|

시장보고서

상품코드

1850244

팔레타이저 : 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Palletizer - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

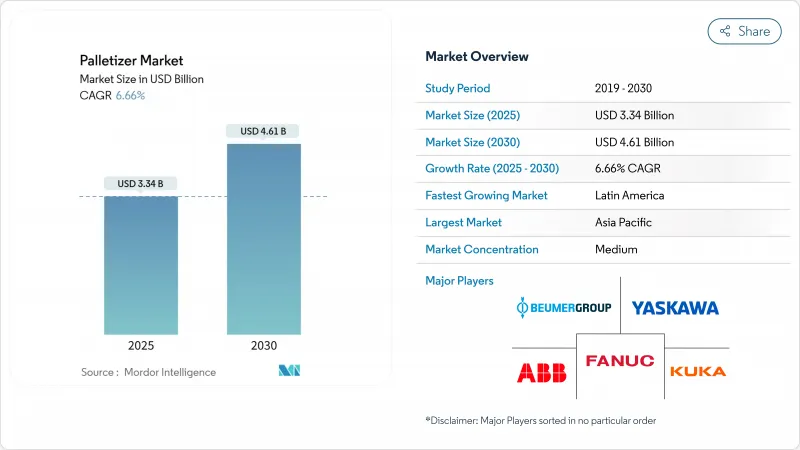

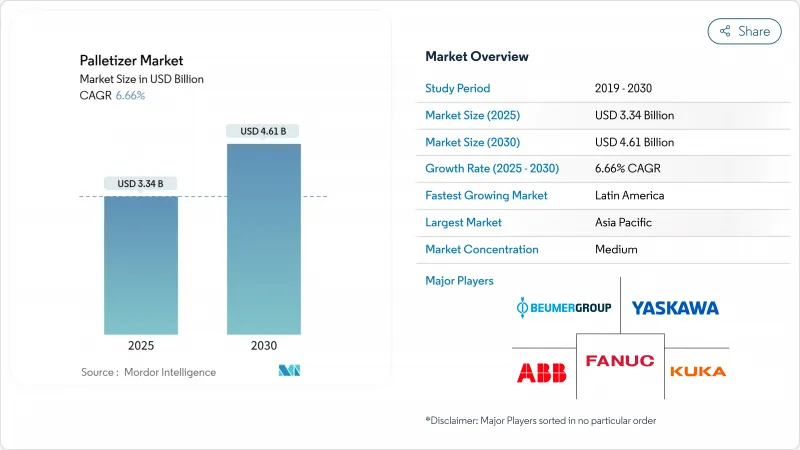

세계의 팔레타이저 시장은 2025년에 33억 4,000만 달러로 평가되었고, 2030년에는 46억 1,000만 달러로 성장할 전망입니다.

이 기세는 수동 팔레트 적재 방식에서 벗어나 노동력 부족을 해결하고 트레일러 활용도를 최적화하며 증가하는 전자상거래 처리량 요구를 충족시키는 자동화 소프트웨어 기반 시스템으로의 지속적인 전환에서 비롯됩니다. 혼합 SKU, AI 기반 팔레타이징 명령이 요구하는 프리미엄, 초기 비용을 낮추는 임대 모델의 급속한 확산, 공간 제약이 있는 공장에서 협동 로봇의 확대되는 매력 등이 성장을 뒷받침합니다. 경쟁 강도는 여전히 중간 수준입니다. 단일 업체의 매출 점유율이 15%를 넘지 않지만, 지역 통합업체들이 로봇을 구독형 또는 서비스형 로봇(RaaS) 계약과 패키지화함에 따라 가격 압박이 나타나고 있습니다. 리쇼어링과 물류 업그레이드가 정부의 세제 혜택과 맞물리면서 남미 지역이 가장 빠른 확장세를 보이고 있습니다. 한편, 중국이 로봇 생산 및 배포 규모에서 우위를 점하고 있어 아시아태평양(APAC) 지역은 물량 측면에서 리더십을 유지하고 있습니다.

세계의 팔레타이저 시장 동향 및 인사이트

전자상거래에서 SKU의 복잡화

풀필먼트 센터는 현재 연간 1,800억 건 이상의 물량을 처리하며, 단일 사이트에서 50,000개 이상의 SKU를 처리하고 있습니다. 이는 기존 소매 허브의 일반적인 다양성의 10배에 달합니다. 고정 패턴 장비로는 이를 따라잡을 수 없어, 루카스 창고 최적화 제품군(Lucas Warehouse Optimization Suite)과 같은 AI 기반 시스템의 도입이 촉진되고 있습니다. 이 시스템은 실시간으로 무게, 파손 가능성 및 적재 가능성을 균형 있게 조정하여 팔레타이징 효율을 15-20% 향상시킵니다. 프리미엄 플랫폼은 30-40% 더 높은 마진을 확보하면서도 최적화된 적재로 빈 트레일러 공간을 최대 30%까지 줄여 총 운송 비용을 여전히 낮춥니다.

창고 자동화를 가속화하는 노동력 부족

중국 내 41개 공장 직종에 걸친 심각한 인력 공백과 북미 창고의 15-20% 공석률은 자동화 투자 회수 기간을 18개월 미만으로 단축시켰습니다. 중견 공장들은 이제 시간당 100개 단위의 소량 생산 라인도 자동화하며, 협업 시스템이 직원들을 더 안전하고 고부가가치 업무로 재배치함에 따라 더 넓은 팔레타이저 시장이 열리고 있습니다.

고하중 로봇 팔의 높은 초기 자본 지출

150kg 이상 등급 설치 비용은 종종 50만 달러를 초과하여 일일 500개 미만 팔레트를 출하하는 제조업체에 장벽이 됩니다. Formic과 같은 서비스형 로봇(RaaS) 선구자들은 월 3,975달러 번들로 이 장벽을 극복하지만, 맞춤화와 소유권 관련 타협점은 여전히 존재합니다.

부문 분석

시간당 1,000케이스 이상의 고속 라인은 검증된 레이어 장치가 필요하여 2024년 기존 기계가 매출의 48%를 유지했습니다. 그러나 팔레타이저 시장은 협동형 장비가 6.2% CAGR로 성장하며 안전 인증을 받은 펜스 없는 운영을 원하는 소규모 부지에서의 신규 투자를 주도하고 있습니다. 로봇식 관절형 암은 중간 성능 계층을 차지하며, 혼합 제품 포트폴리오에 대한 처리량과 전환 유연성 사이의 균형을 맞춥니다. 레이어 포머와 로봇식 피커를 결합한 하이브리드 시스템은 틈새 음료 및 개인용품 셀에서 등장하고 있으나 여전히 비용이 많이 듭니다.

벤더들은 풀스택 생태계로 차별화합니다. 두산의 P-SERIES와 로켓팜의 Pally 소프트웨어 연동은 구축 시간을 단축하고 사용자 자율성을 높입니다. 고객이 독립형 하드웨어보다 단일 공급처 책임성을 우선시함에 따라, 비전 및 시뮬레이션 및 라이프사이클 서비스를 묶어 제공하는 공급업체들은 팔레타이저 시장 내 접근 가능 기회를 확대하고 있습니다.

중형 솔루션이 41.2% 점유율로 우세했으며, 이는 소비재 업계의 50-150kg 박스 선호를 반영합니다. 그러나 대량 운송업체들이 인건비와 운송비 절감을 위해 화물을 통합함에 따라 중대형 시스템 팔레타이저 시장 규모는 연평균 7.4% 성장할 전망입니다. 에너지 효율적인 서보 아키텍처와 고급 안전 스캐너 덕분에 180kg 협동로봇이 직원과 함께 작업할 수 있게 되었으며, 밥스 레드 밀 설치 사례에서 이를 확인할 수 있습니다. 이러한 기능은 중급 제품 대비 40-60%의 가격 상승을 유발하지만, 사용자들은 지게차 이동 감소와 근로자 보상 청구 감소로 프리미엄을 정당화합니다.

50kg 미만의 경량 셀은 청정실 준수 및 정밀도가 단순 작업 능력보다 중요한 제약 및 전자 산업을 대상으로 합니다. 팔레타이저 시장의 이 부문을 겨냥한 공급업체들은 고가치 품목 보호를 위해 클래스 10 등급 인클로저와 진공 그리퍼를 활용하며, 안정적이지만 느린 성장세를 유지하고 있습니다.

지역 분석

아시아태평양(APAC) 지역은 2024년 매출의 38%를 차지했으며, 중국 단독으로 2022년까지 전 세계 신규 로봇 설치량의 52%를 차지했습니다. 국내 공급업체들은 현재 자국 시장의 36%를 확보하며 가격을 낮추고 2차 공장들 사이의 확산을 가속화하고 있습니다. 일본은 전 세계 로봇의 45%를 생산했으며, 393억 달러(437억 달러) 규모의 정부 공급망 펀드 지원을 받아 2024년 물류, 식품, 제약 라인에 73억 5,000만 달러 규모의 주문을 집중시켰습니다. 인도의 생산 연계 인센티브 제도는 자동차 및 제네릭 의약품 공장에서 자동화를 촉진하고 있으나, 기술 격차로 인해 도입 지역별 편차가 여전히 존재합니다.

남미는 2030년까지 8.1%의 가장 강력한 연평균 성장률(CAGR)을 기록할 전망입니다. 브라질의 식품 및 자동차 부문이 수출 규정 준수를 위해 팔레트 조립 자동화를 추진 중이기 때문입니다. 멕시코는 근거리 아웃소싱(nearshoring) 트렌드를 타고 관세 회피 상품을 미국 시장에 공급하며, 북미 안전 규격 인증 로봇 수요를 증대시키고 있습니다. 아르헨티나의 곡물 가공업체들은 거시경제적 변동성에도 불구하고 장거리 해상 운송을 위한 1톤 벌크 백 안정화용 팔레타이저를 설치 중입니다.

북미와 유럽은 용량 증설보다는 교체 수요에 힘입어 안정적인 성장을 보일 전망입니다. 곧 시행될 유럽연합 규정(EU) 2023/1230은 공급업체의 사이버 보안 강화 의무를 부과하여 인증 소프트웨어 스택 보유 업체에 유리하게 작용할 것입니다. 미국 리쇼어링 프로그램은 중소기업 제조업체들이 빈번한 SKU 변경에 대응하고 고령화된 농촌 노동력의 인력 제약을 완화할 수 있는 유연한 협동 로봇을 찾는 가운데 팔레타이저 시장을 부양할 것입니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

목차

제1장 서론

- 조사의 전제조건과 시장의 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 증가하는 전자상거래 SKU의 복잡성

- 노동력 부족이 창고의 자동화를 가속

- 플러그 앤 플레이 협동로봇으로 인한 포장 라인 투자수익률(ROI) 개선

- 로봇 혼합 적재 팔레타이징을 선호하는 FMCG 지속가능성 의무화 급증

- AI 기반 비전 시스템으로 향상된 팔레타이저 가동 시간

- 북미 및 EU 공급망의 회복탄력성 재내국화

- 시장 성장 억제요인

- 중량물 로봇 암의 높은 초기 자본 지출(CAPEX)

- 기존 MES/WMS와의 통합 복잡성

- EU 내 협동 로봇 안전 등급 인증 지연

- 변동성 있는 철강 및 서보 모터 가격으로 인한 투자 회수 기간 연장

- 가치/공급망 분석

- 규제 상황

- 기술의 전망

- Porter's Five Forces

- 공급기업의 협상력

- 구매자의 협상력

- 신규 참가업체의 위협

- 대체품의 위협

- 경쟁 기업간 경쟁 관계

- 가격 분석

제5장 시장 규모와 성장 예측

- 제품 유형별

- 기존 팔레타이저

- 고레벨 팔레타이저

- 저레벨 팔레타이저

- 로봇 팔레타이저

- 직교/갠트리 좌표

- 관절형

- 스칼라

- 협동형(코봇)

- 하이브리드 팔레타이저

- 기존 팔레타이저

- 적재량별

- 경량(50kg 미만)

- 중량(50-150kg)

- 헤비 듀티(150kg 초과)

- 최종 사용자별

- 식품 및 음료

- 의약품

- 퍼스널케어 및 화장품

- 화학약품

- 전자상거래와 3PL

- 기타 산업

- 판매 채널별

- 직접 OEM 판매

- 시스템 통합자

- 애프터마켓 개조 및 업그레이드

- 렌탈 및 임대

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 러시아

- 기타 유럽

- 아시아태평양

- 중국

- 일본

- 인도

- 한국

- 기타 아시아태평양

- 중동 및 아프리카

- 아랍에미리트(UAE)

- 사우디아라비아

- 남아프리카

- 기타 중동 및 아프리카

- 북미

제6장 경쟁 구도

- 시장 집중도

- 전략적 동향

- 시장 점유율 분석

- 기업 프로파일

- ABB Ltd.

- FANUC Corp.

- KUKA AG

- Yaskawa Electric Corp.

- BEUMER Group GmbH and Co. KG

- Honeywell Intelligrated

- Krones AG

- Sidel Group

- ABC Packaging

- Schneider Packaging

- Barry-Wehmiller(BW Packaging)

- Premier Tech Chronos

- MMCI Robotics

- Columbia Machine

- Fuji Yusoki

- Brenton Engineering

- Kawasaki Robotics

- Okura Yusoki

- Regal Rexnord Automation

- Sealed Air AUTOBAG

제7장 시장 기회와 장래의 전망

HBR 25.11.19The global palletizer market stands at USD 3.34 billion in 2025 and is projected to reach USD 4.61 billion by 2030, reflecting a 6.66% CAGR over the forecast period.

Momentum comes from the sustained shift away from manual pallet building toward automated, software-driven systems that resolve labor shortages, optimize trailer utilization, and meet rising e-commerce throughput requirements. Growth is reinforced by the premium that mixed-SKU, AI-enabled palletizing commands, the rapid spread of rental models that lower upfront costs, and the expanding appeal of collaborative robots in space-constrained factories. Competitive intensity remains moderate: no single player holds more than 15% revenue, yet pricing pressure surfaces as regional integrators package robots with subscription or robotics-as-a-service contracts. South America registers the fastest regional expansion as reshoring and logistics upgrades intersect with government tax incentives; meanwhile APAC maintains volume leadership due to China's scale in robot production and deployme

Global Palletizer Market Trends and Insights

Growing e-commerce SKU complexity

Fulfilment centres now handle volumes that exceed 180 billion cases yearly, with single sites processing more than 50,000 SKUs-ten times the diversity typical of legacy retail hubs.Fixed-pattern equipment cannot keep up, prompting adoption of AI-powered systems such as the Lucas Warehouse Optimization Suite, which lifts palletizing efficiency 15-20% by balancing weight, fragility, and stackability in real time. Premium platforms fetch 30-40% higher margins but still lower total shipping cost as optimized loads cut empty trailer space by up to 30%.

Labor shortages accelerating warehouse automation

Critical staffing gaps across 41 factory occupations in China and 15-20% vacancy rates in North American warehouses have compressed automation payback to under 18 months. Mid-market plants now automate runs of just 100 units per hour, unlocking a broader palletizer market as collaborative systems redeploy employees to safer, higher-value roles.

High upfront CAPEX for heavy-payload robotic arms

Installations rated above 150 kg often top USD 500,000, a hurdle for manufacturers shipping fewer than 500 pallets daily. Robotics-as-a-service pioneers such as Formic counter this barrier with USD 3,975 monthly bundles, yet tradeoffs around customisation and ownership persist.

Other drivers and restraints analyzed in the detailed report include:

- Packaging-line ROI improvements from plug-and-play cobots

- Surge in FMCG sustainability mandates favouring robotic mixed-load palletizing

- Integration complexity with legacy MES/WMS

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Conventional machines retained 48% revenue in 2024 as high-speed lines exceeding 1,000 cases per hour depend on proven layer devices. Yet the palletizer market sees collaborative units outpace at 6.2% CAGR, capturing greenfield investments in small-footprint sites that crave safety-certified, fence-free operation. Robotic articulated arms occupy the mid-performance tier, balancing throughput against changeover flexibility for mixed product portfolios. Hybrid systems, blending layer formers with robotic pickers, emerge in niche beverage and personal-care cells but remain cost-intensive.

Vendors differentiate through full-stack ecosystems: Doosan's P-SERIES coupled with Rocketfarm's Pally software reduces deployment time and elevates user autonomy. As customers prioritise single-source accountability over stand-alone hardware, suppliers bundling vision, simulation, and lifecycle services widen addressable opportunities inside the palletizer market.

Medium-duty solutions dominated with 41.2% share, reflecting consumer goods' bias toward 50-150 kg boxes. However the palletizer market size for heavy-duty systems is slated to expand at a 7.4% CAGR as bulk shippers consolidate loads to curb labour and freight costs. Energy-efficient servo architectures and advanced safety scanners now let 180 kg cobots operate alongside staff, as seen in Bob's Red Mill installations. These capabilities command 40-60% price uplifts compared with mid-tier peers, yet users justify the premium through reduced forklift moves and lower workers' compensation claims.

Light-duty cells under 50 kg address pharmaceuticals and electronics, where cleanroom compliance and precision trump brute force. Vendors targeting this end of the palletizer market leverage class-10-rated enclosures and vacuum grippers to protect high-value items, maintaining a stable but slower growth profile.

The Palletizer Market is Segmented by Product (Conventional Palletizer, Robotic Palletizer), by Payload Capacity (Light-Duty, Medium-Duty, and Heavy-Duty), by End-User Vertical (Food & Beverages, Pharmaceuticals, Chemicals, E-Commerce and 3PL, and More), by Sales Channel (Direct OEM Sales, System Integrators, and More) and by Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

APAC held 38% of 2024 revenue, with China alone installing 52% of new global robots by 2022. Domestic suppliers now secure 36% of their home market, pushing price points lower and accelerating diffusion among tier-two factories. Japan built 45% of the world's robots and channelled USD 7.35 billion in 2024 orders into logistics, food, and pharma lines, backed by a USD 39.3 billion (USD 43.7 billion) government supply-chain fund . India's Production-Linked Incentive schemes spark automation across automotive and generics plants, though adoption pockets remain uneven due to skill gaps.

South America records the strongest 8.1% CAGR trajectory to 2030 as Brazil's food and auto sectors automate pallet building for export compliance. Mexico rides near-shoring trends to supply the US market with tariff-proof goods, intensifying demand for robots certified to North American safety codes. Argentina's grain processors install palletizers that stabilise 1-tonne bulk bags for long ocean voyages despite macroeconomic volatility.

North America and Europe show measured growth driven by replacement rather than capacity additions. Upcoming Regulation (EU) 2023/1230 compels vendors to harden cybersecurity, advantaging those with certified software stacks. US reshoring programs lift the palletizer market as SMB manufacturers seek flexible cobots that accommodate frequent SKU changeovers and mitigate labour constraints in ageing rural workforces.

- ABB Ltd.

- FANUC Corp.

- KUKA AG

- Yaskawa Electric Corp.

- BEUMER Group GmbH and Co. KG

- Honeywell Intelligrated

- Krones AG

- Sidel Group

- A-B-C Packaging

- Schneider Packaging

- Barry-Wehmiller (BW Packaging)

- Premier Tech Chronos

- MMCI Robotics

- Columbia Machine

- Fuji Yusoki

- Brenton Engineering

- Kawasaki Robotics

- Okura Yusoki

- Regal Rexnord Automation

- Sealed Air AUTOBAG

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing e-commerce SKU complexity

- 4.2.2 Labor shortages accelerating warehouse automation

- 4.2.3 Packaging-line ROI improvements from plug-and-play cobots

- 4.2.4 Surge in FMCG sustainability mandates favouring robotic mixed-load palletizing

- 4.2.5 AI-driven vision systems boosting palletizer uptime

- 4.2.6 Resilience re-shoring of supply chains in North America and EU

- 4.3 Market Restraints

- 4.3.1 High upfront CAPEX for heavy-payload robotic arms

- 4.3.2 Integration complexity with legacy MES/WMS

- 4.3.3 Safety-rating certification delays for cobots in EU

- 4.3.4 Volatile steel & servo-motor prices widening payback periods

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Pricing Analysis

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Product Type

- 5.1.1 Conventional Palletizer

- 5.1.1.1 High-Level Palletizer

- 5.1.1.2 Low-Level Palletizer

- 5.1.2 Robotic Palletizer

- 5.1.2.1 Cartesian/Gantry

- 5.1.2.2 Articulated

- 5.1.2.3 SCARA

- 5.1.2.4 Collaborative (Cobot)

- 5.1.3 Hybrid Palletizer

- 5.1.1 Conventional Palletizer

- 5.2 By Payload Capacity

- 5.2.1 Light-Duty (<50 kg)

- 5.2.2 Medium-Duty (50-150 kg)

- 5.2.3 Heavy-Duty (>150 kg)

- 5.3 By End-user Vertical

- 5.3.1 Food & Beverages

- 5.3.2 Pharmaceuticals

- 5.3.3 Personal Care and Cosmetics

- 5.3.4 Chemicals

- 5.3.5 E-commerce and 3PL

- 5.3.6 Other Verticals

- 5.4 By Sales Channel

- 5.4.1 Direct OEM Sales

- 5.4.2 System Integrators

- 5.4.3 After-market Retrofits and Upgrades

- 5.4.4 Rental / Leasing

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Russia

- 5.5.3.6 Rest of Europe

- 5.5.4 APAC

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 India

- 5.5.4.4 South Korea

- 5.5.4.5 Rest of APAC

- 5.5.5 Middle East & Africa

- 5.5.5.1 United Arab Emirates

- 5.5.5.2 Saudi Arabia

- 5.5.5.3 South Africa

- 5.5.5.4 Rest of Middle East and Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles

- 6.4.1 ABB Ltd.

- 6.4.2 FANUC Corp.

- 6.4.3 KUKA AG

- 6.4.4 Yaskawa Electric Corp.

- 6.4.5 BEUMER Group GmbH and Co. KG

- 6.4.6 Honeywell Intelligrated

- 6.4.7 Krones AG

- 6.4.8 Sidel Group

- 6.4.9 A-B-C Packaging

- 6.4.10 Schneider Packaging

- 6.4.11 Barry-Wehmiller (BW Packaging)

- 6.4.12 Premier Tech Chronos

- 6.4.13 MMCI Robotics

- 6.4.14 Columbia Machine

- 6.4.15 Fuji Yusoki

- 6.4.16 Brenton Engineering

- 6.4.17 Kawasaki Robotics

- 6.4.18 Okura Yusoki

- 6.4.19 Regal Rexnord Automation

- 6.4.20 Sealed Air AUTOBAG

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment