|

시장보고서

상품코드

1850216

APC(고급 공정 제어) : 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Advanced Process Control - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

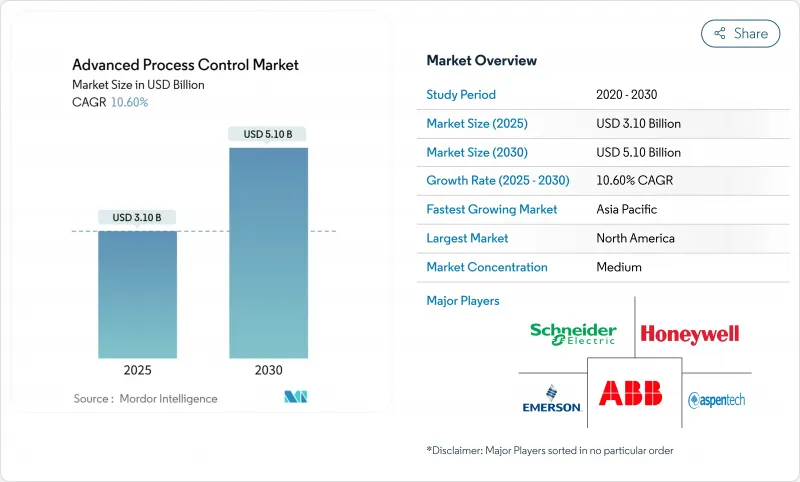

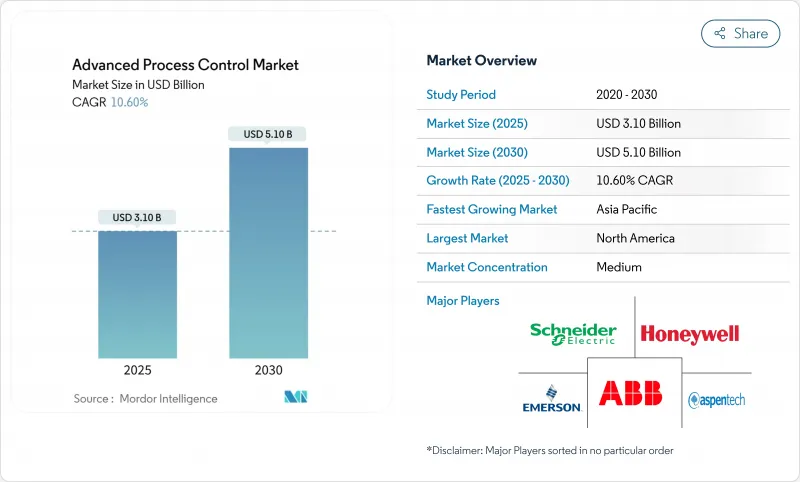

APC(고급 공정 제어) 시장은 2025년에 31억 달러로 평가되었고, 2030년에는 51억 달러에 이를 것으로 예측되며, CAGR은 10.6%를 나타낼 전망입니다.

에너지 집약적 제조업체들이 변동성 높은 유틸리티 가격에 대응하고, 강화되는 배출 규제를 충족하며, 기존 PID 루프의 능력을 뛰어넘는 점점 더 복잡해지는 다변수 공정을 관리하기 위해 도입을 가속화하고 있습니다. 클라우드 연결성과 내장형 인공지능을 통해 이제 예측 제어 모델이 분산된 시설 전반에서 작동할 수 있게 되어 전개 시간을 단축하고 투자 수익률을 개선합니다. 공급업체들은 에너지 비용 최적화, 실시간 품질 보증, 내장형 규제 보고 기능을 중심으로 애플리케이션을 패키징하고 있으며, 이는 1-2%의 수율 개선이 연간 수백만 달러의 절감으로 이어지는 산업 분야에서 투자 회수 기간을 단축합니다. 인수합병 활동의 꾸준한 흐름은 공장 현장부터 기업 클라우드 환경까지 확장 가능한 통합 플랫폼에 소프트웨어, 분석, 사이버보안을 통합하려는 전략적 경쟁을 강조합니다.

세계의 APC(고급 공정 제어) 시장 동향 및 인사이트

실시간 에너지 비용 최적화 요구

변동성 높은 연료 및 전력 가격으로 인해 공정 제어는 효율성 도구에서 수익성 확보의 필수 요소가 되었습니다. 정유 공장의 비원유 운영 비용 중 에너지 비중이 50% 이상을 차지할 수 있으므로, 공장들은 사양 한계를 유지하면서 부하를 저렴한 요금 시간대로 전환하는 예측 알고리즘을 도입합니다. 발표된 사례 연구에 따르면 에너지 사용량이 10-20% 감소했으며, 최적화된 운영으로 유지보수 주기가 연장되고 계획되지 않은 가동 중단 시간이 감소함에 따라 이 효과는 더욱 확대됩니다.

APC와 IIoT 및 AI 분석의 통합

저지연 산업용 네트워크가 센서, 컨트롤러, 클라우드 엔진을 연결하여 머신러닝 모델이 장애를 예측하고 편차가 확산되기 전에 시정 조치를 제안할 수 있게 합니다. FDA의 2025년 1월 지침은 AI 기반 실시간 모니터링을 권장하여 규제 대상 제조업체의 주요 도입 장벽을 제거했습니다.

높은 초기 비용과 통합의 복잡성

전체 설치 비용은 50만-500만 달러에 달할 수 있어 소규모 공장에겐 장벽입니다. 기존 설비(Brownfield)는 계측기 업그레이드 및 DCS 교체가 필요한 경우가 많아 일정이 18개월까지 연장되며 운영자는 생산 중단 위험에 노출됩니다.

부문 분석

소프트웨어는 2024년 고급 공정 제어 시장 점유율의 54%를 차지하며, 하드웨어 중심 시스템에서 클라우드 지원 플랫폼으로의 결정적인 전환을 보여줍니다. 이 부문은 신속한 도입, 원활한 DCS 통합, 자본 집약도를 낮추는 원격 분석에 대한 수요에 힘입어 성장하고 있습니다. 구독 모델이 진입 장벽을 낮추고 지속적인 알고리즘 업그레이드를 제공함에 따라 클라우드 호스팅 솔루션은 2030년까지 연평균 12.9% 성장할 것으로 전망됩니다. 하드웨어는 엣지 실행에 여전히 필수적이지만 점차 상품화되는 반면, 공장들이 지속적인 개선 문화를 수용함에 따라 모델 유지보수 및 성능 튜닝을 포함하는 서비스 계약이 확대되고 있습니다. 이러한 전환으로 공급업체들은 새로운 최적화 템플릿을 몇 달이 아닌 몇 주 만에 출시할 수 있게 되어 디지털 전환 로드맵을 가속화하고 있습니다.

소프트웨어에 기인한 고급 공정 제어 시장 규모는 마이크로서비스 아키텍처와 컨테이너화된 전개 전략의 광범위한 채택을 반영하여 2025년 17억 달러에서 2030년 30억 달러로 확대될 것으로 전망됩니다. 엣지 게이트웨이는 이제 필터링된 데이터를 클라우드 AI 엔진으로 라우팅하여 온프레미스 컨트롤러에 실시간 권장 사항을 제공함으로써 사이버 보안, 지연 시간 및 규제 제약 조건 간의 균형을 맞춥니다.

모델 예측 제어(MPC)는 2024년 매출의 46%를 차지하며, 제약 조건이 있는 다변수 공정 조정의 핵심 도구로서 입지를 공고히 했습니다. 선형 MPC는 열역학적 관계가 상대적으로 안정적인 원유 증류 및 에틸렌 분해와 같은 대규모 연속 공정에서 우위를 점하고 있습니다. 비선형 MPC는 특수 화학 및 제약 공장에서 비정상 상태 반응과 엄격한 품질 기준을 처리해야 하는 수요 증가로 12.8%의 연평균 성장률(CAGR) 전망을 기록하며 성장세를 보이고 있습니다.

비선형 MPC의 고급 공정 제어 시장 규모는 2030년까지 11억 달러에 달할 전망으로, 복잡한 동역학 및 가변 공급 성분을 처리할 수 있는 알고리즘에 대한 수요 증가를 반영합니다. 공급업체들은 수동 개입 없이 드리프트에 대응하는 적응형 모델링 및 자동 조정 기능을 내장하여 차별화하며, 운영자가 적은 엔지니어링 노력으로 최적의 성능을 유지할 수 있도록 합니다.

지역 분석

북미는 조기 디지털화, 풍부한 정유 설비 용량, 탄탄한 인재 생태계에 힘입어 2024년 매출의 37%를 차지했습니다. 연방 정부의 에너지 효율 인센티브와 투명한 탄소 시장은 제어 시스템 업그레이드를 더욱 촉진하고 있습니다. 아시아태평양 지역은 중국이 국내 기술 자립을 우선시하는 3,000억 위안(417억 달러) 규모의 산업 자동화 프로그램을 추진하며 11.8%의 연평균 복합 성장률(CAGR) 전망으로 가장 빠르게 성장하고 있습니다. 인도, 일본 및 아세안(ASEAN) 경제권도 노동력 제약과 생산성 격차 해소를 위한 자동화를 목표로 이를 따르고 있습니다.

유럽은 여전히 혁신의 중심지로, 엄격한 기후 정책과 EU 분류체계가 자금 조달 비용을 측정 가능한 탈탄소화와 연계합니다. 공장들은 경쟁력을 유지하면서 스코프 1 배출량을 줄이기 위해 APC를 활용합니다. 한편 중동, 아프리카, 라틴아메리카는 인프라 한계를 뛰어넘기 위해 클라우드 네이티브 APC를 도입 중이며, 광산 및 LNG 프로젝트가 주요 활용 사례로 자리잡고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

목차

제1장 서론

- 조사의 전제조건과 시장의 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 실시간 에너지 비용 최적화 요구

- APC와 IIoT 및 AI 분석 통합

- 배출가스 규제 엄격화

- 초대형 특수화학 및 LNG 프로젝트의 복잡성

- 모듈식 스키드용 플러그 앤 플레이 클라우드 APC

- 자율 채굴 및 금속 운영 확대

- 시장 성장 억제요인

- 높은 초기 비용 및 통합 복잡성

- APC 인재 부족 및 모델 유지 관리

- 원격/클라우드 APC의 사이버 보안 위험

- 소규모 다품종 배치 플랜트의 낮은 투자 수익률

- 가치/공급망 분석

- 기술의 전망

- 규제 상황

- 신형 APC 시스템과 기존 시스템의 근대화의 비교 분석

- Five Forces 분석

- 공급기업의 협상력

- 구매자의 협상력

- 신규 참가업체의 위협

- 대체품의 위협

- 경쟁도

제5장 시장 규모와 성장 예측

- 컴포넌트별

- 하드웨어

- 소프트웨어

- 서비스

- 제품 유형별

- 고급 규제 제어(ARC)

- 모델 예측 제어(MPC)

- 비선형 MPC

- 다변수 예측 제어

- 추론 및 기타 제어

- 전개 모드별

- 온프레미스

- 클라우드 기반

- 하이브리드

- 공정 유형별

- 연속 공정

- 배치 공정

- 최종 사용자 업계별

- 석유 및 가스

- 화학제품 및 석유화학제품

- 의약품

- 음식

- 에너지 및 전력

- 시멘트

- 금속가공

- 펄프 및 종이

- 기타

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 러시아

- 기타 유럽

- 아시아

- 중국

- 일본

- 인도

- 한국

- 호주 & 뉴질랜드

- 기타 아시아

- 중동 및 아프리카

- 중동

- 사우디아라비아

- 아랍에미리트(UAE)

- 튀르키예

- 기타 중동

- 아프리카

- 남아프리카

- 나이지리아

- 기타 아프리카

- 북미

제6장 경쟁 구도

- 시장 집중도

- 전략적 동향

- 시장 점유율 분석

- 기업 프로파일

- ABB Ltd.

- Aspen Technology Inc.

- Emerson Electric Co.

- General Electric Co.

- Honeywell International Inc.

- Rockwell Automation Inc.

- Schneider Electric SE

- Siemens AG

- Yokogawa Electric Corp.

- SUPCON Technology Co. Ltd

- Hollysys Automation Technologies Ltd

- Endress Hauser Group

- Valmet Oyj

- KBC Advanced Technologies

- Metso Outotec

- FLSmidth & Co. A/S

- AVEVA Group plc

- Azbil Corporation

- Endress Hauser Group

- Valmet Oyj

- AVEVA Group plc

- Gensym Corporation

- ICONICS Inc.

제7장 시장 기회와 장래의 전망

HBR 25.11.17The advanced process control market generated USD 3.1 billion in 2025 and is projected to reach USD 5.1 billion by 2030, advancing at a 10.6% CAGR.

Adoption accelerates as energy-intensive manufacturers seek to counter volatile utility prices, satisfy tightening emission mandates, and manage increasingly complex multi-variable processes that outstrip the capabilities of conventional PID loops. Cloud connectivity and embedded artificial intelligence now allow predictive control models to operate across distributed facilities, cutting deployment time and improving return on investment. Vendors are packaging applications around energy-cost optimization, real-time quality assurance, and embedded regulatory reporting, which shortens payback periods in industries where 1-2% yield improvements translate into multi-million-dollar annual savings. A steady flow of merger and acquisition activity underscores a strategic race to integrate software, analytics, and cybersecurity into unified platforms that can scale from the plant floor to enterprise cloud environments.

Global Advanced Process Control Market Trends and Insights

Real-time energy-cost optimization needs

Volatile fuel and electricity prices have elevated process control from an efficiency lever to a bottom-line necessity. Energy can represent more than 50% of non-crude refinery operating costs, so plants deploy predictive algorithms that shift load to cheaper tariff windows while maintaining specification limits. Published case studies report 10-20% reductions in energy use, which compounds as optimized operations extend maintenance intervals and lower unplanned downtime.

Integration of APC with IIoT & AI analytics

Low-latency industrial networks now connect sensors, controllers, and cloud engines, allowing machine-learning models to predict disturbances and prescribe corrective action before deviations propagate. The FDA's January 2025 guidance endorses AI-enabled real-time monitoring, removing a key adoption barrier for regulated manufacturers .

High upfront cost & integration complexity

Full-scale installations can demand USD 500,000-5 million, a hurdle for smaller plants. Brownfield sites often require instrument upgrades and DCS replacement, stretching schedules to 18 months and exposing operators to production-interruption risk.

Other drivers and restraints analyzed in the detailed report include:

- Emission-driven regulatory stringency

- Mega specialty-chemical & LNG project complexity

- Scarcity of APC talent & model upkeep

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Software captured 54% of the advanced process control market share in 2024, underscoring a decisive migration from hardware-centric systems to cloud-ready platforms. This segment is propelled by demand for rapid rollout, seamless DCS integration, and remote analytics that reduce capital intensity. Cloud-hosted solutions are forecast to grow at 12.9% CAGR through 2030 as subscription models lower entry barriers and provide continuous algorithm upgrades. Hardware remains indispensable for edge execution but is increasingly commoditized, while service contracts covering model maintenance and performance tuning expand as plants embrace continuous-improvement cultures. The shift enables vendors to release new optimization templates in weeks rather than months, accelerating digital-transformation roadmaps.

The advanced process control market size attributed to software is projected to expand from USD 1.7 billion in 2025 to USD 3.0 billion in 2030, reflecting pervasive adoption of microservices architectures and containerized deployment strategies. Edge gateways now route filtered data to cloud AI engines that feed real-time recommendations to on-premises controllers, balancing cybersecurity, latency, and regulatory constraints.

Model Predictive Control held 46% revenue in 2024, affirming its reputation as the primary tool for coordinating constrained, multi-variable processes. Linear MPC dominates large-scale continuous operations such as crude distillation and ethylene cracking, where thermodynamic relationships remain relatively stable. Non-linear MPC is gaining momentum, posting a 12.8% CAGR outlook, as specialty-chemical and pharmaceutical plants face non-steady-state reactions and strict quality windows.

The advanced process control market size for non-linear MPC is set to reach USD 1.1 billion by 2030, reflecting rising demand for algorithms capable of handling complex kinetics and variable feed compositions. Vendors differentiate by embedding adaptive modeling and self-tuning capabilities that respond to drift without manual intervention, allowing operators to maintain optimal performance with less engineering effort.

The Advanced Process Control Market is Segmented by Product Type (Advanced Regulatory Control, Model Predictive Control and More), by Component (Hardware and More), by Deployment Mode (On-Premise and More), by Process Type (Continuous Processes and More), by End-User Industry (Oil and Gas, Chemicals and Petrochemicals, and More), and by Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America commanded 37% of 2024 revenue, underpinned by early digitalization, abundant refinery capacity, and robust talent ecosystems. Federal energy-efficiency incentives and transparent carbon markets further encourage control upgrades. Asia-Pacific is the fastest-growing, with an 11.8% CAGR outlook, fuelled by China's 300 billion-yuan industrial-automation program (USD 41.7 billion) that prioritizes domestic technology self-reliance. India, Japan, and the ASEAN economies are following suit, targeting automation to manage labor constraints and productivity gaps.

Europe remains an innovation hotspot where stringent climate policy and the EU taxonomy link financing costs to measurable decarbonization. Plants exploit APC to cut Scope 1 emissions while safeguarding competitiveness. Meanwhile, the Middle East, Africa, and Latin America are rolling out cloud-native APC to leapfrog infrastructure limitations, with mining and LNG projects often serving as anchor use cases.

- ABB Ltd.

- Aspen Technology Inc.

- Emerson Electric Co.

- General Electric Co.

- Honeywell International Inc.

- Rockwell Automation Inc.

- Schneider Electric SE

- Siemens AG

- Yokogawa Electric Corp.

- SUPCON Technology Co. Ltd

- Hollysys Automation Technologies Ltd

- Endress+Hauser Group

- Valmet Oyj

- KBC Advanced Technologies

- Metso Outotec

- FLSmidth & Co. A/S

- AVEVA Group plc

- Azbil Corporation

- Endress+Hauser Group

- Valmet Oyj

- AVEVA Group plc

- Gensym Corporation

- ICONICS Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Real-time energy-cost optimisation needs

- 4.2.2 Integration of APC with IIoT & AI analytics

- 4.2.3 Emission-driven regulatory stringency

- 4.2.4 Mega specialty-chemical & LNG project complexity

- 4.2.5 Plug-and-play cloud APC for modular skids

- 4.2.6 Autonomous mining & metals operations push

- 4.3 Market Restraints

- 4.3.1 High upfront cost & integration complexity

- 4.3.2 Scarcity of APC talent & model upkeep

- 4.3.3 Cyber-security risks in remote/cloud APC

- 4.3.4 Weak ROI for small, high-mix batch plants

- 4.4 Value / Supply-Chain Analysis

- 4.5 Technological Outlook

- 4.6 Regulatory Landscape

- 4.7 Analysis of New APC Systems vs Modernization

- 4.8 Porters Five Forces

- 4.8.1 Bargaining Power of Suppliers

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitute Products

- 4.8.5 Degree of Competition

5 MARKET SIZE & GROWTH FORECASTS (VALUE)

- 5.1 By Component

- 5.1.1 Hardware

- 5.1.2 Software

- 5.1.3 Services

- 5.2 By Product Type

- 5.2.1 Advanced Regulatory Control (ARC)

- 5.2.2 Model Predictive Control (MPC)

- 5.2.3 Non-linear MPC

- 5.2.4 Multivariable Predictive Control

- 5.2.5 Inferential & Other Controls

- 5.3 By Deployment Mode

- 5.3.1 On-Premises

- 5.3.2 Cloud-based

- 5.3.3 Hybrid

- 5.4 By Process Type

- 5.4.1 Continuous Processes

- 5.4.2 Batch Processes

- 5.5 By End-user Industry

- 5.5.1 Oil & Gas

- 5.5.2 Chemicals & Petrochemicals

- 5.5.3 Pharmaceutical

- 5.5.4 Food & Beverage

- 5.5.5 Energy & Power

- 5.5.6 Cement

- 5.5.7 Metal Processing

- 5.5.8 Pulp & Paper

- 5.5.9 Others

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 South America

- 5.6.2.1 Brazil

- 5.6.2.2 Argentina

- 5.6.2.3 Rest of South America

- 5.6.3 Europe

- 5.6.3.1 Germany

- 5.6.3.2 United Kingdom

- 5.6.3.3 France

- 5.6.3.4 Italy

- 5.6.3.5 Russia

- 5.6.3.6 Rest of Europe

- 5.6.4 Asia

- 5.6.4.1 China

- 5.6.4.2 Japan

- 5.6.4.3 India

- 5.6.4.4 South Korea

- 5.6.4.5 Australia & New Zealand

- 5.6.4.6 Rest of Asia

- 5.6.5 Middle East and Africa

- 5.6.5.1 Middle East

- 5.6.5.1.1 Saudi Arabia

- 5.6.5.1.2 United Arab Emirates

- 5.6.5.1.3 Turkey

- 5.6.5.1.4 Rest of Middle East

- 5.6.5.2 Africa

- 5.6.5.2.1 South Africa

- 5.6.5.2.2 Nigeria

- 5.6.5.2.3 Rest of Africa

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.4.1 ABB Ltd.

- 6.4.2 Aspen Technology Inc.

- 6.4.3 Emerson Electric Co.

- 6.4.4 General Electric Co.

- 6.4.5 Honeywell International Inc.

- 6.4.6 Rockwell Automation Inc.

- 6.4.7 Schneider Electric SE

- 6.4.8 Siemens AG

- 6.4.9 Yokogawa Electric Corp.

- 6.4.10 SUPCON Technology Co. Ltd

- 6.4.11 Hollysys Automation Technologies Ltd

- 6.4.12 Endress+Hauser Group

- 6.4.13 Valmet Oyj

- 6.4.14 KBC Advanced Technologies

- 6.4.15 Metso Outotec

- 6.4.16 FLSmidth & Co. A/S

- 6.4.17 AVEVA Group plc

- 6.4.18 Azbil Corporation

- 6.4.19 Endress+Hauser Group

- 6.4.20 Valmet Oyj

- 6.4.21 AVEVA Group plc

- 6.4.22 Gensym Corporation

- 6.4.23 ICONICS Inc.

7 MARKET OPPORTUNITIES & FUTURE OUTLOOK

- 7.1 White-space & Unmet-Need Assessment