|

시장보고서

상품코드

1850218

방탄 조끼 시장 : 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Bulletproof Vest - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

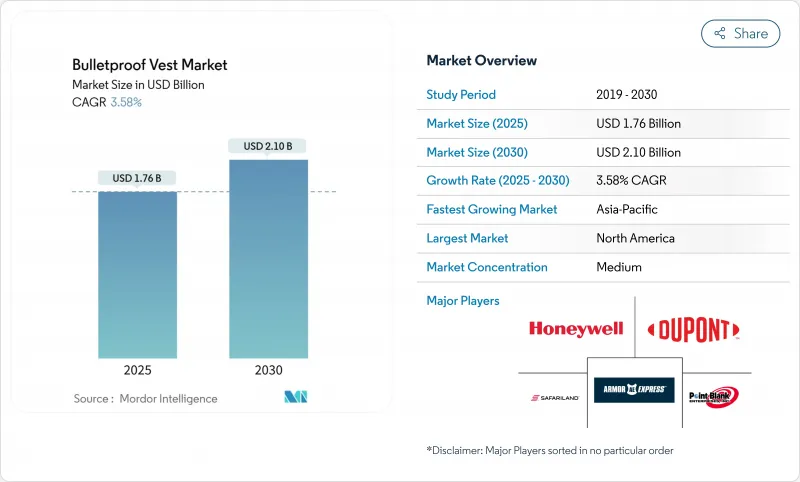

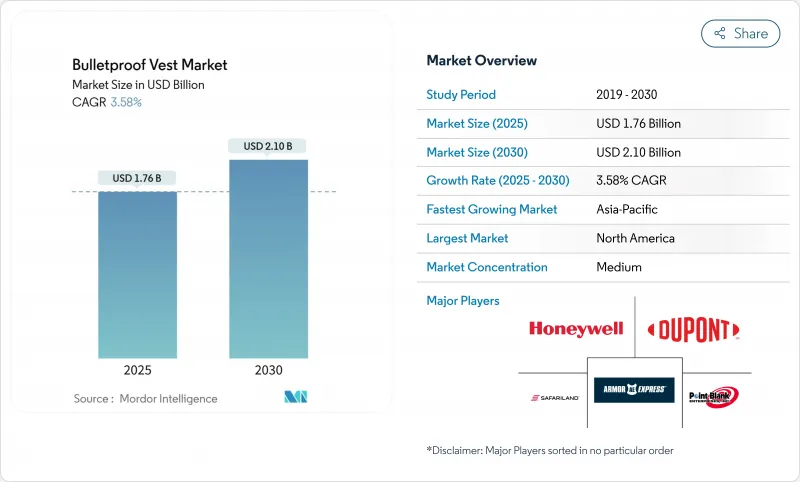

방탄조끼 시장은 2025년에는 17억 6,000만 달러, 2030년에는 21억 달러로 성장할 것으로 예측됩니다.

이는 조달 프로그램이 성숙하고 새로운 위협 프로파일이 출현함에 따라 CAGR이 3.58%가 되고 성장할 것으로 예상됩니다.

성장의 배경에는 유럽과 아시아태평양의 국방 근대화, 법 집행 기관에 의한 경량 소프트 아머의 급속한 채택, 보호와 기동성의 균형을 맞춘 소재 혁신, 교체 수요를 높인 인증 기준의 엄격화 등이 있습니다. 특히 북미와 서유럽의 행정보호지출 증가는 전통적인 군사바이어를 넘어 고객기반을 확대했습니다. 한편, 우크라이나 분쟁은 유럽의 조달 우선순위를 변화시켜, 현지 제조업체에 생산 능력의 확대를 촉구해, 복수회의 피탄을 상정한 레벨 IV 플레이트의 채택을 가속시켰습니다. 지속적인 원재료 가격 변동과 위조품의 스캔들은 눈앞의 성장을 약화했지만 NIJ 인증 정규품에 대한 수요에 박차를 가했습니다.

세계 방탄조끼 시장 동향과 통찰

격화하는 국방 근대화 계획

유럽, 아시아, 북미의 각 군은 생존성을 최우선으로 하는 대규모 재자본화 프로그램을 추진하여 차세대 플레이트와 경력의 수주를 촉진했습니다. 프랑스는 탄화붕소 인서트와 실시간 손상 센서를 갖춘 모듈형 G3P 시스템을 채택했으며 독일은 10만 벌의 MOBAST 베스트를 자국군에 지급했습니다. 캐나다가 1,970만 달러로 계약한 3,000벌의 고성능 세트는 현대화의 파도를 더욱 상징합니다. 이 프로그램은 모듈성, 군인 착용 센서와의 통합, 여성 군인을 포함한 다양한 체형에 대한 인체 공학적 조정을 강조하고 사용자 중심의 장갑 설계로의 체계적인 변화를 보여줍니다. 장기 자금 헌신은 단기 예산 변동으로부터 공급자를 보호했습니다.

법 집행 기관에 의한 경량 소프트 아머의 조달 증가

미국과 유럽 경찰은 NIJ 준수를 희생하지 않고 경찰의 피로를 줄이는 소프트 베스트 주문을 늘렸습니다. 듀폰의 케블러 EXO와 다이니마의 SB301은 기존의 원단에 비해 최대 30%의 경량화를 실현하여 일상복으로서의 채택이 퍼졌습니다. 업데이트된 NIJ 표준 0101.07은 성별 특화된 맞춤 테스트를 도입하여 조달 사양을 보다 다양한 노동력에 대응시켰습니다. 사법부의 현장 시험은 열 압력에 대한 우려를 없애고 승낙율을 증진시키는 현대 장갑을 착용하는 504명의 관리 중에서 무시할 수 있는 중핵 온도 증가를 찾아냈습니다. 이러한 요인들은 집합적으로 교체의 주기를 들고 지자체 기관에 걸친 백로그의 순서에 박차를 가했습니다.

휘발성 아라미드 및 UHMWPE 원료 가격

아라미드와 UHMWPE의 비용은 석유화학제품의 투입과 생산능력의 증강에 따라 급변하여 장기적인 공급계약을 맺지 않은 장갑조립업자의 마진을 압박했습니다. 듀폰이 2025년 1분기에 7억 6,800만 달러의 영업권 손상을 계상한 것으로, 레거시 아라미드 제품군의 수익성에 역풍이 불고 있는 것이 부각되었습니다. 중국의 UHMWPE 제조업체가 유럽과 미국의 라이벌보다 낮은 가격으로 인해 브랜드 공급업체는 품질 관리를 강화하고 PFAS가없는 화학 물질로 프리미엄을 정당화해야합니다. 조사 결과, 수지 파라미터의 변동이 섬유 탄성률에 직접 영향을 미치는 것으로 확인되어 스크랩 리스크가 높아져 품질 재가공시의 가공 비용이 상승했습니다. 그 결과 비용 전가에 의해 조달 예산이 압박되어 구매 사이클이 장기화되었습니다.

부문 분석

2024년 매출의 84.21%를 하드 컨피규레이션이 차지하고, 라이플 사격을 견디는 장갑 플레이트 캐리어를 선호하는 작전상의 우선순위가 확인되었습니다. 하드 베스트 방탄 조끼 시장 규모는 2030년까지 연평균 복합 성장률(CAGR) 3.66% 증가할 것으로 예측되어 철갑탄에 대한 복수 명중시의 생존성을 강조하는 전장에서의 보고에 뒷받침되었습니다. 군 바이어는 통신 라우팅, 외상 팩 및 식별 패널을 통합한 모듈식 캐리어를 찾아 기존 소프트 아머의 점유율을 압축했습니다.

소재의 진보는 무게 페널티를 줄여 보병이 부하의 임계치를 깨지 않고 사이드 플레이트나 삼각근 보호를 추가할 수 있도록 했습니다. 소프트 베스트는 은폐를 필요로 하는 복면 경찰이나 VIP의 세부사항에는 필수적이지만, 하드 플레이트의 경량화에 의해 기동성의 차이가 줄어들기 때문에 그 유닛 점유율은 축소되었습니다. 3D 니트 소재와 스페이서 메쉬는 소프트 캐리어 내부의 온도 조절을 개선하고 플레이트 포켓과 은폐 가능한 섬유를 융합시킨 미래의 크로스오버 제품을 제안했습니다.

아라미드는 2024년 매출액의 53.56%를 차지했지만 UHMWPE는 비에너지 흡수율이 높고 해상 임무용 부력도 있기 때문에 CAGR 4.12%로 급상승했습니다. PPTA/UHMWPE 적층은 단섬유 적층을 능가하고 NIJ RF1 시험에서 하이브리드 적층이 최적의 이면 변형 제어를 제공한다는 것을 입증했습니다. 다이니마의 PFAS 비함유 등급은 화학물질 안전규제가 강화된 유럽 구매자를 매료시켰습니다.

정유소의 가동정지와 운임 불안정성이 원료비용을 흔들었기 때문에 가격변동이 UHMWPE 채택의 발판이 되었습니다. 그럼에도 불구하고 공급업체는 판재 조립업체와 장기 인수 계약을 체결하고 수량 할인을 확보하고 스팟 시장 급등으로부터 프로그램을 보호했습니다. 사슬 뭉치와 같은 2차원 폴리머의 연구는 다음의 도약을 말하는 것으로, 47배의 강성 향상과 현대의 UHMWPE 시트 이하의 중량을 약속하는 것입니다.

지역 분석

북미는 지속적인 연방정부 보조금과 대기업청 기업에 대한 근접성이 구매량을 지지하고 있기 때문에 2024년 세계 매출의 42.29%를 유지했습니다. Point Blank과 Safariland는 수직 통합을 활용하여 리드 타임을 단축했습니다. 한편 미국의 리쇼어링 이니셔티브는 새로운 방위산업시설에서 사이트 보안에 대한 지출이 증가했고, 한 도시권 내에서 보안 리스크 점수가 75포인트나 다른 곳도 있었습니다. 캐나다에서는 2025년 계약 획득을 통해 2026년 납입 예정인 모듈식 플레이트 운반선이 지역적으로 공급될 것이 확정되었습니다.

아시아태평양의 2030년까지의 CAGR은 3.90%를 나타내고, 이는 동아시아의 방위 예산이 전년대비 6.2% 증가하여 인도, 중국, 한국에서 국산화가 확대된 것에 따릅니다. MKU의 Kavro Doma 360 헬멧 주문은 이 지역이 최전선 부대의 신속한 배송 목표를 충족하는 현지화된 공급망을 선호한다는 것을 보여줍니다. 중국의 UHMWPE 수출업체는 가격 경쟁을 추진하고 능력과 예산의 상한을 균형화하는 동남아시아 신흥 구매자의 가격 감각을 높였습니다.

우크라이나 전쟁이 탄약과 장갑 부족을 유발한 후 유럽에서는 구조적 재조합이 이루어졌으며 EU는 5억 유로 상당의 자금을 제공하여 보호복 제조 라인 등의 방위 제조를 강화했습니다. 독일이 10만 벌의 MOBAST를 납품하고 프랑스가 G3P 베스트를 전개한 것은 NATO STANAG 사양에 적합한 국산 솔루션에 대한 대륙의 헌신을 나타냈습니다. 불가리아의 150,000 평방미터의 새로운 공장은 유럽 공급업체의 다양성을 확대하고 장기 생산량에 대한 투자자의 신뢰를 보여주었습니다. 영국에서 진행 중인 리콜은 컴플라이언스 갭을 부각시켜 각 기관에 NATO 인증 실험실에서 집중 테스트를 촉구했습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 서포트

목차

제1장 서론

- 조사의 전제조건과 시장의 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 시장 성장 억제요인

- 밸류체인 분석

- 규제 상황

- 기술의 전망

- Porter's Five Forces 분석

- 구매자의 협상력

- 공급기업의 협상력

- 신규 참가업체의 위협

- 대체품의 위협

- 경쟁 기업간 경쟁 관계

제5장 시장 규모와 성장 예측

- 제품 유형별

- 소프트 베스트

- 하드 베스트

- 소재별

- 아라미드 섬유

- UHMWPE-textiles

- 세라믹 및 복합재 인서트

- 철강 및 기타 재료

- 보호 레벨별

- 레벨 II

- 레벨 IIIA

- 레벨 III

- 레벨 IV

- 최종 사용자별

- 군

- 민간 및 법 집행기관

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 영국

- 독일

- 프랑스

- 이탈리아

- 스페인

- 러시아

- 기타 유럽

- 아시아태평양

- 중국

- 인도

- 일본

- 한국

- 호주

- 기타 아시아태평양

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 중동 및 아프리카

- 중동

- 사우디아라비아

- 아랍에미리트(UAE)

- 튀르키예

- 기타 중동

- 아프리카

- 남아프리카

- 기타 아프리카

- 북미

제6장 경쟁 구도

- 시장 집중도

- 전략적 동향

- 시장 점유율 분석

- 기업 프로파일

- Point Blank Enterprises, Inc.

- Safariland, LLC

- Central Lake Armor Express, Inc.

- MKU Limited

- EnGarde BV

- ELMON SA

- US Armor Corporation

- DuPont de Nemours, Inc.

- Honeywell International Inc.

- Hardshell Ltd.

- Indian Armour Systems Pvt. Ltd.

- ARGUN sro

- Seyntex NV

- MARS Armor

- Zhejiang Hua An Safety Equipment Co. Ltd.

- Survival Armor

- GARED sro

제7장 시장 기회와 장래의 전망

SHW 25.11.11The bulletproof vest market stood at USD 1.76 billion in 2025 and is forecast to rise to USD 2.10 billion by 2030, reflecting a 3.58% CAGR that signals measured expansion as procurement programs mature and new threat profiles emerge.

Growth hinged on defense modernization in Europe and Asia-Pacific, rapid adoption of lightweight soft armor by law enforcement agencies, material innovations that balanced protection with mobility, and tighter certification standards that raised replacement demand. Rising executive protection spending, particularly in North America and Western Europe, broadened the customer base beyond traditional military buyers. Meanwhile, the Ukraine conflict reshaped European procurement priorities, prompting local manufacturers to scale capacity and accelerating the adoption of Level IV plates for multi-hit scenarios. Ongoing raw-material price swings and counterfeit equipment scandals tempered near-term growth yet spurred demand for authenticated, NIJ-certified gear.

Global Bulletproof Vest Market Trends and Insights

Escalating Defense Modernization Programs

European, Asian, and North American armies pursued large-scale re-capitalization programs prioritizing survivability, driving orders for next-generation plates and carriers. France adopted the modular G3P system with boron-carbide inserts and real-time damage sensors, while Germany delivered 100,000 MOBAST vests to its troops, underscoring demand for scalable, technology-enabled solutions. Canada's USD 19.7 million contract for 3,000 advanced sets further exemplified the modernization wave. These programs emphasized modularity, integration with soldier-worn sensors, and ergonomic adjustments for diverse body types, including female personnel, indicating a systemic shift toward user-centric armor design. Long-run funding commitments sheltered suppliers from short-term budget volatility.

Rising Procurement of Lightweight Soft Armor by Law Enforcement

Police departments in the United States and Europe increased orders for soft vests that cut officer fatigue without sacrificing NIJ compliance. DuPont's Kevlar EXO and Dyneema's SB301 reduced weight by up to 30% compared with prior fabrics, widening daily-wear adoption. Updated NIJ Standard 0101.07 introduced gender-specific fit testing that aligned procurement specifications with a more diverse workforce. Department of Justice field trials found negligible core-temperature increases among 504 officers wearing modern armor, dispelling heat-stress concerns and strengthening compliance rates. These factors collectively lifted replacement cycles and spurred backlog orders across municipal agencies.

Volatile Aramid and UHMWPE Raw Material Prices

Aramid and UHMWPE costs swung sharply with petrochemical inputs and capacity additions, compressing margins for armor assemblers that lacked long-term supply pacts. DuPont's USD 768 million goodwill impairment in Q1 2025 highlighted profitability headwinds inside legacy aramid lines. Chinese UHMWPE makers undercut Western rivals on price, forcing brand-name suppliers to justify premiums through tighter quality control and PFAS-free chemistries. Research confirmed that resin-parameter variance directly affected fiber modulus, elevating scrap risk and raising processing costs during quality re-work. The resulting cost pass-through squeezed procurement budgets and elongated purchasing cycles

Other drivers and restraints analyzed in the detailed report include:

- Growing Demand for Female-Fit Ballistic Vests

- Adoption of Multi-Hit Ceramic-UHMWPE Hybrid Plates

- Proliferation of Counterfeit/Uncertified Body-Armor Products

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Hard configurations captured 84.21% of 2024 sales, confirming operational priorities that favored armored plate carriers able to withstand rifle fire. The bulletproof vest market size for hard vests was expected to increase by 3.66% CAGR to 2030, fueled by battlefield reports emphasizing multi-hit survivability against armor-piercing rounds. Military buyers demanded modular carriers that integrated communications routing, trauma packs, and identification panels, compressing legacy soft-armor share.

Material advances trimmed weight penalties, allowing infantry to add side plates or deltoid protection without breaching load thresholds. Soft vests remained essential for undercover police and VIP details that required concealment, yet their unit share contracted as weight savings in hard plates narrowed the mobility gap. 3D-knit fabrics and spacer meshes improved thermal regulation inside soft carriers, hinting at future crossover products that merge plate pockets with concealable textiles.

Aramid preserved 53.56% of 2024 revenues, but UHMWPE climbed fastest at a 4.12% CAGR on the strength of higher specific energy absorption and buoyancy for maritime missions. PPTA/UHMWPE laminates outperformed single-fiber layups, demonstrating that hybrid stacks supplied optimal back-face deformation control during NIJ RF1 trials. Dyneema's PFAS-free grades attracted buyers in Europe, where chemical-safety rules tightened.

Price volatility remained a drag on UHMWPE adoption because refinery outages and freight instability jolted feedstock costs. Still, suppliers secured long-term offtake agreements with plate assemblers, locking in volume discounts and shielding programs from spot-market spikes. Research into chainmail-like 2D polymers signaled the next leap, promising 47-fold stiffness gains and weights below contemporary UHMWPE sheets.

The Bulletproof Vest Market Report is Segmented by Type (Soft Vest and Hard Vest), Material (Aramid Fibers, UHMWPE Fibers, Ceramic and Composite Inserts, and More), Protection Level (Level II, Level IIIA, and More), End User (Military and Civilian, and Law Enforcement ), and Geography (North America, Europe, South America, Asia-Pacific, and the Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America retained 42.29% of global sales in 2024 as sustained federal grants and proximity to major prime contractors anchored purchase volumes. Point Blank and Safariland exploited vertical integration to compress lead times. At the same time, US reshoring initiatives heightened site-security spending across new defense-industrial facilities, and some faced 75-point differences in security risk scores within a single metro area. Canada's 2025 contract award confirmed a regional pipeline of modular plate carriers with delivery slated for 2026.

Asia-Pacific charted a 3.90% CAGR to 2030, propelled by 6.2% year-on-year growth in East-Asian defense budgets and indigenous production scale-ups in India, China, and South Korea. MKU's Kavro Doma 360 helmet order illustrated the region's preference for localized supply chains that met fast-track delivery targets for frontline units. Chinese UHMWPE exporters drove price competition, enhancing affordability for emerging Southeast-Asian buyers who balanced capability with budget caps.

Europe underwent structural realignment after the Ukraine war sparked ammunition and armor shortages, prompting EU funding worth EUR 500 million to boost defense manufacturing, including body armor fabrication lines. Germany's 100,000-unit MOBAST delivery and France's roll-out of the G3P vest indicated continental commitment to home-grown solutions that met NATO STANAG specifications. Bulgaria's new 150,000 m2 plant broadened European supplier diversity and signaled investor confidence in long-run volume. Ongoing recalls in the United Kingdom highlighted compliance gaps that encouraged agencies to centralize testing at NATO-accredited labs.

- Point Blank Enterprises, Inc.

- Safariland, LLC

- Central Lake Armor Express, Inc.

- MKU Limited

- EnGarde B.V.

- ELMON S.A.

- U.S. Armor Corporation

- DuPont de Nemours, Inc.

- Honeywell International Inc.

- Hardshell Ltd.

- Indian Armour Systems Pvt. Ltd.

- ARGUN s.r.o.

- Seyntex N.V.

- MARS Armor

- Zhejiang Hua An Safety Equipment Co. Ltd.

- Survival Armor

- GARED s.r.o.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Escalating defense modernization programs

- 4.2.2 Rising procurement of lightweight soft armor by law-enforcement

- 4.2.3 Growing demand for female-fit ballistic vests

- 4.2.4 Adoption of multi-hit ceramic-UHMWPE hybrid plates

- 4.2.5 Intensifying geopolitical conflicts and territorial disputes

- 4.2.6 Expansion of private security and VIP protection industry

- 4.3 Market Restraints

- 4.3.1 Volatile aramid and UHMWPE raw-material prices

- 4.3.2 Stringent export licensing for ballistic products

- 4.3.3 Heat-stress and back-face deformation concerns in tropical climates

- 4.3.4 Proliferation of counterfeit / uncertified body-armor products

- 4.4 Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Buyers

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitute Products

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Product Type

- 5.1.1 Soft Vest

- 5.1.2 Hard Vest

- 5.2 By Material

- 5.2.1 Aramid Fibers

- 5.2.2 UHMWPE Fibers

- 5.2.3 Ceramic and Composite Inserts

- 5.2.4 Steel and Other Materials

- 5.3 By Protection Level

- 5.3.1 Level II

- 5.3.2 Level IIIA

- 5.3.3 Level III

- 5.3.4 Level IV

- 5.4 By End User

- 5.4.1 Military

- 5.4.2 Civilian and Law Enforcement

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 United Kingdom

- 5.5.2.2 Germany

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Russia

- 5.5.2.7 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 India

- 5.5.3.3 Japan

- 5.5.3.4 South Korea

- 5.5.3.5 Australia

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Argentina

- 5.5.4.3 Rest of South America

- 5.5.5 Middle East and Africa

- 5.5.5.1 Middle East

- 5.5.5.1.1 Saudi Arabia

- 5.5.5.1.2 United Arab Emirates

- 5.5.5.1.3 Turkey

- 5.5.5.1.4 Rest of Middle East

- 5.5.5.2 Africa

- 5.5.5.2.1 South Africa

- 5.5.5.2.2 Rest of Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Point Blank Enterprises, Inc.

- 6.4.2 Safariland, LLC

- 6.4.3 Central Lake Armor Express, Inc.

- 6.4.4 MKU Limited

- 6.4.5 EnGarde B.V.

- 6.4.6 ELMON S.A.

- 6.4.7 U.S. Armor Corporation

- 6.4.8 DuPont de Nemours, Inc.

- 6.4.9 Honeywell International Inc.

- 6.4.10 Hardshell Ltd.

- 6.4.11 Indian Armour Systems Pvt. Ltd.

- 6.4.12 ARGUN s.r.o.

- 6.4.13 Seyntex N.V.

- 6.4.14 MARS Armor

- 6.4.15 Zhejiang Hua An Safety Equipment Co. Ltd.

- 6.4.16 Survival Armor

- 6.4.17 GARED s.r.o.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment