|

시장보고서

상품코드

1850140

무균 검사 : 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Sterility Testing - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

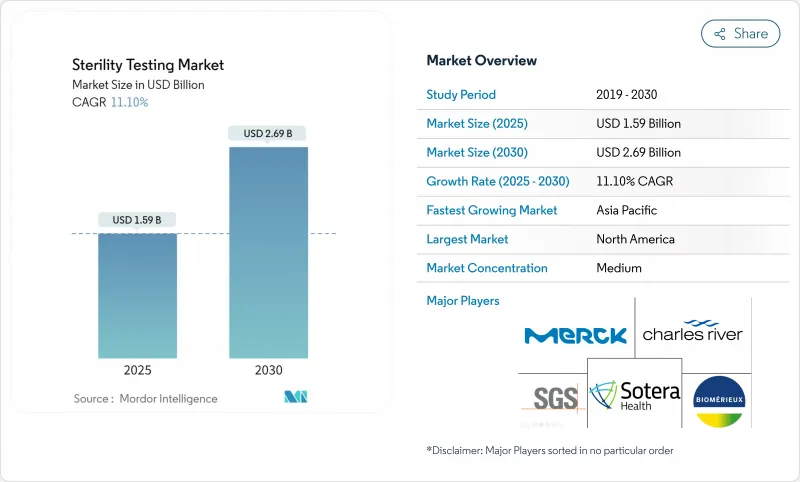

무균 검사 시장의 2025년 시장 규모는 15억 9,000만 달러로 평가되었고, 2030년에는 26억 9,000만 달러에 이를 것으로 예측되며, 이 기간의 CAGR은 11.1%를 나타낼 전망입니다.

이러한 추세는 EU GMP 부속서 1의 제로 CFU 요구사항, 복잡한 생물학적 제제 파이프라인의 상용화, 그리고 약물-환자 사이클을 단축하는 신속 출시 방법의 융합을 반영합니다. 세포 및 유전자 치료 분야로의 지속적인 벤처 캐피털 유입, 공공 부문의 백신 조달 증가, 무균 충전-완성 공정 능력의 계약 파트너로의 이전은 수요를 더욱 촉진합니다. 막 여과는 오랜 기간 확고한 입지를 유지하고 있으나, 신속 미생물 검출 플랫폼이 규제 당국의 선호를 얻으며 배치 처분을 주 단위가 아닌 시간 단위로 가능하게 하고 있습니다. 북미의 정교한 규제 생태계가 그 리더십을 뒷받침하는 반면, 아시아태평양 지역의 신흥 메가 플랜트, 우대 세제 제도, 조화된 약전 업데이트는 해당 지역을 가장 높은 지역 CAGR로 이끌고 있습니다.

세계의 무균 검사 시장 동향 및 인사이트

고급 생물학적 제제 파이프라인을 위한 엄격한 GMP 업그레이드

EU GMP 부속서 1 개정으로 지침이 16페이지에서 59페이지로 확대되었으며, A등급 환경에서의 제로 CFU 허용 기준이 공식화되면서 아이솔레이터, 생체 모니터링, 사용 전 멸균 후 무결성 시험(PUPSIT)에 대한 자본 지출이 급증했습니다. PUPSIT 프로토콜, 의무적 공기 흐름 다이어그램, 디지털 데이터 무결성 기록은 다중 사이트 네트워크를 운영하는 시판 허가 신청자에게 기본 요건이 되었습니다. EMA와 FDA 간 조화로 절차적 차이가 좁혀지면서 다국적 제조사들은 검증 마스터 플랜을 표준화하고 배치 출시 결정을 가속화할 수 있게 되었습니다.

신속 출시 무균 검사가 필요한 세포 및 유전자 치료제 상업 배치 급증

1,200건 이상의 미국 임상 연구와 자가 이식 승인 물결로 인해 생세포 효능 보호를 위한 4시간 내 무균 확인 요구가 더욱 강해지고 있습니다. 바이오메리외의 SCANRDI는 고체상 세포계측법을 활용해 단일 생존 가능한 비배양성 미생물을 검출하며, 결과 도출 시간을 14일에서 150분 미만으로 단축하면서도 USP <1223> 수용 기준을 충족합니다. 신속 방법을 인용한 FDA 생물학적 제제 허가 신청은 상업적 신뢰성을 검증하며, 소규모 후원사가 기존 프로토콜을 대체하도록 장려합니다.

클래스 B 아이솔레이터 인프라의 높은 자본 비용

자동 누출 테스트 모듈이 장착된 이중 챔버 아이솔레이터 구입 비용은 검증 및 연간 서비스 계약을 제외하고도 30만 달러 이상입니다. 사양 미달 중국 무균 실험실의 데이터 무결성 결함을 지적한 검사 결과는 투자 부족의 위험성을 부각시키며, 신생 기업조차도 불균형적인 자본 지출을 할당하도록 강요합니다.

부문 분석

서비스 부문은 10.8%의 연평균 복합 성장률(CAGR)을 보이며, 미생물학자 부족 속에서 정교한 분석을 아웃소싱하려는 업계의 열망을 반영합니다. 주요 CDMO 기업들이 무균 충전 라인 옆에 QC 시설을 구축함으로써 물류 체류 시간을 대폭 단축하는 “생산지에서의 테스트(test where you make)” 패러다임을 가능하게 함에 따라 무균 시험 시장이 혜택을 보고 있습니다. 매출 점유율 50.7%를 차지하는 키트 및 시약 부문은 중소 제조업체의 분산된 품질 관리 지점을 지원함으로써 여전히 탄력성을 유지하고 있습니다. 일회용 매니폴드, 색변화 배지, 즉시 사용 가능한 0.45μm 친수성 PVDF 멤브레인은 자동화가 확산되는 가운데서도 여전히 관련성을 유지하고 있습니다. 기기는 가장 낮은 매출 비중을 차지하지만 가장 높은 혁신 지수를 보입니다. Growth Direct 모듈은 이제 126개의 카세트를 동시에 배양하고 AI 이미지 분석을 통합하여 높은 신뢰도 기준에서 48시간 내에 공식적인 무균 판독값을 제공합니다.

한천 배지의 지속적인 상품화는 키트 마진을 압박하여 공급업체들이 클라우드 기반 분석 및 추적성 소프트웨어를 번들로 제공하도록 유도하고 있습니다. 서비스 업체들은 자문 전문성을 활용해 편차 조사, 오염원 추적, 사전 승인 검사를 위한 첫 시도부터 정확한 문서화를 제공합니다. 메릴랜드에 위치한 자빌의 36만 평방피트 규모 Pii 캠퍼스는 무균 충전-완성 공정과 현장 미생물학 실험실을 통합하여 샘플을 캠퍼스 내에 유지하고 관리 이력 위험을 줄이는 수평적 확장의 사례를 보여줍니다. 이와 병행하여 아일랜드, 싱가포르, 상파울루의 지역 실험실들은 팬데믹 대비 비축용 주사제 대상 가속 출시 시험을 처리하기 위해 24시간 교대 근무를 운영합니다. 의뢰사들이 '최후의 공급처'에서 '전략적 파트너십'으로 사고방식을 전환함에 따라 서비스 수익 흐름은 다년간의 가시성을 확보하며, 무균 시험 시장을 안정적인 연금형 수익원으로 강화합니다.

지역 분석

북미의 42.3% 매출 점유율은 생물학적 제제 허가 파이프라인의 밀집도, 적극적인 벤처 자금 지원, 신속한 방법의 조기 채택을 장려하는 FDA의 명확한 무균성 지침에서 비롯됩니다. STERIS는 2024년 매사추세츠와 캘리포니아에 두 개의 새로운 검증 실험실을 가동하여 당일 멤브레인 여과 설정을 제공함으로써 전국적 배송 지연을 단축했습니다. 이 지역은 북동부 회랑과 텍사스-노스캐롤라이나 생물학적 제제 벨트에 걸쳐 성숙한 CDMO 클러스터를 보유하고 있어 소모품 조달 및 방법 조화에 네트워크 효과를 창출합니다. 인력 부족은 지속되고 있으며, QC 분석가의 공석률이 15%를 초과하여 기업들이 지역 대학과 견습생 양성 경로를 마련하도록 촉구하고 있습니다.

아시아태평양 지역은 정책 인센티브, 대규모 백신 캠페인, 다중 입주형 바이오파크에 대한 사모펀드 투자에 힘입어 9.7%의 연평균 성장률(CAGR)을 기록하며 전 지역 중 가장 빠른 성장세를 보입니다. 중국의 최근 국내 시험 기준을 PIC/S와 일치시키라는 지침은 부속서 1 등급 아이솔레이터 수요를 가속화하고 있습니다. 일본의 의약품 및 의료기기청(PMDA)은 클라우드 기반 환경 모니터링을 활용한 원격 검사 시범 운영을 적극 추진하며 디지털 플랫폼 도입을 촉진하고 있습니다. 인도의 하이데라바드 게놈 밸리는 2026년까지 180만 평방피트의 무균 제조 공간을 추가로 확보하여 다운스트림 무균 시험 작업량을 확대할 예정입니다. 그러나 아세안 국가들 간 일관성 없는 규제 집행으로 인해 이중 시험 전략이 필요해지며, 서비스 수출업체의 마진 실현이 다소 저하되고 있습니다. 글로벌 스폰서들이 제품 출시 전 미국 또는 EU 실험실에서 핵심 검사를 재현하기로 선택함에 따라 무균 검사 시장이 혜택을 보고 있습니다.

유럽 시장은 2023년 8월 부속서 1(Annex 1)의 완전 시행으로 안정적인 전망을 유지합니다. 독일, 영국, 프랑스가 아이솔레이터 개조 시장을 주도하며, 소규모 생물학적 제제 공장이 완전 통합형 HEPA 필터 배리어 시스템으로 업그레이드 중입니다. EU의 ‘Fit-for-55’ 탄소 감축 목표는 공급업체들이 저에너지 증발형 과산화수소 사이클을 개발하도록 촉진하며, 이는 신흥 구매 기준으로 부상 중입니다. 벨기에, 덴마크 등 소규모 유럽 경제권은 국가 생명과학 클러스터를 활용해 CDMO 확장을 유치하며 스칸디나비아 및 베네룩스 시장 대상 지역 서비스 역량을 강화하고 있습니다. 한편 중동부 유럽은 비용 효율적인 노동력을 내세우지만, 느린 규제 처리 속도가 신속 검사 도입을 저해하고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월의 애널리스트 지원

목차

제1장 서론

- 조사의 전제조건과 시장의 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 고급 생물학적 제제 파이프라인을 위한 엄격한 GMP 업그레이드

- 신속 멸균 시험이 필요한 세포 및 유전자 치료 상업용 배치 급증

- 사내 QC에서 아웃소싱 CDMO 무균 서비스로의 전환

- 오양성률 감소 위한 모듈식 아이솔레이터 시스템 도입

- 검증된 신속 미생물학적 방법에 대한 규제적 추진

- 일회용 기술 호환 테스트 키트 수요 증가

- 시장 성장 억제요인

- 클래스 B 아이솔레이터 인프라의 높은 자본 비용

- 공정 시험 기준의 국제적 조화의 한계

- 신흥 시장의 숙련된 미생물학자 급격한 부족

- 직접 접종 검사의 오양성 위험으로 인한 출시 지연

- 공급망 분석

- 규제 상황

- 기술의 전망

- Porter's Five Forces 분석

- 신규 참가업체의 위협

- 구매자의 협상력

- 공급기업의 협상력

- 대체품의 위협

- 경쟁 기업간 경쟁 관계

제5장 시장 규모와 성장 예측

- 제품 유형별

- 기기

- 키트 및 시약

- 서비스

- 검사 유형별

- 막 여과

- 직접 접종

- 신속 무균 검사

- 용도별

- 의약품 및 바이오의약품 제조

- 의료기기 제조

- 기타

- 모드별

- 사내 검사

- 아웃소싱/위탁검사

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 기타 유럽

- 아시아태평양

- 중국

- 일본

- 인도

- 한국

- 호주

- 기타 아시아태평양

- 중동 및 아프리카

- GCC

- 남아프리카

- 기타 중동 및 아프리카

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 북미

제6장 경쟁 구도

- 시장 집중도

- 시장 점유율 분석

- 기업 프로파일

- bioMerieux SA

- Charles River Laboratories

- Merck KGaA

- Sartorius AG

- SGS SA

- Sotera Health(Nelson Laboratories)

- STERIS Plc

- Thermo Fisher Scientific

- Laboratory Corporation of America Holdings

- WuXi AppTec

- Rapid Micro Biosystems Inc.

- Pace Analytical

- Eurofins Scientific

- Pacific BioLabs

- Lonza Group

- Boston Analytical

- Bio-Outsource(SGS)

- Toxikon Europe

제7장 시장 기회와 장래의 전망

HBR 25.11.19The sterility testing market is valued at USD 1.59 billion in 2025 and is forecast to attain USD 2.69 billion by 2030, reflecting an 11.1% CAGR over the period.

This trajectory mirrors the convergence of EU GMP Annex 1's zero-CFU requirement, the commercialization of complex biologics pipelines, and rapid-release methods that compress drug-to-patient cycles. Persistent venture capital inflows into cell and gene therapy, mounting public-sector vaccine procurement, and the migration of sterile fill-finish capacity to contract partners further energize demand. Membrane filtration maintains its long-established foothold, yet rapid microbial detection platforms are gaining regulatory favor, enabling batch disposition in hours rather than weeks. North America's sophisticated regulatory ecosystem underpins its leadership, while Asia Pacific's emerging mega-plants, preferential tax regimes, and harmonized pharmacopeial updates push it toward the highest regional CAGR.

Global Sterility Testing Market Trends and Insights

Stringent GMP Upgrades For Advanced Biologics Pipelines

The revision of EU GMP Annex 1 lengthened guidance from 16 to 59 pages and formalized the zero-CFU tolerance in Grade A environments, prompting a surge in capital expenditures on isolators, viable monitoring, and pre-use post-sterilization integrity testing. PUPSIT protocols, mandatory airflow diagrams, and digital data-integrity logs have become baseline requirements for marketing-authorization sponsors operating multi-site networks. Harmonization between the EMA and FDA narrows procedural divergence, letting multi-country manufacturers standardize validation master plans and accelerate lot-release decisions.

Surge In Cell & Gene-Therapy Commercial Batches Needing Rapid-Release Sterility Tests

More than 1,200 active US clinical studies and a wave of autologous approvals intensify the call for sterility confirmation within a 4-hour window to safeguard living-cell potency. bioMerieux's SCANRDI exploits solid-phase cytometry to detect single viable but non-culturable organisms, cutting time-to-result from 14 days to under 150 minutes while meeting USP <1223> acceptance criteria. FDA biologics license applications referencing rapid methods validate their commercial reliability and embolden smaller sponsors to replace legacy protocols.

High Capital Cost of Class B Isolator Infrastructure

Acquiring a dual-chamber isolator with automatic leak-test modules costs upward of USD 300,000, excluding validation and annual service contracts. Inspections citing data-integrity lapses at under-spec Chinese sterility labs underscore the risk of under-investment and force even start-ups to allocate disproportionate capex.

Other drivers and restraints analyzed in the detailed report include:

- Shift From In-House QC To Outsourced CDMO Sterility Services

- Adoption Of Modular Isolator Systems That Curb False Positives

- Limited Global Harmonization of Compendial Standards

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Services exhibit a 10.8% CAGR, reflecting industry eagerness to outsource sophisticated assays amid microbiologist scarcity. The sterility testing market benefits as leading CDMOs embed QC suites next to aseptic filling lines, enabling "test where you make" paradigms that slash logistic dwell. Kits and reagents, holding 50.7% revenue share, remain resilient by servicing decentralized quality-control points at small and midsize manufacturers. Single-use manifolds, color-change growth media, and off-the-shelf 0.45 µm hydrophilic PVDF membranes preserve relevance even as automation spreads. Instruments form the leanest revenue slice yet the highest innovation quotient. Growth Direct modules now incubate 126 cassettes simultaneously and integrate AI image analytics, delivering official sterility reads in 48 hours at high confidence thresholds.

Continued commoditization of agar plates pressures kit margins, motivating suppliers to bundle cloud-based analytics and traceability software. Services vendors capitalize on their consultative expertise, providing deviation investigations, contamination-source mapping, and right-first-time documentation for pre-approval inspections. Jabil's 360,000-sq-ft Pii campus in Maryland integrates sterile fill-finish with on-site microbiology labs, illustrating horizontal expansion that keeps samples on campus and reduces chain-of-custody risk. In parallel, regional labs in Ireland, Singapore, and Sao Paulo run 24-hour shifts to absorb accelerated release testing for parenterals destined for pandemic-preparedness stockpiles. As sponsors pivot from supplier-of-last-resort to strategic partnership mentality, service revenue streams gain multi-year visibility-bolstering the sterility testing market as a dependable annuity.

The Sterility Testing Market is Segmented by Product Type (Instruments, Kits & Reagents, and More), Test Type (Membrane Filtration, Direct Inoculation, and More), Application (Pharmaceutical & Biologics Manufacturing, and More), Mode (In-House Testing and Outsourced/Contract Testing), and Geography (North America, Europe, Asia-Pacific, and More). The Market Sizes and Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America's 42.3% revenue share stems from its dense biologics licensure pipeline, aggressive venture funding, and the FDA's well-articulated sterility guidelines that incentivize early adoption of rapid methods. STERIS commissioned two new validation labs in Massachusetts and California during 2024 which provide same-day membrane filtration setup, shortening cross-country shipment lags. The region houses a mature CDMO cluster across the North-East corridor and the Texas-North Carolina biologics belt, generating network effects in consumables procurement and method harmonization. Workforce gaps persist; vacancy rates surpass 15% among QC analysts, pushing firms to create apprenticeship pathways with local colleges.

Asia Pacific exhibits a 9.7% CAGR, the fastest among all regions, driven by policy incentives, scaled vaccine campaigns, and private equity funding for multi-tenant bioparks. China's recent mandate aligning domestic test standards with PIC/S intensifies demand for Annex 1-grade isolators. Japan's Pharmaceuticals and Medical Devices Agency (PMDA) actively pilots remote inspections aided by cloud-based environmental monitoring, spurring adoption of digital platforms. India's Hyderabad Genome Valley adds 1.8 million sq ft of sterile manufacturing space by 2026, widening downstream sterility testing workloads. However, inconsistent enforcement across ASEAN nations necessitates dual testing strategies, mildly eroding margin realization for service exporters. The sterility testing market benefits as global sponsors opt to replicate critical tests in US or EU labs before product launch.

Europe's outlook remains steady, buoyed by Annex 1's full enforcement in August 2023. Germany, the UK, and France lead in isolator retrofits, with small-batch biologics plants upgrading to fully integrated HEPA-filtered barrier systems. The EU's Fit-for-55 carbon targets spur suppliers to engineer low-energy vaporized hydrogen peroxide cycles, an emerging purchasing criterion. Smaller European economies such as Belgium and Denmark leverage national life-science clusters to court CDMO expansions, adding regional service capacity for Scandinavian and Benelux markets. Meanwhile, Central and Eastern Europe pitch cost-efficient labor pools, though slower regulatory turnaround times temper rapid testing adoption.

- bioMerieux

- Charles River

- Merck

- Sartorius

- SGS

- Sotera Health (Nelson Laboratories)

- STERIS Plc

- Thermo Fisher Scientific

- LabCorp

- WuXi App Tec

- Rapid Micro Biosystems

- Pace Analytical Services

- Eurofins

- Pacific BioLabs

- Lonza Group

- Boston Analytical

- Bio-Outsource (SGS)

- Toxikon Europe

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Stringent GMP Upgrades For Advanced Biologics Pipelines

- 4.2.2 Surge In Cell & Gene-Therapy Commercial Batches Needing Rapid-Release Sterility Tests

- 4.2.3 Shift From In-House QC To Outsourced CDMO Sterility Services

- 4.2.4 Adoption Of Modular Isolator Systems Cutting False-Positive Rates

- 4.2.5 Regulatory Push For Validated Rapid Microbiological Methods

- 4.2.6 Rising Demand For Single-Use Technology Compatible Test Kits

- 4.3 Market Restraints

- 4.3.1 High Capital Cost Of Class B Isolator Infrastructure

- 4.3.2 Limited Global Harmonization Of Compendial Test Standards

- 4.3.3 Acute Shortage Of Skilled Microbiologists In Emerging Markets

- 4.3.4 False-Positive Risk In Direct-Inoculation Tests Delaying Releases

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value)

- 5.1 By Product Type

- 5.1.1 Instruments

- 5.1.2 Kits & Reagents

- 5.1.3 Services

- 5.2 By Test Type

- 5.2.1 Membrane Filtration

- 5.2.2 Direct Inoculation

- 5.2.3 Rapid Sterility Tests

- 5.3 By Application

- 5.3.1 Pharmaceutical & Biologics Manufacturing

- 5.3.2 Medical Device Manufacturing

- 5.3.3 Others

- 5.4 By Mode

- 5.4.1 In-house Testing

- 5.4.2 Outsourced/Contract Testing

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 South Korea

- 5.5.3.5 Australia

- 5.5.3.6 Rest of Asia Pacific

- 5.5.4 Middle East and Africa

- 5.5.4.1 GCC

- 5.5.4.2 South Africa

- 5.5.4.3 Rest of Middle East and Africa

- 5.5.5 South America

- 5.5.5.1 Brazil

- 5.5.5.2 Argentina

- 5.5.5.3 Rest of South America

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.3.1 bioMerieux SA

- 6.3.2 Charles River Laboratories

- 6.3.3 Merck KGaA

- 6.3.4 Sartorius AG

- 6.3.5 SGS SA

- 6.3.6 Sotera Health (Nelson Laboratories)

- 6.3.7 STERIS Plc

- 6.3.8 Thermo Fisher Scientific

- 6.3.9 Laboratory Corporation of America Holdings

- 6.3.10 WuXi AppTec

- 6.3.11 Rapid Micro Biosystems Inc.

- 6.3.12 Pace Analytical

- 6.3.13 Eurofins Scientific

- 6.3.14 Pacific BioLabs

- 6.3.15 Lonza Group

- 6.3.16 Boston Analytical

- 6.3.17 Bio-Outsource (SGS)

- 6.3.18 Toxikon Europe

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment