|

시장보고서

상품코드

1850233

외래 전자 건강 기록(EHR) 시장 : 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Ambulatory EHR - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

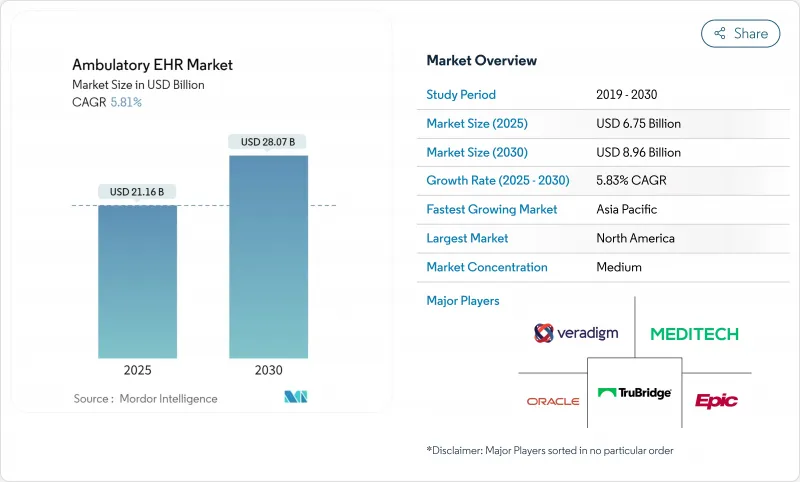

외래 전자 건강 기록(EHR) 시장 규모는 현재 67억 5,000만 달러, 2030년에는 89억 6,000만 달러에 이르고, 기간 중 CAGR은 5.83%를 나타낼 전망입니다.

정보 차단에 대한 규제 당국의 벌칙 강화, 새로운 고급 1차 케어 관리 청구 코드, 어카운터블 케어 계약 확대로 레거시 기록 시스템에 의존하는 의료 제공업체의 부담이 증가하고 있습니다. 클라우드로의 전환은 여전히 주류이며 대규모 정보 유출 사건으로 인해 보안 격차가 드러나더라도 신속한 확장성과 낮은 자본 지출을 실현합니다. 문서화 시간을 단축하고 위험 계층화를 개선하는 인공지능 모듈은 현재 고전적인 기능 세트보다 구매 결정에 영향을 미치고 있습니다. 공급업체는 상호 운용성, 원격 의료 워크플로우 및 앰비언트 리스닝 도구를 대규모 의료 시스템과 소규모 독립 클리닉 모두를 지원하는 통합 플랫폼에 통합하려고 경쟁하고 있습니다.

세계 외래 전자 건강 기록(EHR) 시장 동향과 통찰

정부 인센티브와 컴플라이언스 의무화가 시장 확대를 촉진

EHR 정책에서는 이제 벌칙이 보상을 능가하고 있습니다. 21세기 치료법(21st Century Cures Act)에서 정보를 차단한 의료기관은 최대 5%의 메디케어 지급 삭감, 공유 저축 프로그램에서 제외, 풍평 피해 등의 위험을 겪게 됩니다. 2025년 품질 지불 프로그램은 7가지 새로운 품질 지표를 도입하여 보다 상세한 전자 임상 보고를 요구합니다. CMS는 또한 환자 접근을 위해 FHIR 대응 API를 요구하고 있으며, 이 규칙은 이미 73%의 디지털 헬스 기업이 충족하고 있지만 여전히 고액의 도입 비용이 부담되고 있습니다. 그 결과, 외래 전자 건강 기록(EHR)시장은 늦은 클리닉과 소규모 전문 클리닉 간의 컴플라이언스 주도 리플레이스 사이클에서 이익을 얻고 있습니다.

클라우드 마이그레이션 기세, 강화되는 보안 요건 상쇄

클라우드 환경은 하드웨어 비용을 낮추고 업데이트를 가속화하지만 공격 대상은 확대됩니다. HHS 시민권국은 2024년에 626건의 심각한 정보 유출을 기록했으며 4,170만 명에 영향을 주었습니다. 2024년 2월에 발생한 변경 건강 관리의 랜섬웨어 공격은 미국의 청구 트래픽의 절반을 방해하여 중앙 집중식 데이터 처리의 시스템적 위험을 부각시켰습니다. 공급업체는 현재 다중 요소 인증, 지속적인 모니터링, 제로 트러스트 아키텍처를 공급업체 계약의 양도할 수 없는 조건으로 요구하고 있으며, 주요 플랫폼에 탄력성을 부여함으로써 보다 이익률이 높은 보안 서비스 계층을 지원하고 있습니다.

사이버 보안 취약점으로 클라우드 배포 속도를 억제

Change Healthcare의 ALPHV 랜섬웨어 침해는 미국 의사 진료소의 80%에 수익 손실을 초래하여 2,200만 달러의 몸값 지불을 요구했지만, 여전히 몇 주간의 지불 지연이 발생했습니다. 이러한 사건은 분산형 데이터 스토리지 및 멀티클라우드 장애 조치 전략을 요구하는 목소리에 박차를 가하지만 소규모 공급업체는 이를 완전히 도입하는 예산과 직원이 부족한 경우가 많습니다. 그 결과 클라우드 마이그레이션을 앞당기고 하이브리드 아키텍처를 점진적으로 선택하는 기업도 있어 외래 전자 건강 기록(EHR)시장 전체의 성장 궤도는 둔화되고 있습니다.

부문 분석

2024년 외래 전자 건강 기록(EHR)시장 점유율은 진료 관리 모듈이 24.64%를 차지했습니다. 이는 결제, 스케줄링 및 자격 검사에서 중요한 역할을 반영합니다. 그러나 집단건강관리의 외래 전자 건강 기록(EHR)시장 규모는 2030년까지 연평균 복합 성장률(CAGR) 6.47%로 확대될 것으로 예측되며, 적극적인 만성기 케어 모니터링에 보답하는 리스크 기반 상환으로 박차가 걸립니다. 공급업체는 현재 인공지능 리스크 계층화를 집단 대시보드에 통합하여 소규모 그룹이 직원을 늘리지 않고도 복잡한 환자 패널을 관리할 수 있도록 하고 있습니다. 소개 관리 도구는 현재 Trusted Exchange Framework 및 Common Agreement를 통해 의료 정보 교환 기관과 통합되어 네트워크를 가로지르는 환자의 환자 여정를 파악할 수 있도록 되어 있습니다. 심장 종양학에서 피부과학에 이르는 전문 모듈은 대규모 코드 재작성 없이 전환 가능한 AI 대응 애드온으로 등장하여 플랫폼 벤더에 새로운 수익 트랙을 구축하고 있습니다.

포퓰레이션 헬스 대시보드는 환자 1인당 월15달러에서 110달러까지 확장하는 첨단 1차 케어 매니지먼트의 상환으로부터 직접 이익을 얻을 수 있습니다. 리스크 기반 아웃리치 및 후속 프로토콜을 입증하는 클리닉은 거의 즉시 투자 회수가 가능하기 때문에 이 용도 부문은 외래 전자 건강 기록(EHR)시장 내에서 업그레이드의 강한 견인 역할을 하고 있습니다. 클라우드 호스팅은 인프라 비용을 절감하기 때문에 한 곳의 의사 그룹이라도 한때 기업 시스템 전용이었던 분석 엔진에 적당한 가격으로 접근할 수 있어 예측 기간 동안 시장의 보급이 진행됩니다.

2024년 외래 전자 건강 기록(EHR)시장 규모에서 차지하는 클라우드 호스팅 비율은 77.58%로 CAGR 6.25%로 추이할 것으로 예측되고 있습니다. Epic, Oracle, athenahealth의 퍼블릭 클라우드 인스턴스는 소비 기반 가격 설정, 지속적인 버전 업데이트 및 턴키 분석을 제공하지만, 2024년 랜섬웨어 사건을 통해 고객은 공유 책임 조항을 검토하고, 외부 침입 테스트를 실시하고, 계약에서 사이버 배상 책임 특약의 요구를 강요했습니다. On-Premise 솔루션은 특히 임상 연구 데이터를 관리하는 학술 의료 그룹과 같은 데이터 주권에 대한 요구가 높은 소수공급자에게는 여전히 적절한 솔루션입니다. 그러나 클라우드의 보안 관리가 성숙함에 따라 그 점유율은 떨어질 것으로 보입니다.

핵심 의료 기록의 로컬 사본을 유지하면서 클라우드 분석의 탄력성을 추구하는 대규모 의료 시스템 간에는 하이브리드 모델이 급속히 상승하고 있습니다. 이 아키텍처는 단일 장애 지점(single-point-of-failure)의 위험을 줄이고 신속한 재해 복구 옵션을 가능하게 합니다. 또한 의료 시점에서 '에지 AI' 추론을 지원하고 의사 결정 지원 도구의 대기 시간을 단축합니다. 이러한 구조적 변화는 클라우드 보안의 실적이 있고 상호 운용성이 높고 세계적인 규모의 벤더에게 유리한 승자가 가장 유리한 역동성을 강화하는 것입니다.

지역 분석

북미는 2024년 매출의 40.32%를 차지했으며, 디지털화에서 최적화로의 전환에 따라 CAGR 5.52%로 성장할 것입니다. CMS의 새로운 규칙은 180일간의 EHR 보고 창과 eCQM 제출의 확대를 의무화하고 있으며, 공급자는 볼트 온 모듈을 네이티브 상호 운용 가능한 대체품으로 대체해야 합니다. AI의 도입은 특히 활발하며, 30개 이상의 의료 시스템이 앰비엔트리 스닝을 대규모로 도입하고, 의사의 문서 작성 시간을 단축하고, 시스템 갱신의 ROI 계산을 높이고 있습니다. 미국의 소규모 진료소는 종단적인 케어 조정 활동을 상환하는 코드에서 새로운 인센티브를 얻고 있으며, 지방 주에서도 시장 진입이 확산되고 있습니다.

아시아태평양은 CAGR 7.09%로 가장 급성장하고 있으며 인도, 호주, 일본이 이를 지원하고 있습니다. 인도의 Ayushman Bharat Digital Mission은 5억 6,800만건의 건강 계정을 등록했지만, 연결 문제와 언어 다양성으로 인해 EHR의 적극적인 활용으로 이어지는 것은 단지 일부에 불과합니다. 네트워크 업그레이드 및 장비 조달에 대한 정부 보조금이 이 격차를 메우기 시작했습니다. 중국과 한국은 AI 기반의 의료 분석에 적극적으로 보조금을 내고 있어 머신러닝 파이프라인을 통합한 클라우드 호스트의 외래 시스템에 대한 그린필드 수요를 창출하고 있습니다. 이러한 추세로 인해 지역은 예측 기간 동안 외래 전자 건강 기록(EHR) 시장에서 가장 큰 수익 증가 요인이 될 것입니다.

유럽은 CAGR 5.89%로 성장하여, 국경을 넘어서는 데이터 공유를 중시하는 독일, 프랑스, 북유럽 국가 e헬스 계획에 지지되고 있습니다. GDPR(EU 개인정보보호규정) 준수는 엄격한 액세스 제어 및 감사 로깅을 부과하기 때문에 조달은 강력한 프라이버시 프레임워크가 있는 유명한 공급업체를 기울입니다. 중동 및 아프리카는 CAGR 6.41%로 성장하고 있으며, 사우디아라비아와 아랍에미리트(UAE)의 원격 의료 프로그램이 환자가 생성한 데이터를 직접 외래 기록에 반영하는 데 도움이 되고 있습니다. 남미는 CAGR 6.04%로 성장하고 있으며 브라질이 공공 의료보고 포털과 통합하는 클라우드 네이티브 EHR에 대한 투자를 선도하고 있습니다. 신흥 시장 전체에서는 인프라 격차가 여전히 제약을 받고 있습니다. 그러나 멀티 테넌트 퍼블릭 클라우드의 도입과 모바일 퍼스트 프론트엔드는 비용 효율적인 해결 방법을 제공하여 외래 전자 건강 기록(EHR) 시장의 장기적인 전망을 강화하고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 서포트

목차

제1장 서론

- 조사의 전제조건과 시장의 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 정부 인센티브와 컴플라이언스 의무

- 클라우드 호스팅 EHR로의 전환 가속

- 상호 운용 가능한 데이터를 요구하는 가치 기반 케어의 추진

- 업그레이드를 강화하는 전문 분야의 AI 모듈

- 원격 의료 워크플로우를 EHR 플랫폼에 통합

- 원격 모니터링과 외래 환자의 데이터 수집에 대한 상환

- 시장 성장 억제요인

- 사이버 보안과 프라이버시 침해 우려

- 신흥국에서의 인프라의 불균형

- 복잡한 복수 관할 구역의 규제 준수

- 타사 통합의 종량 과금제 API 비용 상승

- 기술의 전망

- Porter's Five Forces 분석

- 신규 참가업체의 위협

- 구매자의 협상력

- 공급기업의 협상력

- 대체품의 위협

- 경쟁 기업간 경쟁 관계

제5장 시장 규모와 성장 예측

- 용도별

- 진료 관리

- 환자 관리

- 전자 처방

- 소개 관리

- 인구건강관리

- 기타

- 배송 방법별

- 클라우드 기반 솔루션

- On-Premise 솔루션

- 하이브리드 솔루션

- 진료소의 규모별

- 대규모 진료소

- 중규모 진료소

- 소규모 진료소

- 최종 사용자별

- 병원 소유의 외래 센터

- 독립 외래 센터

- 의료 시스템 제휴 의사 그룹

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 기타 유럽

- 아시아태평양

- 중국

- 인도

- 일본

- 호주

- 한국

- 기타 아시아태평양

- 중동 및 아프리카

- GCC

- 남아프리카

- 기타 중동 및 아프리카

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 북미

제6장 경쟁 구도

- 시장 집중도

- Competitive Benchmarking

- 시장 점유율 분석

- 기업 프로파일

- AdvancedMD, Inc.

- athenahealth Inc.

- Azalea Health Innovations, Inc.

- CompuGroup Medical SE & Co. KGaA

- CureMD.com, Inc.

- eClinicalWorks, LLC

- Epic Systems Corporation

- EverHealth Solutions Inc.

- Greenway Health LLC

- Infor-Med, Inc.(Praxis EMR)

- Kareo, Inc.

- MEDHOST, Inc.

- Medical Information Technology, Inc.(Meditech)

- Modernizing Medicine, Inc.(ModMed)

- NextGen Healthcare, Inc.

- Oracle Corporation

- PointClickCare Technologies Inc.

- Practice Fusion, Inc.

- TruBridge, Inc.

- Veradigm Inc.

제7장 시장 기회와 장래의 전망

SHW 25.11.11The ambulatory EHR market size is currently valued at USD 6.75 billion and is forecast to reach USD 8.96 billion by 2030, advancing at a 5.83% CAGR through the period.

Accelerating regulatory penalties for information blocking, new Advanced Primary Care Management billing codes, and expansion of accountable-care contracts raise the stakes for providers that still rely on legacy record systems. Cloud migration remains the dominant deployment choice, delivering rapid scalability and lower capital outlays even as high-profile breaches expose security gaps. Artificial-intelligence modules that shorten documentation time and improve risk stratification now influence buying decisions more than classic feature sets. Competitive intensity is sharpening, with vendors racing to combine interoperability, telehealth workflows, and ambient listening tools into cohesive platforms that serve both large health systems and small independent practices.

Global Ambulatory EHR Market Trends and Insights

Government Incentives & Compliance Mandates Drive Market Expansion

Penalties now outweigh rewards in EHR policy. Under the 21st Century Cures Act, providers that block information risk up to a 5% Medicare payment cut, potential removal from the Shared Savings Program, and reputational harm. The 2025 Quality Payment Program introduces seven new quality measures that demand deeper electronic clinical-quality reporting. CMS also requires FHIR-enabled APIs for patient access, a rule already met by 73% of digital-health firms but still burdened by high implementation fees. As a result, the ambulatory EHR market benefits from a compliance-driven replacement cycle among laggard practices and smaller specialty clinics.

Cloud Migration Momentum Offset by Escalating Security Imperatives

Cloud environments lower hardware costs and speed updates, yet they expand the attack surface. The HHS Office for Civil Rights logged 626 significant breaches in 2024, affecting 41.7 million individuals; hacking accounted for 74% of incidents and network servers were the prime vector. The February 2024 Change Healthcare ransomware attack, which disrupted half of U.S. claims traffic, underscored the systemic risks of centralized data processing. Providers now demand multi-factor authentication, continuous monitoring, and zero-trust architectures as non-negotiables in vendor contracts, supporting a higher-margin security-services layer that adds stickiness to leading platforms.

Cyber-Security Vulnerabilities Constrain Cloud Adoption Velocity

The ALPHV ransomware breach at Change Healthcare triggered revenue losses for 80% of U.S. physician practices and required a USD 22 million ransom payment, yet still produced multi-week payment delays. Such events spur calls for distributed-ledger data storage and multi-cloud fail-over strategies, but smaller providers often lack the budgets or staff to implement them fully. As a result, some organizations postpone cloud migrations, opting for incremental hybrid architectures that slow overall ambulatory EHR market growth trajectory.

Other drivers and restraints analyzed in the detailed report include:

- Value-Based Care Integration Accelerates Interoperability Demands

- AI-Powered Clinical Documentation Transforms Workflow Economics

- Infrastructure Disparities Limit Emerging-Market Penetration

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Practice-management modules captured 24.64% of the ambulatory EHR market share in 2024, reflecting their vital role in billing, scheduling, and eligibility checks. However, the ambulatory EHR market size for population-health management is projected to expand at 6.47% CAGR through 2030, spurred by risk-based reimbursement that rewards proactive chronic-care oversight. Vendors now embed AI-driven risk stratification into population dashboards, enabling small groups to manage complex patient panels without adding staff. Referral-management tools now integrate with health-information exchanges via the Trusted Exchange Framework and Common Agreement, positioning them to capture cross-network patient journeys. Specialty modules ranging from cardio-oncology to dermatology are emerging as AI-ready add-ons that can be switched on without major code rewrites, laying fresh revenue tracks for platform vendors.

Population-health dashboards benefit directly from Advanced Primary Care Management reimbursements that scale from USD 15 to USD 110 per patient per month. Clinics that demonstrate risk-based outreach and follow-up protocols see near-immediate return on investment, making this application segment the strongest pull for upgrades inside the ambulatory EHR market. As cloud hosting trims infrastructure costs, even single-site physician groups gain affordable access to analytics engines once reserved for enterprise systems, deepening market diffusion over the forecast horizon.

Cloud-hosted deployments accounted for 77.58% of the ambulatory EHR market size in 2024, and the segment is set to advance at a 6.25% CAGR. Public-cloud instances from Epic, Oracle, and athenahealth offer consumption-based pricing, rolling version updates, and turnkey analytics, but 2024's ransomware events forced customers to scrutinize shared-responsibility clauses, conduct external penetration tests, and demand cyber-liability riders in contracts. On-premise solutions remain relevant to a minority of providers with heightened data-sovereignty needs, particularly academic medical groups that manage clinical-research data. Still, their share will keep eroding as cloud security controls mature.

Hybrid models are rising quickly among large health systems that want the elasticity of cloud analytics while retaining a local copy of core health records. This architecture mitigates single-point-of-failure risk and enables rapid disaster-recovery options. It also supports "edge-AI" inference at the point of care, reducing latency for decision support tools. These structural shifts reinforce a winner-takes-most dynamic that favors vendors with proven cloud security track records, deep interoperability credentials, and global scale.

The Ambulatory EHR Market Report is Segmented by Application (Practice Management, Patient Management, and More), by Delivery Mode (Cloud-Based Solutions and More), by Practice Size (Large Practices, Medium-Sized Practices, Small Practices), by End-User (Hospital-Owned Ambulatory Centers and More), and Geography (North America, Europe, Asia-Pacific, and More). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America accounted for 40.32% of 2024 revenue and will grow at 5.52% CAGR as the market transitions from digitization to optimization. New CMS rules mandate a 180-day EHR-reporting window and expanded eCQM submissions, compelling providers to replace bolt-on modules with natively interoperable alternatives. AI uptake is particularly robust; more than 30 health systems have deployed ambient listening at scale, shaving physician documentation time and elevating the ROI calculus for system refreshes. Smaller U.S. practices gain fresh incentives from codes that reimburse longitudinal care-coordination activities, widening market participation across rural states.

Asia-Pacific is the fastest-growing region at 7.09% CAGR, underpinned by India, Australia, and Japan. India's Ayushman Bharat Digital Mission registered 568 million health accounts, yet only a fraction translates to active EHR utilization because of patchy connectivity and language diversity. Government subsidies for network upgrades and device procurement are beginning to bridge this gap. China and South Korea aggressively subsidize AI-based medical analytics, creating green-field demand for cloud-hosted ambulatory systems that ship with built-in machine-learning pipelines. These trends position the region as the largest incremental revenue pool for the ambulatory EHR market during the forecast period.

Europe shows a 5.89% CAGR, supported by national e-health plans in Germany, France, and the Nordics that emphasize cross-border data sharing. GDPR compliance imposes rigid access controls and audit logging, tilting procurement toward established vendors with robust privacy frameworks. Middle East & Africa follow at 6.41% CAGR, helped by telemedicine programs in Saudi Arabia and the UAE that funnel patient-generated data directly into ambulatory records. South America is growing 6.04% CAGR, with Brazil leading investments in cloud-native EHRs that integrate with public-health reporting portals. Infrastructure gaps remain a constraint throughout emerging markets. Still, multi-tenant public-cloud deployments and mobile-first front ends offer cost-effective workarounds, bolstering long-run prospects for the ambulatory EHR market.

- AdvancedMD

- Athenahealth

- Azalea Health Innovations, Inc.

- CompuGroup Medical SE & Co. KGaA

- CureMD.com, Inc.

- eClinicalWorks

- Epic Systems

- EverHealth Solutions Inc.

- Greenway Health

- Infor-Med, Inc. (Praxis EMR)

- Kareo

- Medhost

- Medical Information Technology

- Modernizing Medicine, Inc. (ModMed)

- NextGen Healthcare

- Oracle

- PointClickCare Technologies Inc.

- Practice Fusion, Inc.

- TruBridge, Inc.

- Veradigm Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Government incentives & compliance mandates

- 4.2.2 Accelerated shift to cloud-hosted EHRs

- 4.2.3 Value-based-care push for interoperable data

- 4.2.4 Specialty-specific AI modules boosting upgrades

- 4.2.5 Integration of telehealth workflows into EHR platforms

- 4.2.6 Reimbursement for remote monitoring & outpatient data capture

- 4.3 Market Restraints

- 4.3.1 Cyber-security & privacy breach concerns

- 4.3.2 Uneven infrastructure in emerging economies

- 4.3.3 Complex multi-jurisdiction regulatory compliance

- 4.3.4 Rising pay-per-use API costs for third-party integrations

- 4.4 Technological Outlook

- 4.5 Porter's Five Forces Analysis

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Bargaining Power of Suppliers

- 4.5.4 Threat of Substitutes

- 4.5.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value)

- 5.1 By Application

- 5.1.1 Practice Management

- 5.1.2 Patient Management

- 5.1.3 E-Prescribing

- 5.1.4 Referral Management

- 5.1.5 Population Health Management

- 5.1.6 Others

- 5.2 By Delivery Mode

- 5.2.1 Cloud-based Solutions

- 5.2.2 On-premise Solutions

- 5.2.3 Hybrid Solutions

- 5.3 By Practice Size

- 5.3.1 Large Practices

- 5.3.2 Medium-sized Practices

- 5.3.3 Small Practices

- 5.4 By End-User

- 5.4.1 Hospital-owned Ambulatory Centers

- 5.4.2 Independent Ambulatory Centers

- 5.4.3 Health-system Affiliated Physician Groups

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 India

- 5.5.3.3 Japan

- 5.5.3.4 Australia

- 5.5.3.5 South Korea

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 Middle East and Africa

- 5.5.4.1 GCC

- 5.5.4.2 South Africa

- 5.5.4.3 Rest of Middle East and Africa

- 5.5.5 South America

- 5.5.5.1 Brazil

- 5.5.5.2 Argentina

- 5.5.5.3 Rest of South America

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Competitive Benchmarking

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.4.1 AdvancedMD, Inc.

- 6.4.2 athenahealth Inc.

- 6.4.3 Azalea Health Innovations, Inc.

- 6.4.4 CompuGroup Medical SE & Co. KGaA

- 6.4.5 CureMD.com, Inc.

- 6.4.6 eClinicalWorks, LLC

- 6.4.7 Epic Systems Corporation

- 6.4.8 EverHealth Solutions Inc.

- 6.4.9 Greenway Health LLC

- 6.4.10 Infor-Med, Inc. (Praxis EMR)

- 6.4.11 Kareo, Inc.

- 6.4.12 MEDHOST, Inc.

- 6.4.13 Medical Information Technology, Inc. (Meditech)

- 6.4.14 Modernizing Medicine, Inc. (ModMed)

- 6.4.15 NextGen Healthcare, Inc.

- 6.4.16 Oracle Corporation

- 6.4.17 PointClickCare Technologies Inc.

- 6.4.18 Practice Fusion, Inc.

- 6.4.19 TruBridge, Inc.

- 6.4.20 Veradigm Inc.

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment