|

시장보고서

상품코드

1850185

모듈식 실험실 자동화 시장 : 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Modular Laboratory Automation - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

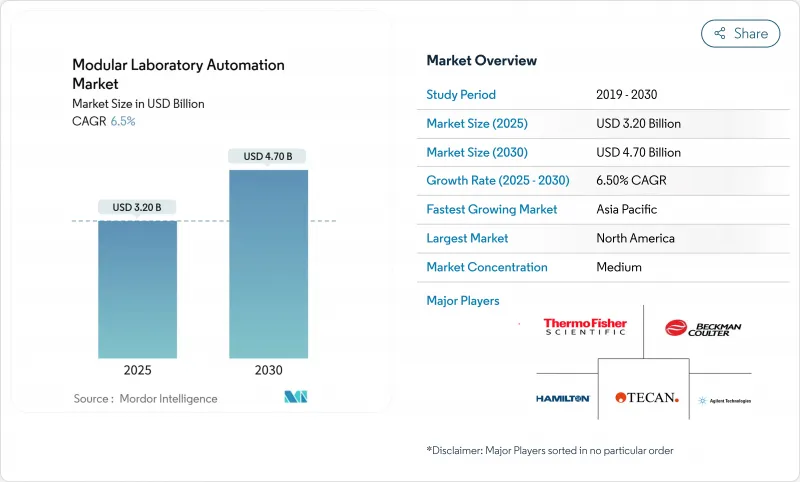

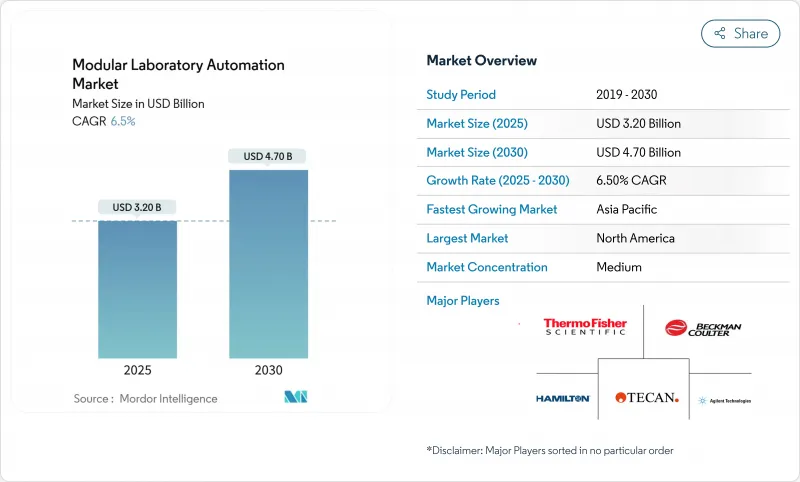

모듈식 실험실 자동화 시장 규모는 2025년에 32억 달러, 2030년에는 47억 달러로 확대될 것으로 예측됩니다.

규제 당국의 모니터링 강화, 실험실 노동력 감소, 재현 가능한 데이터에 대한 요구가 증가함에 따라 자동화된 네트워크 지원 워크셀이 생명 과학 혁신을 위한 중요한 인프라로 자리매김하고 있습니다. 공급업체는 현재 인공지능 소프트웨어와 로봇 공학을 번들로 제공하고, 실험실이 프로토콜을 표준화하고, 완전한 감사 추적을 얻고, 테스트 주기를 단축할 수 있습니다. 제약 제조업체는 EU의 GMP 부속서 1의 오염 관리 요구 사항을 충족하기 위해 도입을 가속화하고 있으며, 병원 네트워크는 장기 건설 프로젝트 없이 분산 검사를 확장하는 모듈식 도입을 지원합니다. 병행하여, NIH MATChS 프로그램과 같은 연방 정부의 지원은 실험실 자동화가 더 이상 재량적이지 않고 생물 의학 연구를 위한 전략적인 지원자임을 시사합니다.

세계 모듈식 실험실 자동화 시장 동향 및 통찰

반복성과 데이터 무결성에 대한 요구 증가

자동화된 플랫폼은 엄격한 공정 제어를 부과하여 수작업이 자주 발생하는 편차를 줄입니다. 메이요 클리닉의 정렬 시스템은 시간당 6,000개의 튜브를 미스 정렬 없이 이동시켜 불량품 제로의 데이터 취득을 입증하고 있습니다. 이러한 결과는 규제 당국이 모든 분석에 대해 상세한 감사 추적을 요구하는 데 필수적입니다. 여러 시설의 컨소시엄에서는 표준화된 로봇 워크플로우를 사용하여 결과를 확실히 비교하고 협동 연구를 뒷받침하고 있습니다. 공급업체는 원시 데이터를 보호하기 위해 블록체인 지원 로그를 통합합니다. 이러한 기능은 규제 당국에 증거를 제출할 때 실험실의 신뢰성을 향상시킵니다.

생명 과학 연구소의 만성 기술 노동자 부족

북미 전역에서 2만 5,000명 가까운 결원으로 실험실은 과학자가 해석에 집중하는 동안 반복 작업을 기계에 재할당하는 자동화를 향하고 있습니다. 클라라파스의 로봇 마이크로 토미는 한 기술자가 여러 슬라이드 플립 스테이션을 감독할 수 있게 하여 생산 능력을 3배로 늘립니다. 이러한 노동 배증의 이점은 검사 백로그를 단축하고 시간외 할증 없이 24시간 365일의 운영을 지원합니다. 자동화는 또한 프로토콜을 소프트웨어로 인코딩하여 암시적 지식을 제도화하고 신입 사원의 수락 시간을 단축합니다. 퇴직률이 상승함에 따라 모듈식 실험실 자동화 시장에 대한 투자의 경제적 합리성은 더욱 높아지고 있습니다.

높은 초기 투자와 긴 투자 회수 사이클

엔트리 레벨 로봇 벤치는 10만-30만 달러, 전체 라인은 100만 달러를 넘어 대학과 중견기업의 예산을 압박하고 있습니다. 오류가 없는 데이터나 직원 재배치 등의 이점이 단순한 수익화로 이어지지 않기 때문에 투자 회수는 3년을 넘는 경우가 많습니다. 리스 방식이나 사용량에 따른 가격 설정에 의해 부분적으로는 장벽이 낮아지는 것, 보수 계약, 검증, 오퍼레이터 트레이닝은 여전히 총 소유 비용을 상승시킵니다. 따라서 재무위원회는 단계적으로 투자를 수행하고 각 기지가 단계적으로 용량을 강화할 수 있도록 하는 모듈식 실험실 자동화 시장 접근법을 선호합니다.

부문 분석

자동 리퀴드 핸들러는 2024년 모듈식 실험실 자동화 시장 규모의 26.41%를 차지하여 분석 준비의 핵심 역할을 확고히 하고 있습니다. 정확한 피펫팅이 다운스트림 데이터 품질을 보장하는 동시에 직원이 분석 작업에 전념할 수 있기 때문에 실험실에서는 이러한 플랫폼을 선호합니다. 갑판 레이아웃을 최적화하고 칩 소비를 예측하는 통합 소프트웨어에 대한 수요가 증가하고 있으며 소모품 낭비와 예기치 않은 다운 타임을 줄입니다. CAGR7.21%를 보일 것으로 예측되는 자동 저장 및 검색 시스템은 샘플을 저스트 인 타임으로 워크셀에 공급함으로써 샘플 보관이라는 만성적인 과제를 해결합니다. 공급업체는 현재 저온 창고와 AI 경로 계획을 결합하여 냉동 용융 이벤트를 최소화하고 생체분자의 무결성을 보호하고 있습니다.

소프트웨어 혁신은 공급업체가 분석 실패가 전파되기 전에 이상을 알리는 머신러닝 알고리즘을 통합하여 경쟁사와 차별화를 형성합니다. Thermo Fisher의 Vulcan 플랫폼은 로봇 암과 자체 조정 워크플로우를 결합하여 처리량이 어떻게 향상되는지 보여줍니다. 인라인 질량 분석 또는 형광 검출이 가능한 분석 장치는 총 턴어라운드 시간을 단축하여 실험실이 며칠에 걸친 프로토콜을 한 시프트로 응축할 수 있도록 합니다. 순 효과는 단일 목적 박스보다 오히려 일관된 에코시스템에 대한 수요의 구조적 증가이며, 하드웨어와 데이터를 하나의 유리로 오케스트레이션하는 모듈식 실험실 자동화 시장의 에코시스템을 중시하는 공급자의 자세를 강화하고 있습니다.

임상 진단은 2024년에 28.50%의 매출에 기여하고, 대량의 화학물질과 재현성이 높은 자동화에 보답하는 엄격한 인정 기준에 지지되고 있습니다. 병원의 실험실은 컨베이어 링크 된 작업 셀과 검증된 결과를 전자 의료 기록에 직접 게시하는 미들웨어를 통합하여 환자의 치료주기를 단축합니다. CAGR 예측 9.66%의 세포 및 유전자 치료 워크플로우는 장기간 배양 중 오염 위험을 최소화하는 폐쇄 시스템 로봇이 필요합니다. 환경 센서와 AI 분류기를 탑재한 로봇은 서브 미크론의 청정도를 유지하며 수백만 달러의 비용이 드는 배치 불량을 방지합니다.

의약품 그룹은 1,536개의 웰 플레이트에서 높은 처리량 스크린을 지속적으로 확장하고 유전체학 컨소시아는 집단 코호트의 라이브러리 준비를 자동화합니다. 단백질체학은 실험실이 샘플 소화와 LC-MS 로딩을 자동화함에 따라 상승하고 있습니다. 시약 진단 프로토콜을 지원하는 크로스 디시프리너리 플랫폼은 진단, 탐구 및 제조 작업 간의 용량을 조정할 수 있기 때문에 인기를 끌고 있습니다. 이러한 범용성은 모듈식 실험실 자동화 시장에 대한 투자를 강화하고 있습니다.

모듈식 실험실 자동화 시장은 장비 및 소프트웨어(자동 리퀴드 핸들러, 자동 플레이트 핸들러 등), 응용 분야(약물발견, 유전체 등), 최종 사용자(제약회사, 바이오테크놀러지 회사 등), 자동화 유형(독립형 기기 자동화, 모듈형 워크셀 등), 지역별로 구분되어 있습니다. 시장 예측은 금액(달러)으로 제공됩니다.

지역 분석

북미는 2024년 41.70%의 매출 점유율을 유지했습니다. 바이오 의약품 본사의 집중, NIH의 두꺼운 자금 지원, 기술 투자에 유리한 성숙한 규제 환경을 반영합니다. 215만 달러의 MATChS 상과 같은 최근 연방 보조금은 지능형 자동화에 대한 공공 부문의 지지를 뒷받침합니다. Tier-1 병원은 분산형 작업 셀을 통합하고 시료 처리를 환자 수용에 가깝게 하여 물류 지연을 줄입니다. 캐나다의 생명 과학 클러스터는 주세 공제를 활용하여 연구 인프라를 업그레이드하고 있지만 인력 부족은 여전히 심각합니다. 무균주사제의 수출인정을 목표로 하는 멕시코는 부속서 1의 요건을 충족하고 제조위탁계약을 확보하기 위해 로봇 아이솔레이터를 시험적으로 도입하고 있습니다.

아시아태평양은 정부가 생명 공학 인프라에 보조금을 내고 선진 치료제의 현지 생산을 장려하고 있기 때문에 가장 높은 성장률을 보이고 있습니다. 중국은 완전히 자동화된 폐쇄 루프 파이프라인을 채택한 국가 시퀀싱 허브에 투자하여 유전체당 비용을 절감하고 정밀의료 파일럿 프로그램을 가속화하고 있습니다. 고령화가 진행되는 일본에서는 만성질환 패널을 다룰 수 있는 진단 자동화에 대한 수요가 높아집니다. 인도의 위탁제조부문은 세계적인 무균 기준에 준거한 모듈식 아이솔레이터를 도입하여 국내 공장을 규제시장용 수출에 위치시킵니다. 한국은 복잡한 생물제제를 보다 신속하게 시장에 투입하기 위해 듀얼암 로봇과 AI 분석을 조합한 세포치료센터 오브 엑설런스에 주력하고 있습니다. 이러한 노력은 이 지역 전체의 모듈식 실험실 자동화 시장의 지속적인 수요를 지원합니다.

유럽은 여전히 매우 중요한 시장이지만, 그 이유는 부속서 1이 로봇 공학에 유리한 기술적 장벽을 철폐하고 기존의 충전 마감 라인의 업그레이드를 촉진하기 때문입니다. 독일의 엔지니어링 거점은 고정밀 메카트로닉스와 클라우드 네이티브 MES 플랫폼을 통합하고 영국은 연구 자금을 대학과 병원의 파트너십에 돌려 AI 지향 워크셀을 검증하고 있습니다. 프랑스는 선행 투자를 상쇄하는 자극책을 통해 공공 부문의 실험실을 현대화합니다. 이탈리아와 스페인은 수혈 과오를 억제하기 위해 혈액은행 업무에서 검사실 전체의 자동화를 우선합니다. 유럽 경제권의 규제 공통성은 국경을 넘어선 표준화를 촉진하고 공급업체에 통일된 검증 패키지를 제공함으로써 모듈식 실험실 자동화 시장 내 여러 사이트에서 조달을 가속화합니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월의 애널리스트 서포트

목차

제1장 서론

- 조사의 전제조건과 시장의 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 재현성과 데이터 무결성의 필요성 증가

- 생명과학연구실에서 만성적인 숙련노동자 부족

- 높은 처리량 유전체학 및 세포 치료 파이프라인

- EU GMP Annex 1의 오염 관리 의무에 의해 로봇 공학이 가속(보고 부족)

- 시장 성장 억제요인

- 고액의 초기 투자와 긴 ROI 사이클

- 기존 기기와 LIMS의 통합 복잡성

- 가치/공급망 분석

- 규제 상황

- 기술의 전망

- Porter's Five Forces 분석

- 공급기업의 협상력

- 구매자의 협상력

- 신규 참가업체의 위협

- 대체품의 위협

- 경쟁 기업간 경쟁 관계

제5장 시장 규모와 성장 예측

- 기기와 소프트웨어별

- 자동 액체 핸들러

- 자동 플레이트 핸들러

- 로봇 암

- 자동 창고 시스템(ASRS)

- 분석기

- 소프트웨어

- 용도 분야별

- 약물발견

- 유전체학

- 단백질체학

- 임상 진단

- 기타 용도

- 최종 사용자별

- 제약 및 생명 공학 기업

- 학술연구기관

- 임상 및 진단실험실

- 계약연구기관

- 식품 및 환경 시험 실험실

- 자동화 유형별

- 독립형 기기 자동화

- 모듈러 워크셀

- 통합 워크셀

- Total Lab Automation(TLA) 라인

- 모바일/클라우드 접속 로봇

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 유럽

- 영국

- 독일

- 프랑스

- 이탈리아

- 러시아

- 기타 유럽

- 아시아태평양

- 중국

- 일본

- 인도

- 한국

- 기타 아시아태평양

- 중동

- 이스라엘

- 사우디아라비아

- 아랍에미리트(UAE)

- 튀르키예

- 기타 중동

- 아프리카

- 남아프리카

- 이집트

- 기타 아프리카

- 북미

제6장 경쟁 구도

- 시장 집중도

- 전략적 동향

- 시장 점유율 분석

- 기업 프로파일

- Thermo Fisher Scientific

- Danaher Corporation(Beckman Coulter)

- Tecan Group AG

- Agilent Technologies

- PerkinElmer Inc.

- Siemens Healthineers

- Becton Dickinson(BD)

- Hudson Robotics Inc.

- Honeywell International Inc.

- Hamilton Company

- HighRes Biosolutions

- Biosero Inc.

- QIAGEN NV

- Copan Diagnostics

- Retisoft Inc.

- Bruker(Chemspeed)

- Roche Diagnostics

- ABB Ltd.

- LabVantage Solutions

- Festo AG and Co. KG

제7장 시장 기회와 장래의 전망

SHW 25.11.11The modular laboratory automation market size is estimated at USD 3.2 billion in 2025 and is set to advance to USD 4.7 billion by 2030, translating to a 6.50% CAGR throughout the forecast window.

Heightened regulatory scrutiny, a shrinking laboratory workforce, and the growing need for reproducible data position automated, network-ready work cells as critical infrastructure for life-science innovation. Suppliers now bundle artificial-intelligence software with robotics, allowing laboratories to standardize protocols, capture complete audit trails, and shorten testing cycles. Pharmaceutical manufacturers are accelerating adoption to satisfy the EU GMP Annex 1 contamination-control requirements, while hospital networks favour modular deployments that scale distributed testing without lengthy construction projects. In parallel, federal support such as the NIH MATChS program signals that laboratory automation is no longer discretionary but a strategic enabler for biomedical research.

Global Modular Laboratory Automation Market Trends and Insights

Rising Need for Reproducibility & Data Integrity

Automated platforms impose strict process control, cutting variability that manual techniques often introduce. The Mayo Clinic's sorting system moves 6,000 tubes per hour without mis-sorts, demonstrating zero-defect data capture. Such results are indispensable as regulators demand granular audit trails for every assay. Multi-site consortia use standardized robotic workflows to compare results confidently, boosting collaborative studies. Vendors increasingly embed blockchain-ready logs to safeguard raw data. These capabilities elevate laboratory credibility when submitting evidence to regulatory agencies.

Chronic Skilled-Labor Shortages in Life-Science Labs

Vacancies nearing 25,000 positions across North America have pushed labs toward automation that reassigns repetitive tasks to machines while scientists focus on interpretation. Clarapath's robotic microtomy lets one technician oversee multiple slide-prep stations, tripling output capacity. Such labour-multiplying benefits shorten testing backlogs and support 24/7 operations without overtime premiums. Automation also institutionalizes tacit knowledge by encoding protocols into software, reducing onboarding time for new hires. With retirement rates climbing, the economic rationale for modular laboratory automation market investments strengthens further.

High Upfront Capex & Long ROI Cycles

Entry-level robotic benches cost USD 100,000-300,000, while full lines exceed USD 1 million, straining academic and midsize budgets. Payback often stretches past three years because benefits like error-free data or staff redeployment resist simple monetization. Leasing schemes and usage-based pricing partially lower the barrier, yet maintenance contracts, validation, and operator training still elevate total cost of ownership. Finance committees therefore stage investments in phases, favouring the modular laboratory automation market approach that lets sites bolt on capacity incrementally.

Other drivers and restraints analyzed in the detailed report include:

- High-Throughput Genomics & Cell-Therapy Pipelines

- EU GMP Annex 1 Contamination-Control Mandates

- Integration Complexity with Legacy Instruments & LIMS

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Automated liquid handlers generated 26.41% of the modular laboratory automation market size in 2024, cementing their role as the backbone of assay preparation. Laboratories favour these platforms because precision pipetting ensures downstream data quality while freeing staff for analytical tasks. Demand for integrated software that optimizes deck layouts and predicts tip consumption is growing, reducing consumable waste and unplanned downtime. Automated storage & retrieval systems, projected to grow at 7.21% CAGR, solve the chronic challenge of sample archiving by delivering samples to work cells just-in-time. Vendors now combine low-temperature warehouses with AI route planning, minimizing freeze-thaw events and safeguarding biomolecule integrity.

Software innovation shapes competitive differentiation as vendors embed machine-learning algorithms that flag anomalies before assay failures propagate. Thermo Fisher's Vulcan platform illustrates how combining robotic arms with self-tuning workflows elevates throughput. Analysers capable of inline mass spectrometry or fluorescence detection compress total turnaround time, letting labs condense multi-day protocols into single shifts. The net effect is a structural rise in demand for cohesive ecosystems rather than single-purpose boxes, reinforcing supplier emphasis on modular laboratory automation market ecosystems that orchestrate hardware and data in one pane of glass.

Clinical diagnostics contributed 28.50% revenue in 2024, underpinned by high-volume chemistries and strict accreditation criteria that reward reproducible automation. Hospital laboratories integrate conveyor-linked work cells with middleware that posts verified results directly to electronic health records, shortening patient care cycles. Cell & gene therapy workflows, forecast for 9.66% CAGR, need closed-system robots that minimize contamination risk during lengthy culture periods. Robots equipped with environmental sensors and AI classifiers maintain sub-micron cleanliness, preventing batch failures that could cost millions of USD.

Drug-discovery groups continue to deploy high-throughput screens on 1,536-well plates, while genomics consortia automate library prep for population cohorts. Proteomics is emerging as laboratories automate sample digestion and LC-MS loading. Cross-disciplinary platforms that support reagent-agnostic protocols are gaining traction, as they let sites pivot capacity between diagnostic, discovery, and manufacturing workloads. This versatility reinforces investment in the modular laboratory automation market because a single capital outlay serves many revenue streams.

Modular Laboratory Automation Market is Segmented by Equipment and Software (Automated Liquid Handlers, Automated Plate Handlers and More), Field of Application (Drug Discovery, Genomics and More), End User (Pharmaceutical and Biotech Companies, and More), Automation Type (Standalone Instrument Automation, Modular Workcells and More) and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America sustained a 41.70% revenue share in 2024, reflecting the concentration of biopharmaceutical headquarters, generous NIH funding, and a mature regulatory environment that favours technology investments. Recent federal grants, such as the USD 2.15 million MATChS award, confirm public-sector endorsement of intelligent automation. Tier-1 hospitals are integrating decentralized work cells, pushing specimen processing closer to patient intake to reduce logistics delays. Canada's life-science clusters leverage provincial tax credits to upgrade research infrastructure, though staffing shortages remain acute; automation therefore offers a pragmatic path to maintain throughput despite limited headcount. Mexico, seeking export accreditation for sterile injectables, is piloting robotic isolators to meet Annex 1 requirements and secure contract manufacturing deals.

Asia-Pacific registers the highest growth trajectory as governments subsidize biotech infrastructure and encourage local manufacturing of advanced therapies. China invests in national sequencing hubs that adopt fully automated, closed-loop pipelines, reducing per-genome costs and accelerating precision-medicine pilot programs. Japan's aging population elevates demand for diagnostic automation capable of handling chronic-disease panels. India's contract-manufacturing sector implements modular isolators that comply with global sterility standards, positioning domestic plants for regulated-market exports. South Korea focuses on cell-therapy centers of excellence that combine dual-arm robots with AI analytics, bringing complex biologics to market more swiftly. Collectively, these initiatives underpin sustained demand across the modular laboratory automation market throughout the region.

Europe remains a pivotal market because Annex 1 lifts technical barriers in favour of robotics, driving upgrades across legacy fill-finish lines. Germany's engineering base integrates high-precision mechatronics with cloud-native MES platforms, while the United Kingdom channels research funding into university-hospital partnerships that validate AI-directed work cells. France modernizes public-sector laboratories through stimulus packages that offset upfront capex. Italy and Spain prioritize total laboratory automation in blood-bank operations to curb transfusion errors. The regulatory commonality across the European Economic Area encourages cross-border standardization, letting suppliers offer uniform validation packages and thereby expedite procurement across multiple sites within the modular laboratory automation market.

- Thermo Fisher Scientific

- Danaher Corporation (Beckman Coulter)

- Tecan Group AG

- Agilent Technologies

- PerkinElmer Inc.

- Siemens Healthineers

- Becton Dickinson (BD)

- Hudson Robotics Inc.

- Honeywell International Inc.

- Hamilton Company

- HighRes Biosolutions

- Biosero Inc.

- QIAGEN N.V.

- Copan Diagnostics

- Retisoft Inc.

- Bruker (Chemspeed)

- Roche Diagnostics

- ABB Ltd.

- LabVantage Solutions

- Festo AG and Co. KG

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising need for reproducibility and data integrity

- 4.2.2 Chronic skilled-labor shortages in life-science labs

- 4.2.3 High-throughput genomics and cell-therapy pipelines

- 4.2.4 EU GMP Annex 1 contamination-control mandates accelerating robotics (under-reported)

- 4.3 Market Restraints

- 4.3.1 High upfront capex and long ROI cycles

- 4.3.2 Integration complexity with legacy instruments and LIMS

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Equipment and Software

- 5.1.1 Automated Liquid Handlers

- 5.1.2 Automated Plate Handlers

- 5.1.3 Robotic Arms

- 5.1.4 Automated Storage and Retrieval Systems (ASRS)

- 5.1.5 Analyzers

- 5.1.6 Software

- 5.2 By Field of Application

- 5.2.1 Drug Discovery

- 5.2.2 Genomics

- 5.2.3 Proteomics

- 5.2.4 Clinical Diagnostics

- 5.2.5 Other Applications

- 5.3 By End User

- 5.3.1 Pharmaceutical and Biotech Companies

- 5.3.2 Academic and Research Institutes

- 5.3.3 Clinical and Diagnostic Laboratories

- 5.3.4 Contract Research Organisations

- 5.3.5 Food and Environmental Testing Labs

- 5.4 By Automation Type

- 5.4.1 Standalone Instrument Automation

- 5.4.2 Modular Workcells

- 5.4.3 Integrated Workcells

- 5.4.4 Total Laboratory Automation (TLA) Lines

- 5.4.5 Mobile/Cloud-connected Robots

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 United Kingdom

- 5.5.3.2 Germany

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Russia

- 5.5.3.6 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 India

- 5.5.4.4 South Korea

- 5.5.4.5 Rest of Asia-Pacific

- 5.5.5 Middle East

- 5.5.5.1 Israel

- 5.5.5.2 Saudi Arabia

- 5.5.5.3 United Arab Emirates

- 5.5.5.4 Turkey

- 5.5.5.5 Rest of Middle East

- 5.5.6 Africa

- 5.5.6.1 South Africa

- 5.5.6.2 Egypt

- 5.5.6.3 Rest of Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Thermo Fisher Scientific

- 6.4.2 Danaher Corporation (Beckman Coulter)

- 6.4.3 Tecan Group AG

- 6.4.4 Agilent Technologies

- 6.4.5 PerkinElmer Inc.

- 6.4.6 Siemens Healthineers

- 6.4.7 Becton Dickinson (BD)

- 6.4.8 Hudson Robotics Inc.

- 6.4.9 Honeywell International Inc.

- 6.4.10 Hamilton Company

- 6.4.11 HighRes Biosolutions

- 6.4.12 Biosero Inc.

- 6.4.13 QIAGEN N.V.

- 6.4.14 Copan Diagnostics

- 6.4.15 Retisoft Inc.

- 6.4.16 Bruker (Chemspeed)

- 6.4.17 Roche Diagnostics

- 6.4.18 ABB Ltd.

- 6.4.19 LabVantage Solutions

- 6.4.20 Festo AG and Co. KG

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment