 대한 민감성은 고소득층에 대한 도입을 왜곡시켜 혈당 조절의 격차를 넓히고 있습니다.

부문 분석

모니터링 장비는 2024년 미국 당뇨병 기기 시장 점유율의 58.12%를 차지하며 제품 분류에서 유일하게 최대 판매 블록을 형성하고 있습니다. 지속 포도당 모니터링 시스템은 2025년부터 2030년까지의 예측 CAGR이 7.82%로 섹터 평균을 크게 상회하고 있으며, 이 확산은 이익률이 높은 디스포저블로의 믹스 시프트의 진행을 시사하고 있습니다. 많은 공급업체는 현재 스타터 키트에 범위 내 시간 그래프를 자동으로 생성하는 스마트폰 앱을 번들로 제공하고 있어 수작업으로 기록장의 필요성을 줄이고 인지 가치를 높이고 있습니다. CGM 데이터는 5분마다 실용적인 통찰력을 제공하기 때문에 임상의는 손가락을 찌르는 단독 가치가 아니라 동향을 기반으로 치료를 증가시키는 데 점점 더 익숙해지고 있으며 장비의 필수성이 강화되고 있습니다. 주목할만한 파급 효과는 SMBG 스트립 시장의 축소입니다. 과도한 환자가 거의 되돌아가지 않기 때문에 레거시 미터에 크게 의존하는 기업의 경우, 수익 창출이 가속화됩니다.

FDA가 2024년에 특히 비인슐린 사용자를 대상으로 하는 상용 바이오센서를 허가함에 따라 단기 수익화가 현금 지불 구매에 의존하더라도 대응 가능한 수영장은 실질적으로 수천만 명의 성인으로 퍼졌습니다. 초기 상업 시험에서 소매 약국 직원이 10분 미만으로 온보딩을 완료할 수 있음이 분명해졌으며, 처방전 기반 워크플로와는 현저하게 다른 확장 가능한 POS 모델을 제안했습니다. 또한 포도당의 동향은 보다 광범위한 웰니스 대시보드에 자연스럽게 적합하기 때문에 이 움직임은 가전 제조업체를 화제에 도입하고 있습니다. 경쟁의 관점에서 모니터링 대기업은 의료 주장과 라이프 스타일 브랜딩의 균형을 맞추는 전략적 딜레마에 직면하고 있습니다.

2024년 미국 당뇨병 기기 시장 규모의 92.14%는 2형 당뇨병 환자이며, 1인당 소비액이 1형 당뇨병 환자보다 낮더라도 그 수가 많음이 절대적인 대수 성장의 원동력이 됩니다. 성인 2형 당뇨병 환자를 위해 조정된 자동 인슐린 투여 알고리즘이 2024년에 규제 당국에 승인된 것은 환자 그룹 간의 기술적 동등성 전환점을 나타냅니다. 지불자가 응급 진찰의 감소를 보여주는 초기 실제 데이터를 연구함에 따라 보험 적용 정책이 확대되고 과거의 접근 격차가 더욱 손상 될 것으로 예측됩니다. 2형은 인생의 후반에 발생하는 경우가 많기 때문에 기기 설계의 우선순위는 간소화된 인터페이스와 낮은 유지보수를 포함하고, 튜브식 시스템보다 패치식 펌프가 선호되는 요인이 되고 있습니다.

판매량의 8%를 차지하는 1형 환자는 여러 기기 클래스를 동시에 채택하여 펌웨어의 진보에 따라 하드웨어 교환이 보다 신속하게 이루어지기 때문에 예측 CAGR은 6.92%로 높습니다. 1형 당뇨병 환자의 10명 중 8명 가까이가 이미 CGM과 펌프 요법을 병용하고 있어, 단계적인 소프트웨어 혁신에 의해 측정 가능한 임상적 이익을 이끌어낼 수 있는 환경을 만들어 가고 있습니다. 이 코호트는 또한 학문적 조사가 필요한 고밀도 데이터 세트를 생성하기 때문에 알고리즘에 의한 투여에 대한 첫인간 연구의 최강의 후보가 됩니다. 1형 당뇨병 환자를 위한 임상시험에서 얻은 지견은 2형 당뇨병 환자를 위한 후기 프로토콜에 반영되는 경우가 많으며, 이 소규모 부문을 차세대 제품의 실험장으로 효과적으로 자리매김하고 있습니다.

이 보고서는 미국 당뇨병 기기 회사를 대상으로 하며 관리 장치(인슐린 펌프, 인슐린 주사기, 재사용 가능한 펜 카트리지, 인슐린 일회용 펜, 제트 인젝터) 및 모니터링 장치(자가혈당 모니터링, 지속 포도당 모니터링)로 구분됩니다. 이 보고서는 위 부문의 금액(단위 : 달러)을 제공합니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월의 애널리스트 서포트

목차

제1장 서론

- 조사의 전제조건과 시장의 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 메디케어의 상환 확대에 의해 실시간 CGM의 도입이 급증

- 젊은이의 비만률 상승과 당뇨병의 조기 발병 증가

- 당뇨병 기기와 스마트폰 생태계의 통합으로 환자 참여도 향상

- 인슐린 주입 장치의 사용 증가

- 가치에 근거한 케어로의 이행에 의한 원격 모니터링의 보급 촉진

- 당뇨병의 유병률 증가

- 시장 성장 억제요인

- 높은 관련 비용

- 보험 적용 범위의 제한

- 일회용 플라스틱 펜에 대한 지속가능성에 대한 압력

- 엄격한 규제 요건

- 공급망 분석

- 규제 전망

- 기술의 전망

- Porter's Five Forces 분석

- 공급기업의 협상력

- 구매자의 협상력

- 신규 참가업체의 위협

- 대체품의 위협

- 경쟁 기업간 경쟁 관계

- 시장 지표

- 1형 당뇨병 환자수

- 2형 당뇨병 환자수

제5장 시장 규모와 성장 예측(가치와 양)

- 기기 유형별

- 감시 기기

- 자기 혈당 측정(SMBG)

- 포도당 미터

- 테스트 스트립

- 란셋

- 연속 혈당 모니터링(CGM)

- 센서

- 내구품(트랜스미터와 리더)

- 관리 기기

- 인슐린 펌프

- 펌프장치

- 저수지

- 주입 세트

- 인슐린 펜

- 일회용 펜

- 재사용 가능한 펜용 카트리지

- 인슐린 주사기

- 제트 인젝터

- 감시 기기

- 환자 유형별

- 1형 당뇨병

- 2형 당뇨병

- 최종 사용자별

- 재택 케어 설정

- 병원과 전문 클리닉

- 기타

- 유통 채널별

- 병원 약국

- 소매 약국

- 전자상거래

- 미국 지역별

- 북동

- 중서부

- 남

- 서쪽

제6장 시장 지표

- 1형 당뇨병 환자수

- 2형 당뇨병 환자수

제7장 경쟁 구도

- 시장 집중도

- 시장 점유율 분석

- 기업 프로파일

- Abbott Laboratories

- Medtronic plc

- Dexcom Inc.

- Insulet Corporation

- F. Hoffmann-La Roche AG

- Becton, Dickinson and Company

- Tandem Diabetes Care Inc.

- Novo Nordisk A/S

- Eli Lilly and Company

- Sanofi

- Ypsomed Holding AG

- Senseonics Holdings Inc.

- Ascensia Diabetes Care

- Glooko Inc.

- AgaMatrix Inc.

- Bigfoot Biomedical

- Terumo Corporation

- Owen Mumford Ltd.

제8장 시장 기회와 장래의 전망

- 화이트 스페이스와 미충족 요구의 평가

The US Diabetes Devices market size is estimated at USD 26.74 billion in 2025 and is forecast to reach USD 36.24 billion by 2030, reflecting a compound annual growth rate (CAGR) of 6.27 % over the period.

This trajectory unfolds against an epidemiological backdrop of 38.4 million Americans living with diabetes, a figure that continues to propel demand for both monitoring and management solutions. The economic burden of USD 413 billion in 2022 further exposes the cost of inadequate control and places medical technology at the center of policy discussions . One direct consequence is the rising penetration of connected devices, which now underpin remote-first care models across much of the US healthcare system. The sizeable chronic population ensures long product lifecycles, giving manufacturers scope to recoup hefty research outlays while still holding prices within reimbursement ceilings. Because of this combination of persistent clinical need and policy support, the US Diabetes Devices industry has become a crucial bellwether for global product launches, as firms increasingly prioritize stateside clearance before moving into other regions.

Over the next five years, payer rules are set to shape the competitive field almost as strongly as novel engineering. Medicare's expansion of continuous glucose monitoring (CGM) coverage to all insulin-using beneficiaries has already broadened the eligible pool by several million patients. That decision has also triggered parallel moves among commercial insurers that fear adverse selection if they lag behind federal policy. As the payer landscape liberalizes, suppliers are re-designing workflows to favor pharmacy and direct-to-consumer dispensing, which shorten refill cycles and reduce total cost to serve. An observable result is the convergence of monitoring and dosing hardware inside app-based ecosystems, making software upgrades as strategically important as sensor chemistry. The stronger pull-through of consumables implied by a 6.27 % CAGR therefore hints at widening gross margins, even if average selling prices of base hardware continue their gradual decline.

United States Diabetes Devices Market Trends and Insights

Surge in Adoption of Real-Time CGM Driven by Medicare Reimbursement Expansion

Medicare's April 2023 policy update extended CGM eligibility to all insulin users and individuals with problematic hypoglycemia, removing a critical access barrier . Prescription abandonment rates fell sharply as finger-stick documentation disappeared from coverage requirements. Providers now use automated alerts to intercept glucose excursions, replacing many routine phone calls with data-driven interventions. This operational relief enables clinics to enroll more patients without expanding staffing, a clear productivity dividend.

Rising Prevalence of Obesity Among Youth Increasing Earlier Onset Diabetes

The sharp climb in childhood obesity is translating into more type 2 diagnoses during adolescence, expanding lifetime exposure to device therapy. Manufacturers are releasing youth-oriented form factors, such as smaller on-body transmitters and colorful user interfaces, which help mitigate device stigma in school settings. Because these users may require technology for several decades, product loyalty established in teenage years could create unusually sticky revenue streams. This demographic shift also suggests that long-horizon actuarial models may underestimate the eventual installed base of advanced pumps and sensors.

High Associated Costs

Cost remains the single biggest brake on technology penetration. A 2024 claims analysis reported that patients filling CGM prescriptions at retail pharmacies incurred 53 % higher annual medical costs than those using durable medical equipment channels . Even with supplemental coverage, the typical 20 % Medicare co-insurance can deter budget-constrained seniors. Price sensitivity thus skews adoption toward higher-income users, widening glycemic control disparities.

Other drivers and restraints analyzed in the detailed report include:

- Integration of Diabetes Devices with Smartphone Ecosystem Boosting Patient Engagement

- Growing Usage of Insulin Delivery Devices

- Shift Toward Value-Based Care Incentivizing Remote Monitoring Penetration

- Insurance Coverage Limitations

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Monitoring devices account for 58.12% US Diabetes Devices market share in 2024, creating the single largest revenue block within the product taxonomy. Continuous glucose monitoring systems exhibit a forecast 7.82% CAGR from 2025 to 2030, markedly faster than the sector average, and this spread implies progressive mix shift toward higher-margin disposables. Many suppliers now bundle starter kits with smartphone apps that auto-generate time-in-range charts, reducing the need for manual logbooks and boosting perceived value. Because CGM data provide actionable insights every five minutes, clinicians are increasingly comfortable titrating therapy based on trends rather than isolated finger-stick values, reinforcing device indispensability. A notable spillover is the shrinking SMBG strip market, as patients who transition seldom revert, which accelerates revenue cannibalization for firms still heavily exposed to legacy meters.

The FDA's 2024 clearance of an over-the-counter biosensor specifically aimed at non-insulin users effectively widened the addressable pool by tens of millions of adults, even if near-term monetization relies on cash-pay purchases. Early commercial pilots reveal that retail pharmacy staff can complete onboarding in under 10 minutes, hinting at a scalable point-of-sale model that differs markedly from prescription-based workflows. The move has also introduced consumer electronics players into the conversation, as glucose trend lines fit naturally within broader wellness dashboards. From a competitive standpoint, monitoring giants face the strategic dilemma of balancing medical claims with lifestyle branding, because over-medicalizing messaging may dampen mass-market appeal.

Type 2 patients account for 92.14% of US Diabetes Devices market size in 2024, and their sheer numbers ensure they drive absolute unit growth even if per-capita spend lags type 1 cohorts. The 2024 regulatory nod for an automated insulin dosing algorithm tailored to adults with type 2 diabetes signals a turning point in technology parity between patient groups. As payers study early real-world data showing fewer emergency visits, coverage policies are expected to broaden, further eroding historical access gaps. Because type 2 onset often occurs later in life, device design priorities include simplified interfaces and low maintenance, factors that favor patch-style pumps over tubed systems.

Type 1 patients, representing 8% of volume, sustain a higher 6.92% forecast CAGR because they adopt multiple device classes in tandem and replace hardware more rapidly as firmware advances. Nearly eight out of ten people with type 1 diabetes already combine CGM with pump therapy, creating an environment where incremental software innovation can unlock measurable clinical gains. This cohort also generates dense data sets that attract academic scrutiny, making them prime candidates for first-in-human studies of algorithmic dosing. The knowledge spillovers from type 1 trials often inform later-stage protocols for type 2 users, effectively positioning this smaller segment as a proving ground for next-generation products.

The Report Covers US Diabetes Devices Companies and It is Segmented by Management Devices (insulin Pumps, Insulin Syringes, Cartridges in Reusable Pens, Insulin Disposable Pens, and Jet Injectors) and Monitoring Devices (self-Monitoring Blood Glucose and Continuous Glucose Monitoring). The Report Offers the Value (in USD) for the Above Segments.

List of Companies Covered in this Report:

- Abbott Laboratories

- Medtronic

- Dexcom

- Insulet

- Roche

- Beckton Dickinson

- Tandem Diabetes Care

- Novo Nordisk

- Eli Lilly and Company

- Sanofi

- Ypsomed

- Senseonics

- Ascensia

- Glooko Inc.

- AgaMatrix

- Bigfoot Biomedical

- Terumo

- Owen Mumford

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surge in Adoption of Real-Time CGM Driven by Medicare Reimbursement Expansion

- 4.2.2 Rising Prevalence of Obesity Among Youth Increasing Earlier Onset Diabetes

- 4.2.3 Integration of Diabetes Devices with Smartphone Ecosystem Boosting Patient Engagement

- 4.2.4 Growing Usage of Insulin Delivery Devices

- 4.2.5 Shift Toward Value-Based Care Incentivizing Remote Monitoring Penetration

- 4.2.6 Increasing Prevalence of Diabetes

- 4.3 Market Restraints

- 4.3.1 High Associated Costs

- 4.3.2 Insurance Coverage Limitations

- 4.3.3 Sustainability Pressure on Single-Use Plastic Pens

- 4.3.4 Stringent Regulatory Requirements

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Outlook

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Market Indicators

- 4.8.1 Type-1 Diabetes Population

- 4.8.2 Type-2 Diabetes Population

5 Market Size & Growth Forecasts (Value & Volume)

- 5.1 By Device Type

- 5.1.1 Monitoring Devices

- 5.1.1.1 Self-Monitoring Blood Glucose (SMBG)

- 5.1.1.1.1 Glucometers

- 5.1.1.1.2 Test Strips

- 5.1.1.1.3 Lancets

- 5.1.1.2 Continuous Glucose Monitoring (CGM)

- 5.1.1.2.1 Sensors

- 5.1.1.2.2 Durables (Transmitters & Readers)

- 5.1.2 Management Devices

- 5.1.2.1 Insulin Pumps

- 5.1.2.1.1 Pump Device

- 5.1.2.1.2 Reservoir

- 5.1.2.1.3 Infusion Set

- 5.1.2.2 Insulin Pens

- 5.1.2.2.1 Disposable Pens

- 5.1.2.2.2 Cartridges for Re-usable Pens

- 5.1.2.3 Insulin Syringes

- 5.1.2.4 Jet Injectors

- 5.1.1 Monitoring Devices

- 5.2 By Patient Type

- 5.2.1 Type-1 Diabetes

- 5.2.2 Type-2 Diabetes

- 5.3 By End User

- 5.3.1 Homecare Settings

- 5.3.2 Hospitals & Specialty Clinics

- 5.3.3 Others

- 5.4 By Distribution Channel

- 5.4.1 Hospital Pharmacies

- 5.4.2 Retail Pharmacies

- 5.4.3 E-commerce

- 5.5 By US Region

- 5.5.1 Northeast

- 5.5.2 Midwest

- 5.5.3 South

- 5.5.4 West

6 Market Indicators

- 6.1 Type-1 Diabetes Populaton

- 6.2 Type-2 Diabetes Populaton

7 Competitive Landscape

- 7.1 Market Concentration

- 7.2 Market Share Analysis

- 7.3 Company Profiles (includes Global-level Overview, Market-level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products & Services, and Recent Developments)

- 7.3.1 Abbott Laboratories

- 7.3.2 Medtronic plc

- 7.3.3 Dexcom Inc.

- 7.3.4 Insulet Corporation

- 7.3.5 F. Hoffmann-La Roche AG

- 7.3.6 Becton, Dickinson and Company

- 7.3.7 Tandem Diabetes Care Inc.

- 7.3.8 Novo Nordisk A/S

- 7.3.9 Eli Lilly and Company

- 7.3.10 Sanofi

- 7.3.11 Ypsomed Holding AG

- 7.3.12 Senseonics Holdings Inc.

- 7.3.13 Ascensia Diabetes Care

- 7.3.14 Glooko Inc.

- 7.3.15 AgaMatrix Inc.

- 7.3.16 Bigfoot Biomedical

- 7.3.17 Terumo Corporation

- 7.3.18 Owen Mumford Ltd.

8 Market Opportunities & Future Outlook

- 8.1 White-space & Unmet-Need Assessment