|

시장보고서

상품코드

1850238

소프트웨어 정의 보안 시장 : 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Software Defined Security - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

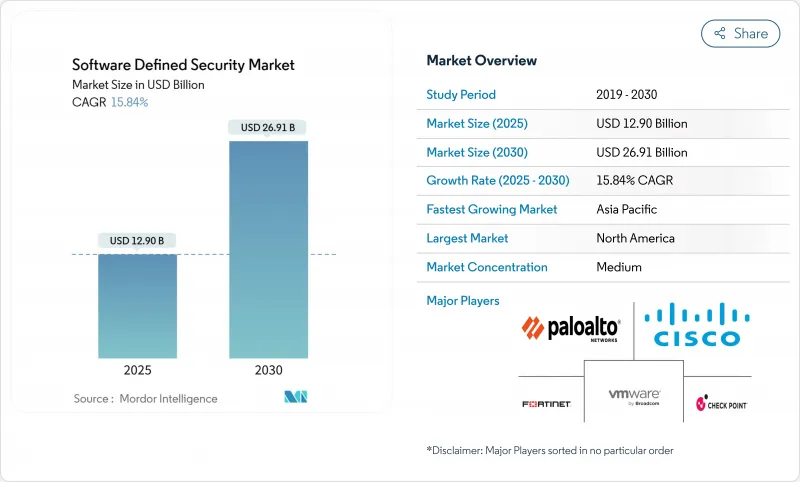

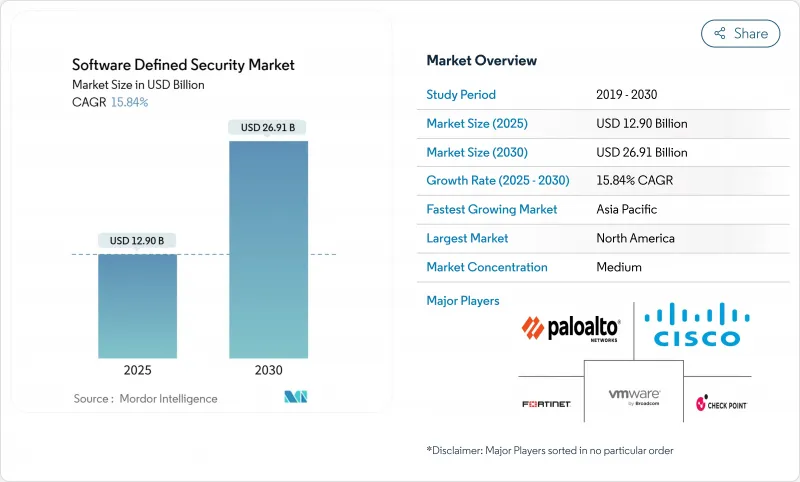

소프트웨어 정의 보안 시장 규모는 2025년에 129억 달러로 추정되고, 2030년에는 2배 이상인 269억 1,000만 달러로 확대될 전망이며, CAGR 15.84%로 성장할 것으로 예측됩니다.

대부분의 기업은 경계 중심의 제어에서 데이터센터, 여러 퍼블릭 클라우드, 엣지 위치를 이동하는 워크로드를 따르는 프로그래머블 아키텍처로 이동하고 있습니다. 자동화된 정책 구현은 사고 대응 사이클을 줄이는 반면, 제로 트러스트 원칙은 지속적인 검증을 일상적인 네트워크 운영에 통합합니다. EU 사이버 탄력성 법과 NIS2 지침과 같은 규제 기한은 재량 지출을 의무적인 투자로 바꾸고 있습니다. 동시에, 컨테이너화된 애플리케이션의 급격한 증가로 인해 보안 팀은 소프트웨어 정의 접근 방식만 제공할 수 있는 미세한 세분화 및 런타임 보호를 채택해야 합니다. 이러한 힘이 결합되어 소프트웨어 정의 보안 시장은 10년 말까지 두 자릿수의 기세를 유지할 수 있습니다.

세계의 소프트웨어 정의 보안 시장 동향 및 인사이트

신속한 인시던트 응답 및 정책 자동화 요구

감지까지의 평균 시간은 일 단위가 아닌 분 단위로 측정해야 합니다. Coalition의 2025 Cyber Threat Index에 따르면, ransomware 침입의 58%는 침해된 VPN 장치에서 시작되었으며 수작업에 의한 대응의 한계를 나타냅니다. 따라서 기업은 위협 인텔리전스가 정의된 위험 임계값을 초과하면 엔드포인트를 자동으로 격리하는 프로그래머블 보안 제어를 채택합니다. 캐나다의 평균 침해 비용은 466만 달러에 달했으며 2025년에는 영향을 받은 고객의 해지율이 38%로 상승했습니다. 자동화된 소프트웨어 정의 플레이북을 통해 보안 팀은 인력을 늘리지 않고 규모를 확장하고 방어 속도를 적의 템포에 맞출 수 있습니다.

멀티클라우드 및 하이브리드 클라우드 아키텍처 채택 증가

Nutanix의 보고에 따르면 현재 세계 기업의 90%가 프라이빗 클라우드와 여러 퍼블릭 클라우드를 '클라우드 스마트'로 결합하여 운영하고 있습니다(nutanix.com). 이러한 다양성은 가시성을 단편화하고 71%의 팀이 최소한 하나의 환경에서 정책 맹점을 인정합니다. 소프트웨어 정의 보안 플랫폼은 기본 인프라에서 정책을 추상화하여 이 단편화를 해결합니다. 통합된 대시보드는 워크로드가 온프레미스, AWS, Azure 또는 OCI에서 실행되는지 여부에 관계없이 동일한 컨트롤을 적용하고 지속적인 컴플라이언스를 보장하는 동시에 개발자에게 애플리케이션을 최적의 위치에 배치할 수 있는 자유를 제공합니다.

DevSecOps 인력 부족

오라일리의 2024년 조사에서는 38.9%의 조직이 클라우드 보안 기술을 최대의 갭으로 꼽았습니다. 미국 DevSecOps 엔지니어의 급여는 이미 평균 140,000달러이며 예산과 프로젝트 타임라인을 압박하고 있습니다. 많은 기업들이 이 격차를 관리형 서비스 제공업체로 채우고 있으며 서비스 부문은 확장되고 있지만 고급 기능의 내부 도입은 지연되고 있습니다.

부문 분석

퍼블릭 클라우드는 계속해서 전체의 보급을 이끌어 2024년 매출의 39%를 차지했습니다. 그 중 SaaS 전용 분야는 CAGR 18.20%로 가장 빠르게 성장하고 있습니다. 특히 중소기업 IT 팀은 온프레미스 어플라이언스에 패치를 적용할 필요가 없기 때문에 클라우드 네이티브 공급업체에서 제공하는 즉각적인 스케일링 및 롤링 업데이트를 높이 평가합니다. 또한 대기업은 제로 트러스트 프레임 워크가 성숙함에 따라 자본 투자를 줄이고 기능 채택을 가속화하기 위해 워크로드를 SaaS 노드로 이동합니다.

온프레미스 전개는 소블린 및 대기 시간이 요구되는 경우에는 여전히 필수적이지만, 하이브리드 설계에서는 SaaS의 보안 웹 게이트웨이를 통해 아웃바운드 트래픽을 라우팅하는 경우가 늘고 있습니다. 이러한 트렌드를 결합하면 정책 제어가 네트워크 에지로 이동하여 멀티 테넌트 및 탄력적인 백플레인을 구축하는 공급업체가 유리합니다. 이 마이그레이션은 소프트웨어 정의 보안 시장이 어플라이언스 판매에서 구독 수익으로 보다 광범위하게 재배치됨을 확인합니다.

네트워크 보안은 레거시 방화벽 새로 고침주기와 소프트웨어 정의 Wide-area Network 전개를 반영하여 2024년 매출의 40%를 차지했습니다. 성장률이 높은 것은 클라우드 및 컨테이너 보안으로 2030년까지 연평균 복합 성장률(CAGR) 24%로 확대됩니다. 개발 팀은 모놀리스를 수백 개의 마이크로서비스로 컨테이너화하기 때문에 포드의 리스폰에 맞추어 런타임 제어를 즉시 적응시켜야 합니다. 따라서 지속적인 이미지 스캔, 승인 제어 후크 및 서비스 메시 암호화가 조달 목록의 상위를 차지합니다.

조기 도입 기업에서는 AWS, Azure 및 Google Cloud 전반의 구성 실수를 인벤토리화하는 자세 관리 모듈과 컨테이너 보안을 번들하는 경우가 늘고 있습니다. 이러한 수렴은 워크로드와 구성의 보안 경계를 더욱 모호하게 만들고 공급업체는 클라우드 네이티브 애플리케이션 보호 플랫폼을 보다 광범위한 소프트웨어 정의 보안 마켓 스위트에 직접 통합합니다.

지역 분석

북미는 2024년 매출의 38%를 차지했으며 연방 정부의 적극적인 노력에 힘입었습니다. 미국 국방부는 2025 회계연도의 DISA 사이버 오퍼레이션에 5억 490만 달러를 할당해 계약자 생태계에 파급하는 제로 트러스트 참조 아키텍처 구축을 명했습니다. 이 지역의 사이버 보안 지출은 전반적으로 전년 대비 15% 증가했으며, 이는 연방 정부공급망 전반에 걸쳐 소프트웨어 부품표와 지속적인 모니터링을 의무화하는 백악관의 대통령령을 뒷받침한 것입니다.

유럽은 2위이지만 소프트웨어 정의 보안 시장이 발본적인 법규제와 발길을 맞춘 것으로 건전한 가속을 보였습니다. 2027년 12월에 시행되는 '사이버 레지리언스법'은 첫날부터 보안을 짜넣은 제품을 설계할 것을 제조업체에 의무화하는 것입니다. 디지털 운영 탄력성 법(금융) 및 NIS2(중요 서비스)와 같은 보완적인 조치는 유사한 의무를 경제 전체로 확대하는 것입니다. 따라서 기업은 여러 감독 기관에 실시간으로 컴플라이언스를 증명할 수 있는 프로그래머블 정책 엔진에 집중하고 있습니다.

아시아태평양은 성장의 프론트 러너이며 2030년까지 연평균 복합 성장률(CAGR) 14.90%로 성장할 것으로 예측됩니다. 중국, 일본, 한국의 제조업체는 운영 기술 네트워크를 인터넷 위협에 노출시키는 인더스트리 4.0 프로그램을 추진하고 있습니다. 각국 정부는 마이크로 세분화이나 제로 트러스트를 추천하는 분야별 프레임워크로 대응하여 새로운 프로젝트를 추진하고 있습니다. 인도의 디지털 개인 데이터 보호법도 마찬가지로 의료 및 전자상거래 사업자에 대한 규제를 강화하고 있습니다. 이러한 움직임을 종합하면 세계 소프트웨어 정의 보안 시장의 지역별 점유율이 확대됩니다.

중동 및 아프리카, 남미가 새로운 채용국이 되고 있습니다. 에너지 수출 기업은 보안 바이 디자인의 정유소 제어 시스템을 위탁하고, 브라질의 금융 규제 당국은 엄격한 오픈 뱅킹 보안 가이드 라인을 공표하고 있습니다. 절대적인 수익 기회는 아직 적고 높은 성장률을 자랑하는 이 지역은 그린필드의 기회를 요구하는 클라우드 네이티브 벤더에게 매력적입니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 서포트

목차

제1장 서론

- 조사의 전제조건 및 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 보다 신속한 사고 대응 및 정책 자동화의 요건

- 멀티클라우드 및 하이브리드 클라우드 아키텍처 채택 증가

- 컨테이너 및 Kubernetes 보안 지출 급증

- 제로 트러스트 및 SASE의 통합으로의 이행(보고 부족)

- AI에 의한 위협 헌팅으로 체류 시간 단축(보고 부족)

- 중요 인프라 공격 후 국가 사이버 탄력 의무(보고 부족)

- 시장 성장 억제요인

- DevSecOps 인력 부족

- 레거시 시스템의 상호 운용성 문제

- 동서 마이크로 세분화에서 숨은 퍼포먼스 오버헤드(보고 부족)

- 단일 벤더의 정책 컨트롤러에 의한 집중 위험(보고 부족)

- 밸류체인 및 공급망 분석

- 규제 상황

- 기술의 전망

- Porter's Five Forces 분석

- 신규 참가업체의 위협

- 구매자의 협상력

- 공급기업의 협상력

- 대체품의 위협

- 경쟁 기업 간 경쟁 관계

제5장 시장 규모 및 성장 예측

- 컴포넌트별

- 소프트웨어

- 서비스

- 전개 모델별

- 온프레미스

- 퍼블릭 클라우드

- 프라이빗 클라우드

- 하이브리드 클라우드

- 보안 유형별

- 네트워크 보안

- 엔드포인트 보안

- 애플리케이션 보안

- 클라우드 및 컨테이너 보안

- 기타

- 조직 규모별

- 중소기업

- 대기업

- 최종 사용자별

- BFSI

- 통신 및 IT

- 헬스케어

- 정부 및 방위

- 소매업 및 전자상거래

- 에너지 및 유틸리티

- 기타

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 영국

- 독일

- 프랑스

- 이탈리아

- 기타 유럽

- 아시아태평양

- 중국

- 일본

- 인도

- 한국

- 기타 아시아태평양

- 중동

- 이스라엘

- 사우디아라비아

- 아랍에미리트(UAE)

- 튀르키예

- 기타 중동

- 아프리카

- 남아프리카

- 이집트

- 기타 아프리카

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 북미

제6장 경쟁 구도

- 시장 집중도

- 전략적 동향

- 시장 점유율 분석

- 기업 프로파일

- Palo Alto Networks

- Cisco Systems

- Fortinet

- Juniper Networks

- VMware(Broadcom)

- Check Point Software

- IBM

- Oracle

- Microsoft

- Trend Micro

- Huawei

- Sophos

- McAfee

- Splunk

- Illumio

- Akamai Technologies

- Netskope

- Zscaler

- Forcepoint

- Darktrace

- Proofpoint

제7장 시장 기회 및 향후 전망

AJY 25.11.07The software-defined security market size is estimated at USD 12.9 billion in 2025 and is forecast to more than double to USD 26.91 billion by 2030, advancing at a 15.84% CAGR.

Most enterprises are moving away from perimeter-centric controls toward programmable architectures that follow workloads as they shift across data centers, multiple public clouds, and edge locations. Automated policy enforcement shortens incident-response cycles, while zero-trust principles embed continuous verification into everyday network operations. Regulatory deadlines such as the EU Cyber Resilience Act and the NIS2 Directive are converting discretionary spending into mandatory investments. At the same time, the rapid growth of containerized applications forces security teams to embrace granular micro-segmentation and runtime protection that only software-defined approaches can deliver. Together, these forces give the software-defined security market durable, double-digit momentum through the end of the decade.

Global Software Defined Security Market Trends and Insights

Requirement for quicker incident response and policy automation

Mean time to detection must now be measured in minutes, not days. Coalition's 2025 Cyber Threat Index found that 58% of ransomware intrusions began with compromised VPN devices, exposing the limits of manual responses. Enterprises therefore employ programmable security controls that auto-isolate endpoints once threat intelligence crosses defined risk thresholds. The financial stakes remain high: average breach costs in Canada reached USD 4.66 million and churn rates climbed to 38% among affected customers in 2025. Automated, software-defined playbooks let security teams scale without proportional head-count increases, aligning protection speed with adversary tempo.

Rising adoption of multi-cloud and hybrid cloud architectures

Nutanix reports that 90% of global organizations now run a "cloud-smart" mix of private and multiple public clouds [nutanix.com]. Such diversity fragments visibility; 71% of teams acknowledge policy blind spots in at least one environment. Software-defined security platforms resolve that fragmentation by abstracting policy from the underlying infrastructure. Unified dashboards apply identical controls regardless of whether workloads run on-premises, AWS, Azure, or OCI, ensuring continuous compliance while giving developers freedom to place applications where they perform best.

Shortage of DevSecOps talent

O'Reilly's 2024 survey shows 38.9% of organizations citing cloud security skills as their biggest gap. DevSecOps engineer salaries in the United States already average USD 140,000, pressuring budgets and project timelines. Many firms backfill the gap with managed service providers, which boosts the services segment but slows in-house adoption of advanced features.

Other drivers and restraints analyzed in the detailed report include:

- Surge in container/Kubernetes security spend

- National cyber-resilience mandates after critical-infrastructure attacks

- Legacy-system interoperability issues

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Public cloud continues to lead overall penetration, delivering 39% of 2024 revenue. Within that category, the SaaS-only slice is climbing fastest at an 18.20% CAGR. Smaller IT teams in particular prize the instant scaling and rolling updates that cloud-native vendors provide, since no on-premises appliances require patching. Larger enterprises also shift workloads into SaaS nodes to reduce capex and accelerate feature adoption as zero-trust frameworks mature.

On-premises deployments remain indispensable where sovereignty or latency mandates apply; however, hybrid designs increasingly route outbound traffic through SaaS secure web gateways. Combined, these trends move policy control toward the network edge and favour vendors that architect multi-tenant, elastic backplanes. The transition underscores the broader repositioning of the software defined security market from appliance sales to subscription revenue.

Network security still represents 40% of 2024 revenue, reflecting legacy firewall refresh cycles and software-defined wide-area network rollouts. The higher-growth story lies in cloud/container security, which will expand at a 24% CAGR through 2030. Development teams containerize monoliths into hundreds of microservices, so runtime controls must adapt in seconds as pods respawn. Continuous image scanning, admission-control hooks, and service-mesh encryption therefore top procurement lists.

Early adopters increasingly bundle container security with posture-management modules that inventory misconfigurations across AWS, Azure, and Google Cloud. This convergence further blurs lines between workload and configuration security, pushing vendors to integrate cloud-native application protection platforms directly into their broader software defined security market suites.

Software Defined Security Market Report is Segmented by Component (Software, Services), Deployment Model (On-Premises, Public Cloud and More), Security Type (Network Security, Endpoint Security and More), Organization Size (Small & Medium Enterprises and Large Enterprises), End User (BFSI, Telecommunications & IT and More) and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America captured 38% of 2024 revenue, underpinned by decisive federal action. The U.S. Department of Defense allocated USD 504.9 million to DISA cyber operations for fiscal 2025, with a mandate to build zero-trust reference architectures that ripple into contractor ecosystems. Corporate boards mirror that urgency: overall cybersecurity spending in the region grew 15% year over year, buoyed by the White House's executive orders that require software bills of materials and continuous monitoring across the federal supply chain.

Europe sits in second place but posts healthy acceleration as the software defined security market aligns with sweeping legislation. The Cyber Resilience Act coming into force in December 2027 obliges manufacturers to design products with security baked in from day one. Complementary measures such as the Digital Operational Resilience Act (for finance) and NIS2 (for essential services) extend similar obligations across the economy. Enterprises are therefore converging on programmable policy engines capable of proving compliance in real time to multiple supervisory bodies.

Asia-Pacific is the growth frontrunner, set to log a 14.90% CAGR through 2030. Manufacturing heavyweights in China, Japan, and South Korea pursue Industry 4.0 programs that expose operational-technology networks to internet threats. Governments respond with sector-specific frameworks that recommend micro-segmentation and zero-trust, propelling new projects. India's Digital Personal Data Protection Act similarly raises bars for healthcare and e-commerce operators. Collectively, these moves expand the regional share of the global software defined security market.

The Middle East, Africa, and South America are emerging adopters. Energy exporters commission secure-by-design refinery control systems, while Brazilian financial regulators publish stringent open-banking security guidelines. Although absolute spend remains lower, high growth rates make these geographies attractive for cloud-native vendors seeking greenfield opportunities.

- Palo Alto Networks

- Cisco Systems

- Fortinet

- Juniper Networks

- VMware (Broadcom)

- Check Point Software

- IBM

- Oracle

- Microsoft

- Trend Micro

- Huawei

- Sophos

- McAfee

- Splunk

- Illumio

- Akamai Technologies

- Netskope

- Zscaler

- Forcepoint

- Darktrace

- Proofpoint

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Requirement for quicker incident response and policy automation

- 4.2.2 Rising adoption of multi-cloud and hybrid cloud architectures

- 4.2.3 Surge in container/Kubernetes security spend

- 4.2.4 Shift toward zero-trust and SASE convergence (under-reported)

- 4.2.5 AI-driven threat-hunting reducing dwell time (under-reported)

- 4.2.6 National cyber-resilience mandates after critical-infrastructure attacks (under-reported)

- 4.3 Market Restraints

- 4.3.1 Shortage of DevSecOps talent

- 4.3.2 Legacy-system interoperability issues

- 4.3.3 Hidden performance overhead in east-west micro-segmentation (under-reported)

- 4.3.4 Concentration risk from single-vendor policy controllers (under-reported)

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porters Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitute Products

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SIZE & GROWTH FORECASTS (VALUE)

- 5.1 By Component

- 5.1.1 Software

- 5.1.2 Services

- 5.2 By Deployment Model

- 5.2.1 On-premises

- 5.2.2 Public Cloud

- 5.2.3 Private Cloud

- 5.2.4 Hybrid Cloud

- 5.3 By Security Type

- 5.3.1 Network Security

- 5.3.2 Endpoint Security

- 5.3.3 Application Security

- 5.3.4 Cloud / Container Security

- 5.3.5 Others

- 5.4 By Organization Size

- 5.4.1 Small and Medium Enterprises

- 5.4.2 Large Enterprises

- 5.5 By End User

- 5.5.1 BFSI

- 5.5.2 Telecommunications and IT

- 5.5.3 Healthcare

- 5.5.4 Government and Defense

- 5.5.5 Retail and eCommerce

- 5.5.6 Energy and Utilities

- 5.5.7 Others

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 Europe

- 5.6.2.1 United Kingdom

- 5.6.2.2 Germany

- 5.6.2.3 France

- 5.6.2.4 Italy

- 5.6.2.5 Rest of Europe

- 5.6.3 APAC

- 5.6.3.1 China

- 5.6.3.2 Japan

- 5.6.3.3 India

- 5.6.3.4 South Korea

- 5.6.3.5 Rest of APAC

- 5.6.4 Middle East

- 5.6.4.1 Israel

- 5.6.4.2 Saudi Arabia

- 5.6.4.3 United Arab Emirates

- 5.6.4.4 Turkey

- 5.6.4.5 Rest of Middle East

- 5.6.5 Africa

- 5.6.5.1 South Africa

- 5.6.5.2 Egypt

- 5.6.5.3 Rest of Africa

- 5.6.6 South America

- 5.6.6.1 Brazil

- 5.6.6.2 Argentina

- 5.6.6.3 Rest of South America

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Palo Alto Networks

- 6.4.2 Cisco Systems

- 6.4.3 Fortinet

- 6.4.4 Juniper Networks

- 6.4.5 VMware (Broadcom)

- 6.4.6 Check Point Software

- 6.4.7 IBM

- 6.4.8 Oracle

- 6.4.9 Microsoft

- 6.4.10 Trend Micro

- 6.4.11 Huawei

- 6.4.12 Sophos

- 6.4.13 McAfee

- 6.4.14 Splunk

- 6.4.15 Illumio

- 6.4.16 Akamai Technologies

- 6.4.17 Netskope

- 6.4.18 Zscaler

- 6.4.19 Forcepoint

- 6.4.20 Darktrace

- 6.4.21 Proofpoint

7 MARKET OPPORTUNITIES & FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment