|

시장보고서

상품코드

1850177

네트워크 연결 스토리지(NAS) 시장 : 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Network Attached Storage (NAS) - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

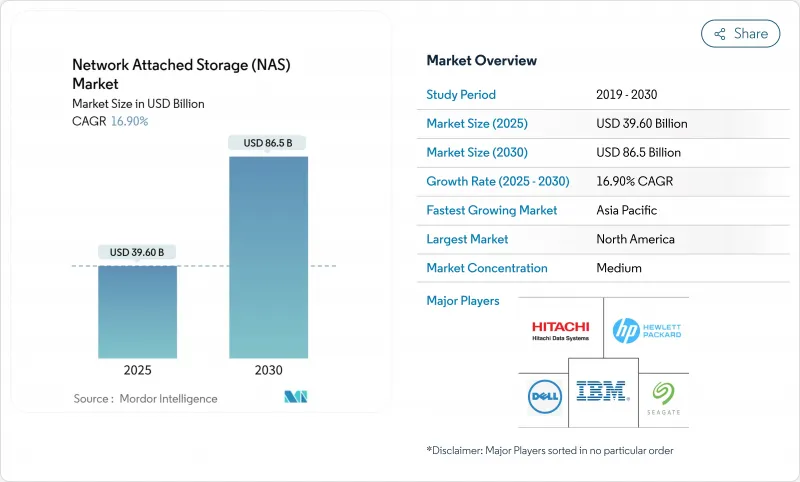

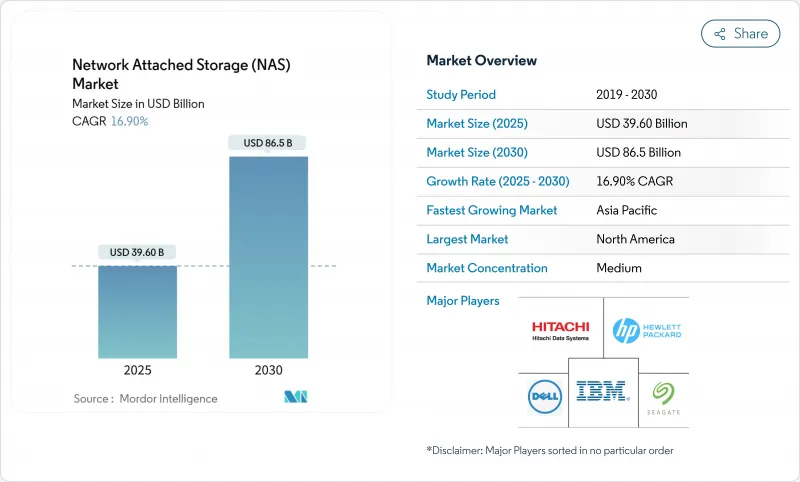

네트워크 연결 스토리지(NAS) 시장 규모는 2025년에 396억 달러, 예측 기간(2025-2030년)의 CAGR은 16.90%를 나타내고, 2030년에는 865억 달러에 달할 것으로 예측됩니다.

수요는 비구조화된 데이터 증가를 억제하려는 기업, 하이브리드 워크의 추진, 높은 처리량의 파일 서비스를 필요로 하는 AI/ML 워크로드의 도입에 의해 추진되고 있습니다. 벤더는 또한 지연 시간에 민감한 애플리케이션이 사용자 가까이에서 실행되는 5G 에지 사이트 부근의 On-Premise 솔루션에 대한 관심이 다시 높아진 것으로부터 이익을 얻었습니다. 북미는 2024년 기준에서도 수익의 리더로 지속되고 있지만, 아시아태평양은 대규모 데이터센터 구축과 디지털 변혁의 가속을 배경으로 성장 페이스를 올리고 있습니다. 경쟁력 다이어그램은 소프트웨어 정의, AI 최적화 및 하이브리드 클라우드에 기울어지고 있으며 로컬 성능과 클라우드 경제성이 융합되어 있습니다.

세계 네트워크 연결 스토리지(NAS) 시장 동향 및 통찰

비정형 데이터의 폭발적 증가

기업의 연간 데이터 양은 20% 이상의 속도로 확대되었으며 IT 팀은 스토리지의 탄력성을 재검토할 필요가 있었습니다. 많은 기업들은 비용과 성능의 균형을 맞추기 위해 자동 계층화를 적용하면서 다운타임 없이 노드별로 확장할 수 있는 스케일 아웃 NAS로 전환했습니다. 의료 서비스 제공업체는 일반적으로 이러한 이동을 보여주며 지출을 억제하기 위해 정책 중심의 배치에 의존하면서 이전보다 더 큰 이미지 파일을 아카이브하고 있습니다.

원격 워크와 하이브리드 워크의 데이터 급증

하이브리드 워크는 에지 오피스와 홈 네트워크를 주요 데이터 작성 장소로 만들었습니다. 기업은 세계 네임스페이스를 공개하고 WAN 캐싱으로 트래픽을 가속화하는 NAS 어플라이언스를 배포하여 대응했습니다. 많은 팀은 콜드 데이터를 클라우드 계층에 넣고 활성 프로젝트 파일을 자동으로 동기화하는 프리미어 장치에 넣어 사용자 경험에 영향을주지 않고 브랜치 인프라 비용을 줄였습니다.

클라우드 스토리지 대체

소비 기반 클라우드 스토리지는 순수한 On-Premise NAS 수요를 계속 낮추고 OPEX 모델과 탄력적인 스케일링을 선호하는 조직을 끌어들였습니다. 벤더는 클라우드 티어링, 객체 버킷에 대한 스냅샷 복제, 기존의 설비 투자 경계를 모호하게 하는 구독 가격을 통합함으로써 위험을 줄이고 클라우드의 인력을 인식하면서 어플라이언스의 관련성을 유지했습니다.

부문 분석

2024년 네트워크 연결 스토리지(NAS) 시장 점유율은 스케일 아웃 어레이가 52%를 차지했습니다. 이 아키텍처를 통해 관리자는 성능과 용량을 선형에 추가할 수 있게 되었으며 지게차 업그레이드가 필요 없으며 몇 달 안에 두 배가 되는 데이터 세트를 지원할 수 있습니다. 그 결과, 이 부문은 2025년부터 2030년까지 18%의 연평균 복합 성장률(CAGR)을 나타낼 전망입니다. 이와는 대조적으로, 스케일업 어플라이언스는 탄력적인 스케일링보다 단순성을 선호하는 소규모 팀들 사이에서 인기를 유지하고 있습니다. IBM SONAS는 수십억 개의 파일을 단일 네임스페이스로 관리하고 자동 계층화를 통해 소유 비용을 최대 40%까지 절감하여 스케일 아웃의 효율성을 입증했습니다.

스케일업 제품은 초기 정가의 저렴함과 관리의 용이성에 도움이 되어 부문이나 중소기업용으로 계속 출하되었습니다. 그러나 미디어 포스트 프로덕션 및 유전체 분석기업에서 전형적인 높은 동시 처리량을 필요로 하는 워크로드는 클러스터된 설계에 끌렸습니다. 예측 기간 동안 NVMe-oF 및 400GbE 네트워킹과 같은 하드웨어의 발전이 스케일 아웃 분야에 기세를 주고, 보다 광범위한 네트워크 부착 스토리지 시장의 중심으로 자리를 강화할 것으로 예측됩니다.

On-Premise 구성은 여전히 2024년 매출의 52%를 차지하지만, 기업은 로컬 어레이와 온디맨드 클라우드 용량을 혼합하는 경향을 강화하고 있습니다. 하이브리드 계층 CAGR은 21.1%로 네트워크 연결 스토리지(NAS) 시장에서 가장 빠른 것으로 예측됩니다. 엔터프라이즈는 컴플라이언스에서 중요한 데이터 세트를 현장에 보관하면서 비활성 파일을 클라우드 버킷으로 리디렉션합니다. 이 모델은 환경에서 스냅샷을 원활하게 이동하는 Dell 비정형 데이터 서비스에서 지원됩니다.

데이터센터의 설치 면적을 축소하고, 클라우드 퍼스트 전략을 채택하도록 기업에 명명됨으로써 퓨어 클라우드 NAS도 성장했습니다. 공급업체는 이에 따라 엔드포인트 간의 정책 관리를 위한 단일 대시보드, 정지 시 기본 암호화, DevOps 자동화를 위한 API 후크를 선호했습니다. 시간이 지남에 따라 지역 및 공급업체를 가로지르는 멀티클라우드 파일 서비스는 비용 차이를 평준화하고, 하이브리드 아키텍처에 대한 전반적인 견인력을 강화하고, 네트워크 연결 스토리지(NAS) 시장 규모의 상호작용에서 역할을 확고하게 할 것으로 예측됩니다.

지역 분석

북미는 딥 클라우드 연결성, 하이퍼스케일 구매자 집중, 성숙한 채널 생태계를 통해 2024년 매출의 39%를 차지했습니다. 미국 기업은 AI 추론을 지원하고 사이버 보험 요구 사항 증가를 충족하기 위해 파일 플랫폼의 혁신을 계속했습니다. 캐나다와 멕시코는 금융, 정부 기관 및 제조업의 업그레이드를 추진하여 네트워크 연결 스토리지(NAS) 시장에서 이 지역의 중진으로서의 지위를 강화했습니다.

아시아태평양은 2025년부터 2030년까지 18%의 연평균 복합 성장률(CAGR)로 성장하여 가장 빠른 궤도를 기록할 것으로 예상됩니다. 중국의 디지털 인프라에 대한 자극책, 인도의 5G 전개, 일본의 엣지 제조 로봇에 대한 투자로 용량 전개가 확대되었습니다. 국내 ODM은 가격 경쟁력 있는 올플래시 기어를 제공하고 국내 기업에 외자계 기존 기업을 대체할 수 있는 옵션을 제공했습니다. 디지털 성숙도 향상과 의욕적인 데이터센터 건설이 결합되어 아시아태평양은 미래의 네트워크 연결 스토리지(NAS) 시장 점유율의 일각을 차지하게 됩니다.

유럽은 GDPR(EU 개인정보보호규정) 기반 컴플라이언스에 대한 지출과 자동차 및 제약 업계의 엣지 컴퓨팅에 의해 지원되며 여전히 중요한 위치를 차지하고 있습니다. 중동 및 아프리카에서는 스마트 시티와 유전 원격 측정 프로젝트에서 조기에 도입이 진행되었고, 라틴아메리카에서는 광대역 품질과 데이터 주권의 틀이 성숙함에 따라 더욱 완만한 상승세가 보였습니다. 전 지역에서 공통적인 것은 데이터 레지던시의 검토가 강화되어 네트워크 연결 스토리지(NAS) 시장에 꿰매어진 하이브리드 및 에지 편중의 배포 전략이 더욱 입증되었습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 서포트

목차

제1장 서론

- 조사의 전제조건과 시장의 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 비구조화 데이터의 폭발적 증가

- 리모트 워크와 하이브리드 워크 데이터의 급증

- 데이터센터 가상화와 SD-NAS

- 5G 엣지 구축에 의해 On-Premise NAS가 강화

- AI/ML 트레이닝 워크로드에는 병렬 파일 액세스가 필요

- NAS 생산의 관세 기반 리쇼어링

- 시장 성장 억제요인

- 클라우드 스토리지 대체

- 페타바이트 규모의 퍼포먼스 병목

- 폭발적인 데이터 증가로 TCO 상승

- On-Premise 파일 시스템의 사이버 보험료 상승

- 규제 상황

- 기술의 전망

- Porter's Five Forces

- 공급기업의 협상력

- 구매자의 협상력/소비자

- 신규 참가업체의 위협

- 대체품의 위협

- 경쟁 기업간 경쟁 관계

제5장 시장 규모와 성장 예측

- 유형별

- 스케일업

- 스케일 아웃

- 최종 사용자 업계별

- BFSI

- IT 및 통신

- 헬스케어

- 소매업 및 전자상거래

- 미디어 및 엔터테인먼트

- 정부 및 공공 부문

- 기타(교육, 제조)

- 전개별

- On-Premise

- 클라우드

- 하이브리드

- 제품 계층별

- 하이엔드/엔터프라이즈

- 미드마켓

- 로우엔드/SOHO

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 영국

- 독일

- 프랑스

- 이탈리아

- 기타 유럽

- 아시아태평양

- 중국

- 일본

- 인도

- 한국

- 기타 아시아

- 중동

- 이스라엘

- 사우디아라비아

- 아랍에미리트(UAE)

- 튀르키예

- 기타 중동

- 아프리카

- 남아프리카

- 이집트

- 기타 아프리카

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 북미

제6장 경쟁 구도

- 시장 집중도

- 전략적 동향

- 시장 점유율 분석

- 기업 프로파일

- Dell Technologies

- NetApp Inc.

- Synology Inc.

- QNAP Systems Inc.

- Hewlett Packard Enterprise

- Western Digital Corp.

- Seagate Technology PLC

- IBM Corporation

- Hitachi Vantara

- Cisco Systems Inc.

- Huawei Technologies Co. Ltd.

- Lenovo Group Ltd.

- Supermicro Computer Inc.

- Buffalo Inc.

- Zyxel Communications Corp.

- Asustor Inc.

- TerraMaster

- Thecus Technology Corp.

- Drobo Inc.

- Promise Technology

- Infortrend Technology Inc.

- Netgear Inc.

- HGST(WD subsidiary)

- TrueNAS(iXsystems)

- Fujitsu Ltd.

- NEC Corp.

제7장 시장 기회와 장래의 전망

SHW 25.11.07The Network Attached Storage Market size is estimated at USD 39.60 billion in 2025, and is expected to reach USD 86.5 billion by 2030, at a CAGR of 16.90% during the forecast period (2025-2030).

Demand has been buoyed by enterprises racing to contain unstructured-data growth, the push for hybrid work, and the capture of AI/ML workloads that need high-throughput file services. Vendors also benefited from renewed interest in on-premises solutions near 5G edge sites, where latency-sensitive applications run close to users. North America remained the revenue leader as of 2024, yet Asia-Pacific is setting the growth pace on the back of sizeable data-center build-outs and accelerated digital transformation. Competitive dynamics are tilting toward software-defined, AI-optimized, and hybrid-cloud offerings that blend local performance with cloud economics.

Global Network Attached Storage (NAS) Market Trends and Insights

Explosion of Unstructured Data

Annual enterprise data volume expanded at rates that routinely exceeded 20%, forcing IT teams to rethink storage elasticity. Many migrated toward scale-out NAS that scales node-by-node without downtime, while applying automated tiering to balance cost and performance. Healthcare providers typified this shift, archiving ever-larger imaging files while relying on policy-driven placement to curb spending.

Remote and Hybrid-Work Data Surge

Hybrid work turned edge offices and home networks into primary data creators. Enterprises responded by rolling out NAS appliances that expose a global namespace and accelerate traffic with WAN caching. Many teams placed cold data in cloud tiers while keeping active project files on-prem devices that synchronize automatically, reducing branch infrastructure cost without impacting user experience.

Cloud-Storage Substitution

Consumption-based cloud storage kept eroding demand for purely on-prem NAS, attracting organizations that preferred opex models and elastic scaling. Vendors mitigated the risk by embedding cloud tiering, snapshot replication to object buckets, and subscription pricing that blurs traditional capex boundaries, preserving appliance relevance while acknowledging the cloud's pull.

Other drivers and restraints analyzed in the detailed report include:

- Data-Center Virtualization and SD-NAS

- 5G Edge Build-Out Boosts On-Prem NAS

- Performance Bottlenecks at Petabyte Scale

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Scale-out arrays held 52% of the network-attached storage market share in 2024. The architecture allowed administrators to add performance and capacity linearly, removing forklift upgrades and supporting data sets that were doubling in months. As a result, the segment is forecast to log an 18% CAGR from 2025-2030. In contrast, scale-up appliances stayed popular with smaller teams that favored simplicity over elastic scaling. IBM SONAS demonstrated scale-out efficiency by managing billions of files under a single namespace while driving ownership costs down by up to 40% through automated tiering.

Scale-up products continued to ship into departmental and SMB settings, helped by lower initial list prices and straightforward administration. Yet once workloads required high concurrent throughput, typical in media post-production or genomic analysis enterprises, gravitated to clustered designs. Over the forecast period, incremental hardware advances such as NVMe-oF and 400 GbE networking are expected to add momentum to the scale-out segment, reinforcing its position at the heart of the broader network-attached storage market.

On-premise configurations still commanded 52% of 2024 revenue, yet enterprises increasingly blended local arrays with on-demand cloud capacity. The hybrid tier is projected to notch a 21.1% CAGR, the fastest within the network-attached storage market. Organizations retained compliance-sensitive datasets onsite while redirecting inactive files to cloud buckets, a model supported by Dell's unstructured-data services that move snapshots seamlessly between environments.

Pure-cloud NAS grew too, propelled by corporate mandates to shrink data-center footprints and adopt cloud-first strategies. Vendors accordingly prioritized single dashboards for policy management across endpoints, default encryption at rest, and API hooks for DevOps automation. Over time, multi-cloud file services that span regions and providers are expected to flatten cost differentials and strengthen the overall pull toward hybrid architectures, cementing their role in the network-attached storage market size dialogue.

Network Attached Storage (NAS) Market Report is Segmented by Type (Scale-Up, Scale-Out), End-User Industry (BFSI, IT and Telecom, and More), Deployment (On-Premise, Cloud, and Hybrid), Product Tier (High-end/Enterprise, Mid-Market, Low-end/SOHO), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America held 39% of 2024 revenue owing to deep cloud connectivity, a concentration of hyperscale buyers, and a mature channel ecosystem. United States enterprises continued to refresh file platforms to support AI inference as well as to satisfy rising cyber-insurance requirements. Canada and Mexico made progress in finance, government, and manufacturing upgrades, reinforcing the region's heavyweight status within the network attached storage market.

Asia-Pacific registered the quickest trajectory, clocking an expected 18% CAGR for 2025-2030. China's stimulus for digital infrastructure, India's 5G rollout, and Japan's investment in edge manufacturing robotics amplified capacity deployments. Local ODMs offered price-competitive all-flash gear, giving domestic firms alternatives to foreign incumbents. The combination of rising digital maturity and ambitious data-center construction positions Asia-Pacific to lift its slice of future network attached storage market share.

Europe remained significant, helped by GDPR-driven compliance spending and edge computing in automotive and pharmaceutical corridors. The Middle East and Africa saw early adoption in smart-city and oil-field telemetry projects, while Latin America trended upward more gradually as broadband quality and data-sovereignty frameworks matured. Across all regions, the common denominator was heightened scrutiny of data residency, further validating hybrid and edge-heavy deployment strategies sewn into the network attached storage market.

- Dell Technologies

- NetApp Inc.

- Synology Inc.

- QNAP Systems Inc.

- Hewlett Packard Enterprise

- Western Digital Corp.

- Seagate Technology PLC

- IBM Corporation

- Hitachi Vantara

- Cisco Systems Inc.

- Huawei Technologies Co. Ltd.

- Lenovo Group Ltd.

- Supermicro Computer Inc.

- Buffalo Inc.

- Zyxel Communications Corp.

- Asustor Inc.

- TerraMaster

- Thecus Technology Corp.

- Drobo Inc.

- Promise Technology

- Infortrend Technology Inc.

- Netgear Inc.

- HGST (WD subsidiary)

- TrueNAS (iXsystems)

- Fujitsu Ltd.

- NEC Corp.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Explosion of unstructured data

- 4.2.2 Remote and hybrid-work data surge

- 4.2.3 Data-center virtualization and SD-NAS

- 4.2.4 5G edge build-out boosts on-prem NAS

- 4.2.5 AI/ML training workloads need parallel file access

- 4.2.6 Tariff-driven reshoring of NAS production

- 4.3 Market Restraints

- 4.3.1 Cloud-storage substitution

- 4.3.2 Performance bottlenecks at petabyte scale

- 4.3.3 High TCO with explosive data growth

- 4.3.4 Rising cyber-insurance premiums for on-prem file systems

- 4.4 Regulatory Landscape

- 4.5 Technological Outlook

- 4.6 Porter's Five Forces

- 4.6.1 Bargaining Power of Suppliers

- 4.6.2 Bargaining Power of Buyers/Consumers

- 4.6.3 Threat of New Entrants

- 4.6.4 Threat of Substitutes

- 4.6.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Type

- 5.1.1 Scale-up

- 5.1.2 Scale-out

- 5.2 By End-user Industry

- 5.2.1 BFSI

- 5.2.2 IT and Telecom

- 5.2.3 Healthcare

- 5.2.4 Retail and E-commerce

- 5.2.5 Media and Entertainment

- 5.2.6 Government and Public Sector

- 5.2.7 Others (Education, Manufacturing)

- 5.3 By Deployment

- 5.3.1 On-premise

- 5.3.2 Cloud

- 5.3.3 Hybrid

- 5.4 By Product Tier

- 5.4.1 High-end / Enterprise

- 5.4.2 Mid-market

- 5.4.3 Low-end / SOHO

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 United Kingdom

- 5.5.2.2 Germany

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 South Korea

- 5.5.3.5 Rest of Asia

- 5.5.4 Middle East

- 5.5.4.1 Israel

- 5.5.4.2 Saudi Arabia

- 5.5.4.3 United Arab Emirates

- 5.5.4.4 Turkey

- 5.5.4.5 Rest of Middle East

- 5.5.5 Africa

- 5.5.5.1 South Africa

- 5.5.5.2 Egypt

- 5.5.5.3 Rest of Africa

- 5.5.6 South America

- 5.5.6.1 Brazil

- 5.5.6.2 Argentina

- 5.5.6.3 Rest of South America

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Dell Technologies

- 6.4.2 NetApp Inc.

- 6.4.3 Synology Inc.

- 6.4.4 QNAP Systems Inc.

- 6.4.5 Hewlett Packard Enterprise

- 6.4.6 Western Digital Corp.

- 6.4.7 Seagate Technology PLC

- 6.4.8 IBM Corporation

- 6.4.9 Hitachi Vantara

- 6.4.10 Cisco Systems Inc.

- 6.4.11 Huawei Technologies Co. Ltd.

- 6.4.12 Lenovo Group Ltd.

- 6.4.13 Supermicro Computer Inc.

- 6.4.14 Buffalo Inc.

- 6.4.15 Zyxel Communications Corp.

- 6.4.16 Asustor Inc.

- 6.4.17 TerraMaster

- 6.4.18 Thecus Technology Corp.

- 6.4.19 Drobo Inc.

- 6.4.20 Promise Technology

- 6.4.21 Infortrend Technology Inc.

- 6.4.22 Netgear Inc.

- 6.4.23 HGST (WD subsidiary)

- 6.4.24 TrueNAS (iXsystems)

- 6.4.25 Fujitsu Ltd.

- 6.4.26 NEC Corp.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment