|

시장보고서

상품코드

1850196

물리치료 장비 시장 : 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Physiotherapy Equipment - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

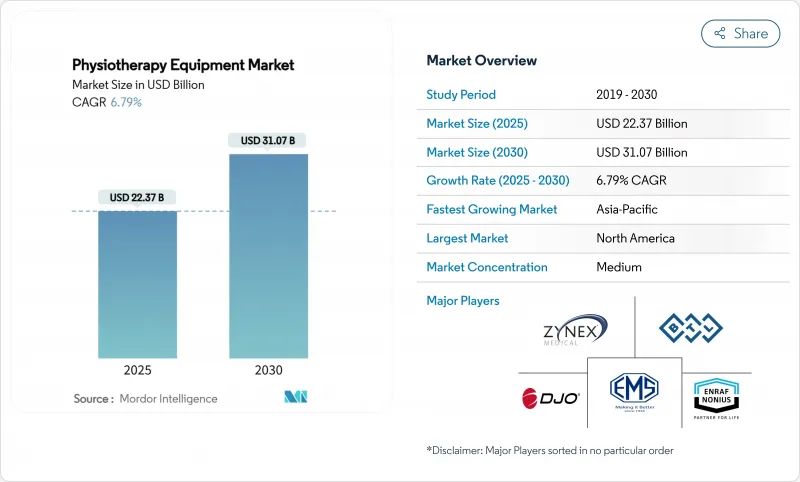

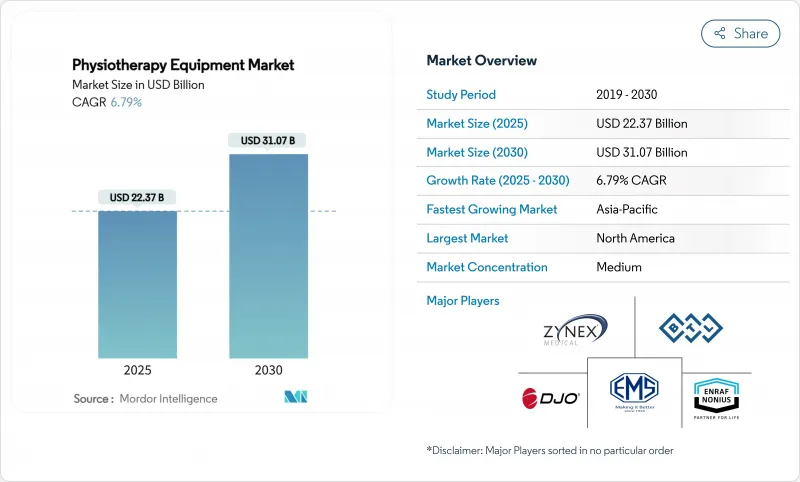

물리치료 장비 시장은 2025년에 223억 7,000만 달러, 2030년에는 310억 7,000만 달러에 이르고 기간 중 CAGR은 6.79%를 나타낼 전망입니다.

세계 인구의 고령화, 만성 근골격계 및 신경계 질환 증가, 커넥티드 디바이스에 의해 치료자가 클리닉의 벽을 넘어 경과를 모니터할 수 있게 됨으로써 수요가 확대되고 있습니다. 휴대용 시스템은 치료주기를 단축하고 가정 관리를 지원하기 때문에 치료자는 휴대용 시스템을 주류 진료에 통합합니다. 병원 구매 부문은 여전히 주요 구매자이지만 전문센터와 스포츠 의학 클리닉은 정확한 재활 목표를 충족하기 위해 더 새로운 양식을 주문합니다. 기존 공급업체는 인공지능을 장비에 통합하여 프로토콜을 개인화하는 반면, 신흥 기업은 구독 기반 분석을 통해 조기 채택자를 획득했습니다.

세계 물리치료 장비 시장 동향과 통찰

노년인구와 만성질환 부담 증가

세계적으로 65세 이상의 노인 인구가 급속히 증가하고 있으며, 운동 능력 저하와 합병증을 완화시키는 재활에 대한 장기적인 수요가 높아지고 있습니다. 의료제도는 물리치료를 변성관절질환의 수술을 대체하는 비용 효율적인 옵션으로 자리매김하여 전기요법, 초음파요법, 로봇보행시스템의 조달을 촉진하고 있습니다. 세계보건기구(WHO)의 건강 장수 의제는 노인의 기능적 능력을 강화하는 외골격의 사용을 장려하고 선진국 시장의 구매 기준에 영향을 미칩니다. 공급업체는 낙하 방지 분석과 더 부드럽고 가벼운 외골격 정장을 표준 제품에 통합하여 적응합니다. 이러한 개발은 보다 대규모 노인 집단의 치료를 목표로 하는 클리닉의 안정적인 교체 사이클을 유지하고 있습니다.

확대 수술 후 및 종양학 재활 수요

낮은 침습 수술은 퇴원을 가속화하고 컴팩트하고 다중 모드 워크 스테이션을 필요로하는 외래 환자 환경으로 회복을 이동시킵니다. 외래수술센터(ASC)는 당일 관절 수술을 지원하기 위해 휴대용 전기 자극 장치와 지속적인 수동 운동 장치를 구입합니다. 암의 생존율은 계속 개선되고 있으며, 종양학의 가이드라인에서는 피로나 신경장애에 대한 대책으로서 물리치료가 권장되게 되어 저강도 초음파나 공기압박의 주문이 쇄도하고 있습니다. 2024년에는 51개의 재활 전문 병원이 개원 또는 건설되고, 그 중 많은 부분에 종양 치료실이 설치되는 등 전문 기기에 대한 시설 수준의 설비 투자가 현저해지고 있습니다. 공급업체는 수술 후 이정표를 추적하는 원격 모니터링 대시보드와 장비를 번들로 지원합니다.

세계 물리치료사 부족

많은 국가에서는 충분한 교육 프로그램이 없으며 초등 교육에서 노년 의학 모듈을 포함하는 것은 절반에 불과하므로 고급 전기 기계 시스템의 도입이 제한됩니다. 클리닉은 데이터 수집을 자동화하고 표준 프로토콜로 환자를 유도하는 AI를 도입함으로써 보완하고 있지만, 복잡한 경우에는 여전히 인간 모니터링이 필요합니다. 인재 확보가 어려운 지방의 병원이나 저소득 지역에서는 인재 부족이 심각화해, 기기의 활용이 제약됩니다. 결과적으로 공급업체는 직원의 숙련을 촉진하기 위해 현장 교육과 가상 튜토리얼을 번들로 제공하지만 전반적인 능력 부족은 주요 신흥 국가에서의 대응 가능한 기반을 억제합니다.

부문 분석

2024년 물리치료 장비 시장 점유율에서 35.72%를 차지한 이유는 통증과 신경근관리에서 전기치료의 역할이 확립되어 있기 때문입니다. 병원은 멀티채널 자극장치의 대량 구매를 계속하고 있는데, 이는 상환 코드가 명확하게 정의되고 오피오이드 감소 프로그램이 비약리학적 통증 완화를 지지하고 있기 때문입니다. 저주파치료기에서는 블루투스 접속이 가능하게 되어 원격조작이나 사용상황의 기록이 가능하게 되었습니다. 2030년까지 연평균 복합 성장률(CAGR)이 가장 빠른 이유는 초음파 시스템으로, 연골 재생을 위한 저강도 응용이 조사에서 입증되었기 때문입니다. 따라서 초음파장치의 물리치료 장비 시장 규모는 스포츠클리닉에 도입되는 FDA 인가의 지속적인 음향의료유닛에 의해 꾸준히 확대될 것으로 예측됩니다. 레이저와 빛 치료기는 만성 상처와 같은 틈새 분야를 긁지만, 충격파와 PEMF는 여전히 전문가의 선택입니다.

소비자 급 TENS 장비가 매력적인 가격으로 온라인으로 판매되고 있기 때문에 전기 치료 경쟁이 치열해지고 있으며, 프리미엄 브랜드는 증거로 뒷받침되는 파형과 통합된 결과 대시보드로 차별화를 도모할 필요가 있습니다. 이와는 대조적으로 초음파 제조업체는 온열 효과 이외의 적응 확대에 주력하고 젤없이 가정에서 연속 사용이 가능한 비접촉형 기기를 판매하고 있습니다. 하나의 콘솔에 자극, 초음파, 진공 마사지를 담은 복합 치료 스테이션은 공간에 제약이 있는 외래 센터에 어필하고 있습니다. 이러한 하이브리드 제품은 시설 관리자가 통합 서비스 계약 및 소프트웨어 업데이트를 선호하기 때문에 공급업체와의 관계를 강화합니다.

2024년 물리치료 장비 시장 규모의 52.58%는 근골격계 장애이며, 변형성 관절증과 요통의 유행에 지지되고 있습니다. 인공 슬관절 치환술과 같은 대량 수술은 지속적인 수동 운동 기계 및 신경근 전기 자극 장치의 예측 가능한 수요를 생성합니다. 그러나 스포츠와 정형외과적 손상은 2030년까지 연평균 복합 성장률(CAGR)이 7.44%로 다른 모든 적응증을 상회합니다. 팀과 레크리에이션 선수는 과도한 부상으로 발전하기 전에 비대칭으로 플래그를 지정하는 웨어러블 모션 센서에 투자합니다. 그 기세는 관절에 부담을 주지 않고 고강도의 컨디셔닝을 할 수 있는 동적 부하 플랫폼이나 반중력 디딜방아로 조달처를 시프트시킵니다.

신경 재활은 로봇형 엑소슈트가 집중적인 보행 훈련 세션을 단축하고 진행 상황을 객관적으로 기록하므로 가시성이 향상됩니다. 심폐 프로토콜은 COVID 후 운동 허용 프로그램을 포함하도록 확장되고 호흡 피드백 모듈이 장착된 사이클 에르고미터의 판매에 박차를 가합니다. 소아과의 치료실에는 소형화된 로봇과 어드히어런스를 높이는 다채로운 가상현실 게임이 필요합니다. 임신과 관련된 골반통과 산후 회복에 대응하는 여성 건강 물리치료는 고객층을 넓히는 한편, 저레벨 레이저 치료 등의 친절한 치료법이 요구되고 있습니다. 다양한 적응증에서 AI를 갖춘 평가 앱은 치료사를 증거 기반 매개 변수 설정으로 안내합니다.

물리치료 장비 시장은 기기유형별(전기요법, 초음파요법, 기타), 용도별(근골격계, 신경계, 기타), 최종사용자별(병원, 재활센터/전문클리닉, 재택간병 현장, 기타), 유통채널별(시설 직접 판매, 전자상거래, 소매), 지역별(북미, 유럽, 아시아)로 세분화됩니다.

지역별 분석

북미는 2024년에 물리치료 장비 시장의 39.52%를 차지했으며, 이는 성숙한 상환과 접속모달리티의 높은 채택을 반영하고 있습니다. 미국 메디케어는 텔레헬스 유연성을 2025년까지 확대하여 재택용 전기 자극 키트를 포함한 원격 환자 모니터링 번들을 합법화했습니다. 미국 물리치료 서비스 부문은 2025년에 610억 달러 규모에 달하고, 안정된 구매력을 장비 갱신주기로 향합니다. 캐나다 각 주의 의료 제도는 학술 센터의 첨단 로봇 공학에 자금을 제공하고 멕시코는 디지털 보고 기능을 지정한 조달 프로그램을 통해 공립 병원을 업그레이드하고 있습니다. 경쟁 입찰은 환자 데이터를 보호하기 위해 사이버 보안 인증을 강조하는 경향이 커지고 있습니다.

2030년까지 연평균 복합 성장률(CAGR)이 가장 빠른 이유는 아시아태평양으로 중국, 일본, 인도가 재활의 용량을 확대하기 때문입니다. 정부 보조금은 센서가 있는 디딜방아와 AI 분석 엔진이 장착된 스마트 호스피탈의 시험 운영을 시작합니다. 의료기술에 대한 지역 벤처기업의 자금조달은 최근 22% 줄어들고 있지만, 국내 장비 제조업체는 저렴한 가격이지만 연결된 솔루션을 필요로 하는 중견 클리닉에서 비즈니스 기회를 발견하고 있습니다. 인구동태의 변화가 수요를 가속화한다: 일본에서는 실버경제가 하지외골격의 매출을 견인하고 인도에서는 새로운 의과대학 내에 물리치료 연구실에 투자를 하고 있습니다. 진료 보수에 편차가 있는 것은 변함없지만, 중류 가정 증가에 의해 가정용 초음파 진단의 비용을 자기 부담하는 경향이 강해지고 있습니다.

유럽은 국민 모두 보험 제도와 안전성을 보장하는 엄격한 규제 감독으로 안정적인 성장을 유지하고 있습니다. 독일의 질병 기금은 증거 기반 전기 치료 세션에 환불을 실시하고 디지털 건강에의 응용을 장려합니다. 영국의 외래 진료과는 족저근막염에 충격파 요법을 도입하고, 스칸디나비아 국가는 지방 주민들을 위한 원격 재활을 개척하고 있습니다. 동유럽에서는 EU 구조 기금이 재활 업그레이드에 충당되고 카운티 병원의 현대화로 격차가 줄어들고 있습니다. 중동 및 아프리카에서는 새로운 기세를 볼 수 있습니다. 2025년에 개장한 바레인의 아마나 의료시설에는 수처리 수영장이 있으며, '비전 2030' 하에서 정부의 헌신을 보여줍니다. 남미는 여전히 가격에 민감하지만 브라질의 민간 보험 회사가 수술 후 증례에 대한 신경근 전기 자극 보험 적용을 시작하고 장비 수입량이 점차 확대되고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 서포트

목차

제1장 서론

- 조사의 전제조건과 시장의 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 고령화와 만성질환의 부담 증가

- 수술 후 및 종양 재활 수요 증가

- 연결형 및 휴대용형의 물리치료 장비의 급속한 도입

- 외래 및 스포츠 의학 시설에 대한 투자 증가

- AI 기반 원격 재활 플랫폼, 보험 급여 적용 확대(아직 주목받지 않은 영역)

- 물리치료실에 있어서의 외골격과 로봇의 통합(아직 주목받지 않은 영역)

- 시장 성장 억제요인

- 세계에서 숙련리학치료사가 부족

- 신흥국 시장에서 불리하거나 불균일한 상환

- 첨단 전기 기계 시스템의 초기 비용이 증가

- 연결된 기기에서의 사이버 보안과 데이터 준수 위험(아직 주목받지 않은 영역)

- 가치/공급망 분석

- 규제 상황

- 기술의 전망

- Porter's Five Forces 분석

- 구매자의 협상력/소비자

- 공급기업의 협상력

- 신규 참가업체의 위협

- 대체품의 위협

- 경쟁 기업간 경쟁 관계

제5장 시장 규모와 성장 예측

- 기기별

- 전기요법

- 초음파 요법

- 레이저&광선치료

- 충격파 요법

- 자기 요법과 PEMF 요법

- 온열·동결요법 시스템

- 수처리 시스템

- 멀티 운동 & 재활 스테이션

- 기타

- 용도별

- 근골격

- 신경학

- 심장혈관 및 폐

- 스포츠와 정형외과적 상해

- 소아

- 여성의 건강 및 산부인과

- 기타

- 최종 사용자별

- 병원

- 재활센터/전문 클리닉

- 재택 케어의 설정

- 외래수술센터(ASC)

- 기타

- 유통 채널별

- 기관 투자가를 위한 직접 판매

- 전자상거래와 소매

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 기타 유럽

- 아시아태평양

- 중국

- 일본

- 인도

- 호주

- 한국

- 기타 아시아태평양

- 중동 및 아프리카

- GCC

- 남아프리카

- 기타 중동 및 아프리카

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 북미

제6장 경쟁 구도

- 시장 집중도

- 시장 점유율 분석

- 기업 프로파일

- Enovis Corporation(DJO Global Inc.)

- BTL Industries

- Zimmer MedizinSysteme(Enraf-Nonius BV)

- EMS Physio

- Patterson Medical(Performance Health)

- Dynatronics

- Zynex Medical Inc.

- HMS Medical Systems

- SEERS Medical

- Mectronic Medicale

- Guangzhou Longest Science&Technology Co.,Ltd.

- ITO Co. Ltd.

- Lifeward, Inc.

- Restorative Therapies

- Hocoma

제7장 시장 기회와 장래의 전망

SHW 25.11.07The physiotherapy equipment market reached USD 22.37 billion in 2025 and is forecast to attain USD 31.07 billion by 2030, registering a 6.79% CAGR over the period.

Demand is advancing as the global population ages, chronic musculoskeletal and neurological conditions climb, and connected devices enable therapists to monitor progress beyond clinic walls. Clinicians are integrating portable systems into mainstream practice because they shorten treatment cycles and support home-based care. Hospital purchasing departments remain the primary buyers, yet specialty centers and sports-medicine clinics are ordering newer modalities to address precise rehabilitation goals. Established suppliers now embed artificial intelligence into devices to personalize protocols, while start-ups court early adopters with subscription-based analytics.

Global Physiotherapy Equipment Market Trends and Insights

Rising Geriatric Population & Chronic Disease Burden

The global population aged 65 and above is expanding quickly, raising long-term demand for rehabilitation that mitigates mobility loss and co-morbidities. Health systems position physiotherapy as a cost-effective alternative to surgery for degenerative joint disease, propelling procurement of electrotherapy, ultrasound and robotic gait systems. The World Health Organization's healthy-aging agenda encourages exoskeleton use that augments functional capacity in older adults, influencing purchasing criteria in developed markets.Suppliers adapt by integrating fall-prevention analytics and softer, lighter exosuits into standard offerings. These developments sustain steady replacement cycles for clinics seeking to treat larger elderly cohorts.

Expanding Post-Surgical & Oncology Rehabilitation Demand

Minimally invasive surgery accelerates discharge, shifting recovery to outpatient settings that require compact, multi-modality workstations. Ambulatory surgical centers purchase portable electrical stimulation and continuous-passive-motion units to support same-day joint procedures. Cancer survival rates continue to improve, and oncology guidelines now recommend physiotherapy to counter fatigue and neuropathy, igniting orders for low-intensity ultrasound and pneumatic compression. Fifty-one dedicated rehabilitation hospitals opened or broke ground in 2024 and many include oncology suites, underscoring facility-level capital spending devoted to specialised equipment.Vendors respond by bundling devices with remote-monitoring dashboards that track post-operative milestones.

Shortage of Skilled Physiotherapists Worldwide

Many nations lack sufficient training programs, and only half include geriatric modules in entry-level education, limiting adoption of sophisticated electro-mechanical systems. Clinics compensate by automating data collection and incorporating AI that guides patients through standard protocols, yet complex cases still require human oversight. Workforce gaps intensify in rural hospitals and low-income regions where recruitment is difficult, constraining equipment utilisation. As a result, vendors bundle on-site training and virtual tutorials to accelerate staff proficiency, but the overall capacity shortfall suppresses the addressable base in key emerging economies.

Other drivers and restraints analyzed in the detailed report include:

- Rapid Adoption of Connected & Portable Physiotherapy Devices

- Growing Investments in Outpatient & Sports Medicine Facilities

- Unfavorable or Patchy Reimbursement in Developing Markets

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Electrotherapy accounted for 35.72% of physiotherapy equipment market share in 2024 thanks to its established role in pain and neuromuscular management. Hospitals continue bulk purchases of multi-channel stimulators because reimbursement codes are well defined and opioid-reduction programs favour non-pharmacological pain relief. Low-frequency variants now feature Bluetooth connectivity, giving therapists remote control and usage logging. Ultrasound systems post the fastest 7.18% CAGR to 2030 as research validates low-intensity applications for cartilage regeneration. The physiotherapy equipment market size for ultrasound devices is therefore projected to swell steadily, supported by FDA-cleared sustained acoustic medicine units deployed in sports clinics. Laser and light devices nibble at niche segments such as chronic wounds, while shockwave and PEMF remain specialist options.

The competitive field for electrotherapy tightens because consumer-grade TENS gadgets sell online at attractive prices, forcing premium brands to differentiate with evidence-backed waveforms and integrated outcome dashboards. In contrast, ultrasound suppliers focus on expanding indications beyond thermal effects, marketing non-contact devices that allow continuous use at home without gel. Combined therapy stations that house stimulation, ultrasound and vacuum massage within a single console appeal to space-constrained outpatient centers. These hybrid offerings reinforce vendor relationships because facility managers prefer unified service contracts and software updates.

Musculoskeletal disorders delivered 52.58% of physiotherapy equipment market size in 2024, underpinned by the prevalence of osteoarthritis and lower-back pain. High-volume procedures such as knee replacements generate predictable demand for continuous-passive-motion machines and neuromuscular electrical stimulators. Sports and orthopedic injuries, however, outpace all other indications with a 7.44% CAGR through 2030. Teams and recreational athletes invest in wearable motion sensors that flag asymmetries before they escalate into overuse injuries. That momentum shifts procurement toward dynamic loading platforms and anti-gravity treadmills capable of high-intensity conditioning without joint strain.

Neurorehabilitation gains visibility because robotic exosuits shorten intensive gait-training sessions and document progress objectively. Cardio-pulmonary protocols expand to include post-COVID exercise tolerance programs, spurring sales of cycle ergometers fitted with respiratory feedback modules. Pediatric suites require scaled-down robotics and colorful virtual-reality games that encourage adherence. Women's-health physiotherapy, addressing pregnancy-related pelvic pain and post-partum recovery, broadens the client base yet calls for gentler modalities such as low-level laser therapy. Across indications, AI-powered assessment apps guide therapists toward evidence-based parameter settings.

The Physiotherapy Equipment Market is Segmented by Equipment Type (Electrotherapy, Ultrasound Therapy, and More), by Application (Musculoskeletal, Neurology, and More), by End User (Hospitals, Rehabilitation Centers / Specialty Clinics, Home-Care Settings, and More), by Distribution Channel (Direct Institutional Sales, E-Commerce and Retail), by Geography (North America, Europe, Asia-Pacific, and More).

Geography Analysis

North America controlled 39.52% of the physiotherapy equipment market in 2024, reflecting mature reimbursement and high adoption of connected modalities. United States Medicare extended telehealth flexibilities to 2025, legitimising remote patient-monitoring bundles that include electrical stimulation kits for home use. The U.S. physical-therapy services sector, worth USD 61 billion in 2025, channels stable purchasing power toward equipment refresh cycles. Canada's provincial health systems fund advanced robotics in academic centers, while Mexico upgrades public hospitals through procurement programs that specify digital-reporting capabilities. Competitive bids increasingly weight cybersecurity certifications to safeguard patient data.

Asia-Pacific posts the fastest 8.52% CAGR through 2030 as China, Japan and India scale rehabilitation capacity. Government grants subsidise smart-hospital pilots outfitted with sensor-laden treadmills and AI analytics engines. Although regional venture funding for med-tech declined by 22% in recent years, domestic device makers find opportunities in mid-tier clinics requiring affordable but connected solutions. Demographic shifts accelerate demand: Japan's silver economy drives sales of lower-limb exoskeletons, while India invests in physiotherapy laboratories within new medical colleges. Variations in reimbursement persist, but growing middle-class households increasingly pay out of pocket for home-use ultrasound.

Europe maintains steady growth owing to universal healthcare and strict regulatory oversight that guarantees safety. German sickness funds reimburse evidence-based electrotherapy sessions and encourage digital-health applications. United Kingdom outpatient departments deploy shockwave therapy for plantar fasciitis, and Scandinavian countries pioneer telerehabilitation for rural residents. Eastern Europe narrows the gap by modernising county hospitals with EU structural funds earmarked for rehabilitation upgrades. The Middle East and Africa show emerging momentum: Bahrain's Amana Healthcare facility opening in 2025 includes hydrotherapy pools, signalling government commitment under Vision 2030. South America remains price sensitive, yet private insurers in Brazil start covering neuromuscular electrical stimulation for post-operative cases, gradually broadening equipment import volumes.

- Enovis Corporation (DJO Global Inc.)

- BTL

- Zimmer MedizinSysteme (Enraf-Nonius BV)

- EMS Physio

- Patterson Medical (Performance Health)

- Dynatronics

- Zynex Medical

- HMS Medical system

- SEERS Medical

- Mectronic Medicale

- Guangzhou Longest Science&Technology Co.,Ltd.

- ITO Co. Ltd.

- Lifeward, Inc.

- Restorative Therapies

- Hocoma

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising geriatric population & chronic disease burden

- 4.2.2 Expanding post-surgical & oncology rehabilitation demand

- 4.2.3 Rapid adoption of connected & portable physiotherapy devices

- 4.2.4 Growing investments in outpatient & sports medicine facilities

- 4.2.5 AI-driven tele-rehabilitation platforms gaining reimbursement (under-radar)

- 4.2.6 Exoskeleton & robotics integration in physiotherapy suites (under-radar)

- 4.3 Market Restraints

- 4.3.1 Shortage of skilled physiotherapists worldwide

- 4.3.2 Unfavorable or patchy reimbursement in developing markets

- 4.3.3 High upfront cost of advanced electro-mechanical systems

- 4.3.4 Cyber-security & data-compliance risk in connected devices (under-radar)

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Buyers/Consumers

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitute Products

- 4.7.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value)

- 5.1 By Equipment Type

- 5.1.1 Electrotherapy

- 5.1.2 Ultrasound Therapy

- 5.1.3 Laser & Light Therapy

- 5.1.4 Shockwave Therapy

- 5.1.5 Magnetic & PEMF Therapy

- 5.1.6 Heat & Cryotherapy Systems

- 5.1.7 Hydrotherapy Systems

- 5.1.8 Multi-exercise & Rehabilitation Stations

- 5.1.9 Others

- 5.2 By Application

- 5.2.1 Musculoskeletal

- 5.2.2 Neurology

- 5.2.3 Cardiovascular and Pulmonary

- 5.2.4 Sports and Orthopedic Injuries

- 5.2.5 Pediatrics

- 5.2.6 Women's Health & OB/GYN

- 5.2.7 Others

- 5.3 By End User

- 5.3.1 Hospitals

- 5.3.2 Rehabilitation Centers / Specialty Clinics

- 5.3.3 Home-care Settings

- 5.3.4 Ambulatory Surgical Centers

- 5.3.5 Others

- 5.4 By Distribution Channel

- 5.4.1 Direct Institutional Sales

- 5.4.2 E-commerce and Retail

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 Australia

- 5.5.3.5 South Korea

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 Middle East and Africa

- 5.5.4.1 GCC

- 5.5.4.2 South Africa

- 5.5.4.3 Rest of Middle East and Africa

- 5.5.5 South America

- 5.5.5.1 Brazil

- 5.5.5.2 Argentina

- 5.5.5.3 Rest of South America

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.3.1 Enovis Corporation (DJO Global Inc.)

- 6.3.2 BTL Industries

- 6.3.3 Zimmer MedizinSysteme (Enraf-Nonius BV)

- 6.3.4 EMS Physio

- 6.3.5 Patterson Medical (Performance Health)

- 6.3.6 Dynatronics

- 6.3.7 Zynex Medical Inc.

- 6.3.8 HMS Medical Systems

- 6.3.9 SEERS Medical

- 6.3.10 Mectronic Medicale

- 6.3.11 Guangzhou Longest Science&Technology Co.,Ltd.

- 6.3.12 ITO Co. Ltd.

- 6.3.13 Lifeward, Inc.

- 6.3.14 Restorative Therapies

- 6.3.15 Hocoma

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment