|

시장보고서

상품코드

1850148

약물감시 및 의약품 안전성 소프트웨어 시장 : 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Pharmacovigilance And Drug Safety Software - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

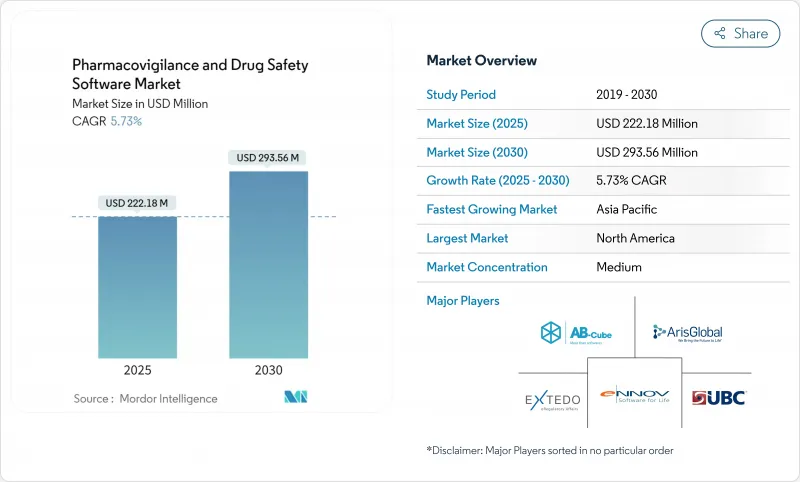

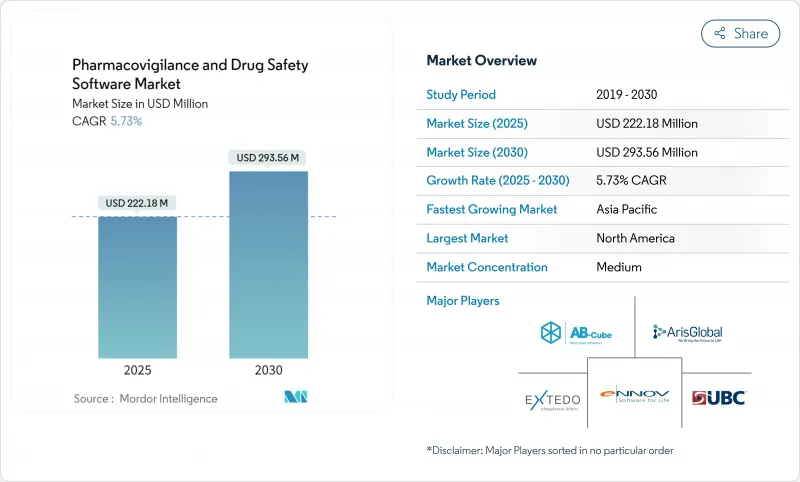

약물감시 및 의약품 안전성 소프트웨어 시장은 2025년에 2억 2,218만 달러, 2030년에는 2억 9,356만 달러에 이르고, CAGR은 5.73%를 나타낼 전망입니다.

성장의 축은 기본적인 컴플라이언스 시스템에서 스폰서가 실제 세계의 증거를 거의 실시간으로 평가할 수 있도록 지원하는 AI 지원 안전 인텔리전스 플랫폼으로의 전환입니다. FDA의 E2B(R3) 지침과 유럽 의료 데이터 공간 규제를 필두로 세계적인 보고 규칙의 조화가 진행되고, 규제의 기한이 비재량적인 IT 지출로 변환됩니다. 생명과학 기업에서 클라우드의 보급률은 80%를 넘어 최신 안전성 데이터베이스의 바람직한 배포 기반을 구축하고 있습니다. 한편, 사례의 트리아지를 자동화하는 설명 가능한 AI 모듈은 처리 비용을 50%나 줄여 조기 도입 기업에 경제적 우위를 가져옵니다. 아시아태평양의 지정학적 안정은 합리화된 윤리승인과 함께 임상시험 점유율을 동쪽으로 옮겨 가면서 고급 감시도구에 대한 지역 수요를 높이고 있습니다.

세계의 파마코비질런스 및 의약품 안전 소프트웨어 시장 동향과 통찰

부작용(ADR) 발생률 증가

새로운 분자 화합물이 널리 사용됨에 따라 ADR의 확산이 가속화되고 첨단 모니터링에 대한 수요가 재구성되고 있습니다. Cureus Journal의 데이터에 따르면, 21-40세 연령층이 가장 높은 빈도로 ADR을 보고하고 있으며, 이는 다양성 증가와 병원과의 상호작용 증가를 반영합니다. FDA는 2024년에 50개의 신규 분자 화합물을 승인하기 때문에 스폰서는 다양한 환자 하위 집단에 대해 이전에 발견되지 않은 안전 신호를 조사해야 합니다. 생물학적 제제와 유전자 치료는 유전적 배경에 따라 반응이 다를 수 있으므로 복잡성이 증가하고 있습니다. 따라서 Pharmacobillances 소프트웨어 시장은 정적 보고서 저장소에서 이기종 종단 데이터 세트를 분석 할 수있는 실제 세계의 증거 엔진으로 이동하고 있습니다. 수작업으로는 양과 복잡성에 대응할 수 없기 때문에 AI를 활용한 패턴 인식을 보고 워크플로우에 통합하는 벤더가 중요성을 늘리고 있습니다.

엄격한 세계 E2B(R3)/IDMP 규정 준수 기한

2026년 4월, FDA는 E2B(R3) 신청 마감일을 맞이하고, 스폰서는 기존의 R2 형식을 포기하고 업그레이드된 플랫폼에 대한 투자를 강요합니다. 동시에, 유럽 의약품청(EEA)의 IDMP(European Medicines Agency: European Medicines Agency) 배포는 의약품 데이터 요구사항을 강화하고 하나의 스키마에서 이벤트와 제품 식별자를 모두 관리해야 합니다. 이중 시스템 유지 보수는 위험과 오버 헤드를 증가시키기 때문에 기업은 법령에 앞서 전환을 가속화합니다. 이러한 규제의 동기성으로 인해 컴플라이언스 업그레이드에 대한 지출은 재량적 예산 항목이 아니라 확실하게 되어 약물감시 소프트웨어 시장 예측 가능한 성장을 뒷받침하고 있습니다.

데이터 주권과 국경을 넘어서는 이전 제한

2025년 5월에 발효된 유럽 의료 데이터 공간 규칙은 의료 데이터의 2차 이용에 새로운 기준을 설정하고 소프트웨어가 존중해야 하는 동의층을 도입합니다. GDPR(EU 개인정보보호규정)은 이미 외부 처리를 제한하고 있으며, 아시아와 라틴아메리카에서도 비슷한 틀이 탄생하고 있습니다. 따라서 벤더는 데이터를 국내에 유지하면서 비식별화된 신호를 세계하게 공유하는 연계 모델을 설계해야 합니다. 이 아키텍처는 비용을 증가시키고 배포주기를 장기화하기 때문에 파마 코비지 런스 소프트웨어 시장의 확대 부분을 방해합니다.

부문 분석

부작용 보고 소프트웨어는 2024년 약물감시 소프트웨어 시장에서 40.7%라는 압도적인 점유율을 유지해 양보할 수 없는 컴플라이언스의 기둥으로서의 지위를 강조하고 있습니다. 그러나 신호 검출 및 리스크 관리 모듈은 CAGR 18.4%를 보일 것으로 예측되며, 규제 당국이 개입하기 전에 이상을 알리는 예방적 분석으로 전환하는 추세를 보여줍니다. 현재 많은 스폰서들은 흡입, 트리아지, 애널리틱스 및 제출을 하나의 워크플로우로 통합하는 통합 플랫폼을 선호합니다. Oracle은 2024년 Argus에 AI를 탑재한 조건부 터치리스 프로세싱을 추가하여 임베디드 인텔리전스가 레거시 솔루션을 개선하는 방법을 보여줍니다. 생물학적 승인의 지속적인 증가는 다양한 실세계 데이터 피드와 결합하여 민족적, 유전체적 및 건강의 사회적 결정 요인의 데이터 세트 간의 상관관계를 이끌어내는 플랫폼 기회를 넓히고 있습니다.

통합 제품군은 또한 단일 품질 관리 시스템이 여러 모듈을 커버하므로 검증 오버헤드를 줄여줍니다. 결과적으로 포인트 솔루션을 엔드 투 엔드 아키텍처에 조화시킬 수 있는 공급업체는 틈새 경쟁사보다 빠르게 설치 기반을 확장하고 있습니다. 신호 검출 유닛은 결국 이벤트 보고 매출을 초과할 수 있지만, 규제 당국에 제출하는 것은 여전히 소스가 되는 사례 데이터에서 파생되기 때문에 두 모듈은 여전히 공생하고 있습니다. 따라서 고급 분석으로 인한 파마코비질런스 소프트웨어 시장 규모는 보고가 기본적인 관련성을 유지하더라도 전체 시장보다 빠르게 확대될 것으로 예측됩니다.

지역 분석

북미가 2024년 수익 점유율 35.9%로 선두를 차지해 FDA의 엄격한 감독과 상위 20개 제약기업의 밀집이 그 요인이 되고 있습니다. 화이자 이용 사례는 자동 방어 및 중복 제거를 통해 150만 건 이상의 COVID-19 백신 사례를 처리했습니다. FDA가 2025년에 AI 최고 책임자를 설치한 것은 규제 당국이 알고리즘에 의한 신청을 평가할 준비가 있음을 강조하는 것으로, AI를 다용한 업그레이드에 대한 지역의 의욕을 강화하고 있습니다. 인력 부족은 여전히 장애물이며 데이터 사이언스 전문가의 급여는 급등하고 중소기업은 아웃소싱을 당하고 있습니다.

아시아태평양은 한국, 대만, 싱가포르로의 임상시험 이행을 배경으로 CAGR로 가장 빠른 14.3%를 기록했습니다. 무석 AppTec을 필두로 확대하는 중국의 의약품 개발 업무 수탁은 국가 의약품 관리국(National Medical Products Administration)의 규칙에 따른 PV 능력을 필요로 하는 세계 클라이언트를 끌고 있습니다. 일본의 AI 의약품 안전 연구 보조금(AMED)과 같은 정부 투자 프로그램은 국내 소프트웨어 채택을 더욱 자극하고 있습니다. 다양한 법적 틀이 있음에도 불구하고, 아시아태평양의 규제 당국 중 상당수는 현재 ICH E2B(R3) XML을 받아들여 현지화 장벽을 줄이고 있습니다.

유럽에서는 약물감시 의무와 GDPR(EU 개인정보보호규정)이 성숙하고, 구성 가능하고 감사 대응 가능한 플랫폼의 필요성이 높아지고 있기 때문에 큰 규모를 유지하고 있습니다. 유럽 건강 데이터 공간 규제는 건강 데이터의 2차 이용을 공식화하고, 스폰서에 보다 세밀한 동의 관리가 가능한 소프트웨어의 채택을 촉구하고 있습니다. 독일의 새로운 Digital Act는 조사를 위해 비식별화된 청구 데이터세트를 개방하여 안전 알고리즘이 이전에 출입 금지였던 국가 저장소를 마이닝할 수 있도록 합니다. 그러나 엄격한 데이터 주권 조항은 EU 기반 호스팅을 요구하며 지역별 클라우드 존 수요에 박차를 가하고 있습니다. 이러한 역학을 종합하면 아시아태평양보다 성장이 늦어지고 있다고는 해도 유럽은 기능이 풍부한 플랫폼의 프리미엄 시장으로 변함이 없습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 서포트

목차

제1장 서론

- 조사의 전제조건과 시장의 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 약물 유해 반응(ADR)의 발생률 상승

- 엄격한 세계 E2B(R3)/IDMP 컴플라이언스 기한

- 안전 데이터베이스의 클라우드 퍼스트 마이그레이션

- 개요 가능한 AI 모듈이 케이스 처리 비용을 대폭 절감

- 조기 시그널을 위한 리얼 월드 증거(RWE) 통합

- 신흥 시장용 폼의 로우 코드 현지화

- 시장 성장 억제요인

- 데이터 주권과 국경을 넘은 이전의 제한

- PV 데이터 사이언스 인력 부족

- AI 승인을 지연시키는 알고리즘 편향성 조사

- 주요 DB 벤더에 의한 API 가격의 상승

- 공급망 분석

- 규제 상황

- 기술의 전망

- Porter's Five Forces 분석

- 신규 참가업체의 위협

- 구매자의 협상력

- 공급기업의 협상력

- 대체품의 위협

- 라이벌 관계의 격렬

제5장 시장 규모와 성장 예측

- 기능성별

- 부작용 보고 소프트웨어

- 의약품 안전성 감사 소프트웨어

- 문제 추적 소프트웨어

- 완전히 통합된 안전 스위트

- 신호 검출 및 리스크 관리 툴

- 배송 방법별

- On-Premise

- 클라우드/SaaS

- 하이브리드 전개

- 최종 사용자별

- 제약 및 바이오테크놀러지 기업

- 계약연구기관(CRO)

- 비즈니스 프로세스 아웃소싱(BPO) 기업

- 의료기기 제조업체

- 기타 PV 서비스 제공업체

- 지역

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 기타 유럽

- 아시아태평양

- 중국

- 일본

- 인도

- 한국

- 호주

- 기타 아시아태평양

- 중동 및 아프리카

- GCC

- 남아프리카

- 기타 중동 및 아프리카

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 북미

제6장 경쟁 구도

- 시장 집중도

- 시장 점유율 분석

- 기업 프로파일

- Oracle Corporation

- ArisGlobal

- Veeva Systems

- Sparta Systems

- IQVIA

- Ennov Solutions

- Extedo GmbH

- AB Cube

- Anju Software

- Sarjen Systems

- United BioSource Corp.

- Accenture

- Cognizant

- Tata Consultancy Services(TCS ADD)

- Parexel International

- Medidata Solutions

- Saama Technologies

- Intellimed(Vigilance 360)

제7장 시장 기회와 장래의 전망

SHW 25.11.07The pharmacovigilance software market is valued at USD 222.18 million in 2025 and is forecast to reach USD 293.56 million by 2030, advancing at a steady 5.73% CAGR.

Growth pivots on the transition from basic compliance systems to AI-enabled safety intelligence platforms that help sponsors evaluate real-world evidence in near-real time. Intensifying harmonization of global reporting rules, spearheaded by the FDA's E2B(R3) mandate and the European Health Data Space Regulation, converts regulatory deadlines into non-discretionary IT spending.Cloud adoption crosses 80% penetration among life-science firms, creating a preferred deployment backbone for modern safety databases. Meanwhile, explainable-AI modules that automate case triage lower processing costs by as much as 50%, giving early adopters an economic edge. Geopolitical stability in Asia Pacific, coupled with streamlined ethics approvals, is relocating a rising share of clinical trials eastward and lifting regional demand for advanced surveillance tools.

Global Pharmacovigilance And Drug Safety Software Market Trends and Insights

Rising Incidence of Adverse Drug Reactions (ADRs)

Escalating ADR prevalence reshapes demand for advanced monitoring as new molecular entities enter wider use. Cureus Journal data show the 21-40 age group now reports the highest ADR frequencies, reflecting greater polypharmacy and increased hospital interactions. With the FDA approving 50 new molecular entities in 2024, sponsors must surveil diverse patient sub-populations for previously unseen safety signals. Biologics and gene therapies add complexity because reactions can vary across genetic backgrounds. Accordingly, the pharmacovigilance software market shifts from static report repositories toward real-world evidence engines capable of analyzing heterogeneous longitudinal datasets. Vendors that embed AI-powered pattern recognition into reporting workflows gain relevance because manual methods cannot keep pace with volume and complexity.

Stringent Global E2B(R3)/IDMP Compliance Deadlines

April 2026 marks the FDA's cut-off for E2B(R3) submissions, forcing sponsors to abandon legacy R2 formats and invest in upgraded platforms. Simultaneously, the European Medicines Agency's IDMP roll-out tightens medicinal-product data requirements, compelling software to manage both event and product identifiers in one schema. Dual-system maintenance inflates risk and overhead, so firms accelerate migration ahead of statute. This regulatory synchrony turns spending on compliance upgrades into a certainty rather than a discretionary budget item, underpinning predictable growth for the pharmacovigilance software market.

Data-Sovereignty & Cross-Border-Transfer Restrictions

The European Health Data Space Regulation, effective May 2025, sets new standards for secondary health-data use and introduces consent layers that software must honor. GDPR already limits external processing, and similar frameworks are emerging in Asia and Latin America. Vendors must therefore design federated models that keep data in the country while sharing de-identified signals globally. This architecture raises costs and elongates deployment cycles, damping part of the pharmacovigilance software market's expansion.

Other drivers and restraints analyzed in the detailed report include:

- Cloud-First Migration of Safety Databases

- Explainable-AI Modules Slash Case-Processing Costs

- Shortage of PV Data-Science Talent

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Adverse events reporting software retained a commanding 40.7% share of the pharmacovigilance software market in 2024, underscoring its status as a non-negotiable compliance pillar. Yet signal detection and risk-management modules are forecast to grow at an 18.4% CAGR, demonstrating the pivot toward preventive analytics that flag anomalies before regulators intervene. Many sponsors now favor unified platforms that merge intake, triage, analytics, and submission into one workflow. Oracle added AI-powered conditional touchless processing to Argus in 2024, illustrating how embedded intelligence elevates legacy solutions. Continuous rise in biological approvals coupled with diverse real-world data feeds widens the opportunity for platforms that draw correlations across ethnic, genomic, and social determinants of health datasets.

Integrated suites also reduce validation overhead because a single quality-management system covers multiple modules. As a result, vendors capable of harmonizing point solutions into end-to-end architecture are expanding their installed bases faster than niche competitors. Signal detection units may ultimately outpace event-reporting revenue, yet both modules remain symbiotic because regulatory filings still stem from source case data. The pharmacovigilance software market size attributable to advanced analytics is therefore set to climb more rapidly than the aggregate market, even as reporting retains foundational relevance.

The Pharmacovigilance and Drug Safety Software Market is Segmented by Functionality (Adverse Event Reporting, Drug Safety Audit Software, and More), Mode of Delivery (On-Premise, Cloud/SaaS, and More), End User (Pharmaceutical & Biotechnology Companies, Contract Research Organizations, and More), and Geography (North America, Europe, Asia-Pacific, and More). The Market Sizes and Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America led with 35.9% revenue share in 2024, anchored by stringent FDA oversight and a dense concentration of top 20 pharmaceutical companies. Many regional sponsors pioneered cloud-based safety systems before 2020; Pfizer's COVAES platform processed more than 1.5 million COVID-19 vaccine cases using automated triage and de-duplication. The FDA's 2025 creation of a chief AI officer underscores the regulator's readiness to evaluate algorithmic submissions, reinforcing regional appetite for AI-rich upgrades. Talent shortages remain a hurdle, inflating salaries for data-science specialists and pressuring smaller firms to outsource.

Asia Pacific records the fastest 14.3% CAGR on the back of clinical-trial migration to South Korea, Taiwan and Singapore, where shorter ethics-committee timelines accelerate recruitment. China's expanding contract research landscape, led by Wuxi AppTec, pulls in global clients that need local PV capacity aligned with National Medical Products Administration rules. Government investment programs, such as Japan's AMED grants for AI drug-safety research, further stimulate domestic software adoption. Despite diverse legal frameworks, many Asia-Pacific regulators now accept ICH E2B(R3) XML, reducing localization barriers.

Europe maintains significant scale because mature pharmacovigilance obligations and GDPR heightens the need for configurable, audit-ready platforms. The European Health Data Space Regulation formalizes secondary health-data use, prompting sponsors to adopt software capable of granular consent management. Germany's new Digital Act unlocks de-identified claims datasets for research, enabling safety algorithms to mine national repositories once off-limits. However, strict data-sovereignty clauses require EU-based hosting, spurring demand for region-specific cloud zones. Collectively, these dynamics keep Europe a premium market for feature-rich platforms even though growth trails Asia Pacific.

- Oracle

- Aris Global

- Veeva Systems

- Sparta Systems

- IQVIA

- Ennov Solutions

- Extedo

- AB Cube

- Anju Software

- Sarjen Systems

- United BioSource Corp.

- Accenture

- Cognizant

- Tata Consultancy Services (TCS ADD)

- Parexel International

- Medidata Solutions

- Saama Technologies

- Intellimed (Vigilance 360)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Incidence Of Adverse Drug Reactions (ADRs)

- 4.2.2 Stringent Global E2B(R3)/IDMP Compliance Deadlines

- 4.2.3 Cloud-First Migration Of Safety Databases

- 4.2.4 Explainable-AI Modules Slash Case-Processing Costs

- 4.2.5 Real-World-Evidence (RWE) Integration For Early Signals

- 4.2.6 Low-Code Localisation For Emerging-Market Forms

- 4.3 Market Restraints

- 4.3.1 Data-Sovereignty & Cross-Border-Transfer Restrictions

- 4.3.2 Shortage Of PV Data-Science Talent

- 4.3.3 Algorithmic-Bias Scrutiny Delaying AI Approvals

- 4.3.4 Escalating API Pricing From Dominant DB Vendors

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Rivalry

5 Market Size & Growth Forecasts (Value)

- 5.1 By Functionality

- 5.1.1 Adverse Event Reporting Software

- 5.1.2 Drug Safety Audit Software

- 5.1.3 Issue Tracking Software

- 5.1.4 Fully Integrated Safety Suites

- 5.1.5 Signal Detection & Risk-Management Tools

- 5.2 By Mode of Delivery

- 5.2.1 On-premise

- 5.2.2 Cloud / SaaS

- 5.2.3 Hybrid Deployment

- 5.3 By End User

- 5.3.1 Pharmaceutical & Biotechnology Companies

- 5.3.2 Contract Research Organizations (CROs)

- 5.3.3 Business-Process-Outsourcing (BPO) Firms

- 5.3.4 Medical-Device Manufacturers

- 5.3.5 Other PV Service Providers

- 5.4 Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 Europe

- 5.4.2.1 Germany

- 5.4.2.2 United Kingdom

- 5.4.2.3 France

- 5.4.2.4 Italy

- 5.4.2.5 Spain

- 5.4.2.6 Rest of Europe

- 5.4.3 Asia Pacific

- 5.4.3.1 China

- 5.4.3.2 Japan

- 5.4.3.3 India

- 5.4.3.4 South Korea

- 5.4.3.5 Australia

- 5.4.3.6 Rest of Asia Pacific

- 5.4.4 Middle East and Africa

- 5.4.4.1 GCC

- 5.4.4.2 South Africa

- 5.4.4.3 Rest of Middle East and Africa

- 5.4.5 South America

- 5.4.5.1 Brazil

- 5.4.5.2 Argentina

- 5.4.5.3 Rest of South America

- 5.4.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.3.1 Oracle Corporation

- 6.3.2 ArisGlobal

- 6.3.3 Veeva Systems

- 6.3.4 Sparta Systems

- 6.3.5 IQVIA

- 6.3.6 Ennov Solutions

- 6.3.7 Extedo GmbH

- 6.3.8 AB Cube

- 6.3.9 Anju Software

- 6.3.10 Sarjen Systems

- 6.3.11 United BioSource Corp.

- 6.3.12 Accenture

- 6.3.13 Cognizant

- 6.3.14 Tata Consultancy Services (TCS ADD)

- 6.3.15 Parexel International

- 6.3.16 Medidata Solutions

- 6.3.17 Saama Technologies

- 6.3.18 Intellimed (Vigilance 360)

7 Market Opportunities & Future Outlook

- 7.1 White-Space & Unmet-Need Assessment