|

시장보고서

상품코드

1850151

소형 UAV : 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Small UAV - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

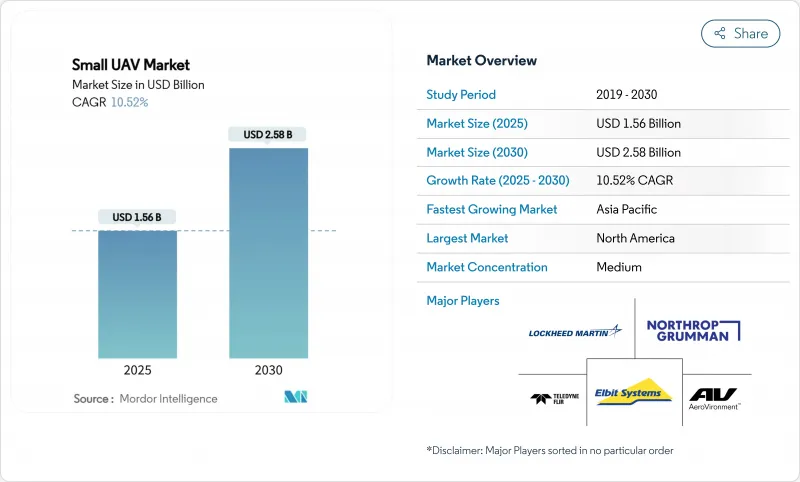

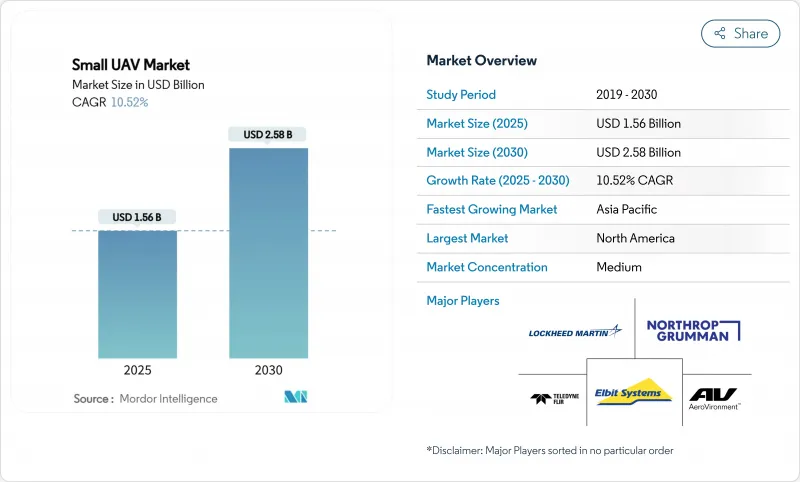

소형 UAV 시장 규모는 2025년에 15억 6,000만 달러로 평가되었고, 2030년에 25억 8,000만 달러에 이를 것으로 예측되며, CAGR은 10.59%를 나타낼 전망입니다.

북미의 방위 조달 프로그램과 국내 드론 우위 확보를 위한 행정 명령이 초기 수요를 주도했으며, 아시아태평양 지역의 현대화 계획은 도입 속도를 지속적으로 가속화했습니다. 군집 자율성, 하이브리드 기체 설계, 수소 연료전지 추진 기술은 차별화의 새로운 길을 열었으나, 대 UVA(C-UAS) 지출이 전술적 이점을 약화시킬 위험이 존재했습니다. 반도체와 리튬이온 전지는 여전히 공급망 병목 지점으로 남아 구매자들이 국내 조달이 보장된 공급업체를 선호하도록 했습니다. 경쟁사들은 소형 UVA 시장 점유율 확보를 위해 수직 통합, 소프트웨어 중심 아키텍처, 수출 규격 준수 설계에 집중하고 있습니다.

세계의 소형 UAV 시장 동향 및 인사이트

경쟁 환경에서의 실시간 ISR 수요

지속적 감시는 완전한 공중 우위 없이 작전하는 지휘관에게 필수적이었습니다. 소형 UVA는 레이더 탐지 범위 아래에서 비행하며 전술용 태블릿으로 직접 영상을 전송했는데, 미군의 소형 정찰 시스템에 5억 달러를 투자한 사례가 대표적입니다. 우크라이나군은 수백만 대의 드론을 투입해 전장 인식 능력을 확보함으로써 양보다 질을 중시하는 전술의 유효성을 입증했습니다. 이후 독일산 HF-1 공격용 UVA는 AI 지형 매핑 기능을 추가해 GNSS 교란을 회피함으로써 GPS 차단 구역 내에서도 ISR 가치를 확장했습니다. 이러한 교훈들은 조달 시급성을 높였고 소형 UVA 시장의 상당 부분을 뒷받침했습니다.

전력 증강 효과 vs 유인 항공기

F-35 한 대의 가격은 약 8,000만 달러인 반면, 소형 UVA 혼합 군집은 그 예산의 일부로도 동등한 정찰 범위를 제공하여 지휘관들이 더 많은 표적을 위협 상태로 유지할 수 있게 합니다. 호주 시험에서 AI 알고리즘이 다중 드론을 동시 교전에 투입해 조종사 업무량을 줄이고 작전 발자국을 축소하는 모습이 확인되었습니다. 이후 록히드 마틴은 F-35가 자율 비행 편대를 통제하는 시연을 통해 개념의 실현 가능성을 입증하며 전 세계 공군들이 소형 UVA 시장으로 자금을 재분배하도록 유도했습니다.

사이버/EW 취약성과 UAS 확산

RTX 코퍼레이션의 사업부인 레이시온은 코요테 요격기 수주액 1억 9600만 달러를, 앤두릴은 로드러너/펄서 수주액 2억 5000만 달러를 기록하며 공격용 드론의 우위를 잠식할 수 있는 방위 무기 경쟁을 부각시켰습니다. 카타르의 10억 달러 규모 FS-LIDS 구매는 소규모 군대조차도 암호화되지 않은 무선 통신을 무력화할 수 있는 다층 방위 체계를 구축할 수 있음을 보여주었습니다. 엘빗 시스템즈는 NATO 회원국에 C-UAS 키트를 공급하며, 생존성 업그레이드가 플랫폼 로드맵을 형성하고 소형 UVA 시장의 단기 성장을 억제할 것임을 재확인했습니다.

부문 분석

고정익 시스템은 ISR 순찰에 필요한 항속 거리를 확장하는 공기역학적 효율성 덕분에 2024년 소형 UVA 시장에서 55.45% 점유율로 선두를 차지했습니다. 운영자들은 회전익 플랫폼 대비 은밀한 음향 시그니처와 단순한 유지보수 주기를 높이 평가했습니다. 그러나 육군의 미래 전술 무인 항공기 시스템(FTUAS)과 같은 프로그램이 수직 발사와 장거리 순항 능력을 동시에 요구함에 따라 하이브리드 기체는 13.60%의 연평균 성장률(CAGR)을 기록했습니다. 동시에 하이브리드 변형의 소형 UVA 시장 규모는 서보 무게 감소와 더 소형화된 비행 컴퓨터의 혜택을 받았습니다.

회전익 UVA는 기동성이 내구성을 압도하는 밀집된 도시 골목에서 틈새 시장을 유지했습니다. AI 비행 제어기는 하이브리드 기체가 호버링과 활공 사이를 자동 전환하도록 하여 조종사 작업량 증가 없이 커버리지율을 향상시켰습니다. 에어로바이런먼트(AeroVironment)와 같은 업체들은 이러한 크로스 도메인 기동성을 구현한 JUMP 20-X 프로토타입을 선보였으며, 활주로가 없는 환경에서 시험을 통과했습니다. 이러한 특성으로 인해 조달 기획자들은 기체 다양화를 추진했으며, 이로 인해 소형 UVA 시장 전반에 걸쳐 하이브리드 기종이 점유율을 점진적으로 확대할 수 있었습니다.

2-20kg의 소형 UVA는 2024년 소형 UVA 시장 점유율의 59.17%를 차지했으며, 이는 분대 수준의 휴대성과 EO/IR 탑재체에 충분한 배터리 용량을 반영한 결과입니다. 보병 부대가 발사 레일이나 회수망 없이 운용 가능했기에 채택률은 높은 수준을 유지했습니다. 그러나 2kg 미만의 나노/마이크로 기체는 비디오게임 스타일 컨트롤러와 250g 미만 센서가 새로운 정찰 임무를 가능케 하면서 12.47%의 연평균 성장률(CAGR)을 기록했습니다. 이러한 초경량 기체의 소형 UAV 시장 규모는 네로스 아처 FPV 드론이 블루 UAS 인증을 획득하며 전선 배치에 대한 규제적 수용 신호를 보내면서 더욱 확대되었습니다. 소형(20-150kg) 기체는 기동력과 연료 용량이 은밀성보다 중요한 분야에서 유용성을 유지했으나, 분산형 살상력으로의 교리 전환으로 인해 추가 주문량은 소폭 증가에 그쳤습니다. 해병대와 육군의 실험 결과, 일회용 폼 바디 쿼드콥터조차도 최소 비용으로 의미 있는 전장 인지 능력을 제공함이 확인되었습니다. 이에 따라 조달 규정은 점점 더 다양한 구성 요소를 명시하여 소대장이 지속 시간, 탑재량, 투척 후 즉시 사용 편의성 중 선택할 수 있도록 함으로써 소형 UVA 시장을 강화했습니다.

지역 분석

북미는 2024년 매출의 48.90%를 차지했으며, 에어로바이런먼트(AeroVironment)의 9억 9천만 달러 수주와 같은 다년 계약 및 국내 조달을 의무화한 정책 조치의 혜택을 받았습니다. 블루 UAS 인증 제도는 미국 공급업체들이 인쇄회로기판, 배터리, 광학 부품 공급망을 내재화하도록 유도하여 대외 제재 위험을 제한했습니다. 캐나다와 멕시코도 유사한 심사 체계를 도입하여 소형 UVA 시장 내 국경 간 수요를 유지했습니다.

아시아태평양 지역은 중국, 호주, 인도, 일본이 지역적 분쟁 지점 완화를 위해 경쟁하면서 2030년까지 11.95%라는 가장 가파른 연평균 성장률(CAGR)을 기록했습니다. 베이징의 모선 개념과 도쿄의 유로드론 연계 가능성은 조달을 개별 프로그램에서 통합 전력 구조로 전환시켜 시장 총 가치를 높였습니다. 캔버라의 인공지능 제어 유령박쥐형 군집 투자로 인한 교리 전환은 태평양 동맹국들이 이를 모방하며 소형 UVA 시장 기회를 증폭시켰습니다. 그러나 말레이시아 배터리 공장 및 대만 마이크로컨트롤러를 중심으로 한 공급망 집적은 지정학적 리스크 프리미엄을 초래했습니다.

유럽에서는 8,000억 유로(9,371억 1,000만 달러)의 ReArm Europe 펀드와 1,500억 유로(1,757억 1,000만 달러)의 EU 대출 계획이 현지 생산을 지원하고 외부 공급업체에 대한 의존도를 완화했습니다. 유로 드론 프로그램, 독일에 의한 영국 주도의 GCAP 회원의 검토, NATO 대 UAS 조달은 ISR과 공격형에 지출을 분산시켜 대륙의 탄력성을 강화했습니다. 카타르의 30억 달러 계약으로 대표되는 중동 주문은 아프리카에서의 채택 지연을 상쇄하는 수량 증가를 초래하여 소형 UAV 시장의 광범위한 지리적 균형을 확보했습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

목차

제1장 서론

- 조사의 전제조건과 시장의 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 경쟁 환경에서 실시간 ISR 수요

- 유인 항공기 대비 전투력 증강 효과

- 국방부 지원 병사 휴대형 및 분대급 드론 프로그램

- AI 기반 자율 군집 작전 능력

- GPS 차단 환경 항법 기술 개발을 위한 DARPA 프로젝트

- 소모성 체공형 무기의 신속 배치

- 시장 성장 억제요인

- 사이버/전자전 취약성 및 대 UVA(C-UAS) 확산

- 짧은 항속 시간 및 제한된 살상 페이로드

- 수출 통제(ITAR/MTCR) 장벽

- 반도체 및 리튬 이온 전지 공급망 위험

- 밸류체인 분석

- 규제 상황

- 기술의 전망

- Porter's Five Forces 분석

- 신규 참가업체의 위협

- 구매자의 협상력

- 공급기업의 협상력

- 대체품의 위협

- 경쟁 기업간 경쟁 관계

제5장 시장 규모와 성장 예측

- 날개 유형별

- 고정익

- 회전익

- 하이브리드

- 사이즈 클래스별

- 나노/마이크로(2kg 미만)

- 미니(2-20kg)

- 소형(20-150kg)

- 용도별

- 정찰, 감시 및 정보 수집(ISR)

- 전투 - 체공형 무기

- 물류 및 재보급

- 전자전(EW)

- 훈련 및 시뮬레이션

- 추진 유형별

- 내연기관

- 배터리

- 연료전지

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 영국

- 프랑스

- 독일

- 러시아

- 기타 유럽

- 아시아태평양

- 중국

- 일본

- 인도

- 한국

- 호주

- 기타 아시아태평양

- 남미

- 브라질

- 기타 남미

- 중동 및 아프리카

- 중동

- 사우디아라비아

- 아랍에미리트(UAE)

- 이스라엘

- 튀르키예

- 기타 중동

- 아프리카

- 남아프리카

- 기타 아프리카

- 북미

제6장 경쟁 구도

- 시장 집중도

- 전략적 동향

- 시장 점유율 분석

- 기업 프로파일

- AeroVironment, Inc.

- Teledyne Technologies Incorporated

- Elbit Systems Ltd.

- BAYKAR MAKINA SANAYI VE TICARET AS

- Northrop Grumman Corporation

- Lockheed Martin Corporation

- Textron Inc.

- Parrot Drones SAS

- Skydio, Inc.

- Anduril Industries, Inc.

- EDGE Group PJSC

- Israel Aerospace Industries Ltd.

- Leonardo SpA

- QinetiQ Group

- ideaForge Technology Ltd.

제7장 시장 기회와 장래의 전망

HBR 25.11.10The small UAV market size stood at USD 1.56 billion in 2025 and is forecasted to reach USD 2.58 billion by 2030, advancing at a 10.59% CAGR.

North American defense procurement programs and an executive order on domestic drone dominance drove early demand, while Asia-Pacific modernization plans continued to accelerate adoption. Swarm autonomy, hybrid airframe designs, and hydrogen fuel-cell propulsion created fresh avenues for differentiation, even as counter-UAS spending threatened to blunt tactical advantages. Semiconductors and lithium-ion cells remained supply-chain pinch points, pushing buyers to favor vendors with assured domestic sourcing. Competitors are therefore focused on vertical integration, software-first architectures, and export-compliant designs to secure a share in the small UAV market.

Global Small UAV Market Trends and Insights

Demand for Real-Time ISR in Contested Environments

Persistent surveillance proved indispensable for commanders operating without full air superiority. Small UAVs flew below radar coverage and streamed video directly to tactical tablets, as seen in the US Army Short Range Reconnaissance effort that invested USD 500 million in compact systems. Ukrainian forces validated quantity-over-quality tactics by launching millions of drones for field awareness. German-supplied HF-1 strike UAVs then added AI terrain-mapping to evade GNSS jamming, extending ISR value inside GPS-denied corridors. Together, these lessons lifted procurement urgency and underpinned a sizable portion of the small UAV market.

Force-Multiplier Value vs Crewed Aircraft

One F-35 costs roughly USD 80 million, whereas a mixed swarm of small UAVs delivers comparable reconnaissance coverage at a fraction of that budget, enabling commanders to hold more targets at risk. Australian trials showed AI algorithms dispatching multiple drones for simultaneous engagements, trimming pilot workload, and shrinking operational footprints. Lockheed Martin then demonstrated an F-35 controlling autonomous wingmen, proving the concept's viability and nudging air arms worldwide to reallocate funds toward the small UAV market.

Cyber/EW Vulnerability and Counter-UAS Proliferation

Raytheon, a business unit of RTX Corporation, earned a USD 196 million order for Coyote interceptors, while Anduril booked USD 250 million for Roadrunner/Pulsar, underscoring a defensive arms race that could erode offensive drone advantages. Qatar's USD 1 billion FS-LIDS purchase illustrated how even smaller militaries can field layered defenses capable of neutralizing unencrypted radio links. Elbit Systems delivered C-UAS kits to NATO states, reaffirming that survivability upgrades would shape platform roadmaps and temper the near-term growth of the small UAV market.

Other drivers and restraints analyzed in the detailed report include:

- DoD-Funded Soldier-Borne and Squad-Level Drone Programs

- AI-Enabled Autonomous Swarming Capability

- Short Endurance and Limited Lethal Payload

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Fixed-wing systems led the small UAV market with 55.45% share in 2024, thanks to aerodynamic efficiency that extended ranges needed for ISR patrols. Operators valued their stealthier acoustic signatures and simpler maintenance cycles compared with rotary platforms. Hybrid airframes nevertheless logged a 13.60% CAGR as programs such as the Army's Future Tactical Unmanned Aircraft System demanded vertical launch paired with long-range cruise capabilities. In parallel, the small UAV market size for hybrid variants benefited from shrinking servo weights and more compact flight computers.

Rotary-wing UAVs retained niches in dense urban canyons where maneuverability trumped stamina. AI flight controllers let hybrid vehicles auto-shift between hover and glide, improving coverage rates without adding piloting workload. Vendors such as AeroVironment fielded JUMP 20-X prototypes that embodied this cross-domain agility, winning trials where runways were unavailable. These characteristics prompted procurement planners to diversify fleets, ensuring that hybrids captured incremental budget share across the small UAV market.

Mini UAVs weighing 2 to 20 kg represented 59.17% of the small UAV market share in 2024, aligning with squad portability and enough battery mass for EO/IR payloads. Adoption stayed high because infantry formations required no launch rails or recovery nets. Yet Nano/Micro craft under 2 kg registered a 12.47% CAGR as videogame-style controllers and sub-250 g sensors unlocked new reconnaissance roles. The small UAV market size for these featherweight units grew further once the Neros Archer FPV drone achieved Blue UAS certification, signaling regulatory acceptance for frontline use. Small (20 to 150 kg) vehicles retained utility where lift and fuel capacity trumped stealth, but doctrinal shifts toward distributed lethality kept incremental orders modest. Marine Corps and Army experiments confirmed that even disposable foam-bodied quadcopters produced meaningful battlefield awareness at minimal cost. Accordingly, procurement charters increasingly specified mixed complements that let platoon leaders choose between endurance, payload, and throw-and-go convenience, strengthening the small UAV market.

The Small UAV Market Report is Segmented by Wing Type (Fixed Wing, Rotary Wing, and Hybrid), Size Class (Nano/Micro, Mini, and Small), Application (Electronic Warfare, Logistics and Resupply, and More), Propulsion Type (Internal Combustion Engine, Batteries, and More), and Geography (North America, Europe, Asia-Pacific, and More). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America commanded 48.90% revenue in 2024, benefiting from multi-year contracts such as AeroVironment's USD 990 million award and policy measures that mandated domestic sourcing. Blue UAS accreditation incentivized U.S. suppliers to internalize printed-circuit, battery, and optical supply chains, limiting exposure to foreign sanctions. Canada and Mexico adopted similar vetting regimes, sustaining cross-border demand inside the small UAV market.

Asia-Pacific delivered the steepest 11.95% CAGR through 2030 as China, Australia, India, and Japan raced to offset regional flashpoints. Beijing's mothership concept and Tokyo's potential tie-ins with Eurodrone moved procurement from isolated programs to integrated force structures, raising total market value. Canberra's investment in AI-controlled ghost-bat style swarms signalled a doctrinal pivot that other Pacific allies replicated, compounding opportunity for the small UAV market. Supply-chain clustering around Malaysian battery plants and Taiwanese microcontrollers, however, introduced geopolitical risk premiums.

Europe's ReArm Europe fund of EUR 800 billion( USD 937.11 billion) and a EUR 150 billion (USD 175.71 billion) EU loan scheme underwrote local production and eased reliance on external vendors. The Eurodrone program, German consideration of UK-led GCAP membership, and NATO counter-UAS procurements diversified spend across ISR and strike variants, reinforcing continental resilience. Middle East orders, exemplified by Qatar's USD 3 billion agreement, added incremental volumes that offset slower adoption in Africa, ensuring broad geographic balance for the small UAV market.

- AeroVironment, Inc.

- Teledyne Technologies Incorporated

- Elbit Systems Ltd.

- BAYKAR MAKINA SANAYI VE TICARET A.S.

- Northrop Grumman Corporation

- Lockheed Martin Corporation

- Textron Inc.

- Parrot Drones SAS

- Skydio, Inc.

- Anduril Industries, Inc.

- EDGE Group PJSC

- Israel Aerospace Industries Ltd.

- Leonardo S.p.A

- QinetiQ Group

- ideaForge Technology Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Demand for real-time ISR in contested environments

- 4.2.2 Force-multiplier value vs crewed aircraft

- 4.2.3 DoD-funded soldier-borne and squad-level drone programs

- 4.2.4 AI-enabled autonomous swarming capability

- 4.2.5 DARPA projects for GPS-denied navigation

- 4.2.6 Rapid fielding of expendable loitering munitions

- 4.3 Market Restraints

- 4.3.1 Cyber/EW vulnerability and counter-UAS proliferation

- 4.3.2 Short endurance and limited lethal payload

- 4.3.3 Export-control (ITAR/MTCR) hurdles

- 4.3.4 Semiconductor and Li-ion cell supply-chain risk

- 4.4 Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Wing Type

- 5.1.1 Fixed Wing

- 5.1.2 Rotary Wing

- 5.1.3 Hybrid

- 5.2 By Size Class

- 5.2.1 Nano/Micro (Less than 2 kg)

- 5.2.2 Mini (2-20 kg)

- 5.2.3 Small (20-150 kg)

- 5.3 By Application

- 5.3.1 Intelligence, Surveillance, and Reconnaissance (ISR)

- 5.3.2 Combat - Loitering Munition

- 5.3.3 Logistics and Resupply

- 5.3.4 Electronic Warfare (EW)

- 5.3.5 Training and Simulation

- 5.4 By Propulsion Type

- 5.4.1 Internal Combustion Engine

- 5.4.2 Batteries

- 5.4.3 Fuel Cells

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 United Kingdom

- 5.5.2.2 France

- 5.5.2.3 Germany

- 5.5.2.4 Russia

- 5.5.2.5 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 South Korea

- 5.5.3.5 Australia

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Rest of South America

- 5.5.5 Middle East and Africa

- 5.5.5.1 Middle East

- 5.5.5.1.1 Saudi Arabia

- 5.5.5.1.2 United Arab Emirates

- 5.5.5.1.3 Israel

- 5.5.5.1.4 Turkey

- 5.5.5.1.5 Rest of Middle East

- 5.5.5.2 Africa

- 5.5.5.2.1 South Africa

- 5.5.5.2.2 Rest of Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global-level Overview, Market-level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 AeroVironment, Inc.

- 6.4.2 Teledyne Technologies Incorporated

- 6.4.3 Elbit Systems Ltd.

- 6.4.4 BAYKAR MAKINA SANAYI VE TICARET A.S.

- 6.4.5 Northrop Grumman Corporation

- 6.4.6 Lockheed Martin Corporation

- 6.4.7 Textron Inc.

- 6.4.8 Parrot Drones SAS

- 6.4.9 Skydio, Inc.

- 6.4.10 Anduril Industries, Inc.

- 6.4.11 EDGE Group PJSC

- 6.4.12 Israel Aerospace Industries Ltd.

- 6.4.13 Leonardo S.p.A

- 6.4.14 QinetiQ Group

- 6.4.15 ideaForge Technology Ltd.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment