|

시장보고서

상품코드

1850182

자동차 연료 탱크 시장 : 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Automotive Fuel Tank - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

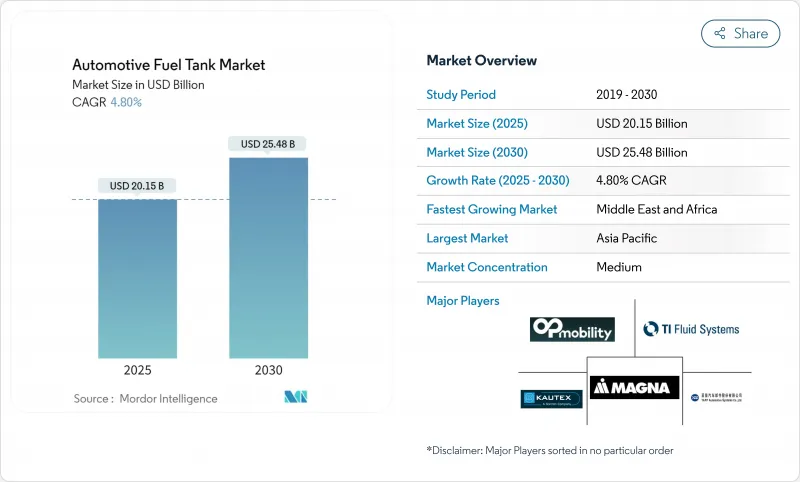

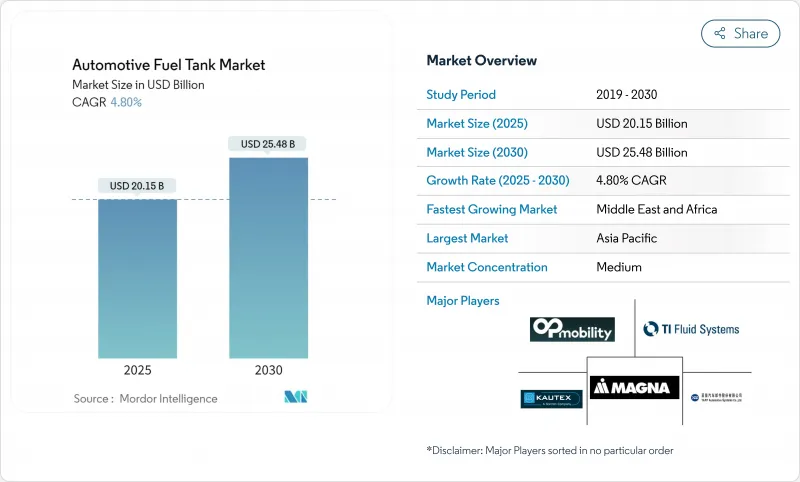

자동차 연료 탱크 시장은 2025년에 201억 5,000만 달러, CAGR 4.80%로 성장하여, 2030년에는 254억 8,000만 달러에 이를 것으로 예측됩니다.

이 확장은 자동차 연료 탱크 시장이 내연 엔진(ICE) 출력의 회복과 기존 탱크의 필요성을 없애는 급속한 전기화의 균형을 어떻게 취하고 있는지를 보여줍니다. 안정성에 대한 수요는 새로운 수소 저장 형식, 고농도 에탄올 혼합을위한 개조, 액체 연료 탱크가 장착된 하이브리드 파워트레인의 새로운 주문에 의해 제공됩니다. 또한 자동차 제조업체는 차량의 질량을 줄이고 온실가스 규제를 충족하며 항속거리를 늘리기 위해 플라스틱 다층 시스템을 선호하고 사용합니다. 복합 탱크에 대한 지속적인 투자로 수소 압력 임계치가 높아지고 배터리 전기자동차의 수가 증가하더라도 공급업체는 장기적인 성장을 이룰 수 있습니다.

세계 자동차 연료 탱크 시장 동향과 통찰

경량 플라스틱 탱크가 CO2 컴플라이언스를 추진

자동차 제조업체는 스틸제에 비해 질량을 최대 40% 삭감할 수 있는 다층 플라스틱 연료 탱크로의 이행을 진행하고 있습니다. 유럽과 미국의 차량 규칙에서 1kg의 경량화는 차량 평균 CO2 배출량의 구체적인 개선으로 이어졌으며, 플랫폼 전체의 플라스틱으로의 재조달을 촉진하고 있습니다. 또한 Kautex Textron의 Green 프로그램과 같은 이니셔티브는 재활용 및 바이오 수지를 추구하여 원형 경제의 목표를 달성했습니다. OEM이 경량화의 메리트와 가격 규율을 저울에 걸치고 있는 코스트 의식이 높은 아시아에서도, 채택이 진행되고 있습니다. 이러한 움직임은 플라스틱 탱크 전업 제조업체에게 옛 금속 탱크 공급 기업의 협상력보다 큰 힘을 주고 있습니다.

ICE와 하이브리드 생산 회복이 수요를 뒷받침

2024년 세계 ICE와 하이브리드 생산량이 증가하고 폭스바겐 그룹은 7,920만 대의 소형 상용차와 790만 대의 소형 상용차를 추적하고 있습니다. 마일드 하이브리드 드라이브 트레인에는 여전히 액체 연료 저장소가 필요하며, 여분의 배터리 패키징을 장착하기 위해 맞춤형 모양을 채택하는 경우가 많습니다. 아시아태평양의 공장은 팬데믹에 의한 조업 정지를 거쳐 가동률이 상승하고 자동차 연료 탱크 시장 전체의 단기 수요를 끌어올리고 있습니다. 그러나 공급업체는 원재료 상승과 칩 부족으로 인한 마진 압박을 해결해야 합니다.

전동화가 기존의 연료 탱크 수요를 촉발

북미만으로도 2025년부터 2030년에 걸쳐 배터리 일렉트릭의 점유율이 크게 도약해 수백만개의 기존 탱크가 철거됩니다. ICE 프로그램은 투자 우선순위를 잃고 프리미엄 브랜드는 가장 수익성이 높은 탱크 계약을 선호하여 순수한 전기자동차로 신속하게 전환합니다. 일부 블로우 성형 제조업체는 생산 능력을 줄이기 위해 생산 능력을 멈추고 배터리 인클로저로 다각화하기 시작했습니다.

부문 분석

45-70리터의 대역이 2024년에 44.59%의 점유율을 차지해 자동차 연료 탱크 시장의 중심인 세계의 B부문와 C부문의 승용차의 대부분에 적합하고 있습니다. OEM 플랫폼 사이클이 이 크기 창을 예측 수평의 깊이까지 고정하므로 안정적인 수량이 지속됩니다. 그러나 70리터 이상의 탱크는 CAGR 11.53%로 성장하여 이 클래스의 자동차 연료 탱크 시장 규모는 2030년까지 확대합니다. 장거리 트럭, 대형 SUV, 높은 차재 에너지의 혜택을 받는 수소 프로토타입이 성장을 견인합니다. 군용 차량은 항속 거리를 늘리기 위해 100 리터 이상의 보조 셀을 조달하여 전방 지역의 물류 위험을 줄입니다. 컴포지트 오버랩 실린더는 이전 금속 탱크보다 무게가 15-20% 가벼워져 수소 서비스의 부피 페널티를 부분적으로 상쇄합니다. 자동 섬유 배치를 활용하는 공급업체는 기존 필라멘트 와인딩보다 빠르게 생산 규모를 확대할 수 있어 비용면에서 우위를 차지하며 70리터 이상의 카테고리에서 점유율 확대를 강화하고 있습니다.

45리터 이하의 제품 범위는 바닥 패키징이 엄격하고 비용 제한을 위해 복잡한 모양과 소재가 존경받는 컴팩트한 시티카용입니다. 가격에 민감한 신흥 시장에서는 수량은 안정되어 있지만, 전동화와 라이드헤일의 채택이 상승을 억제하고 있습니다. 공급업체는 공통 캐리어 브래킷을 갖춘 모듈식 플라스틱 설계를 제공함으로써 프로그램 간 표준화 및 동질화 단축을 도모하고 익스포저를 헤지합니다. 향후 예측에서는 중급 차종의 용량이 여전히 최대이지만 수익이 대형 차종의 틈새 시장에 치우쳐 선진 소재가 더 높은 단가를 요구합니다.

플라스틱 다층 구조는 20년에 걸쳐 입증된 기밀성, 낮은 금형 비용, 기하학적 자유도를 반영하여 2024년에는 43.29%의 매출을 확보했습니다. 에틸렌·비닐알코올 등의 배리어 수지가 HDPE층 사이에 배치되어 탄화수소를 차단함으로써 금속에 의존하지 않고 유로 7의 투과 기준을 충족할 수 있습니다. 일부 헤비 듀티 및 오프로드 프로그램은 내 덴트성과 현장 수리성이 무게보다 우선하기 때문에 고전적인 강철을 사용합니다. 알루미늄은 스타일링과 무게가 교차하는 프리미엄 스포츠카를 위한 좁은 틈새를 채우고 있지만 공급에는 제약이 있습니다.

복합수소탱크는 한국, 일본, 유럽, 캘리포니아의 연료전지 전기차에 밀려 CAGR 10.53%로 가장 빠른 상승을 보였습니다. 유형 IV 설계에서는 폴리머 라이너와 탄소섬유 랩이 결합되어 700bar의 사용 압력을 견딜 수 있습니다. Quantum Fuel Systems와 OneH2는 최근 27kg의 수소를 저장하는 930 기압의 실린더를 검증하여 에너지 밀도 향상의 여지가 있음을 밝혔습니다. 자동화된 섬유 배치는 반복 가능한 레이업을 가능하게 하고, 스크랩을 감소시키고, 복합재료는 대량 생산 프로그램에서 금속과 동등한 비용에 접근합니다. 곧 탄소섬유와 라이너 압출 성형의 학습 속도 곡선이 재료 프리미엄을 낮추고 자동차 연료 탱크 시장 내 점유율이 재구성 될 것으로 예측됩니다.

자동차 연료 탱크 시장은 용량(45리터 미만, 45-70리터, 70리터 이상), 재료 유형(플라스틱-단층, 플라스틱-다층/배리어, 기타), 차량 유형(승용차, 소형 상용차, 중형/대형 상용차, 기타), 연료 유형(가솔린, 디젤, 기타), 지역별로 구분 시장 예측은 금액(달러)과 수량(단위)으로 제공됩니다.

지역별 분석

아시아태평양은 2024년 매출의 53.76%를 차지하며 중국과 인도의 치밀한 공급망, 경쟁력 있는 노동력, 지원적인 재정 인센티브에 지지되고 있습니다. 중국 본토는 ICE 판매량과 2세대 연료전지 조종사가 섞여 있기 때문에 공급업체는 철강, 플라스틱, 복합재의 라인을 통해 점유율을 지켜야 합니다. 인도의 생산 연동 인센티브 제도는 신규 투자를 유치하고 비용 규율을 강화함으로써 자동차 연료 탱크 시장을 위한 높은 처리량 플라스틱 블로우 성형 셀을 우월하게 합니다. ASEAN 국가 간의 정합화는 국경을 넘어서는 부품의 흐름을 완화하고 이 지역의 허브로서의 지위를 더욱 확립합니다.

중동 및 아프리카는 CAGR 10.34%로 가장 급성장하는 클러스터로, 전자상거래와 건설과 관련된 경제의 다양화와 물류 확대로 혜택을 누리고 있습니다. 사우디아라비아의 '비전 2030' 장려책이 트럭 차량 업데이트에 박차를 가해 사막 기후에 최적화된 대형 이중 탱크 및 보조 금속 유닛의 수주가 증가합니다. 모로코와 이집트에서는 현지 조립 노력이 점차 리드 타임을 단축하고 Tier1 기업이 미래의 자동차 연료 탱크 시장에서 점유율을 확보하기 위해 플라스틱 블로우 성형 셀의 니어 쇼어링을 검토하게 됩니다.

북미는 여전히 기술이 풍부합니다. 가솔린의 3차 기준, 인플레이션 억제법(Inflation Reduction Act)에 의한 바이오연료에 대한 자금 공급, 캘리포니아 주와 텍사스 주 주변의 급성장 중인 수소 회랑은 모두 제품의 로드맵을 형성하고 있습니다. 픽업 트럭의 높은 보급률은 대형 스틸 탱크와 플라스틱 탱크를 지원하지만 일부 주에서 BEV 의무화는 장기적으로 분명히 역풍이됩니다. 유럽은 유로 7과 탄소 가격 제도에서 규제 강화를 이끌고 있습니다. 이 지역의 OEM R&D 센터는 향후 세계화할 차세대 투과 장벽과 증기 회수 컨셉을 테스트하고 있으며, 판매량 부진에도 불구하고 초기 단계 검증에서 이 지역의 가치를 높이고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 서포트

목차

제1장 서론

- 조사의 전제조건과 시장의 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 함대 전체의 CO2 배출량 규제에 적합한 경량 플라스틱 탱크

- 세계의 내연 기관차 및 하이브리드차 생산의 회복

- 보다 엄격한 LEV III/Euro 7 증발 가스 배출 제한

- 장벽 탱크 개조를 위한 플렉스 연료(E20-E85) 롤아웃

- 신흥의 수소 ICE 트럭용 고압 복합 탱크

- 오프로드 및 방어에 있어서의 장거리 보조 금속 탱크 수요

- 시장 성장 억제요인

- 급속한 전동화에 의해 ICE 대응 가능량이 감소

- HDPE와 알루미늄의 비용 변동이 Tier 1의 이익률을 압박

- HDPE 탱크내의 고에탄올 혼합물의 화재 안전성의 우려

- 탱크리스 스케이트 보드형 BEV 플랫폼이 OEM의 설비 투자를 압박

- 가치/공급망 분석

- 규제 상황

- 기술의 전망

- Porter's Five Forces

- 신규 참가업체의 위협

- 구매자의 협상력

- 공급기업의 협상력

- 대체품의 위협

- 경쟁 기업간 경쟁 관계

제5장 시장 규모와 성장 예측

- 용량별

- 45L 미만

- 45-70L

- 70L 이상

- 소재 유형별

- 플라스틱 - 단층

- 플라스틱 - 다층/장벽

- 알루미늄

- 강철

- 차량 유형별

- 승용차

- 소형 상용차

- 중형 및 대형 상용차

- 버스와 장거리 버스

- 연료유형별

- 가솔린

- 디젤

- 플렉스 연료/에탄올 혼합 연료

- 수소

- CNG와 LPG

- 지역별

- 북미

- 미국

- 캐나다

- 기타 북미

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 러시아

- 기타 유럽

- 아시아태평양

- 중국

- 인도

- 일본

- 한국

- 기타 아시아태평양

- 중동 및 아프리카

- 사우디아라비아

- 아랍에미리트(UAE)

- 이집트

- 튀르키예

- 남아프리카

- 기타 중동 및 아프리카

- 북미

제6장 경쟁 구도

- 시장 집중도

- 전략적 동향

- 시장 점유율 분석

- 기업 프로파일

- Magna International Inc.

- Compagnie Plastic Omnium SE

- TI Fluid Systems plc

- Kautex Textron GmbH and Co. KG

- YAPP Automotive Systems Co. Ltd

- Fuel Total Systems Co. Ltd

- Sakamoto Industry Co. Ltd

- Yachiyo Industry Co. Ltd

- SRD Holdings Ltd

- Donghee Industrial Co. Ltd

- Continental AG

- Forvia(Faurecia Hydrogen Solutions)

- Hexagon Composites ASA

- Lumax Industries Ltd

- Cangzhou Mingzhu Plastic Co. Ltd

- Unipres Corporation

- SKH Metals Ltd

- AIA Engineering

- MFG USA

제7장 시장 기회와 장래의 전망

SHW 25.11.07The automotive fuel tank market reached USD 20.15 billion in 2025 and is forecast to climb to USD 25.48 billion by 2030, reflecting a 4.80% CAGR.

This expansion shows how the automotive fuel tank market balances a rebound in internal-combustion-engine (ICE) output with fast-rising electrification that removes the need for conventional tanks. Demand for stability comes from new hydrogen storage formats, retrofits for higher ethanol blends, and fresh orders from hybrid powertrains that still carry a liquid-fuel tank. Automakers also favor plastic multi-layer systems to cut vehicle mass, meet greenhouse-gas rules, and extend range. Ongoing investments in composite tanks unlock higher pressure thresholds for hydrogen, positioning suppliers for longer-term growth even as battery-electric volumes scale up.

Global Automotive Fuel Tank Market Trends and Insights

Lightweight Plastic Tanks Drive CO2 Compliance

Automakers are shifting to multi-layer plastic fuel tanks that cut mass by up to 40% versus steel. European and United States fleet rules link every kilogram saved to tangible fleet-average CO2 improvements, prompting platform-wide re-sourcing toward plastics. Barrier designs now meet lifetime permeation and crash targets, while efforts such as Kautex Textron's Green+ program pursue recycled or bio-based resins to hit circular-economy goals. Uptake is also strong in cost-aware Asia, where OEMs weigh lightweighting benefits against pricing discipline. This dynamic gives specialized plastic-tank makers greater bargaining power over older metal-tank suppliers.

ICE and Hybrid Production Recovery Fuels Demand

Global ICE and hybrid builds climbed in 2024, with Volkswagen Group tracking 79.2 million light vehicles plus 7.9 million light commercial units. Mild-hybrid drivetrains still require a liquid-fuel reservoir and often adopt bespoke shapes to fit extra battery packaging, which lifts average revenue per unit. Asia-Pacific plants run at higher utilization after pandemic shutdowns, lifting short-term demand across the automotive fuel tank market. Suppliers must, however, navigate raw-material inflation and chip shortages that compress margins.

Electrification Erodes Traditional Fuel Tank Demand

Battery-electric share in North America alone is set to take a significant leap from 2025 to 2030, removing millions of conventional tanks. ICE programs lose investment priority, and premium brands migrate swiftly to pure electric, hitting the most profitable tank contracts first. Some blow-molders have begun shuttering capacity and diversifying into battery enclosures to offset shrinking volumes.

Other drivers and restraints analyzed in the detailed report include:

- Euro 7 Regulations Tighten Evaporative Standards

- Flex-Fuel Infrastructure Drives Barrier-Tank Adoption

- Raw Material Cost Volatility Pressures Margins

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

The 45-70 liter band dominated 2024 with a 44.59% share as it fits most global B- and C-segment passenger cars, the heart of the automotive fuel tank market. Steady volumes persist because OEM platform cycles lock this size window deep into the forecast horizon. Yet tanks above 70 liters advance at 11.53% CAGR, lifting this class's automotive fuel tank market size through 2030. Growth traces to long-haul trucks, large SUVs, and hydrogen prototypes benefitting from higher onboard energy. Military fleets procure auxiliary cells exceeding 100 liters to extend operational range, mitigating forward-area logistics risk. Composite over-wrapped cylinders now weigh 15-20% less than earlier metal tanks, partially offsetting volume penalties in hydrogen service. Suppliers that master automated fiber placement can scale production faster than traditional filament winding, holding a cost edge, reinforcing share gains in the more than 70-liter category.

The sub-45-liter range caters to compact city cars where tight under-floor packaging and cost limits dissuade complex shapes or materials. Volume remains stable in price-sensitive emerging markets, but electrification and ride-hail adoption curb upside. Suppliers hedge exposure by offering modular plastic designs with common carrier brackets to standardize across programs and shorten homologation. Over the forecast, mid-range capacities remain the largest pool, yet revenue skews toward big-tank niches where advanced materials command higher unit pricing within the broader automotive fuel tank market.

Plastic multi-layer constructions secured 43.29% revenue in 2024, reflecting two decades of proven leak-tightness, lower tooling cost, and geometric freedom. Barrier resins such as ethylene vinyl alcohol sit between HDPE layers to block hydrocarbons, allowing compliance with Euro 7 permeation norms without resorting to metal. Classic steel persists in some heavy-duty and off-road programs where dent resistance and field repairability trump weight. Aluminium fills a narrow niche for premium sports cars where styling and weight intersect, but remains supply-constrained.

Composite hydrogen tanks show the fastest climb at 10.53% CAGR, propelled by fuel-cell electric pushes in Korea, Japan, Europe, and California. Type IV designs pair polymer liners with carbon-fiber wrap to withstand 700-bar service pressure, giving a 5-to-1 strength-to-weight edge over steel. Quantum Fuel Systems and OneH2 recently validated a 930-bar cylinder that stores 27 kg of hydrogen, underscoring headroom for energy density gains. Automated fiber placement now yields repeatable lay-ups and lowers scrap, inching composites closer to cost parity with metal for high-volume programs. Over time, learning-rate curves in carbon fiber and liner extrusion are expected to erode material premiums, reshaping share within the automotive fuel tank market

The Automotive Fuel Tank Market is Segmented by Capacity (Less Than 45 Liters, 45-70 Liters, Above 70 Liters), Material Type (Plastic - Single Layer, Plastic - Multi-Layer / Barrier, and More), Vehicle Type (Passenger Cars, Light Commercial Vehicles, Medium and Heavy Commercial Vehicles, and More), Fuel Type (Gasoline, Diesel, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD) and Volume (Units).

Geography Analysis

Asia-Pacific claimed 53.76% of revenue during 2024, supported by China's and India's dense supply chains, competitive labor, and supportive fiscal incentives. Mainland China blends strong ICE volumes with second-generation fuel-cell pilots, so suppliers must straddle steel, plastic, and composite lines to defend their share. India's Production Linked Incentive scheme attracts new investments and enforces cost discipline that favors high-throughput plastic blow-molding cells for the automotive fuel tank market. Association harmonization between ASEAN nations eases cross-border component flow, further entrenching the region's hub status.

Middle East and Africa, the fastest-growing cluster at 10.34% CAGR, benefit from economic diversification and logistics expansions tied to e-commerce and construction. Saudi Arabia's Vision 2030 incentives spur truck fleet renewals, which lift orders for large dual tanks and auxiliary metal units optimized for desert climates. Local assembly initiatives in Morocco and Egypt gradually shorten lead times, prompting tier-1s to consider near-shoring plastic blow-molding cells to secure their future share in the automotive fuel tank market.

North America remains technology-rich: Tier 3 gasoline standards, Inflation Reduction Act biofuel funding, and fast-growing hydrogen corridors around California and Texas all shape product roadmaps. High pickup-truck penetration supports large steel and plastic tanks, yet BEV mandates in several states are a clear long-term headwind. Europe leads regulatory stringency with Euro 7 and carbon-pricing schemes. OEM R&D centers here test next-generation permeation-barrier and vapor-recovery concepts that later globalize, reinforcing the region's value in early-stage validation despite softer volumes.

- Magna International Inc.

- Compagnie Plastic Omnium SE

- TI Fluid Systems plc

- Kautex Textron GmbH and Co. KG

- YAPP Automotive Systems Co. Ltd

- Fuel Total Systems Co. Ltd

- Sakamoto Industry Co. Ltd

- Yachiyo Industry Co. Ltd

- SRD Holdings Ltd

- Donghee Industrial Co. Ltd

- Continental AG

- Forvia (Faurecia Hydrogen Solutions)

- Hexagon Composites ASA

- Lumax Industries Ltd

- Cangzhou Mingzhu Plastic Co. Ltd

- Unipres Corporation

- SKH Metals Ltd

- AIA Engineering

- MFG USA

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Lightweight plastic tanks for fleet-wide CO? compliance

- 4.2.2 Rebound in global ICE and hybrid vehicle production

- 4.2.3 Stricter LEV III / Euro 7 evaporative-emission limits

- 4.2.4 Flex-fuel (E20-E85) roll-outs driving barrier-tank retrofits

- 4.2.5 High-pressure composite tanks for emerging hydrogen ICE trucks

- 4.2.6 Off-road and defence demand for long-range auxiliary metal tanks

- 4.3 Market Restraints

- 4.3.1 Rapid electrification reducing addressable ICE volume

- 4.3.2 HDPE and aluminium cost volatility squeezing tier-1 margins

- 4.3.3 Fire-safety concerns with high-ethanol blends in HDPE tanks

- 4.3.4 Tank-less skateboard BEV platforms eroding OEM CAPEX

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 Market Size and Growth Forecasts (Value)

- 5.1 By Capacity

- 5.1.1 Less than 45 L

- 5.1.2 45 - 70 L

- 5.1.3 Above 70 L

- 5.2 By Material Type

- 5.2.1 Plastic - single-layer

- 5.2.2 Plastic - multi-layer / barrier

- 5.2.3 Aluminium

- 5.2.4 Steel

- 5.3 By Vehicle Type

- 5.3.1 Passenger Cars

- 5.3.2 Light Commercial Vehicles

- 5.3.3 Medium and Heavy Commercial Vehicles

- 5.3.4 Buses and Coaches

- 5.4 By Fuel Type

- 5.4.1 Gasoline

- 5.4.2 Diesel

- 5.4.3 Flex-fuel / Ethanol blends

- 5.4.4 Hydrogen

- 5.4.5 CNG and LPG

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Rest of North America

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Russia

- 5.5.3.7 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 India

- 5.5.4.3 Japan

- 5.5.4.4 South Korea

- 5.5.4.5 Rest of Asia-Pacific

- 5.5.5 Middle East and Africa

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 United Arab Emirates

- 5.5.5.3 Egypt

- 5.5.5.4 Turkey

- 5.5.5.5 South Africa

- 5.5.5.6 Rest of Middle East and Africa

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global level Overview, Market level overview, Core Segments, Financials, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Magna International Inc.

- 6.4.2 Compagnie Plastic Omnium SE

- 6.4.3 TI Fluid Systems plc

- 6.4.4 Kautex Textron GmbH and Co. KG

- 6.4.5 YAPP Automotive Systems Co. Ltd

- 6.4.6 Fuel Total Systems Co. Ltd

- 6.4.7 Sakamoto Industry Co. Ltd

- 6.4.8 Yachiyo Industry Co. Ltd

- 6.4.9 SRD Holdings Ltd

- 6.4.10 Donghee Industrial Co. Ltd

- 6.4.11 Continental AG

- 6.4.12 Forvia (Faurecia Hydrogen Solutions)

- 6.4.13 Hexagon Composites ASA

- 6.4.14 Lumax Industries Ltd

- 6.4.15 Cangzhou Mingzhu Plastic Co. Ltd

- 6.4.16 Unipres Corporation

- 6.4.17 SKH Metals Ltd

- 6.4.18 AIA Engineering

- 6.4.19 MFG USA

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-need Assessment