|

시장보고서

상품코드

1850235

의료기기 커넥티비티 시장 : 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Medical Device Connectivity - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

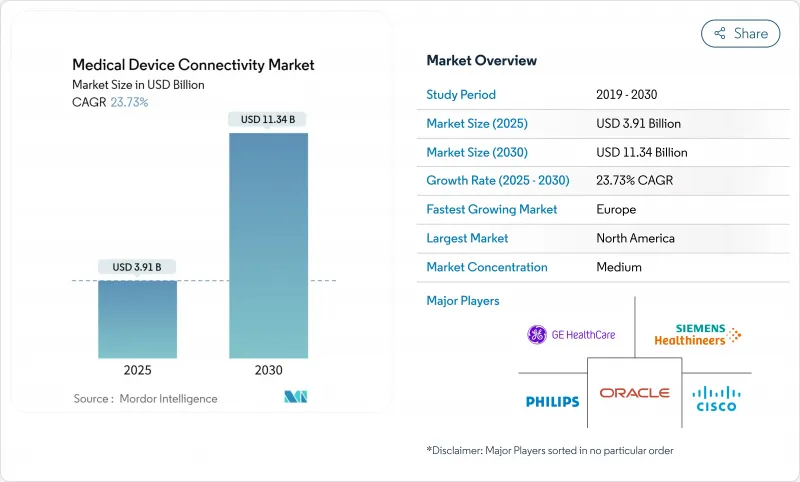

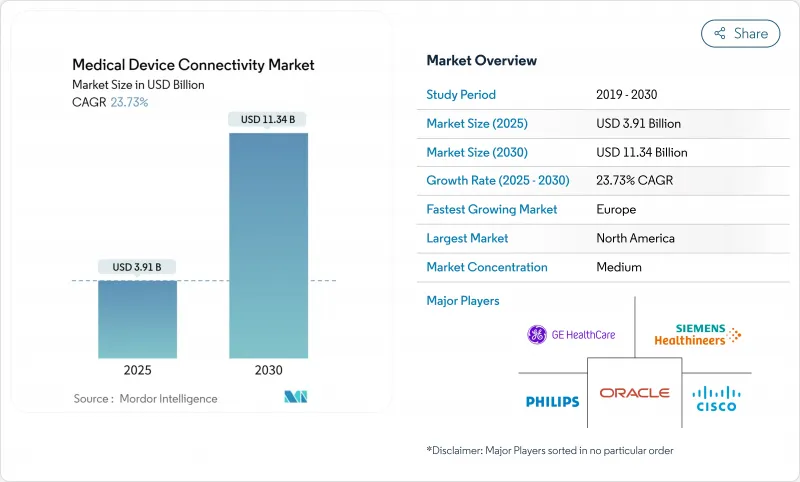

세계의 의료기기 커넥티비티 시장 규모는 2025년 39억 1,000만 달러로 추정되고, 2030년에는 113억 4,000만 달러에 이를 것으로 예측되며, CAGR 23.73%로 성장할 전망입니다.

헬스케어의 급속한 디지털화, 임상의의 작업 부하 증가, 가치 기반 진료 보상으로의 전환으로 장비와 시스템의 원활한 데이터 교환에 대한 수요가 증가하고 있습니다. 의료 제공업체는 자체 프로토콜을 개방형 표준으로 대체하여 정보 차단으로 인한 페널티를 완화하고 문서화에 소요되는 시간을 단축하려고 합니다. 전문의 부족의 심각화에 의해 Tele-ICU 프로그램이 확대되는 한편, 급성기, 외래, 재택의 각 세팅에 걸치는 지속적인 모니터링이 재입원을 줄여, 케어 제휴를 향상시키고 있습니다. 규제 당국이 사이버 보안 모니터링을 강화하고 6G 연구가 중요한 관리 애플리케이션을 위한 초고신뢰성, 저지연 무선 링크를 약속하면서 보안 연결 아키텍처에 대한 투자가 가속화되고 있습니다.

세계의 의료기기 커넥티비티 시장 동향 및 인사이트

EMR 상호 운용성 의무화 및 디지털 건강 정책

21세기 치료법(21st Century Cures Act)이 의무화한 표준화 API는 자체 프로토콜에서 FHIR 기반 교환으로의 전환을 강요합니다. 컴플라이언스 프로그램을 완료한 의료 시스템은 문서화 시간을 13% 단축하고, 케어 연계를 개선하며, 접속 엔진의 폭넓은 배치를 촉진하고 있습니다. 계측기 제조업체는 현재 비용이 많이 드는 후행 사이클을 피하고 연결성 안전 대책을 점점 더 중시하는 FDA 인증 프로세스를 가속화하기 위해 신제품에 상호 운용성을 설계하고 있습니다.

실시간 데이터를 요구하는 성과 기반 상환

CMS의 대체 지불 모델은 수익을 임상 결과에 연결하는 것으로, 병원은 환자의 악화를 조기에 감지하는 지속적인 모니터링과 엣지 분석 기능을 갖춘 침대를 도입하도록 촉구합니다. 커넥티드 RPM 플랫폼을 사용하는 의료 시스템에서는 심부전 재입원이 24% 감소한 것으로 보고되어 재정과 질의 인센티브가 일치하고 있습니다. 이 비즈니스 사례는 집중 치료실, 뇌졸중 병동, 종양 주입 센터에서 가장 효과적입니다.

데이터 표준이 없는 이종 레거시 기기군

병원은 주입 펌프, 인공 호흡기 및 모니터를 8년 이상의 수명 주기로 운영하는 경우가 많으며, 대부분은 패치가 가능한 운영 체제가 없습니다. 인터페이스 엔진은 공급업체별 프로토콜을 번역해야 하며 프로젝트 일정을 늘리고 지속적인 유지보수를 요청합니다. 절연 네트워크는 취약한 엔드포인트를 보호하지만 배선이 중복되므로 확장 프로젝트에 비용과 복잡성이 추가됩니다.

부문 분석

커넥티비티 솔루션은 2024년 매출의 63.67%를 차지하였고, 이종 장비 데이터를 정규화하며 빠르게 진화하는 상호 운용성 규칙을 구현하기 위한 백본으로 확립되었습니다. 이러한 플랫폼은 HL7v2, FHIR 및 고유한 스트림을 임상 의사결정 지원 엔진에 제공하는 EHR 가능 페이로드로 변환합니다. Mirth Connect와 같은 공급업체 중립 게이트웨이는 오픈소스 유연성을 제공하며 엔터프라이즈 제품군은 디바이스 라이브러리, 알람 관리 및 분석 모듈을 통합하여 제공합니다. 의료 시스템은 중복 서버 클러스터를 도입하여 급성기 병동의 다운타임을 거의 0으로 유지합니다. 업데이트 사이클이 가속화됨에 따라 의료기기 커넥티비티 시장에서는 주입 펌프, 마취기 및 무선 원격 측정 팩을 위한 즉시 사용할 수 있는 어댑터를 제공하는 솔루션이 점점 더 선호되고 있습니다.

연결 서비스는 병원이 도입, 유지보수, 사이버 보안 패치를 외주함으로써 연간 26.12%의 성장이 예측됩니다. 관리 서비스 계약은 가동 시간을 보장하고 공급자를 인력 부족으로부터 보호하며 규정 준수 문서가 최신인지 확인합니다. 중소규모 시설에서는 자본 지출을 예측 가능한 운영 비용으로 변환하는 구독 모델이 선택되었습니다. 서비스 회사는 인터페이스 튜닝, 24시간 365일 모니터링, 멀티벤더 에스테이트에 걸친 변경 관리 거버넌스를 통합으로 제공합니다. 이 추세는 서비스 하위 부문을 보다 광범위한 시장 세분화에서 중요한 수익 증진 요인으로 자리매김합니다.

유선 링크는 2024년 매출의 57.92%를 차지했으며, 치명타 케어 및 수술실에서의 실드 이더넷 백본이 그 중심이 되고 있습니다. 실시간 파형 충실도와 알려진 지연 프로파일을 통해 고대역폭 생명 유지 장치에는 유선 네트워크가 필수적입니다. 수술실 재배선은 임상 처리량을 중단하고 엄격한 검증이 필요하기 때문에 교체 사이클이 느립니다. 그럼에도 병원이 코어 스위치를 파워 오버 이더넷 대응으로 업그레이드함으로써 콘센트의 증설 없이 장래의 기기 클래스가 가능하게 되어 의료기기 커넥티비티 시장에 있어서의 유선 인프라의 관련성이 높아집니다.

무선 기술은 5G 업그레이드와 밀리초 미만의 대기 시간을 약속하는 6G 조사를 통해 CAGR 25.86%의 상승을 예상합니다. 액세스 포인트 밀도는 텔레메트리 벨트, 웨어러블 ECG 패치, 자세 및 낙하 데이터를 전송하는 스마트 침대를 지원하기 위해 일반 병동에서 증가하고 있습니다. Wi-Fi 6E의 도입은 레거시 간섭이 없는 새로운 주파수 대역을 확보하고, 프라이빗 5G 슬라이스는 모바일 CT 스캐너와 신속한 응답 스커트에 확실한 서비스 품질을 제공합니다. 병원에서는 점적 펌프가 자동으로 SSID를 전환하기 때문에 병동 경계에서 수동으로 다시 연결할 필요가 없어 환자의 이동이 원활해졌다고 보고합니다. 이러한 혁신은 무선이 의료기기 커넥티비티 시장의 모빌리티 엔진임을 뒷받침합니다.

지역 분석

북미는 성숙한 EHR의 보급, 엄격한 상호운용성의 실시, 엣지 분석의 조기 도입으로 2024년 매출의 38.58%를 차지했습니다. 정보 차단에 대한 CMS의 처벌과 새로운 API 의무화로 인해 공급자는 침대 엣지 장비와 지불자 포털을 원활하게 연결하는 표준 기반 게이트웨이를 도입해야 합니다. 학술 의료 센터는 지속적인 모니터링과 예측 점수를 융합시킨 AI 확장 감시를 시험적으로 도입하여 높은 처리량 연결 허브 조달을 가속화합니다. 디지털 건강 신흥 기업에 대한 벤처 투자는 의료기기 커넥티비티 시장의 지역 발자국을 더욱 확대합니다.

아시아태평양은 2025-2030년 연간 26.73% 확대될 것으로 예측되며, 이는 세계에서 가장 빠릅니다. 중국은 프라이빗 5G, 로봇 공학, 클라우드 PACS 통합을 특징으로 하는 스마트 병원의 설계도를 확대하고, 인도는 생산 연동형 인센티브 제도에 의해 원래부터 오픈 스탠다드인터페이스를 통합한 국산 기기 제조업체를 육성하고 있습니다. 일본에서는 암호화된 VPN을 통한 현을 건너는 진찰에 환불을 실시하는 정부의 자극책을 활용해, 원격 뇌졸중 네트워크로 지방의 진료소를 업그레이드합니다. 한국과 호주는 데이터 중심의 헬스케어 파일럿을 장려하고 무선 원격 측정 및 AI 트리어지 알고리즘을 위한 비옥한 토양을 생산하고 있습니다. 이러한 역학에 의해 이 지역은 의료기기 커넥티비티 시장의 중요한 성장 엔진으로서 자리매김되고 있습니다.

유럽의 CAGR은 21.54%로 예측되어 상호 운용성과 사이버 보안을 강화하는 의료기기 규제와 일반 데이터 보호 규제에 지지되고 있습니다. 독일은 병원 미래법에 따라 병원의 디지털 성숙도 업그레이드를 지원하고 HL7-FHIR 게이트웨이 조달을 가속화하고 있습니다. 영국은 NHS 신탁에 디지털 성숙도 평가를 의무화하고 안전한 장치 온보딩을 위한 자금을 확보합니다. 북유럽 국가들은 임상 사용을 위한 6G 연구 테스트 베드를 개척하고, 범 EU 이니셔티브는 유럽 의료 데이터 공간을 통해 국경을 넘은 데이터 교환을 장려하고 있습니다. 프라이버시와 보안에 대한 강한 관심은 공급업체의 선택을 형성하고 병원은 제로 트러스트 설계 및 섬세한 동의 관리를 제공하는 플랫폼을 선호합니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 서포트

목차

제1장 서론

- 조사의 전제조건 및 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- EMR 상호 운용성의 의무 및 디지털 헬스 정책

- 실시간 데이터를 필요로 하는 성과에 기초한 상환

- 원격 및 가정에서의 만성 질환 모니터링 확대

- IoT 사이버 보안 프레임워크의 융합

- 멀티 파라미터 웨어러블 및 임플란트 디바이스의 보급

- 예측적인 임상 인사이트를 가능하게 하는 클라우드 네이티브 분석

- 시장 성장 억제요인

- 데이터 표준이 없는 이기종 혼재의 레거시 디바이스군

- 초기 통합 및 인터페이스 엔진의 높은 비용

- 사이버 보안 및 환자의 프라이버시에 관한 취약성이 여전히 존재

- 워크플로의 조정이 한정적이기 때문에 의사의 저항 초래

- 기술의 전망

- Porter's Five Forces 분석

- 신규 참가업체의 위협

- 구매자의 협상력

- 공급기업의 협상력

- 대체품의 위협

- 경쟁 기업 간 경쟁 관계

제5장 시장 규모 및 성장 예측

- 컴포넌트별

- 연결 솔루션

- 인터페이스 엔진 및 통합 플랫폼

- 연결 허브 및 게이트웨이

- 디바이스 인터페이스 모듈

- 접속 서비스

- 구현 및 통합

- 지원 및 유지 보수

- 컨설팅 및 교육

- 연결 솔루션

- 기술별

- 유선

- 무선

- 하이브리드

- 용도별

- 지속적인 환자 모니터링

- 원격 ICU 및 원격 뇌졸중

- 이미지 및 PACS 연결

- 투약 관리 및 스마트 IV 펌프

- 마취 및 인공호흡기

- 기타 용도

- 최종 사용자별

- 병원 및 클리닉

- 외래 수술 및 전문센터

- 재택 헬스케어 환경

- 기타 최종 사용자

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 기타 유럽

- 아시아태평양

- 중국

- 인도

- 일본

- 호주

- 한국

- 기타 아시아태평양

- 중동 및 아프리카

- GCC

- 남아프리카

- 기타 중동 및 아프리카

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 북미

제6장 경쟁 구도

- 시장 집중도

- 경쟁 벤치마킹

- 시장 점유율 분석

- 기업 프로파일

- Ascom Holding AG

- Baxter International Inc

- Cisco Systems Inc.

- Digi International Inc.

- Dragerwerk AG & Co. KGaA

- GE HealthCare Technologies Inc.

- Honeywell International Inc.

- ICU Medical

- Koninklijke Philips NV

- Lantronix Inc.

- Masimo Corporation

- Medtronic plc

- Mindray Medical International Limited

- NantHealth, Inc.

- Nihon Kohden Corporation

- Oracle Corporation

- S3 Connected Health

- Siemens Healthineers AG

- Spectrum Medical Ltd

- Stryker Corporation

제7장 시장 기회 및 향후 전망

AJY 25.11.07The global medical device connectivity market size will reach USD 3.91 billion in 2025 and is forecast to reach USD 11.34 billion by 2030, registering a 23.73% CAGR.

Rapid digitization of healthcare, mounting clinician workload, and the move to value-based reimbursement are driving demand for seamless device-to-system data exchange. Healthcare providers are replacing proprietary protocols with open standards to ease information blocking penalties and reduce documentation time. Rising specialist shortages are expanding Tele-ICU programs, while continuous monitoring across acute, ambulatory, and home settings is lowering readmissions and improving care coordination. Investments in secure connectivity architectures are accelerating as regulators tighten cybersecurity oversight and 6G research promises ultra-reliable, low-latency wireless links for critical care applications.

Global Medical Device Connectivity Market Trends and Insights

EMR interoperability mandates and digital-health policies

Standardized APIs mandated by the 21st Century Cures Act are forcing a shift from proprietary protocols to FHIR-based exchanges. Health systems completing compliance programs have cut documentation time by 13% and improved care coordination, encouraging broader deployment of connectivity engines. Device makers now design interoperability into new products to avoid costly retrofit cycles and to accelerate FDA clearance processes that increasingly weigh connectivity safeguards.

Outcome-based reimbursement demanding real-time data

CMS alternative payment models link revenue to clinical outcomes, pushing hospitals to instrument beds with continuous monitoring and edge analytics that flag patient deterioration early. Health systems using connected RPM platforms have reported 24% lower readmissions for heart failure, aligning financial and quality incentives. This business case is strongest in intensive care units, stroke wards, and oncology infusion centers, where preventable adverse events carry steep penalties.

Heterogeneous legacy device fleets without data standards

Hospitals often operate infusion pumps, ventilators, and monitors with life cycles exceeding eight years, many of which lack patchable operating systems. Interface engines must translate vendor-specific protocols, increasing project timelines and demanding continuous maintenance. Isolation networks protect vulnerable endpoints, yet duplicative wiring adds cost and complexity to expansion projects.

Other drivers and restraints analyzed in the detailed report include:

- Convergence of IoT cybersecurity frameworks

- Cloud-native analytics enabling predictive clinical insights

- High upfront integration and interface-engine costs

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Connectivity solutions held 63.67% of 2024 revenue, establishing them as the backbone for normalizing heterogeneous device data and enforcing rapidly evolving interoperability rules. These platforms translate HL7v2, FHIR, and proprietary streams into EHR-ready payloads that feed clinical decision support engines. Vendor neutral gateways such as Mirth Connect provide open-source flexibility, while enterprise suites bundle device libraries, alarm management, and analytics modules. Health systems deploy redundant server clusters to maintain near-zero downtime for high-acuity wards. As refresh cycles accelerate, the medical device connectivity market increasingly favors solutions offering out-of-the-box adapters for infusion pumps, anesthesia machines, and wireless telemetry packs.

Connectivity services are forecast to grow 26.12% annually as hospitals outsource implementation, maintenance, and cybersecurity patching. Managed-service contracts guarantee uptime, shield providers from staffing shortages, and ensure compliance documentation stays current. Small and mid-size facilities choose subscription models that convert capital expenditure into predictable operating costs. Service firms bundle interface tuning, 24 X 7 monitoring, and change-control governance across multi-vendor estates. This trend positions the services sub-segment as a key revenue accelerator within the broader medical device connectivity market.

Wired links represented 57.92% of 2024 sales, anchored by shielded Ethernet backbones in critical care and surgical suites. Real-time waveform fidelity and known latency profiles keep hard-wired networks indispensable for high-bandwidth, life-support devices. Replacement cycles are slow because rewiring operating theatres disrupts clinical throughput and requires rigorous validation. Even so, hospitals upgrading core switches to support power-over-Ethernet enable future device classes without additional outlets, extending the relevance of wired infrastructure within the medical device connectivity market.

Wireless technologies are expected to rise 25.86% CAGR on the back of 5G upgrades and forthcoming 6G research that promises sub-millisecond latency. Access point density is increasing in general wards to support telemetry belts, wearable ECG patches, and smart beds transmitting posture and falls data. Wi-Fi 6E deployments carve new spectrum free of legacy interference, while private 5G slices offer deterministic quality of service for mobile CT scanners and rapid response carts. Hospitals report smoother patient transfers when IV pumps automatically switch SSIDs, eliminating manual reconnection at ward boundaries. These innovations confirm wireless as the mobility engine of the medical device connectivity market.

The Medical Device Connectivity Market Report is Segmented by Component (Connectivity Solutions [Device Interface Modules and More] and Connectivity Services [Implementation & Integration and More]), Technology (Wired and More), Application (Continuous Patient Monitoring and More), End-User (Hospitals & Clinics and More) and Geography (North America, Europe, and More). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America held 38.58% of 2024 revenue due to mature EHR penetration, strict interoperability enforcement, and early adoption of edge analytics. CMS penalties for information blocking and new API mandates compel providers to deploy standards-based gateways that seamlessly connect bedside devices with payer portals. Academic medical centers pilot AI-augmented surveillance that merges continuous monitoring with predictive scoring, accelerating procurement of high-throughput connectivity hubs. Venture investment in digital health startups further expands the regional footprint of the medical device connectivity market.

Asia Pacific is forecast to expand 26.73% annually between 2025-2030, the fastest worldwide. China scales smart hospital blueprints featuring private 5G, robotics, and cloud PACS integration, while India's production-linked incentive schemes nurture indigenous device manufacturers embedding open-standard interfaces from inception. Japan upgrades rural clinics with tele-stroke networks, leveraging government stimulus that reimburses cross-prefecture consults over encrypted VPNs. South Korea and Australia incentivize data-centric healthcare pilots, creating fertile ground for wireless telemetry and AI triage algorithms. These dynamics are positioning the region as a critical growth engine of the medical device connectivity market.

Europe grows at a projected 21.54% CAGR, supported by the Medical Device Regulation and General Data Protection Regulation, which jointly elevate interoperability and cybersecurity bars. Germany subsidizes hospital digital maturity upgrades under its Hospital Futures Act, accelerating HL7-FHIR gateway procurements. The United Kingdom mandates digital maturity assessments for NHS trusts, unlocking funding for secure device onboarding. Nordic countries pioneer 6G research testbeds for clinical use, and pan-EU initiatives encourage cross-border data exchange via the European Health Data Space. Strong attention to privacy and security shapes vendor selection, with hospitals favoring platforms offering zero-trust designs and granular consent management, reinforcing Europe's stature within the medical device connectivity market.

- Ascom

- Baxter

- Cisco Systems

- Digi International Inc.

- Dragerwerk

- GE HealthCare Technologies Inc.

- Honeywell International

- ICU Medical

- Koninklijke Philips

- Lantronix Inc.

- Masimo

- Medtronic

- Mindray

- NantHealth

- Nihon Kohden

- Oracle

- S3 Connected Health

- Siemens Healthineers

- Spectrum Medical Ltd

- Stryker

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 EMR interoperability mandates and digital-health policies

- 4.2.2 Outcome-based reimbursement demanding real-time data

- 4.2.3 Expansion of remote and home-based chronic-care monitoring

- 4.2.4 Convergence of IoT cybersecurity frameworks

- 4.2.5 Proliferation of multi-parameter wearable & implantable devices

- 4.2.6 Cloud-native analytics enabling predictive clinical insights

- 4.3 Market Restraints

- 4.3.1 Heterogeneous legacy device fleets without data standards

- 4.3.2 High upfront integration and interface-engine costs

- 4.3.3 Persistent cybersecurity and patient-privacy vulnerabilities

- 4.3.4 Limited workflow alignment causing clinician resistance

- 4.4 Technological Outlook

- 4.5 Porter's Five Forces Analysis

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Bargaining Power of Suppliers

- 4.5.4 Threat of Substitutes

- 4.5.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value)

- 5.1 By Component

- 5.1.1 Connectivity Solutions

- 5.1.1.1 Interface Engines & Integration Platforms

- 5.1.1.2 Connectivity Hubs & Gateways

- 5.1.1.3 Device Interface Modules

- 5.1.2 Connectivity Services

- 5.1.2.1 Implementation & Integration

- 5.1.2.2 Support & Maintenance

- 5.1.2.3 Consulting & Training

- 5.1.1 Connectivity Solutions

- 5.2 By Technology

- 5.2.1 Wired

- 5.2.2 Wireless

- 5.2.3 Hybrid

- 5.3 By Application

- 5.3.1 Continuous Patient Monitoring

- 5.3.2 Tele-ICU & Tele-Stroke

- 5.3.3 Imaging & PACS Connectivity

- 5.3.4 Medication Administration & Smart IV Pumps

- 5.3.5 Anesthesia & Ventilator

- 5.3.6 Other Applications

- 5.4 By End-User

- 5.4.1 Hospitals & Clinics

- 5.4.2 Ambulatory Surgery & Specialty Centers

- 5.4.3 Home Healthcare Settings

- 5.4.4 Other End-Users

- 5.5 By Geography (Value)

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 India

- 5.5.3.3 Japan

- 5.5.3.4 Australia

- 5.5.3.5 South Korea

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 Middle East & Africa

- 5.5.4.1 GCC

- 5.5.4.2 South Africa

- 5.5.4.3 Rest of Middle East & Africa

- 5.5.5 South America

- 5.5.5.1 Brazil

- 5.5.5.2 Argentina

- 5.5.5.3 Rest of South America

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Competitive Benchmarking

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.4.1 Ascom Holding AG

- 6.4.2 Baxter International Inc

- 6.4.3 Cisco Systems Inc.

- 6.4.4 Digi International Inc.

- 6.4.5 Dragerwerk AG & Co. KGaA

- 6.4.6 GE HealthCare Technologies Inc.

- 6.4.7 Honeywell International Inc.

- 6.4.8 ICU Medical

- 6.4.9 Koninklijke Philips N.V.

- 6.4.10 Lantronix Inc.

- 6.4.11 Masimo Corporation

- 6.4.12 Medtronic plc

- 6.4.13 Mindray Medical International Limited

- 6.4.14 NantHealth, Inc.

- 6.4.15 Nihon Kohden Corporation

- 6.4.16 Oracle Corporation

- 6.4.17 S3 Connected Health

- 6.4.18 Siemens Healthineers AG

- 6.4.19 Spectrum Medical Ltd

- 6.4.20 Stryker Corporation

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment