|

시장보고서

상품코드

1850180

클라우드 TV 시장 : 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Cloud TV - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

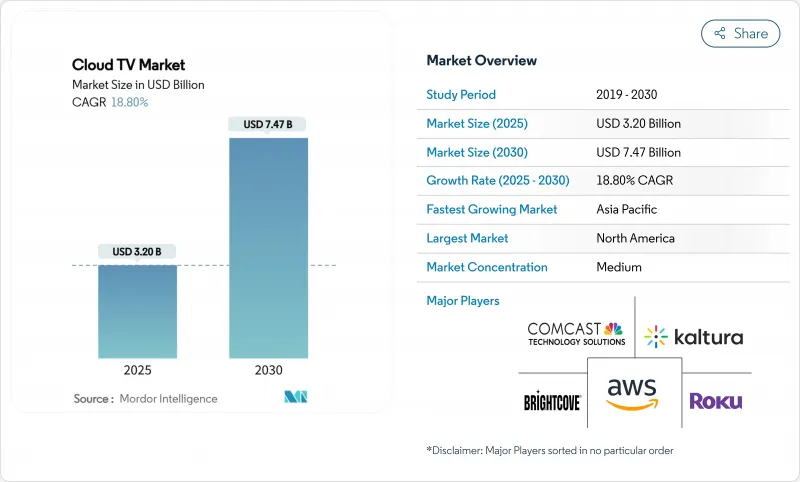

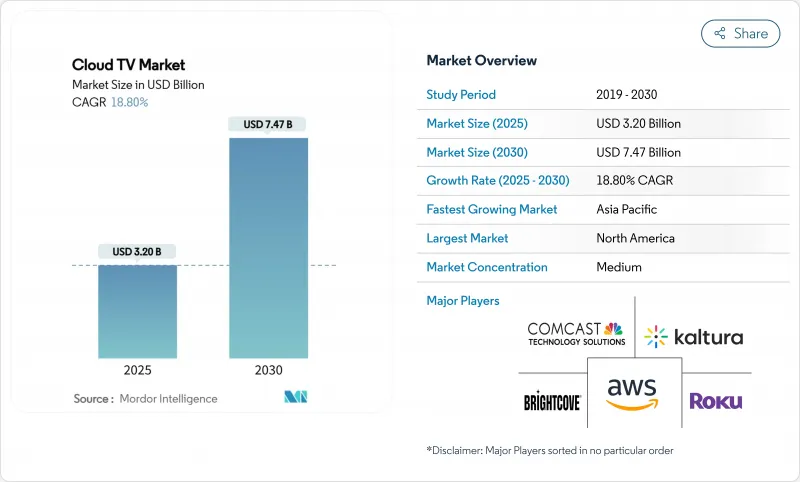

클라우드 TV 시장 규모는 2025년에 32억 달러, 2030년에는 74억 7,000만 달러로 성장하고, 2025-2030년의 CAGR은 18.8%를 나타낼 전망입니다.

확장 가능한 비디오 워크플로우에 대한 수요의 급증, 5G의 급속한 전개, 통신 사업자의 컨버전스 전략이 채택을 추진하고 있습니다. 퍼블릭 클라우드의 도입이 여전히 주류이지만 미디어 회사가 탄력성과 브로드캐스트 등급 성능의 균형을 맞추면서 하이브리드 아키텍처가 지지되고 있습니다. 규제의 단편화, 반도체 공급의 제약, iOS 획득 비용의 상승은 여전히 성장의 역풍입니다. 플랫폼 사업자, 기기 OEM, 통신 사업자 간의 경쟁 격화에 의해 벤더는 AI 주도의 디스커버리, 컨텍스츄얼 광고, 통합 클라우드 게임 서비스에 의한 차별화를 강요받고 있습니다. 아시아태평양에서는 네트워크의 신속한 배치와 스마트폰의 대량 보급으로 조기 진출기업이 비대칭적인 우위를 확보하고 있습니다.

세계 클라우드 TV - 시장 동향과 통찰력

안정적인 OTT 전달을 가능하게 하는 지속적인 광섬유 가정 내 배치

FTTH의 보급률은 대부분의 선진국 시장에서 50%를 넘어 클라우드 TV시장이 버퍼 없는 4K 및 8K 스트림에 필요한 대역폭의 신뢰성을 창출하고 있습니다. AT&T 등의 통신사업자는 2025년까지 150억 달러를 투입하여 3,000만 가구에 광섬유 부설을 진행하고 있으며, 비용이 많이 드는 엣지 캐시에 대한 의존도를 낮추고 프리미엄 스포츠의 라이브 스트리밍을 촉진하고 있습니다. 운영자는 비트율 상한을 없애는 무제한 데이터 계층을 번들링하거나 대화형 기능을 지원하기 위해 결정적 QoS를 활용하여 광섬유를 더욱 수익화합니다.

북미와 유럽에서 5G 고정 무선 액세스의 급속한 확대

5G FWA는 10ms 이하의 대기 시간으로 100-200Mbps의 다운링크를 제공하며, 지금까지 충분한 서비스가 제공되지 않았던 지역의 영역을 실행 가능한 클라우드 TV시장 주소로 바꿉니다. T-Mobile이나 Verizon을 포함한 통신사업자는 2025년까지 400만-500만명의 FWA 가입자와 계약하는 것을 목표로 하고 있으며, 다년간의 트렌치 비용 없이 서비스의 보급을 가속시킵니다. 광대역 + TV 번들 플랜과 RV 차량 소유자를위한 휴대용 클라우드 TV의 이용 사례는 지역 수요를 더욱 증가시킵니다.

신흥 아프리카와 카리브해 제도의 단편 CDN 발자국

국내 평균 대기시간은 북미의 45밀리초 이하에 비해 아프리카의 대부분에서 78밀리초에 이르며 일관된 1080p 스트리밍을 제한하고 있습니다. 이 지역의 인터넷 트래픽의 약 50%는 해외 업스트림 제공업체를 통해 2024년에 서아프리카 해저 케이블에 장애가 발생하여 13개국이 기능부전에 빠졌습니다. 현지 PoP가 없으면 클라우드 TV서비스 제공업체는 비트레이트를 낮춰야 하며 경험의 질과 광고 수익률이 저하됩니다.

부문 분석

퍼블릭 클라우드는 2024년 매출의 52%를 차지했지만 방송국이 예측 가능한 QoS와 함께 유연한 버스트 용량을 추구하고 있기 때문에 하이브리드 구성은 2030년까지 21.3%의 연평균 복합 성장률(CAGR)을 보일 것으로 보입니다. 이 믹스를 통해 권리 소유자는 프리미엄 스포츠 아카이브를 개인 클러스터에 저장하면서 라이브 이벤트 트래픽은 하이퍼스케일러에 의존할 수 있습니다. 하이브리드 배포의 클라우드 TV시장 규모는 컨텐츠 소유자가 워크로드를 비용 곡선에 맞추고 노후화된 온프레임 엔코더에서 철수함에 따라 가속될 것으로 예측됩니다. 공공 미디어와 같은 규제의 영향을 받기 쉬운 업계에서는 이미 워크플로우의 45%를 하이브리드 노드로 마이그레이션하여 사용자 데이터를 현지화하고 있습니다. 이용 사례에 관계없이 단계적 전환은 레거시 폐지 위험을 피하고 피크 시즌에도 시청자에게 도달하지 못하게 지원합니다.

하이브리드의 채택은 국경을 넘은 저작권 관리도 해결합니다. 사업자는 디아스포라 인구에 가까운 공공 지역에 오리진 캐시를 배포하고 워터마크와 DRM 로직은 비공개 도메인에서 실행합니다. 공급업체는 Kubernetes 기반 트랜스코더로 지원되며 두 발자국을 탄력적으로 확장합니다. 그 결과 결제는 자본 투자에서 미세한 사용량으로 이동했으며 중견 네트워크는 새로운 ASIC을 구입하지 않고도 4K 전송을 테스트할 수 있게 되었습니다. 2030년까지 클라우드 TV투자의 결정 틀은 에너지 효율, 탄소 정보 공개, 소블린 클라우드의 의무화를 비트레이트의 경제성과 마찬가지로 중시할 것으로 보입니다.

커넥티드 TV(CTV)는 2024년 매출의 40%를 차지하지만 스마트폰은 23.5%의 연평균 복합 성장률(CAGR) 예측에서 가장 빠르게 성장하는 엔드포인트입니다. 오픈 RAN 5G와 저렴한 OLED 패널로 체감 격차가 모호해지고, 6.7인치 화면의 4K HDR은 라운지룸 세트에 필적합니다. 세로로 자른 단편 시리즈는 Gen-Z의 시계 목록을 석권하고 있으며, 게시자는 세로 및 가로 프레임을 위해 동시에 스토리 보드를 만들 수 있어야합니다. 2027년까지 동남아시아의 여러 나라에서 모바일 이용 클라우드 TV시장 점유율이 CTV를 추구할 것으로 예측됩니다.

광고주는 가구 그래프 기술을 사용하여 모바일에서 15초의 티저, CTV에서 30초의 딥 다이브, 태블릿에서 쇼핑 가능한 오버레이를 같은 날 저녁에 흘립니다. 클라우드 인코더 벤더는 활성 화면 크기에 맞는 동적 QR 코드 신호로 SSAI 마커를 내장하고 있습니다. 이러한 컨버전스는 기본 화면의 개념을 재구성하는 것이며, 이기기 위한 제안은 장치 별 UX가 아닌 마찰없는 핸드 오프를 제공하는 것입니다.

클라우드 TV - 시장 보고서는 배포(퍼블릭 클라우드, 프라이빗 클라우드, 하이브리드 클라우드), 기기 유형(STB, 휴대폰, 연결 TV), 용도(텔레콤, 엔터테인먼트 및 미디어 등), 조직 규모(중소기업, 대기업), 지역별로 분류됩니다. 시장 예측은 금액(달러)으로 제공됩니다.

지역 분석

북미는 성숙한 광대역 보급률, SVOD의 높은 스태킹, 컨텍스트 광고 기술의 조기 도입으로 2024년 매출의 43%를 차지했습니다. 지역 CDN 노드는 초 이하의 시작 시간을 제공하여 4K 및 돌비 비전의 티어에 대한 지불 의향을 강화하고 있습니다. 그러나 iOS의 CPI 상승은 소규모 스튜디오의 수익성을 위협하고 Android 및 웹 채널에 대한 지출을 촉구합니다. 월마트가 VIZIO의 SmartCast OS를 통합한 것으로 대표되는 바와 같이, 소매 미디어 네트워크의 출현은 데이터가 풍부한 소매업체가 기존 방송사를 우회하고 증가하는 연결된 TV 재고를 브랜드에 직접 판매할 수 있음을 보여줍니다.

아시아태평양은 5G의 대량 도입, 저렴한 Android TV, 지역 언어 큐레이션에 힘입어 CAGR 21%에서 가장 급성장하고 있는 지역입니다. 인도의 클라우드 TV3.0 이니셔티브는 10 방언의 음성 어시스턴트를 추가하여 이전에 케이블 TV에 묶여 있던 시청자를 해제합니다. 중국의 OEM은 상거래 게이트웨이를 겸한 독자적인 TV 운영체제를 사전 로드하여 기기 브랜드에 더 큰 광고 수익 공유를 제공합니다. 한국은 2024년 아시아경기대회 8K 라이브 스트리밍을 5G SA에서 시험적으로 실시해 몰입형 방송 벤치마크를 설정했습니다. 이러한 요인들이 결합되어 지상파 TV에서 IP 전달 서비스로 시청자의 전환이 가속화되고 있습니다.

유럽에서는 기회와 제약이 패치워크처럼 존재합니다. 가처분 소득의 높이가 프리미엄 번들의 보급을 지원합니다. 스칸디나비아 시장에서 광섬유 가구는 평균적으로 두 개의 유료 TV 앱과 하나의 클라우드 게임 경로를 활용합니다. 독일에서의 네트워크 슬라이싱의 시험 운영은 전용 대역폭이 AAA급 클라우드 타이틀의 왕복 20ms를 보증할 수 있음을 증명하고 있지만, 국가별 전리품 규정이 범 EU 전개를 복잡하게 하고 있습니다. 이와 동시에 스위스콤의 보다폰 이탈리아 인수와 같은 국경을 넘어선 M&A는 주파수 대역, 파이버 백본, 스트리밍 권리를 적은 산하로 통합하려는 움직임을 보여주며 보다 광범위한 실적 시너지를 기대할 수 있습니다. 유럽의 넷 제로 커미트먼트는 방송국에 보다 친환경 데이터센터로의 플레이아웃의 마이그레이션을 촉구해, 하이브리드 클라우드로의 마이그레이션을 가속시킬 가능성이 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 서포트

목차

제1장 서론

- 조사의 전제조건과 시장의 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 안정적인 OTT 전달을 가능하게 하는 광섬유 홈의 지속적인 전개

- 북미와 유럽의 농촌 지역에서 5G 고정 무선 액세스의 급속한 확대

- 주요 유료 TV 사업자의 「클라우드 퍼스트」STB로의 전환

- 아시아의 클라우드 TV 솔루션과 커넥티드 TV 칩셋의 OEM 번들

- FAST 채널 수익화 모델이 유럽에서의 퍼블리셔의 도입을 가속

- 중견 사업자의 TCO를 삭감하는 멀티 테넌트 SaaS 플랫폼

- 시장 성장 억제요인

- 신흥 아프리카 및 카리브해 제도에서 단편화된 CDN 실적

- 수익 보장에 영향을 미치는 지속적인 불법 복제 및 자격 증명 공유

- UHD/HDR 컨텐츠의 초기 인코딩/트랜스코딩 비용이 높아

- 기존 CAS/DRM 상호 운용성 격차로 인해 소규모 MSO의 마이그레이션 속도 저하

- 규제 전망

- 기술의 전망

- Five Forces 분석

- 공급기업의 협상력

- 소비자의 협상력

- 신규 참가업체의 위협

- 경쟁 기업간 경쟁 관계

- 대체품의 위협

제5장 시장 규모와 성장 예측

- 전개별

- 퍼블릭 클라우드

- 프라이빗 클라우드

- 하이브리드 클라우드

- 기기 유형별

- 커넥티드 TV

- 휴대폰

- 셋톱 박스(STB)

- 용도별

- 엔터테인먼트 및 미디어

- 통신

- 정보기술

- 소비자용 TV

- 기타 용도

- 기업 규모별

- 대기업

- 중소기업

- 지역별

- 북미

- 미국

- 캐나다

- 남미

- 브라질

- 아르헨티나

- 멕시코

- 기타 라틴아메리카

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 기타 유럽

- 아시아태평양

- 중국

- 일본

- 한국

- 인도

- 호주

- 뉴질랜드

- 기타 아시아태평양

- 중동 및 아프리카

- 아랍에미리트(UAE)

- 사우디아라비아

- 남아프리카

- 기타 중동 및 아프리카

- 북미

제6장 경쟁 구도

- Strategic Developments

- Vendor Positioning Analysis

- 기업 프로파일

- Brightcove Inc.

- Kaltura Inc.

- Ooyala Inc.

- Amino Technologies PLC

- DaCast LLC

- MatrixStream Technologies Inc.

- PCCW Ltd.

- Liberty Global PLC

- Charter Communications(Spectrum)

- Roku Inc.

- Comcast Technology Solutions

- Amazon Web Services

- Google(YouTube TV)

- Apple Inc.(tvOS Services)

- Netflix Inc.

- MUVI LLC

- UpLynk LLC

- Minoto Video Inc.

- Monetize Media Inc.

- Fordela Corp.

- Wowza Media Systems

- Edgecast(Edgio)

- Tencent Cloud

- Huawei Cloud

- Akamai Technologies

제7장 시장 기회와 장래의 전망

SHW 25.11.07The Cloud TV market size is estimated at USD 3.20 billion in 2025 and is forecast to expand to USD 7.47 billion by 2030, reflecting an 18.8% CAGR for 2025-2030.

Surging demand for scalable video workflows, rapid 5G deployment, and telco convergence strategies are propelling adoption. Public cloud deployments still dominate, but hybrid architectures are gaining favour as media companies balance elasticity with broadcast-grade performance. Regulatory fragmentation, semiconductor supply constraints, and rising iOS acquisition costs remain growth headwinds. Intensifying competition between platform operators, device OEMs, and telcos is pushing vendors to differentiate through AI-driven discovery, contextual advertising, and integrated cloud gaming services. Early movers in Asia-Pacific are capturing asymmetric advantages thanks to faster network roll-outs and mass smartphone uptake.

Global Cloud TV Market Trends and Insights

Continued Fiber-to-Home Roll-outs Enabling Stable OTT Delivery

FTTH penetration has surpassed 50% in most developed markets, creating the bandwidth reliability the Cloud TV market needs for unbuffered 4K and 8K streams. Carriers such as AT&T are allocating USD 15 billion through 2025 to extend fiber to 30 million premises, which lowers reliance on costly edge caches and fosters premium live sports streaming. Operators further monetize fiber by bundling unlimited data tiers that remove bitrate ceilings and by leveraging deterministic QoS to support interactive features.

Rapid Expansion of 5G Fixed Wireless Access in Rural North America and Europe

5G FWA provides 100-200 Mbps downlinks at sub-10 millisecond latencies, turning previously underserved rural zones into viable Cloud TV market addresses. Operators, including T-Mobile and Verizon, aim to sign 4-5 million FWA subscribers by 2025, accelerating service reach without multi-year trenching costs. Bundled broadband-plus-TV plans and portable cloud-TV use cases for RV owners further inflate rural demand.

Fragmented CDN Footprint in Emerging Africa and Caribbean Islands

Average in-country latency hits 78 milliseconds across much of Africa versus sub-45 milliseconds in North America, limiting consistent 1080p streaming. Roughly 50% of the region's internet traffic transits foreign upstream providers; outages on West African submarine cables in 2024 crippled 13 nations, highlighting fragility. Without local PoPs, Cloud TV service providers must downshift bitrates, impairing the quality of experience and ad yields.

Other drivers and restraints analyzed in the detailed report include:

- Tier-1 Pay-TV Operators' Shift to Cloud-First STB Replacement

- OEM Bundling of Cloud-TV Solutions with Connected-TV Chipsets in Asia

- Persistent Piracy and Credential-Sharing Impacting Revenue Assurance

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Public cloud held 52% of revenue in 2024, yet hybrid configurations are set to grow at a 21.3% CAGR to 2030 as broadcasters pursue flexible burst capacity alongside predictable QoS. This mix lets rights-holders keep premium sports archives in private clusters while relying on hyperscalers for live-event traffic. The Cloud TV market size for hybrid deployments is projected to accelerate as content owners map workloads to cost curves and exit ageing on-prem encoders. Regulatory-sensitive verticals such as public-sector media have already moved 45% of workflows to hybrid nodes to localise user data. Across use-cases, phased migrations de-risk legacy decommissioning, supporting uninterrupted audience reach during peak seasons.

Hybrid adoption also solves cross-border rights management: operators deploy origin caches in public regions close to diaspora populations while watermarking and DRM logic run in private domains. Vendors have responded with Kubernetes-based transcoders that elastically scale across both footprints. As a result, billing shifts from capex to granular usage, letting mid-tier networks test 4K distribution without buying new ASICs. By 2030, decision frameworks for cloud TV investment will weigh energy efficiency, carbon disclosure, and sovereign-cloud mandates as heavily as bitrate economics.

Connected TVs (CTV) delivered 40% of 2024 revenue, yet smartphones are the fastest-growing end-point with a 23.5% CAGR forecast. Open-RAN 5G plus cheaper OLED panels have blurred the experiential gap so that 4K HDR on a 6.7-inch screen rivals lounge-room sets. Short-form series cut for vertical orientation dominate Gen-Z watchlists, forcing publishers to storyboard concurrently for tall and wide frames. The Cloud TV market share of mobile usage is expected to overtake CTVs in several Southeast Asian countries by 2027, powered by lower data tariffs and instalment-plan handset upgrades.

Multi-device sync is now table-stakes: advertisers use household graph technology to sequence a 15-second teaser on mobile, a 30-second deep-dive on CTV, and a shoppable overlay on tablet within the same evening. Cloud encoder vendors embed SSAI markers that cue dynamic QR codes aligned with active screen size. Such convergence recasts the notion of a primary screen; the winning proposition will offer frictionless hand-off rather than device-specific UX.

Cloud TV Market Report is Segment by Deployment (Public Cloud, Private Cloud, Hybrid Cloud), Device Type (STB, Mobile Phones, Connected TV), Applications (Telecom, Entertainment and Media, and More), Organization Size (Small and Medium Enterprises, Large Enterprises), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America held 43% of 2024 revenue owing to mature broadband penetration, high SVOD stacking, and early adoption of contextual ad tech. Regional CDN nodes deliver sub-second start-up times, reinforcing willingness to pay for 4K and Dolby Vision tiers. Yet elevated iOS CPI threatens smaller studios' profitability, nudging spend toward Android and web channels. The emergence of retail media networks, exemplified by Walmart's integration of VIZIO's SmartCast OS, demonstrates how data-rich retailers can bypass traditional broadcasters and sell incremental connected-TV inventory directly to brands .

Asia-Pacific is the fastest-growing region at a 21% CAGR, propelled by mass 5G roll-out, affordable Android TVs, and regional language curation. India's Cloud TV 3.0 initiative adds voice assistants in 10 dialects, unlocking audiences previously tied to cable. Chinese OEMs preload proprietary TV operating systems that double as commerce gateways, giving device brands a bigger revenue share from advertising. South Korea piloted 8K livestreams of the 2024 Asian Games over 5G SA, setting a benchmark for immersive broadcasting. Collectively, these factors speed viewer migration from terrestrial TV to IP-delivered services.

Europe presents a patchwork of opportunities and constraints. High disposable income supports premium bundle uptake, as seen in Scandinavian markets where fibre households average two paid TV apps plus one cloud gaming pass. Network-slicing pilots in Germany prove that dedicated bandwidth can guarantee 20 ms round-trip for AAA cloud titles, yet country-specific loot-box rules complicate pan-EU launches. At the same time, cross-border M&A such as Swisscom's acquisition of Vodafone Italia signals a drive to consolidate spectrum, fibre backbones, and streaming rights under fewer umbrellas, promising broader footprint synergies swisscom.com. Europe's net-zero commitments are prompting broadcasters to move playout into greener data centres, potentially accelerating hybrid-cloud migrations.

- Brightcove Inc.

- Kaltura Inc.

- Ooyala Inc.

- Amino Technologies PLC

- DaCast LLC

- MatrixStream Technologies Inc.

- PCCW Ltd.

- Liberty Global PLC

- Charter Communications (Spectrum)

- Roku Inc.

- Comcast Technology Solutions

- Amazon Web Services

- Google (YouTube TV)

- Apple Inc. (tvOS Services)

- Netflix Inc.

- MUVI LLC

- UpLynk LLC

- Minoto Video Inc.

- Monetize Media Inc.

- Fordela Corp.

- Wowza Media Systems

- Edgecast (Edgio)

- Tencent Cloud

- Huawei Cloud

- Akamai Technologies

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Continued Fiber-to-Home Roll-outs Enabling Stable OTT Delivery

- 4.2.2 Rapid Expansion of 5G Fixed Wireless Access in Rural North America and Europe

- 4.2.3 Tier-1 Pay-TV Operators' Shift to "Cloud-first" STB Replacement

- 4.2.4 OEM Bundling of Cloud-TV Solutions with Connected-TV Chipsets in Asia

- 4.2.5 FAST Channel Monetisation Models Accelerating Publisher Adoption in Europe

- 4.2.6 Multi-tenant SaaS Platforms Reducing TCO for Mid-tier Operators

- 4.3 Market Restraints

- 4.3.1 Fragmented CDN Footprint in Emerging Africa and Caribbean Islands

- 4.3.2 Persistent Piracy and Credential-Sharing Impacting Revenue Assurance

- 4.3.3 High Initial Encoding/Transcoding Costs for UHD/HDR Content

- 4.3.4 Legacy CAS/DRM Interoperability Gaps Slowing Migration for Small MSOs

- 4.4 Regulatory Outlook

- 4.5 Technological Outlook

- 4.6 Porters Five Forces

- 4.6.1 Bargaining Power of Suppliers

- 4.6.2 Bargaining Power of Consumers

- 4.6.3 Threat of New Entrants

- 4.6.4 Intensity of Competitive Rivalry

- 4.6.5 Threat of Substitute Products

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Deployment

- 5.1.1 Public Cloud

- 5.1.2 Private Cloud

- 5.1.3 Hybrid Cloud

- 5.2 By Device Type

- 5.2.1 Connected TV

- 5.2.2 Mobile Phones

- 5.2.3 Set-Top Box (STB)

- 5.3 By Application

- 5.3.1 Entertainment and Media

- 5.3.2 Telecom

- 5.3.3 Information Technology

- 5.3.4 Consumer Television

- 5.3.5 Other Applications

- 5.4 By Organisation Size

- 5.4.1 Large Enterprise

- 5.4.2 Small and Medium Enterprise

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Mexico

- 5.5.2.4 Rest of Latin America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 South Korea

- 5.5.4.4 India

- 5.5.4.5 Australia

- 5.5.4.6 New Zealand

- 5.5.4.7 Rest of Asia-Pacific

- 5.5.5 Middle East and Africa

- 5.5.5.1 United Arab Emirates

- 5.5.5.2 Saudi Arabia

- 5.5.5.3 South Africa

- 5.5.5.4 Rest of Middle East and Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Strategic Developments

- 6.2 Vendor Positioning Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products and Services, and Recent Developments)

- 6.3.1 Brightcove Inc.

- 6.3.2 Kaltura Inc.

- 6.3.3 Ooyala Inc.

- 6.3.4 Amino Technologies PLC

- 6.3.5 DaCast LLC

- 6.3.6 MatrixStream Technologies Inc.

- 6.3.7 PCCW Ltd.

- 6.3.8 Liberty Global PLC

- 6.3.9 Charter Communications (Spectrum)

- 6.3.10 Roku Inc.

- 6.3.11 Comcast Technology Solutions

- 6.3.12 Amazon Web Services

- 6.3.13 Google (YouTube TV)

- 6.3.14 Apple Inc. (tvOS Services)

- 6.3.15 Netflix Inc.

- 6.3.16 MUVI LLC

- 6.3.17 UpLynk LLC

- 6.3.18 Minoto Video Inc.

- 6.3.19 Monetize Media Inc.

- 6.3.20 Fordela Corp.

- 6.3.21 Wowza Media Systems

- 6.3.22 Edgecast (Edgio)

- 6.3.23 Tencent Cloud

- 6.3.24 Huawei Cloud

- 6.3.25 Akamai Technologies

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment